GST Dispute on Exempt Supply of Raw Milk: Lessons from ASMT-10 to DRC-07 Proceedings

Introduction: The Goods and Services Tax (GST) framework is built on the principles of self-assessment, accurate classification, and evidentiary compliance. While the law provides clear exemptions for certain supplies—particularly primary agricultural products such as unprocessed milk— the practical application of these provisions often depends on the taxpayer’s ability to substantiate such claims before the tax authorities.

This article analyses a case where a taxpayer engaged in the supply of milk, ostensibly an exempt commodity, became subject to a tax demand not due to the inherent taxability of the goods, but due to procedural non-compliance. The taxpayer, despite dealing in exempt supplies, obtained GST registration and disclosed turnover under exempt categories. However, the absence of documentary support and failure to respond to statutory notices led the authorities to question the nature of the supply and reclassify it as taxable.

The resulting demand, including tax, interest, and penalty, underscores a critical aspect of GST compliance: exemption claims must be supported by adequate documentation and timely representation. This case serves as a reminder that, within the GST regime, procedural diligence is as vital as substantive correctness in determining tax outcomes.

Chart:01

Exempt Unprocessed milk trade – GST registration – High turnover suspicion – ASMT-10 – No reply – DRC-01 – No reply – DRC-07 order

DRC 07 ORDER 26.12.2025:

KR Agencies (GSTIN: 3XXXX2) is a registered taxpayer. The returns filed by the taxpayer, along with other documents available on the common portal for the financial year 2021–22, have been verified.

With reference to the intimation issued in Form GST ASMT-10 (to furnish the supporting documents for the claim of exemption on the turnovers) dated 25.08.2025, no reply was filed by the taxpayer. Subsequently, a show cause notice in Form GST DRC-01 was issued on 25.09.2025.

As no response was received, the demand proposed in the said notice is hereby confirmed, and an adjudication order is passed under Section 73 of the TNGST Act, 2017, as detailed below.

Conclusion of the Proper Officer:

The taxpayer neither filed any reply nor paid any tax due. And The personal hearing issued in the reference 4th , 5th & 6th cited. The personal hearing notices were sent through common portal on 06.11.2025, 14.11.2025 & 24.11.2025. and also through Registered Post with Acknowledgement Card No. XXXXX / 07.11.2025.

But they have not utilized their opportunity and they did not file any reply. Hence the defect is confirmed & order passes as below. In the view of the above facts, and circumstances, I came to conclude the proceedings as per merits of the records available. Therefore, to safeguard the government revenue, as per section 73 of TNGST & CGST Act, 2017, this final order is passed as confirmed in the notice in the reference 3rd cited as detailed below:

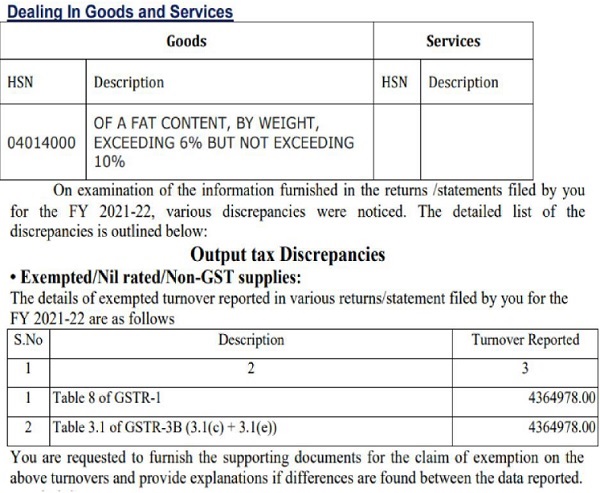

GST Exemption on Supply of Fresh and Unprocessed Milk:

Under Notification No. 2/2017-Central Tax (Rate), the Government has specified a list of goods that are exempt from the levy of GST. Among the entries covered under this notification, fresh milk or raw milk is specifically treated as an exempt supply. Where the milk is supplied in its natural and unprocessed form, without any addition of sugar, flavouring agents, or other substances, such supply attracts a NIL rate of tax. Accordingly, the sale of fresh or raw milk, being unprocessed in nature, does not attract GST and is treated as an exempt supply under the GST law.

