The provisions governing unexplained investments and credits under Sections 68 to 69D of the Income-tax Act (and their counterparts in the Income-tax Act, 2025) empower tax authorities to tax unexplained cash credits, investments, money, expenditure, or hundi transactions where the assessee fails to satisfactorily explain their nature and source. Section 115BBE imposes a special, punitive tax regime on such deemed incomes, with rates escalating from 30% earlier to an effective 78%, and even up to 137% including penalty, post-AY 2017–18. However, extensive judicial precedents show that these provisions are frequently misapplied. Courts and tribunals have consistently held that additions cannot be made merely on suspicion, dumb documents, retracted statements, procedural lapses, or without rejecting books of account. Where income is explained, recorded, taxed under normal provisions, or represents business receipts, double taxation under Section 115BBE is impermissible. The jurisprudence underscores that Sections 68–69D require strict factual proof, proper enquiry, and adherence to natural justice, limiting arbitrary taxation.

TAXATION OF UNEXPLAINED INVESTMENTS / CREDITS U/S 115BBE

Section 68 (S 102 I T Act 2025) – Cash Credits:

- Any sum credited in the books of assessee and

- The Assessee offers no explanation or

- Explanation offered is not satisfactory

- Then, such credit may be charged to income tax as income of that year u/s. 68

Provisions of Section 68 (S 102 I T Act 2025):

Section 68 applies not only to cash transaction but also to amounts received by cheque or draft:

- The words used are “Any sum credited in the books of assessee maintained”

- The sum of money is not restricted to cash transactions only.

- Headnote to 68 refers to cash credits is not sufficient to support the view.

- 68 is unambiguous & the sum referred in the section would include “the sum of money by whatever mode received”

Source of Source also to be explained:

- Where the assessee is a company (not a company where public are substantially interested) & sum credited consists of share application money, share capital, share premium or any amount

- In addition to explanation offered by assessee-company, “explanation about nature & source also to be offered by the person in whose name such sum is recorded in the books of assessee”

- Such explanation should be found to be satisfactory in the opinion of

Finance Act 2022 has inserted the following proviso u/s. 68 (applicable w.e.f. AY 2023-24):

- If the sum credited consists of “loan or borrowing”

- In addition to explanation offered by assessee, “explanation about nature &source to be explained by the person in whose name such sum is recorded in the books of assessee”

- Such explanation should be found to be satisfactory in the opinion of AO

Section 69 (S 103 I T Act 2025) – Unexplained Investments:

- In any Y., the assessee had made investments which are not disclosed in the books, if any maintained

- No explanation about nature & source or

- Explanation offered is not satisfactory

- Then, value of such investments shall be deemed to be income of that year u/s. 69

Section 69A (S 104 I T Act 2025) – Unexplained Money, etc:

- In any Y., the assessee is found to be the owner of Money / Bullion / Jewellery / Other valuable article

- Not recorded in Books of accounts, if any maintained and

- No explanation about nature or source of such acquisition or

- Explanation offered is not satisfactory

- Such money etc., may be deemed to be income of that year u/s. 69A.

Section 69B (S 103 & 104 I T Act 2025) – Investments, etc., not fully disclosed in Books:

- The assessee had made investments or found to be the owner of Money / Bullion / Jewellery / other valuable article

- The finds amount expended exceeds the amount recorded in Books maintained

- No explanation about such excess amount or

- Explanation offered is not satisfactory

- Such excess may be deemed to be income of that year u/s.

Section 69C (S 105 I T Act 2025) – Unexplained Expenditure:

- In any year, the taxpayer has incurred expenditure

- No explanation about source of expenditure or part thereof or

- Explanation offered is not satisfactory

- Such amount covered by expenditure or part thereof may be deemed as income of that year u/s. 69C.

- Such unexplained expenditure shall not be allowed as deduction under any head of

Section 69D (S 106 I T Act 2025) – Amount borrowed or repaid on hundi:

- Any amount borrowed from / repaid to a person through hundi otherwise than by account-payee

- Such shall be deemed to be income of the person borrowing / repaying the amount.

- Treated as income for the year in which it was borrowed /

- If amt borrowed is taxed u/s. 69D, the same cannot be taxed again while

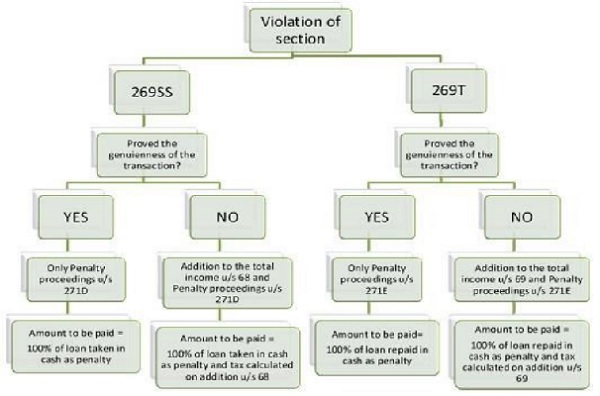

Analysis of Sec 69D & 269SS/T

.

Section 115BBE:

- Introducedin the Finance Act, 2012 dealing with special rate of tax for sec 68 to 69D @30% e.f. 01.04.2013.

- Later amended by Taxation Laws (Second Amendment) Act, 2016 15.12.2016 w.e.f. A.Y. 2017-18:

- Tax shall be calculated @ 60% on unexplained income u/s. 68 to 69D

- Further increased by Surcharge @ 25% on the tax and Cess of 4% of the Tax and SC

- No deduction in respect of expenditure / allowance / set off of any loss in computing income u/s. 68 to 69D

Penalty applicable to Income chargeable to tax u/s. 115BBE Section 271AAC:

- Penalty@ 10% on tax payable u/s. 115BBE shall be imposed if such income is not reflected in Return of Income w.e.f. Y. 2017-18.

- In such a case the tax burden including penalty will come to 25% (excluding interest)

Penalty u/s. 271AAA, 271AAB

| 271AAA @10% | Applicable to cases where Search has been initiated u/s. 132 “On or after 01.06.2007 but before 01.07.2012” |

| 271AAB (1) @10% | Applicable to cases wherein Undisclosed Income found during Search which has been initiated “on or after 01.07.2012 but before 15.12.2016” |

| 271AAB (1A) @30% or 60% | Applicable to cases wherein Undisclosed Income found during Search which has been initiated “on or after 15.12.2016” |

Penalty u s Section 271AAB (1A):

- 30%of Undisclosed income, if

- Assessee admitted undisclosed income

- Paid tax before specified date

- Filed ROI by declaring such undisclosed income

- 60%of Undisclosed income in any other

Tax Rate under Section 115BBE:

Before AY 2017-18:

- Flat 30% tax rateon unexplained income (excluding surcharge & cess).

After AY 2017-18 (Post-Demonetization Amendment):

- 60% tax rate on unexplained income.

- 25% surcharge on tax (i.e., 15% of income).

- 4% cess on tax & surcharge.

- Effective tax rate = 78%.

If unexplained income is not voluntarily declared in ITR & is found by the Department, an additional penalty of 10% is imposed under Section 271AAC. Tax @ 60% + Surcharge @ 25% + Cess @ 4% + Penalty @ 10% = 137% tax liability.

This means if you deposit ₹1 crore unexplained cash, your tax & penalty can be ₹1.37 crore! In addition interest @ 1% p.m. is payable

Section 115BBE is not just a tax provision but a financial warning with 78% to 137% tax liability where we can play a key role in ensuring clients don’t fall into this costly trap.

THE FORGOING SECTIONS ARE INDISCRIMINATELY USED TO HARASS THE ASSESSEES BY TAXING AT 60% INSTEAD OF THE NORMAL RATES AND MAJORITY OF THE ORDERS ARE STRUCTED DOWN IN APPEALS, WHICH IS EVIDENT FROM THE FOLLOWING LIST OF CASE LAWS, WHICH ARE GIVEN TOPIC-WISE (these sections are continued in the Income Tax Act 2025 and there is no relief in the Income Tax Bill 2025 also):

Excess stock found during search / survey cannot be treated as deemed income u/s. 69/69B:

- Excess stock found during search – Addition made u/s 69/69B – unexplained investments not fully disclosed in

- Assessee stated that excess stock got accumulated out of regular unaccounted business income only & “declared such income in ITR post search”.

- ITAT held that provisions of Sec. 115BBE is not applicable on the excess stock surrendered as business income and the same cannot be treated as unexplained

[1. ACIT Vs Shri Anoop Neema- ITA No. 05/Ind/2020

2. Bunty Kumar Vs ACIT – ITA No. 215/Asr/2023

3. Vijay Shriram Gundale Vs ACIT – ITA No. 79/Pun 2023

4. Fathima Jewellers Vs DCIT – ITA 66/Chny/2023

5. CITVs Bajargan Traders c/o. Kalani & Co – ITA 258/2017]

6. A P Knit Fab Vs DCIT (ITAT Chandigarh)

7. Revathi Modern Rice Mill Vs ACIT]

Once penalty u/s 271AAB applied, invoking 115BBE unjustified:

- Filed ROI by including surrendered income – Penalty proceedings u/s. 271AAB(1)(A) was

- AO passed order by adding 5,52,241/- as unexplained jewellery in addition to undisclosed income.

- ITAT held that assessee filed ROI in accordance with penal provisions of 271AAB. “Invoking sec. 115BBE is against the law & also against principle of natural justice”.

[Sandeep Sethi Vs DCIT- ITA No.115/JP/2022]

Additional Income once accepted cannot be later rectified & taxed u/s. 115BBE:

- Additional income was found during search operation – Income was declared, and taxes were paid.

- Surrendered income was treated as Normal business income by AO.

- Dissatisfied, CIT passed “revision order u/s. 263/rectification order u/s. 154” and taxed @ 60% u/s.

- ITAT held that the provisions of 115BBE cannot be invoked via rectification / revision order and treated the surrendered income as normal business income.

[1. Yogesh Kumar Vs PCIT- ITA No. 589/Del/2022

2. Anjanee Vijetha Kasturi ACIT- ITA No. 196/Hyd/2023

3. Sharp Chucks and Machines Ltd Vs. DCIT-ITA No. 169/Asr/2023]

ITAT deletes addition made during search & seizure solely on basis of WhatsApp Chat:

Based on WhatsApp chats, salary paid in cash was found during search operation – Addition was made u/s. 69C.

- Assessee was not given an opportunity of being heard.

- ITA Theld that WhatsApp chats are not valid evidence – directed the AO to delete the addition.

[Designers Point (India) P. Ltd Vs ACIT – ITA No. 2517/Del/2022]

Additional Income cannot be treated as unexplained expenditure u/s. 69C to invoke Sec. 115BBE:

- Loose sheets representing cash payments around 5 Crores was found during search – The same was declared in ITR under the head “PGBP”

- AO rejected & treated the same u/s. 69C and brought to tax u/s. 115BBE.

- ITAT held that “AO should not have treated it as unexplained expenditure without making any further enquiry to disprove the evidence” & directed the AO to tax such income under normal provisions.

[Devender Rao Gaurkanti Vs. ACIT- ITA No. 439/Hyd/2022]

No Addition u/s. 68 if sales properly recorded in Books:

Cash deposits were made after the announcement of demonetization beingopening cash balance & cash sales.

- The AO accepted the books but treated the sales as

- The Tribunal concluded that any addition by treating sales as bogus without rejecting books is unjust, unfair & bad in law.

[ACIT Vs Shri Nitin Sankhla- ITA No.98/RPR/2020]

Addition of presumptive income as undisclosed income u/s. 68 is not tenable:

ROI for the A.Y. 2015-16 was not filed – Form 26AS displayed income u/s. 194J.

- In response to notice u/s. 148, the ROI was filed by computing income u/s. 44AD @ 8%

- Not being satisfied AO treated the income as undisclosed income u/s. 68.

- ITAT held that adopting provisions of sec.44AD is permissible – directed the AOto delete the addition.

[1. Mehjabeen Masood Khan Vs ITO- ITA No.766/MUM/2023

2. CIT v/s Surinder Pal Anand, Surinder Pal Anand – ITA No.156/PUN/2010

3. DCIT Vs Kalpesh Kantilal Gada (ITAT Mumbai)]

No Addition u/s. 68 if depositors are proved:

Cash deposited by a companyto the bank account of assessee was treated u/s.68.

- Assessee proved that such money was interest bearing loan and received through proper banking channel.

- ITAT held that the assessee has proved the identity of the creditor & genuineness of the Hence deleted the addition made u/s. 68.

[Poddar Realtors Vs ITO- ITA No.265/Kol/2023]

Section 68 inapplicable in the absence of maintenance of books of accounts:

- Cash deposited into bank account was treated u/s. 68 – Which was from Agriculture activity & OB of cash.

- Assessee had not maintained books of accounts, and the ROI was not filed as the TI is below the slab.

- The ITAT held that mere possession of passbook cannot be treated as books of accounts & addition u/s. 68 is unsustainable.

[1. Sh. Satbir Singh Bhullar Vs ITO- ITA No.258/Asr/2022

2. Ishtiaq Ahmad Rather Vs ITO (ITAT Amritsar)

3. Bhavanji Jugaji Thakor Vs ITO (ITAT Ahmedabad)

4. Rahul Goel vs ITO (ITAT Delhi)]

ITAT deletes addition of cash deposits during demonetization period:

- Cash deposited during demonetization was treated u/s. 68 – But the same was reflected in P&L as cash sales.

- Cashbooks, details of sales, stock registers, VAT returns filed were available and were submitted.

- The ITAT held that the assessee has provided substantial information & such additionwould amount to double taxation once as sales & again as unexplained credit and hence the addition deleted.

[1. DCIT Vs M/s. Kundan Jewellers P.Ltd- ITA No.1035/Mum/2022

2. ACIT Vs Himachal Fibres Limited- ITA No. 927/Del/2023

3. Ayesha Steels (P) Ltd Vs ITO (ITAT Delhi)]

No Addition u/s. 68 if genuineness, identity & creditworthiness of creditors proved:

AO treated unsecured loans as unexplained credits u/s. 68 and passed order u/s.143(2).

- Bank statements, ledgers, PAN, Confirmation from lenders and other necessary documentary evidence were submitted.

- ITAT held that loans were clearly visible in bank statements and the assessee provedthe genuineness, identity & creditworthiness of the transaction, directed the AO to delete the addition.

[1. Vachitra Builders P.Ltd Vs ITO- ITA No. 8148/DEL/2019

2. DCIT VsShri Jayesh R. Thakkar – ITA No. 34 07/Ahd/2015

3. Dharmvir Merchandise Pvt. Ltd. Vs ITO (ITAT Kolkata)

4. CIT vs P. Mohankala (2007) 291 ITR 278 (SC)

5. CIT vs Orissa Corporation (P) Ltd. (1986) 159 ITR 78 (SC)

6. DCIT Vs Smt. Denisha Rajendra Keshwani (ITAT Ahmedabad)

7. ACIT vs Prayag Polytech Pvt. Ltd.(ITAT Delhi)]

Addition u/s. 68 merely based on assumption / suspicion without cogent evidence:

- Exemption was claimed u/s. 10(38) on LTCG from sale of shares. (Not in effect)

- AO had suspicion that the share prices were rigged and sold at a higher price to arrive at tax free LTCG u/s. 10(38) – entire sale proceeds were treated u/s. 68

- ITAT held that addition by AO merely based on assumption/suspicion is unsustainable.

[1. Abhishek Doshi Vs ACIT- ITA No. 3122/MUM/2022

2. ITO Vs Indus Realty Pvt. Limited (ITAT Kolkata)

3. Himanshu Botadara Vs ITO (ITAT Indore) – I.T.A. No. 155 & 156/Ind/2023]

Addition u/s. 68 unjustified as Trade payable duly explained:

- The Increase in Trade payable compared to previous year were treated u/s. 68.

- The funds were received from one company and paid to other through banking channels; the same were properly accounted.

- The ITAT held that additions u/s. 68 is unjustified and quashed the order passed by AO.

[ITO Vs Shri Mahalakshmi Metal- ITA No. 179/Chny/2020]

Addition u/s. 68 unsustainable as revenue failed to discharge its onus:

- Loans were given to assessee as soon as cash was deposited in the lender’s bank a/c.

- AO held that assessee’s own undisclosed cash brought in the guise of loan & also it is not possible for a company with turnover of 3.95 lacs to advance huge loan, hence added as income of the assessee.

- ITAT held assessee discharged its primary onus, further onus was on the revenueto make further enquiry & turnover alone cannot be considered as source of loan

- Addition u/s. 68 couldn’t be

[Sasi Enterprises Vs DCIT- ITA No. 843/Chny/2018

ACIT vs Amal Corporation ITAT Mumbai, ITA No. 674/Mum/2024, order dated 14.10.2024]

Addition u/s. 69 unjustified on Late demonetisation cash deposit

- Cash deposited after the time limit during demonetisation period were treated u/s. 69 – Cash flow statements and Month wise cash deposits were submitted.

- ITAT found that AO & CIT failed to adequately respond to these submissions and the assessee is a farmer with no other significant sources of income.

- ITAT concluded that “delay in deposit cannot be a valid basis for addition” and directed the AO to delete such addition.

[Rajkumar Vs ACIT- ITA No. 378/DEL/2021]

Addition u/s. 69 untenable as source of investment duly explained

- The AO has made the entire credits in bank account as unexplained investment u/s. 69

- The Assessee engaged in the business of real estate & no other substantial incomeand the credits in bank account represents gross receipts of the

- The ITAT concluded that addition u/s. 69 towards unexplained investment untenable as source of investment stands sufficiently explained.