Non-Mandatory Registration under Section 23 of the CGST Act, 2017

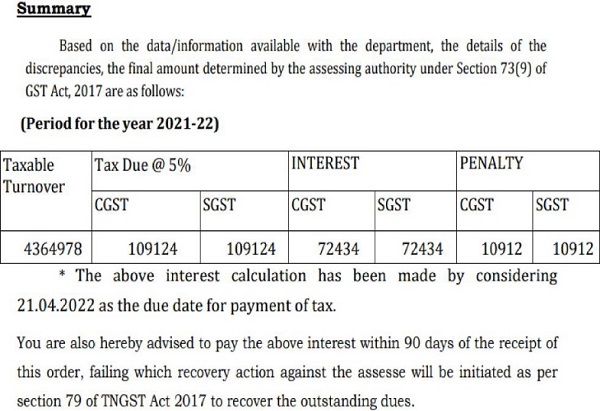

Under Section 23 of the CGST Act, 2017, a person engaged exclusively in the supply of goods or services that are wholly exempt from tax is not liable to obtain GST registration. This statutory exemption applies irrespective of the aggregate turnover threshold prescribed under Section 22. In the present case, KR Agencies had an annual turnover of ₹43,64,978 for the financial year 2021–2022. Although the turnover exceeded ₹40 lakhs, if the nature of the business was confined exclusively to the sale of unprocessed milk, which is an exempt supply under GST, registration was not legally mandatory. Therefore, notwithstanding the turnover crossing the threshold limit, KR Agencies was not required to obtain GST registration, provided its outward supplies consisted solely of exempt goods.

Declared Nature of Business Activity at the Time of GST Registration

At the time of obtaining GST registration, KR Agencies declared its principal business activity as dairy farming and the sale of milk. The entity stated that it maintained approximately 40 milch cows for milk production and supplied the milk directly to end consumers, most of whom were unregistered under the GST regime, thereby constituting business-to-consumer (B2C) transactions. It was further declared that the milk sold was unprocessed and supplied in its natural form without any value addition or processing. This declaration establishes that the nature of the business was primarily agricultural and dairy-oriented, with outward supplies consisting predominantly of exempt B2C sales.

Department’s Grounds for Suspicion and Subsequent Proceedings

The department appears to have suspected the transactions for multiple reasons. First, KR Agencies was not legally required to obtain GST registration, considering the nature of its business activity, namely the sale of unprocessed milk, which is generally treated as an exempt supply under GST. Second, the annual volume of B2C transactions reported as exempt supplies amounted to approximately ₹43 lakhs, which may have raised concerns in the department’s view regarding the genuineness and classification of such supplies.

Another significant reason for the department’s suspicion appears to be the location of the principal place of business. The registered place of business is situated in an area widely known for “Palkova”, a traditional milk-based sweet product prepared from processed milk. This may have led the department to suspect that the transactions were not confined solely to the sale of raw or unprocessed milk, but could also involve the manufacture and sale of processed milk products. On this basis, the department appears to have considered the supply under HSN Code 04014000, relating to milk and cream of a fat content, by weight, exceeding 6% but not exceeding 10%, which attracts GST at 5%.

Further, if Palkova is in fact manufactured and sold through a retail shop, such supply would constitute a taxable outward supply under the GST law. In such circumstances, where the annual aggregate turnover exceeds ₹40 lakhs, GST registration becomes mandatory under Section 22 of the CGST Act, 2017, irrespective of whether the sales are made to registered persons (B2B) or unregistered customers (B2C). Therefore, the department’s suspicion may also stem from the possibility that the business activity involved taxable processed milk products rather than exclusively exempt supplies of raw milk.