[DCIT Vs Sukhbir Shokeen- ITA No. 1477/DEL/2020]

No Addition u/s. 69 in case of investments out of past savings:

- Entire credit in bank a/c were treated u/s. 69 of IT act – Amount deposited were from Agriculture activities and past savings.

- The ITAT concluded that she had not made any unexplained investment and investments out of past savings or loans taken from relatives cannot be made as addition u/s.

[Anjali Roy Vs ITO- ITA No. 516/KOL/2022]

Addition u/s. 69C unsustainable as nature and source explained:

- Documents were found during search operations – where excess salary were paid in cheques and received the excess in cash.

- Office assistant stated that money was spent for day-to-day

- AO rejected and made additions towards as unexplained expenditure u/s. 69C since expenditure incurred outside the

- ITAT stated that source of money and nature of expenditure is very clear, hence the question of making additions towards refund money as unexplained expenditure u/s. 69C does not arise.

[Jeppiaar Educational Trust Vs ACIT- ITA No. 480,481,482&483/Chny/2023]

Addition made u/s. 69A due to non-filing of ROI

- Cash deposits were treated u/s. 69A due to non – filing of ROI. – Firm was dissolved but due to inadvertent mistake PAN of the firm still exists in Bank a/c.

- Assessee was carrying on business in the same name as a proprietorship concern & the deposits were duly declared in its ROI.

- The AO rejected the contention of Assessee and appeal was made against the order passed by AO.

- Looking into the facts that order passed against the non-existing entity & also rejecting the responses of assessee, the ITAT directed the AO to delete the impugned

[M/s. Kishan Singh & Associates Vs ITO- ITA No.1688/DEL/2021]

Calculating Tax u/s. 115BBE the sums which are not taxable under Sections 68 to 69D:

- Delayed deposits of Employee contribution were taxed u/s. 115BBE.

- The Assessee appealed & contended that Sec. 115BBE applies only when sections68 to 69A are

- The ITAT directed the AO to delete the addition as the case does not come underthe mandate of 115BBE.

[M/s. Apcer Life Sciences India P. Ltd Vs. NFAC Delhi- ITA No. 2882/Mum/2022]

115BBE Amendment cannot be applied to search conducted prior to effective date (01.04.2017)

- Excess stock found during search were treated as Business Income by assessee.

- AOtreated such stock as “Unexplained Investments” u/s. 69B and applied amended provisions of sec. 115BBE tax @ 60%

- ITAT held that addition made by AO by invoking sec 115BBE is unsustainable asit came into force only on 04.2017 & allowed the appeal.

[Samir Shantilal Mehta Vs ACIT- ITA No.42/SRT/2022]

Set off of loss denied to invoke section 115BBE:

The AO disallowed set off carry forwarded losses by way of invoking theprovisions of section 115BBE. AO did not disallow in the assessment order u/s. 143(3) but added in subsequent proceedings u/s. 154.

- AO did not make any addition u/s. 68 to 69D, therefore there was no question ofdisallowance of set off of

- The A.Y. involved was 2013-14 & the provisions of denial of set off of losses inrespect of income u/s. 68 to 69D introduced vide Finance Act,

- Based on these grounds, the ITAT Chandigarh directed the AO to allow set off of

[M/s. Mahaluxmi Food Industries Vs. ITO- ITA Nos.711/CHD/2022]

Addition made by using Third party statements without allowing cross examination:

- Notice was issued u/s. 148 without proper enquiry – Assessee proved the source of cash deposit in his bank account

- AO rejected the contention and made addition u/s. 68 by not allowing the opportunity of cross-examination of a third person.

- The ITAT held that third-party statements cannot be used against the assessee unless and until the opportunity of cross-examination is afforded to the assessee, which was not followed by the revenue and deleted the addition.

[1. Shiv Charan Vs. ITO- ITA No. 6003/Del/2017

2. DCIT Vs.Shri Jayesh R. Thakkar – ITA No. 3407/Ahd/2015]

No Addition u/s. 68 if amount does not appear in books:

- The AO made addition u/s. 68 where no such income was credited in the books of account maintained and audited.

- The Assessee neither earned nor received such interest income during the year and no TDS has been claimed.

- The ITAT held that addition made u/s. 68 is not sustainable, if amount doesn’t appear in the books of account.

[Balaji Tirupati Buildcon Ltd., Vs. ITO- ITA No. 7582/Del/2019]

Purchase & Sale of shares through demat account cannot be declared as unexplained income u/s. 68:

- Shares are purchased and sold through demat account and all transactions are carried through banking channel.

- The AO did not agree with the submissions and declared the sale value as unexplained income u/s.68.

- The ITAT dismissed the appeal filed by the revenue that AO was not justified in assessing the sale value.

[ITO Vs. Sanjay Mahabir Maheshka – ITA No. 6168,9/Mum/2019]

Purchase reflected in books cannot be treated as unexplained income:

- The AO treated purchase of jewellery as unexplained investment u/s. 69 and sale of shares as unexplained cash credit u/s. 68.

- The Assessee submitted that these transactions were reflected in the books of account and payment was made through proper banking channel.

- The ITAT allowed both the appeals filed by the assessee and set aside the order passed by AO.

[Vimal Kishore Shah Vs. ITO – ITA No. 1498/Mum/2023]

No addition u/s 69 for cash withdrawal & redeposit in unsuccessful property deal:

- Additions were made u/s. 69 – That assessee failed to explain cash deposits &

- Assessee held that deposits comprised transfer from his grandfather’s bank account, withdrawal for property purchase & redeposit when property deal failed.

- The ITAT held that the authorities did not take into the evidence presented & treated the addition as unjustified.

[Inderjeet Vs. ITO – ITA No. 2646/Del/2018]

Addition u/s 69C based on dumb documents is unsustainable:

- Documents were found during search operation – Addition was made u/s. 69C.

- AO said that all the distilleries of the assessee were contributing certain cash being used as bribe to pay certain public servants/bureaucrats/politicians.

- ITAT held that these documents only having hearsay value or the documents are dumb which cannot be relied upon and not sustainable in law.

[DCM Shriram Industries Vs. DCIT – ITA No. 374/Del/2015]

Assessment of surrendered income as unexplained u/s. 69 is invalid:

- The AO interpreted the voluntary surrender of 30 Lakhs as unexplained income u/s. 69.

- Further levied tax @ 60% u/s. 115BBE – Taxes were paid @ 30% on the voluntarily surrendered amount

- ITAT held that voluntary surrenders should not be misconstrued without concrete proof and the invocation of this section was

[1. Jaspreet Singh Mauj Vs. DCIT/ACIT – ITA No. 755/CHD/2022

2. Parmod Singla Vs ACIT (ITAT Chandigarh)]

ITAT deletes addition u/s. 69B as it cannot be proved that crane purchased from undisclosed income:

- Difference between agreement price and book value – Addition was made u/s. 69B.

- Cost was exaggerated to secure a higher banking loan facility.

- ITAT addition u/s. 69B was unjustified, as it could not be proven that purchases were made from undisclosed income.

[KVR Infra Vs ACIT – ITA No. 323/MUM/2023]

ITAT deletes the addition of cash deposits as unexplained cash credits u/s. 68:

Assessee being an NRI has not filed ROI – Cash were deposited in bank accounts which were from the previous withdrawals.

- The cash deposits were added as unexplained cash credits u/s. 68 and penalty u/s.271(i)(c) [100% of Tax evaded] was separately initiated for concealment of income.

- ITAT concluded that there is no reason to make addition – asthe assessee can demonstrate cash withdrawal and availability of cash out of such

[Smt. Madhuvalli Vs ADIT – ITA No. 294/Hyd/2023]

No Addition u/s. 69A if all possible evidences are available with the assessee in support of its claim:

- Cash Deposited during demonetization period were treated u/s. 69A.

- The sources of deposits were cash withdrawal frombank and capital withdrawal from LLP and evidence were submitted. However, AO rejected the

- ITAT stated that when assessee has all the possible evidence, they cannot be brushedaside based on surmises and guesswork and deleted the addition made by

[1. Hasmukh Kanjibhai Tadhani Vs ITO – ITA No. 19/SRT/2023

2. S. Tulasidoss Nedunselian Vs ACIT – ITA No. 466 & 472/Chny/2020]

ITAT directs AO to accept 50% Demonetized Currency as Sale Proceeds:

- Specified bank notes were deposited during demonetization period. AO contented that appellant should not have accepted after specified date notified by Govt.

- Since the appellant is a distributor & primarily deals with cash transactions, ITAT directed the AO to accept 50% of cash deposits as sale proceeds and remaining 50% as unexplained

[J. Kalappa Naidu Sons Vs ITO– ITA No. 252/Chny/2023]

50 times higher assessment without considering request of petitioner for personal hearing, HC quashed Order:

- Additions were made under sections 68, 69A, 145(3), 36(1)(iii)

- The Assessee made a request for personal hearing through video conferencing more than four

- Assessment was rejected and additions were made upto 50 times the income under SCN.

- The HC quashed the order, allowing the NeAC to issue fresh notice, directing adherence to proper procedures and the opportunity for a personal hearing.

[Margita Infra Vs National E-Assessment- Centre Delhi– R/Special Civil Application No. 15756 of 2021]

No Addition u/s. 68 in absence of actual receipt of money and for accounting mistake:

- Mismatch between sum received and confirmed by party – Addition was made u/s. 68.

- The explanation given by assessee that it was an accounting error was not accepted bythe AO.

- ITAT held that differences in accounts were due to an accounting error and there is noactual receipt of money, hence the question of making addition u/s 68 will not

[Mehboob Amirali Kamdar Vs ITO – ITA No. 1969/Mum/2023]

Addition u/s. 68 based on Retracted Statement unsustainable:

- Share Application was received from a company which is engaged in providing accommodation entries.

- Necessary documents were submitted – AO was not satisfied with the genuineness and only on key person’s statement which was retracted

- ITAT held that addition u/s. 68 merely based on statement of the key person which was retracted subsequently unsustainable as genuineness, identity and creditworthiness

[ITO Vs AMS Trading and Investment Pvt. Ltd., – ITA No. 1863/Mum/2021]

No addition u/s. 69 in the hands of assessee who had not entered into agreement in personal capacity:

- Shareholder made payment on behalf of the company – The same was treated as unexplained

- The payment was supported by Agreement between two companies and was signed by the assessee on behalf of the company not in his personal capacity.

- ITAT concluded that no addition u/s. 69 should have been made in the hands ofassessee, as he had not entered into any agreement in his personal capacity and deleted the

[JCIT Vs Ajay Sharma – ITA No. 1257/Del/2022]

Section 68 addition can be made only in the Assessment year of receipt:

- Nil return was filed for the A.Y. 2012-13 – Rs. 1 Crore credited in Bank a/c on April 1, 2011, was found during assessment.

- Evidence was submitted proving that the amount belongs to F.Y 2010-11.

- The tribunal examining the evidence agreed that the assessee was responsible for explaining the cash credit ofits predecessor or amalgamated company in the assessment year 2011-12, not 2012-13. – Addition was deleted.

[Shaktigarh Textile and Industries Ltd. vs. DCIT – ITA No. 848/KOL/2023]

Addition u/s 69A towards excess jewellery found unsustainable as assessee belonged to wealthy family:

- Excess jewellery was found during search operations – Additions were made u/s. 69A.

- The sources of the jewellery were not explained.

- ITAT concluded the assessee belongs to a wealthy family and receives jewellery on different Consequently, no addition under Section 69A is warranted.

- The ITAT Delhi directed that the addition made in this case be deleted.[Ankit Sharma vs DCIT (ITAT Delhi) – ITA 1842/Del/2022]

Gifts received in shape of cash “Shaguns” on various occasions kept in Locker shall not be treated as Unexplained Money u/s 69A of Income Tax Act:

- During the search operation, cash was found and seized from the locker – In Absence of evidence, cash found was treated u/s. 69A.

- Appeal was made to the tribunal after CIT(A) accepting the same.

- ITAT deleted the order stating that gifts received in the form of cash shaguns on various occasions cannot be treated u/s. 69A.

[ITAT vs Jasmine Anand & Jaswinder Kaur Anand – ITA Nos. 1145 & 1146/Del/2021]

No addition u/s 69A based on statement recorded during survey if there was no supporting evidence:

- During the search, a statement was recorded where sum of Rs.4.23 crores were agreed to be surrendered for taxation over and above regular profit – But the amount mentioned was not offered, hence addition was made.

- According to assessee, Addition was in respect of unsold flats also which was not in accordance with law – Independent enquiry was not conducted with buyers of the flat to ascertain cash payments made by them.

- All the facts cumulatively prove that AO has made the impugned addition without any

- When there was no basis for arriving at the conclusion that assessee had received anyon-money, addition was not justified as was held by Hon’ble Supreme Court in the case of PCIT Nishant Construction (P) Ltd (2019)

[DCIT Vs Parshwa Associates (ITAT Mumbai) – ITA. No. 2584/Mum/2022]

High share premium is not the correct test for section 68 addition:

High premium charged was treated u/s.68

- The court emphasized the triple test that an assessee needs to satisfy: identity, creditworthiness, and genuineness of the transaction.

- The court criticized the Assessing Officer for focusing on the high premium without conducting further inquiries into the details of cheque payments. The court reiterated that charging a high premium is not the correct test for making additions under Section

[ACIT Vs Montage Enterprises Pvt. Ltd. (Delhi High Court) – ITA 734/2019

Montrose Commodities Pvt. Ltd. vs ITO (ITAT Kolkata)]

Section 69B requires evidence, not conjectures:

- The AO noticed discrepancies in the sales bills and sale ledger, suggesting improper accounting of sales and made addition under Section 69B of the Income Tax

- However, there was no instance of non-recording of sales by the

- The ITAT found that the AO’s addition was speculative and lacked proper

- The ITAT concluded that the addition was unjustified and ordered its deletion.[1. Babusona Mondal Vs DCIT (ITAT Kolkata) – T.A. No. 749/KOL/2023

DDK Spinning Mills Vs DCIT (ITAT Chandigarh)]

Addition u/s 69B merely based on statement without corroborative evidence unsustainable:

- Property was purchased for a consideration of Rs 24 crores, but sale deed was executed for Rs. 12 crores.

- AO concluded that additional Rs.12 crores was paid on or before the registration – Addition was made u/s. 69B and assessee’s explanation was rejected.

- Being aggrieved, the assessee made an appeal to ITAT – ITAT orders to set aside stating that Addition cannot be made merely based on statement without any corroborative evidence.

[ARRS Megamall P. Ltd. Vs DCIT (ITAT Chennai) – ITA No.: 311/Chny/2023]

Sections 115BBE not applicable to income not falling under section 69A:

- During search operation a document was found with the notation “Com Trade” – Amount mentioned in the document was treated u/s. 69A

- Assessee claimed that the amount represented profits from offline commodity trading – The same was surrendered in the ROI.

- Both CIT(A) and ITAT ruled in favour stating that the income surrendered by Assessee cannot be treated as unexplained money under Section

[DCIT Vs Tapesh Tyagi (ITAT Delhi) – ITA No. 1344/Del/2021]

Addition u/s 68 towards unexplained cash credit based on presumptions & conjectures unsustainable:

- STCG was declared after setting off the losses – AO concluded that there is no correlation between rise and fall of share prices.

- AO rejected the STCL set off and treated the entire STCG u/s. 68.

- ITAI dismissed stating that the AO has not conducted any independent investigation and made additions on presumptions and conjectures.

[ITO Vs Rajendra Hastimal Mehta (HUF) (ITAT Mumbai) – ITA No. 2400/Mum/2023]

Section 68: cash receipts from jewellery sales not unexplained cash credits:

- Cash deposited during demonetization was treated u/s. 68 – Source of cash deposits was advances received from customers for a gold scheme, and the same were recorded in its books of accounts

- It also claimed sufficient OB as on the date of demonetization, originating from sales declared before the event.

- TheITAT found that the assessee, through bank statements and cash books, demonstrated substantial cash withdrawals preceding the demonetization period and ordered to delete the addition made.

[ITO Vs Sahana Jewellery Exports Pvt. Ltd. (ITAT Chennai) – ITA No.999/Chny/2022]

Section 68: Treating Deposit of normal currencies as SBNs during demonetisation period cancelled by ITAT – ITA 1210/CHNY/2023:

- Cash was deposited to the tune of Rs. 26,49,300/- from 09.11.2016 to 31.12.2016 and the ITO treated a sum of 18,91,407 as unexplained cash credit u.s. 68 after adjusting opening balance, even though the SBNs deposited were below the opening balance in spite of assessee producing documentary evidence being pay-in-slips of the bank with denomination of currencies deposited.

- The ITO had not received reply from the Bank for the notice calling for the details of deposit made by the assessee while passing the order on 28.12.2019. On receipt of the statement of account from Bank by the Department as well as by the assessee, the assessee filed a rectification petition on 06.01.2020, which was not attended to at

- The Assessee filed an appeal before CIT (Appeals), who without looking into the statement of account given by the Bank, wherein the deposit SBNs were termed as OHD (Old Higher Denomination), endorsed the order passed by the

- Onappeal by the assessee the ITAT deleted the addition of 18,91,407/- by considering the statement of account given by the Bank

[Lakshmanan Meenakshi vs. AC NC 2 (MDU) – ITA 1210/CHNY/2023]

Mere retracted statement without nexus insufficient for section 69A addition:

- During search operation a diary containing coded entries were seized – Certain individuals purportedly admitted to engaging in unaccounted money lending activities.