Timeline of GST Proceedings Initiated Against KR Agencies

| Departmental Notices and Final GST Proceedings | ||||

| Sl. No. |

Date | Form / Proceeding | Purpose / Description | Response Status |

| 1 | 25.08.2025 | GST ASMT-10 | Initial scrutiny notice issued seeking clarification regarding the nature of supplies and exempt turnover reported | No response received |

| 2 | 25.09.2025 | GST DRC-01 | Show cause notice issued proposing tax demand under Section 73 due to non-submission of explanation | No response received |

| 3 | 06.11.2025 | Personal Hearing Notice (1st) | Opportunity provided to appear and explain the transactions through common portal | No appearance |

| 4 | 07.11.2025 | Registered Post Notice | Notice also served through RPAD with acknowledgement card | No response received |

| 5 | 14.11.2025 | Personal Hearing Notice (2nd) | Second opportunity for personal hearing | No appearance |

| 6 | 24.11.2025 | Personal Hearing Notice (3rd) | Final opportunity for personal hearing | No appearance |

| 7 | 26.12.2025 | GST DRC-07 | Final demand order issued confirming tax, interest, and penalty | Demand confirmed |

Based on these concerns, the department initially issued a notice in Form GST ASMT-10 dated 25.08.2025 seeking clarification. As no response was received from KR Agencies, a show cause notice in Form GST DRC-01 was subsequently issued on 25.09.2025.

Further, personal hearing notices, as referred to in the 4th, 5th, and 6th references, were issued through the common portal on 06.11.2025, 14.11.2025, and 24.11.2025, respectively. In addition, a notice was also sent through Registered Post with Acknowledgement Card No. XXXXX dated 07.11.2025.

Since no reply or appearance was made by KR Agencies in response to any of the notices, the department appears to have presumed that its suspicion was valid and, accordingly, issued the final demand order in Form GST DRC-07 on 26.12.2025.

What KR Agencies Should Have Actually Done

KR Agencies should have responded to the GST ASMT-10 notice and submitted the relevant documents to establish that the supplies consisted of unprocessed milk. Such supporting documents should have included sales invoices / daily milk bills, the milk production register, bank statements, books of account, and proof of ownership of cows, along with any other records required or specifically called for by the department. Timely submission of these documents would have enabled the taxpayer to substantiate the claim that the supplies were exempt in nature and could have potentially avoided the subsequent demand proceedings.

Estimated Cost Incurred by KR Agencies to Neutralize the DRC-07 Order

1) Statutory Pre-deposit for Filing Appeal

| Particulars | Amount (₹) |

| CGST (Disputed Tax) | 1,09,124 |

| SGST (Disputed Tax) | 1,09,124 |

| Total Tax in Dispute | 2,18,248 |

| Mandatory pre-deposit @ 10% | 21,825 |

Note: The above amount is required to be deposited online at the time of filing the appeal under Section 107(6) of the TNGST / CGST Act, 2017. This statutory pre-deposit is a mandatory condition for admission of the appeal before the Appellate Authority.

Note: The statutory pre-deposit may be treated as a practical cost because it requires an immediate outflow of funds for filing the appeal. Although it is not a final expense and may be adjusted or refunded depending on the outcome, it temporarily blocks the taxpayer’s working capital. Hence, it is considered a litigation and cash flow cost for challenging the order.

2) Total Estimated Cost

| Particulars | Amount (₹) |

| Mandatory pre-deposit | 21,825 |

| Professional fees | 25,000 |

| Documentation / incidental expenses | 5,000 |

| Total estimated cost | 51,825 |

Note: Accordingly, KR Agencies may incur an approximate cost of ₹50,000 to ₹55,000 to effectively challenge and neutralize the order passed in Form GST DRC-07 before the Appellate Authority.

Professional Opinion / Conclusion

In my professional opinion, this case underscores the critical importance of timely compliance with statutory notices issued under the GST law. Any notice received from the GST department should be responded to within the prescribed time limit, as failure to do so may lead to avoidable litigation, additional compliance costs, interest, penalty, and blockage of working capital.

Further, where a taxpayer is engaged exclusively in the business of supplying unprocessed milk, which constitutes an exempt supply under the GST framework, registration may not be mandatory under Section 23 of the CGST Act, 2017, even if the aggregate turnover exceeds ₹40 lakhs. Therefore, proper understanding of the nature of business activity, supported by adequate documentation and prompt response to departmental notices, is essential to prevent unnecessary disputes and financial burden.

Author Bio