- As per AO – Rs. 3.25 crores were lent as cash loan and was not disclosed in ITR.

- Furthermore, the individuals later retracted his statement, casting doubt on its reliability.

- The ITAT observed that the AO had not granted assessee the opportunity to cross-examine and questioned the conversion of a coded amount of Rs. 32,500 to Rs. 3.25 crores. – ITAT suggested to delete the addition made.

[1. Mayur Kanji Bhai Shah Vs ITO (ITAT Mumbai)

2.Konark Fixtures Ltd vs DCIT (ITAT Mumbai)]

Addition u/s 68 deleted as genuineness and creditworthiness of lender proved:

- Assessment was reopened u/s. 148 – Unsecured loan received by the company was treated u/s. 68.

- Necessary documents were submitted and scrutinized by ITAT.

- ITAT deleted the addition stating that genuineness and creditworthiness of lender was proved.

[1. Trident Towers Pvt. Ltd Vs ACIT (ITAT Delhi)

2.Wisley Real Estate Pvt. Ltd Vs Income Tax Officer (ITAT Kolkata)

3. BST Infratech Ltd. Vs DCIT (ITAT Kolkata)

4. DCIT Vs Cabcon India (P) Ltd. (ITAT Kolkata)]

Addition u/s 69 deleted as receipt of cold storage rent in cash not reason to doubt genuineness:

- SCN was issued to furnish details of cold storage rent received – In response, copies of ledger were submitted.

- Stocks of 8 parties found in the storage were treated u/s. 69 – Since the 8 parties paid the rent in cash and no evidence was submitted to prove the stock belonged to the said 8 parties.

- Stocks were valued and additions were made – CIT(A) deleted the addition but revenue appealed before ITAT.

- ITAT deleted the addition stating that the stocks found were belonged to the 8 parties.

[DCIT Vs Suboli Ice and Cold Storage Pvt. Ltd. (ITAT Delhi)]

Difference in stock found during course of survey duly reconciled hence addition u/s 69 unsustainable:

- During the survey – A difference was found between the physical stock and stock as per books.

- AO after considering the submissions, explanations, documents and evidence – the difference found was added u/s. 69 of the act.

- CIT(A) affirmed the order of AO. Being aggrieved, the present appeal is filed.

- ITAT held that merely because some differences were found in stock during survey would not indicate any automatic addition being made in the hands of the assessee when assessee has duly reconciled the differences with necessary evidence.

[Ultimate Creations Vs ACIT (ITAT Delhi)]

Addition u/s. 68 unsustainable as AO failed to conduct independent enquiry to verify genuineness of transaction:

- Failure to provide explanation towards share capital and share premium received – Both share capital and premium were treated u/s. 68.

- CIT(A) deleted the impugned additions made u/s. 68 of the Act. Being aggrieved, revenue has preferred the present appeal.

- ITAT held that the assessee has successfully discharged the burden of proof primarily cast upon it to explain the identity and creditworthiness.

[ITO Vs Express Tradelink Pvt Ltd (ITAT Kolkata)]

Section 68 not to apply to outgo or payment on account of expenditure:

- The contention primarily revolves around Section 68, which mandates the credit of amounts in the books maintained by the assessee.

- However, in this case, the transactions pertain to outgo or payment on account of expenditure, rendering Section 68 inapplicable. The absence of any credit in the books of account regarding the impugned additions further strengthens this argument.

- Moreover, Section 69C is not applicable as it pertains to explaining the source of expenditure, whereas in this scenario, the focus is on the expenditure itself, not its source of payment.

[Feather Infotech Pvt. Ltd. Vs DCIT (ITAT Delhi)]

ITAT deletes Section 68 addition of Advance received against Sale:

- Funds were received from a company – the same was constituted as unexplained cash credit u/s. 68.

- Substantial evidence to support their claim was submitted – Sales registers, invoices, and bank statements, corroborating the sale transactions were also submitted.

- The tribunal concluded that assessee company had indeed made sales to the other company against advance payments, negating the notion of unexplained cash credits.

[Hiral Exports Vs ITO (ITAT Mumbai)]

No Sec 69 Addition merely for Property Transfer via Registered Sale Without Payment to Vendor:

- Sale deed was executed without encashing the cheques issued for payment – AO concluded that payments were made in cash and treated the same u/s 69.

- Appellant argued that cheques were issued and later cleared through exchange of fresh cheques.

- The ITAT, after thorough consideration of facts and legal precedents, concluded that the addition under section 69 was not warranted – addition was deleted.

[Hyfun Frozen Foods Pvt Ltd Vs ITO (ITAT Ahmedabad)]

No Section 68 addition merely for non-response from directors to notices:

- Director failed to respond to the notice – Addition was made u/s. 68

- The Tribunal noted that the AO did not comment on the veracity or admissibility of details and documents provided by the assessee.

- By dismissing the Revenue’s appeal, the decision underscores the principle that the mere non-response to notices cannot serve as the sole basis for drawing adverse inferences in tax matters.

[PCIT Vs Atlantic Dealers Pvt. Ltd. (Calcutta High Court)]

Section 68 addition invalid if creditworthiness proven:

- Significant sums were received as share capital/premium from multiple entities.

- As per Revenue – Funds received from certain entities lacked creditworthiness and authenticity and the same treated u/s.68.

- Necessary evidence was submitted and assessee contended that the transactions were legitimate.

- However, the CIT(A) and subsequently ITAT Delhi found in favor of the assessee – They held that the assessee had sufficiently demonstrated the legitimacy of the funds received.

[1. I.T.O Vs Placid Build well Pvt Ltd (ITAT Delhi)

2. ITO Vs Express Tradelink Pvt Ltd (ITAT Kolkata)]

Section 68 Addition Unjustified if Shares’ Purchase & Sale Validated by Evidence:

- Assessee had LTCG on sale of shares – The sales proceeds were treated u/s. 68 and estimated commission were treated u/s. 69C.

- Explanations were provided but AO was not satisfied with the explanation and material information submitted.

- ITAT deleted the addition stating that the requisite details in respect of purchase and sale of shares were submitted.

[Amarjit Kaur Surinder Singh Kochhar Vs ITO (ITAT Mumbai)

CIT v. Lovely Exports (P) Ltd. (2008)216 CTR 195 (SC)]

Deduction u/s. 80IC eligible on addition u/s. 68 of unsubstantiated share capital:

- The case marks the second round of litigation after the ITSC’s initial order was challenged and set aside by the Delhi High Court, requiring a re-examination of the issues related to unexplained share capital and deductions under Section 80IC.

- The ITSC’s order partially set aside the additions made with respect to the infusion of share capital by M/s Amit Goods and Supplier Private Limited and the denial of benefits under Section 80IC.

- The High Court dismissed the ITSC’s conclusion that the addition of unsubstantiated share capital under Section 68 would not qualify for deduction under Section 80IC, granting the petitioner consequential reliefs.

- The petitioner is entitled to claim deductions under Section 80IC up to AY 2013-14.

[Valley Iron & Steel Co. Ltd. Vs PCIT (Delhi High Court)]

No addition u/s 68 as assessee had not benefited from Round-Tripping of Share Transaction:

- Share application money were received and subsequently shares were allotted.

- The case was reopened u/s.147 based on information suggesting accommodation entry received by the assessee from entities operated by a certain group – Was treated u/s. 68.

- Evidence was submitted to substantiate the transactions’ genuineness.

- ITAT deleted the addition made under section 68 as there was no material to suggest the assessee benefited from round-tripping.

[Lalwani Estates & Realtors Pvt Ltd Vs ITO (ITAT Mumbai)]

Section 69/69A/115BBE not applies to duly explained Excess Stock:

- Excess stocks were found during the survey – The same was declared as additional income.

- The excess stock found were related to the money-lending business and were supported by documents of previous years’ financial statements.

- But similar cases were assessed as regular business income and not subjected to section 69/69A/115BBE.

- The Tribunal uphold the original assessment-order, rejecting the PCIT’s revision-order.

[Naresh Chandra Kalwani Vs PCIT (ITAT Indore)]

No section 68 addition for Share Capital Subscription if assessee submits evidence for source of funds:

- Share capital subscriptions were treated u/s. 68 – Evidence was submitted.

- Evidence submitted was deemed genuine and no unaccounted cash was involved.

- The Revenue’s appeal was dismissed by ITAT Delhi, upholding the learned CIT(A)’s decision that the provisions of Section 68 could not be applied in this case. The document details the legal reasoning and evidence provided that led to this conclusion.

[1. DCIT Vs CDS Infra Projects Limited (ITAT Delhi)

2. PCIT Vs Narsingh Ispat Ltd. (Calcutta High Court)]

Share Capital/Premium amount cannot be added twice in payees & recipients’ hands u/s 68:

- Share capital were raised and genuineness of cash credits were accepted by AO – Except the amount of Rs. 20 Lakh received from M/s. Seacom Merchants.

- M/s. Seacom Merchants was assessed to tax for the same amount and the same was evidenced by the order passed by AO.

- The ITAT Kolkata referenced several precedents to support its decision.

- The ITAT Kolkata concluded that no additions could be made u/s since the share applicant company, M/s. Seacom Merchants, was already taxed for the same amount.

[Shreenath Holding Pvt. Ltd Vs ITO (ITAT Kolkata)]

Notice issued making addition u/s. 68 whereas order confirmed addition u/s 69A untenable: Calcutta HC:

- Notice was issued u/s. 68 to show cause as to show why the sum should not be added back.

- But thesum was added back for the AY on account of unexplained money u/s. 69A.

- It is seen that although, the revenue authorities had invoked the provisions of Section 69A of the said Act.

- The AO stands vitiated by reasons of failure on the part of the revenue authorities to put the petitioner on notice in respect of addition under Section 69A of the said Act.

- Since the above is violative of the principles of natural justice, the order impugned becomes unenforceable in law and is declared as such.

[Vishal Jhajharia Vs Assessment Unit (Calcutta High Court)]

Non-appearance of directors cannot form the sole basis for Section 68 addition:

- A large amount of share premium was received during the financial year – Assessee company complied with all the summons, but the subscribing companies did not.

- Tribunal reviewed the materials on record submitted – Emphasized that Assessee company had submitted all required evidence, thereby discharging its onus.

- ITAT deleted the addition made.

- ITAT Kolkata’s decision to delete the Section 68 addition in the case underscores the importance of thorough investigation by revenue authorities before making additions based on unexplained cash credits.

[1. Sati Promoters Pvt. Ltd Vs ITO (ITAT Kolkata)

2. Amodini Vyapar Pvt. Vs ITAT Kolkata]

No Section 69A Addition for Monies Recorded in Bank Statements: ITAT Bangalore

- Cash deposits were made during the demonetization period – The same was treated u/s. 69A.

- Evidence was submitted to justify that the deposits made were out of previous withdrawals.

- The ITAT found the AO had not disproven the appellant’s explanations nor provided contrary evidence – Ruled in favor by deleting the addition.

[1. Sudarshan Purushothama Vs ITO (ITAT Bangalore)

2. Chiranjeet Kundu Vs AO (ITAT Kolkata)]

No addition u/s. 68 towards unsecured loan if repayment in subsequent year accepted:

- Unsecured loans were borrowed, and Interest were paid.

- AO contended that these were mere paper companies and operated for the purpose of providing accommodation entries – Total income was treated u/s 68 and the Interest paid was treated u/s 69C of the act.

- CIT(A) deleted the additions both u/s.68 and 69C of the Act and allowed the appeal of the assessee. Being aggrieved, revenue has preferred the present appeal.

- ITAT held that the assessee has provided substantial evidence to establish the identity, genuineness, and creditworthiness – CIT(A) order deleting the additions is upheld.

[1. DCIT Vs Tripoli Management Pvt. Ltd. (ITAT Ahmedabad)

2. Aravind Reddy vs ITO (ITAT Vishakapatnam)

3. ACIT vs Jaideep Halwasiya (ITAT Kolkata)

4. PCIT vs Ambe Tradecorp (P) Ltd. (Gujarat HC)]

ITAT allows taxation of excess stock & unexplained marriage expenses as business Income:

- During the survey excess stock and Unaccounted marriage expenses were found – Assessee contended that these amounts were included in his ITR.

- Additional income was taxed @ 60% u/s. 115BBE by the AO.

- Assessee argued that excess stock and marriage expenses should be treated as business income and taxed @ 30%.

- The ITAT Chennai examined the detailed submissions and facts presented by both parties and directed that it should not be taxed under Section 115BBE, as it was derived from the regular business activities of the assessee.

[Santhilal Jain Vijay Kumar Vs ITO (ITAT Chennai)]

Invalid Reassessment Notice due to Lack of PCCIT Approval: ITAT quashes Additions

- Reassessment was issued u/s 148 – Difference between purchase price and Stamp duty value were treated as addition.

- Necessary documents were submitted including Bank statement and details of property purchased.

- Since income escaped was below 50 Lakhs approval from PCCIT was required.

- Approval was received from PCIT which is not in line with law – ITAT deleted the addition.

[Arnab Kumar Goswami Vs AO (ITAT Kolkata)]

Addition of ₹12 Lakh u/s 69A: ITAT holds Sundry Debtors do not Qualify as Unexplained Income

- ITAT found that the addition of ₹12 Lakh under Section 69A of Income Tax Act,1961 was not justified

- The Assessing Officer (AO) found that she had deposited ₹25,00,000 in cash during demonetization, claiming it was declared under the IDS Scheme

- The AO also found that she had shown ₹12,00,000 as debtors but did not provide evidence to prove their identity.

- The assessee appealed before the Commissioner of Income Tax (Appeals)[CIT(A)] against the addition of ₹12,00,000 as unexplained income under Section 69A of the Act.

- The case was initially selected to verify cash deposits and later converted into full scrutiny. During assessment, the AO found that ₹12,00,000 was shown as debtors but without supporting evidence, leading to its addition under Section 69A of the Act.

- The appellate tribunal noted that sundry debtors recorded in the books do not fall under Section 69A. It also found that these debtors related to 2013 and 2014, not the relevant assessment year (2015-16). Since this fact was undisputed, the tribunal ruled that the addition was not justified and allowed the appeal.

[Ratika Kumbhat Vs AO (ITAT Jaipur)]

Addition u/s 68 – Cash Introduction and Insurance Payment Properly Explained – Addition Deleted by ITAT

- The Income Tax Appellate Tribunal deleted an addition of ₹1,40,000 made u/s 68 by the AO.

- The AO treated the amount as unexplained during reassessment proceedings u/s 147.

- The assessee explained that ₹1,40,000 comprised ₹20,000 cash introduction and ₹1,20,000 insurance premium paid on behalf of the firm, later credited to his capital account.

- The AO failed to bring any material evidence to disprove the explanation.

- ITAT held that mere suspicion without justification cannot sustain an addition u/s 68.

- The addition of ₹1,40,000 was directed to be deleted.

[Aravind Reddy vs ITO (ITAT Vishakapatnam)]

Addition under Section 68 not sustainable when source of investment is explained through bank records

- The Income Tax Appellate Tribunal deleted additions made under Section 68 relating to unexplained investments.

- The assessee explained that the investments in two partnership firms were made out of funds transferred from another disclosed partnership firm where he was Managing Partner.

- Bank statements and capital account entries clearly established the source and flow of funds.

- The AO and CIT(A) ignored the documentary evidence and treated the investments as unexplained.

- ITAT held that when transactions are properly recorded and supported by bank records, Section 68 cannot be invoked.

- Accordingly, the AO was directed to delete the additions, and the appeal was allowed.

[Aravind Reddy vs ITO (ITAT Vishakapatnam)]

No additions under Section 69A for Cash Deposits from Recorded Sale Proceeds:

- The Income Tax Appellate Tribunal deleted additions made under Section 69A read with Section 115BBE relating to cash deposits.

- The AO treated cash deposits of ₹7,99,698 in bank accounts as unexplained money.

- The assessee explained that the cash deposits arose from sale proceeds duly recorded in books of accounts.

- Cash book ledgers and documentary evidence were produced to substantiate the explanation.

- ITAT observed that the Revenue had accepted the assessee’s turnover but failed to consider sales during the demonetisation period.

- Holding that the cash deposits were fully explained, ITAT directed the AO to delete the additions.

[Ashoka Enterprises vs ITO (ITAT Vishakapatnam)]

Section 68 Addition Remanded for De Novo Assessment due to Inconsistencies in Evidence:

ITAT Bangalore held that addition under section 68 of the Income Tax Act towards unexplained money send back for de novo reassessment due to difference in amounts and unclear information.

[Ryatar Sahakari Sakkare Karkhane Niyamit Vs ITO (ITAT Bangalore)]

Addition under Section 69A not sustainable to the extent of redeposit of explained cash

- The Income Tax Appellate Tribunal examined an addition of ₹35.13 lakh made u/s 69A r.w.s. 115BBE towards unexplained cash deposits.

- The assessee explained that the deposits were sourced from agricultural income, earlier cash withdrawals redeposited, and sale of vehicles used in his proprietary business.

- ITAT accepted ₹3.50 lakh as agricultural income (already disclosed and accepted by AO) and ₹12.38 lakh as redeposit of earlier cash withdrawals.

- The Tribunal held that cash redeposited from explained withdrawals cannot be treated as unexplained money u/s 69A.

- The balance amount of ₹19.25 lakh relating to sale of vehicles was restored to the AO for fresh verification due to inadequate examination earlier.

- Consequently, the addition was partly deleted, and the appeal was partly allowed.

Section 68 Addition Remanded where Final Addition exceeded Amount Proposed in Notice

- ITAT Delhi held that addition made under section 68 of the Income Tax Act is lower as alleged in show cause notice as compared to addition made by ACIT hence matter remanded for fresh consideration.

[Ducati India Private Limited vs ACIT ITAT Delhi ITA No. 2382/DEL/2024 | Order dated 30.09.2024]

No Addition under Section 68 in Firm for Partners’ Capital Contributions – Onus shifts to Partners

- The issue was whether capital introduced by partners in an LLP can be added u/s 68 in the hands of the firm.

- The assessee firm proved that partners introduced capital through banking channels, thereby discharging its initial onus.

- Relying on Gujarat High Court and Supreme Court precedents, ITAT held that the firm is not required to explain the source of source.

- If the AO doubts creditworthiness or genuineness, enquiry must be made in the hands of the partners, not the firm.

- Tribunal noted that this principle is consistently upheld by High Courts and multiple ITAT benches.

- Accordingly, ITAT dismissed the Revenue’s appeal and confirmed deletion of Section 68 addition in the firm’s hands.

[ITO vs Samvatt Properties LLP ITAT Ahmedabad | ITA No. 277/Ahd/2024 | A.Y. 2016–17 | Order dated 28.08.2024. The following case laws were relied upon:

1. PCIT vs Vaishnodevi Refoils & Solvex – Gujarat High Court

2. CIT vs Pankaj Dyestuff Industries – Gujarat High Court

3. Metachem Industries Ltd – Madhya Pradesh High Court

4. Panda Fuels vs ITO – ITAT Cuttack (ITA No. 07/CTK/2018)

5. Shri Gem vs ITO – ITAT Delhi]

Cash Deposits from Business Turnover cannot be taxed again under Section 69A – No Double Taxation

- The assessee, a jeweller, deposited cash in bank accounts during the demonetisation period, which was treated by the AO as unexplained money u/s 69A.

- ITAT found that the cash deposits arose from recorded business turnover, on which profit had already been offered to tax.

- Treating the same receipts both as business income and unexplained money resulted in impermissible double taxation.

- Once turnover is accepted and profits are assessed, entire cash sales cannot be added u/s 69A.

- The Tribunal noted that cash sales without customer details are normal in retail jewellery trade and are legally permissible.

- ITAT deleted the addition u/s 69A and held that Section 115BBE was also not applicable.

[Nitin Kumar Bohra vs Income Tax Officer Income Tax Appellate Tribunal ITA No. 340/Bang/2024 | A.Y. 2017–18 | Order dated 24.09.2024. The following case laws have been relied upon:

1. R.B. Jessaram Fatehchand (Sugar Deptt.) vs CIT – (1970) 75 ITR 33 (Bombay HC)

2. Kishore Jerambhai Khaniya (Prop. M/s Poonam Enterprises) vs ITO – ITA No. 1220/Del/2011 (ITAT Delhi)

3. CIT vs Kailash Jewellery House – ITA No. 613/2010 (Delhi High Court)

4. CIT vs Vishal Exports Overseas Ltd. – ITA No. 2471 of 2009 (Gujarat High Court)

5. New Pooja Jewellers vs ITO – ITA No. 1329/Kol/2018 (ITAT Kolkata)

6. CIT vs Jaora Flour & Foods (P) Ltd. – (2012) 344 ITR 294

7. Anantapur Kalpana vs ITO – ITA No. 541/Bang/2021 (ITAT Bangalore)

8. CIT vs Associated Transport (P) Ltd. – 84 Taxman 146

9. ACIT vs Hirapanna Jewellers – ITA No. 253/Viz/2020 (ITAT Vizag)

10. ITO vs Tatiparti Satyanarayan – ITA No. 76/Viz/2021 (ITAT Vizag)]

ITAT deletes Section 69C Addition as allegations not substantiated with clear evidence

- The matter primarily pertained to unexplained expenditures assessed under Section 69C of the Income Tax Act for the assessment year (AY) 2020-21. Cross-appeals were filed by the assessee and the Revenue against the order of the CIT(A)-52, Mumbai, which partly confirmed and partly deleted additions made by the Assessing Officer.

[DCIT Vs Triton Hotels and Resorts Pvt. Ltd (ITAT Mumbai)]

Protective Additions under Sections 69A & 69C – Retraction Alone not Sufficient; Matter Remanded for Fresh Adjudication

- A search u/s 132 revealed a structured scheme of routing unaccounted money through shell companies, villagers, and nearly 230 bank accounts into M/s Prime Ispat Ltd., a company linked to the assessee.

- The AO made protective additions u/s 69A (unexplained investments) and 69C (unexplained expenditure) in the hands of the assessee.

- The CIT(A) and ITAT deleted the additions, mainly relying on the retraction of the statement of the Chartered Accountant.

- The High Court found that multiple corroborative statements (of directors and associates) and material evidence were ignored by appellate authorities.

- It held that mere retraction of one statement does not nullify other incriminating evidence, especially where a colorable device to launder income is indicated.

- The Tribunal erred in not appreciating the entire chain of fund routing and surrounding circumstances unearthed during the search.

[ACIT vs B.L. Agrawal (Chhattisgarh High Court)

1. Smt. Tara Devi Aggarwal vs CIT – (1973) 88 ITR 323 (Supreme Court)

2. State of Orissa vs Mamata Mohanty – (2011) 3 SCC 436 (Supreme Court)

3. CIT vs Lovely Exports (P) Ltd. – 216 CTR 195 (Supreme Court)

4. Rajmandir Estates Pvt. Ltd. vs PCIT – SLP (C) Nos. 22566–22567/2016]

Substance over form is critical in evaluating unexplained credits

- The AO is entitled to look beyond the form and assess the substance of a transaction. Surrounding circumstances and human probabilities can be used to determine whether the explanation is satisfactory.

[CIT vs Durga Prasad More (1971) 82 ITR 540 (SC)]

Assessment u/s. 153A quashed as addition u/s. 68 made without any incriminating material found during search

ITAT Delhi held that assessments completed u/s. 153A, making addition u/s. 68 of the Income Tax Act, without any incriminating material found during the search action is unsustainable in law. Accordingly, addition deleted.

[DCIT Vs Frost Falcon Distilleries Ltd (ITAT Delhi) (2024)]

Section 69A Addition not Sustainable in Hands of Intermediary – Money Trail Establishes Ultimate Beneficiary

- The AO made an addition of ₹4.45 crore u/s 69A, treating funds received by the assessee as unexplained money.

- Extensive survey and investigation revealed that the entire money trail was known to the Department, and the ultimate beneficiary was M/s VMS Industries.

- The assessee and its sister concern merely acted as intermediaries/conduits for routing funds.

- Statements of directors and assessment orders of connected entities consistently admitted the same modus operandi.

- The assessee incurred commercially irrational losses, reinforcing that it was not the real beneficiary.

- Applying the test of human probabilities (Sumati Dayal), ITAT held that the funds could not be treated as income of the intermediary.

- Conclusion: The Income Tax Appellate Tribunal, Ahmedabad Bench held that Section 69A cannot be invoked in the hands of an intermediary when the Department itself has established the complete money trail and identified the ultimate beneficiary. Accordingly, the addition of ₹4.45 crore was deleted.

[1. Sumati Dayal vs CIT (1995) (SC)

2. GKN Driveshafts (India) Ltd. vs ITO (2003) (SC)]

Linking RBI notification violation to Section 68 unjustified as nature & source explained: ITAT Ahmedabad

- The Income Tax Appellate Tribunal examined addition of ₹74.65 lakh u/s 68 relating to cash deposits during demonetisation.

- The assessee, a co-operative credit society, deposited SBNs (₹500/₹1000) collected from its members between 10–12 Nov 2016.

- The AO treated the deposits as unexplained solely on the ground that accepting SBNs allegedly violated RBI notifications.

- The assessee produced member details, KYC, ledgers, pay-in slips and books, establishing that deposits were regular business collections/loan repayments.

- ITAT held that contravention (if any) of RBI notification cannot be linked to Section 68 once the nature and source are satisfactorily explained.

- Relying on earlier Tribunal precedent, ITAT upheld deletion of the addition; Revenue’s appeal was dismissed.

No tax on amount received as ‘On-Money’ from sale of Flats u/s 68

Since the addition pertained to the “receipt of money” from the sale of flats by the assessee and these amounts did not represent the actual receipts in the hands of the assessee, they could not be subjected to tax.

[Kalyan Development Corporation Vs ACIT (ITAT Mumbai) 2024]

Sham Share Transaction – Section 68 Addition Upheld

- The tax tribunal found that the share transaction claimed by the assessee did not make practical or business sense.

- The shares were bought in April 2010, but payment was made almost 11 months later, with no proper explanation or agreement, which raised serious doubts.

- The company involved (Karma ISP) was already identified by tax authorities as a penny stock commonly used to convert black money into fake tax-free profits.

- The assessee earned an abnormally high profit of more than 1,100% in just 15–16 months, without any regular share trading activity before or after—suggesting it was not a genuine investment.

- The company had no real business or financial strength to justify such a sharp rise in share price, making the profit highly unrealistic.

- Applying common sense and real-life probability (as supported by Supreme Court rulings), the tribunal held that the transaction was only a paper arrangement to avoid tax, and therefore the addition made by the AO under Section 68 was correct.

Additions for unexplained cash deposits u/s 69A and loans made u/s 68 without proper verification was restored back

- The assessee, a trader in plastic pipes, deposited ₹32.61 lakh in cash during demonetisation, claimed to be from recorded cash sales, and also reflected unsecured loans of ₹3.24 lakh.

- The AO completed a best-judgment assessment u/s 144 due to alleged non-compliance and treated the cash deposits as unexplained u/s 69A (alternatively u/s 68), and loans as unexplained u/s 68, without fully examining records.

- Though the assessee later produced audited financials, cash books, VAT invoices, VAT returns, and reconciliations, neither the AO nor the CIT(A) properly verified these documents or called for a remand report.

- The Tribunal noted factual controversies (opening/closing cash balance mismatch, nature of cash sales, existence of petty cash book, and loan confirmations) that required proper examination.

- Holding that additions were made without adequate verification and opportunity, ITAT did not decide on merits.

- The issues relating to ₹32.61 lakh (u/s 69A) and ₹3.24 lakh (u/s 68) were restored to the AO for de novo adjudication with directions to pass a reasoned order after giving full opportunity.

Section 68 Addition Set Aside where Source and Source-of-Source were Disclosed

- The assessee received funds as an advance for arranging finance, which were fully repaid when the deal failed.

- He disclosed the immediate source (Emperor Builders Pvt. Ltd.) and the source-of-source (Lalitha Cement Ind. Ltd.), supported by MOUs, bank statements, and ledger accounts.

- The AO made multiple additions u/s 68 mainly because the assessee could not produce the intermediary and alleged lack of creditworthiness, without independent verification.

- The Tribunal noted that documentary evidence corroborated the assessee’s explanation and that the AO did not issue notices/summons or verify with the source-of-source.

- Failure to produce a person alone cannot justify an addition when the money trail is documented.

- Accordingly, the additions were set aside and remanded to the AO for fresh verification with directions; appeal allowed for statistical purposes.

[Uday Vithal Nagpure Vs ITO (ITAT Mumbai) Order pronounced on 30.05.2025]

Cash Source Once Accepted and Taxed u/s 269SS cannot be Taxed Again u/s 69A due to Time Gap

- The assessee deposited cash during demonetisation and consistently explained that the source was sale proceeds of agricultural land received earlier in cash.

- In the original assessment u/s 143(3), the AO accepted the source but made an addition u/s 269SS for violation of accepting cash.

- Later, after revision u/s 263, the AO again added the same cash u/s 69A only on the ground of a time gap between receipt and deposit.

- The ITAT held that once the source is accepted, it is clear the assessee had sufficient funds; a time gap alone cannot make it “unexplained”.

- Since the amount was already taxed/settled u/s 269SS (Vivad se Vishwas), a further addition u/s 69A amounts to impermissible double taxation.

- Accordingly, the Section 69A addition was deleted and the assessee’s appeal was allowed.

[Sowjanya Basi Reddy vs ITO (ITAT Hyderabad) A.Y. 2017-18 | Order pronounced on 08.05.2025]

Excess Cash and Stock Found in Search to be Taxed as Business Income, Not as Unexplained Money u/s 69A

- A search u/s 132 in the case of a jewellery and diamond business revealed excess cash (₹34.65 lakh) and excess stock (₹1.38 crore) over and above what was recorded in the books.

- The assessee admitted the excess as unaccounted income during the search and did not retract the statement recorded u/s 132(4).

- The AO sought to tax the amounts as unexplained investment/money u/s 69A, whereas the CIT(A) treated them as business income.

- The Tribunal noted that the audited books were not rejected, and the Revenue failed to prove that the excess cash and stock did not arise from business activities.

- It was held that when excess cash/stock is found in a running business, it normally represents suppressed business income, not unexplained money.

- Accordingly, the ITAT dismissed the Revenue’s appeal and upheld taxation of the surrendered amount as business income, not u/s 69A.

[Raj Diamonds vs ACIT ITAT Bangalore A.Y. 2020-21 | Order dated 26.12.2023 (ITAT order reported on 25.02.2025) Citations relied upon

Roshan Lal Sanchiti vs CIT – Supreme Court

Overseas Leathers vs ACIT – ITAT Chennai

SVS Oil Mills vs ACIT – Madras High Court]

Section 68 Addition Deleted for Squared-up Loans Supported by Banking Trail

- The assessee received unsecured loans from three persons (₹51 lakh) which were taken and fully repaid within the same financial year through banking channels.

- Detailed evidence was filed: PAN/Aadhaar, ITRs, bank statements, ledger accounts, and repayment proofs; one creditor’s non-appearance was explained due to serious illness and subsequent death.

- The AO/CIT(A) sustained addition mainly because notices u/s 133(6) were not responded to and confirmations were not produced, despite the banking trail being undisputed.

- ITAT held that non-response to 133(6) alone cannot negate otherwise genuine transactions, especially when identity, genuineness, and creditworthiness are proved on record.

- Relying on binding precedents, ITAT ruled that loans squared up within the year and evidenced through banks do not attract Section 68.

- Accordingly, ₹51 lakh addition was deleted; assessee’s appeal allowed and Revenue’s appeal dismissed.

[Jasdeep Kaur Chadha vs DCIT ITAT Amritsar | A.Y. 2018-19 | Order pronounced on 22.08.2025]Citations relied upon:

CIT v. Varinder Rawlley (2014)

PCIT v. Wel Intertrade (P) Ltd. (2023)

PCIT v. Merrygold Gems (P) Ltd. (2024)

PCIT v. Ambe Tradecorp (P) Ltd. (2022)

DCIT v. Tripoli Management Pvt. Ltd. (ITAT Ahmedabad, ITA No. 05/Ahd/2024)

Rajhans Construction (P) Ltd. v. ACIT (2022)

ITO v. Shri Agrasen Logistics (ITAT Agra, ITA No. 108/Agr/2025)

Daulat Ram Rawatmull (1964) 53 ITR 574 (SC)]

Presumptive Taxation u/s 44AD does not bar Section 68 Additions – Matter Remanded for Verification

- The assessee (HUF) declared income under presumptive taxation u/s 44AD and argued that no addition u/s 68 could be made due to the non-obstante clause.

- The AO reopened the case based on STR/DRI intelligence alleging fictitious diamond purchases from a suspected paper company (Namo Diamonds Pvt. Ltd.), and added ₹53.09 lakh u/s 68.

- Despite invoices and bank records being produced, field enquiries showed the supplier did not exist at the given addresses, leading authorities to treat the purchases as accommodation entries.

- The CIT(A) upheld the addition, holding that Section 68 applies even when 44AD is opted, if transactions are sham.

- At ITAT, most assessee-relied precedents were distinguished; ITAT noted no statutory bar in Sections 44AD/68 against such additions.

- Since a new factual aspect (payments made through banks in a subsequent year) was not examined earlier, ITAT remanded the matter to the AO for fresh verification; appeal allowed for statistical purposes.

[Hemant M. Shah (HUF) vs ITO (ITAT Mumbai) A.Y. 2018-19 | Order dated 30.04.2025]

Section 115BBE High Tax Rate Applies Only to Transactions After 1.4.2017

- The Income Tax Appellate Tribunal (ITAT) Delhi, in the case of Babu Ram Aggarwal vs.ITO for Assessment Year 2012-13, has ruled that the higher tax rate prescribed under Section 115BBE of the Income Tax Act, 1961, cannot be applied to transactions undertaken before April 1, 2017. This decision aligns with a recent judgment from the Madras High Court.

- The central issue in the appeal was the invocation of Section 115BBE by the Assessing Officer (AO) concerning an addition of Rs. 3,61,000/- made under Section 69C of the Act.

Author Bio

As seen from the various decisions it is seen that these sections are widely used to harass the Assessees. These sections may be made inapplicable from the Assessment Year 2026-27 at least.

Taxing income @ 137% ( including penalty) and in addition levying interest is exorbitant and the operation of these sections should be stopped immediately.

As seen from the various decisions it is seen that these sections are widely used to harass the Assessees. These sections may be made inapplicable from the Assessment Year 2026-27 at least.

Taxing income @ 137% ( including penalty) and in addition levying interest is exorbitant and the operation of these sections should be stopped immediately.

As seen from the various decisions it is seen that these sections are widely used to harass the Assessees. These sections may be made inapplicable from the Assessment Year 2026-27 at least.