Reconciling E-Way Bill Data with GSTR-9C Turnover: A Practical Approach to Handling Audit Notices

Introduction

During audits conducted by the Goods and Services Tax Department, taxpayers often receive notices when there is a significant mismatch between the value reported in outward E-Way Bills and the sales turnover as per GSTR-9C (Books of Accounts). For example, for the financial year 2021–22, the taxpayer had generated 745 outward E-Way Bills covering an assessable value of ₹25,42,66,643, whereas the total turnover as per GSTR-9C was ₹46,21,85,077. This raised a difference of ₹20,79,18,434 and triggered an audit notice from the department.

Such notices primarily aim to ensure that all outward supplies involving movement of goods are duly supported by E-Way Bills, and to rule out any possibility of suppression or underreporting of sales. However, this difference does not always indicate tax evasion – it often arises due to clerical errors, reporting gaps, or business-specific operational reasons.

Response to the Audit Notice

While replying to such a notice, it is important to present a clear reconciliation between the turnover reported in books (GSTR-9C) and the value reported in E-Way Bills, explaining why certain sales are not covered under E-Way Bill provisions. The reconciliation should classify and deduct categories of turnover that do not involve physical movement of goods or are exempt from E-Way Bill generation.

| Audit Notice | ||||

| Year | No. of outward E-Way Bills |

Assessable Value (₹) | Sales Turnover as per GSTR-9C (₹) | Difference between GSTR-9C and E-Way Bill (₹) |

| 2021-22 | 745 | 25,42,66,643 | 46,21,85,077 | 20,79,18,434 |

–

| Reconciliation Statement | |

| Particulars | Amount (₹) |

| Total Turnover as per GSTR-9C (Books) | 46,21,85,077 |

| Less: Pure services supplied | -5,00,00,000 |

| Less: Service related to goods (installation, testing, commissioning) | -3,00,00,000 |

| Less: After-sale support services (repairs, AMC) | -2,00,00,000 |

| Less: Invoices ≤ ₹50,000 (small supplies) | -4,00,00,000 |

| Less: Local deliveries within 20 km using own vehicle/DC | -3,00,00,000 |

| Less: Walk-in consumers carried goods themselves | -2,79,18,434 |

| Less: Stock transfers without physical movement of goods (only book entry) | -1,00,00,000 |

| Reconciled value (covered under E-Way Bill) | 25,42,66,643 |

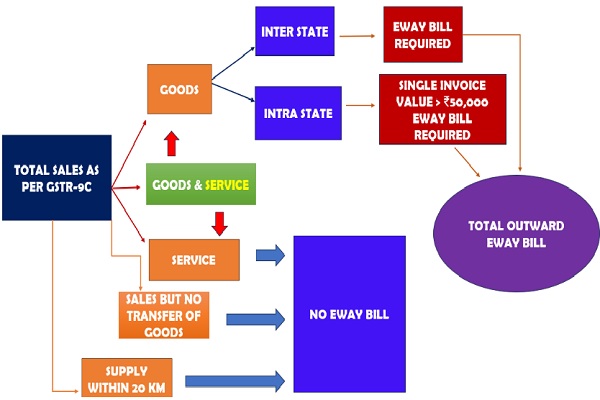

Transactions Not Requiring E-Way Bill

1. Pure Services Supplied

Pure service supplies refer to transactions consisting solely of services without any accompanying goods, such as consultancy, design services, training, software development, or professional fees. Under Rule 138 of the Central Goods and Services Tax Rules, 2017, an E-Way Bill is required only when there is a movement of goods and the consignment value exceeds ₹50,000. Since pure services do not involve any physical movement of goods, the requirement to generate an E-Way Bill does not arise. Logically, as there are no goods being transported, only invoices issued, these transactions fall completely outside the ambit of E-Way Bill compliance.

2. Services Related to Goods (Installation, Testing, Commissioning)

Services related to goods such as installation, testing, and commissioning typically involve carrying out work at the customer’s premises using minimal tools or consumables owned by the service provider, without any transfer of goods ownership. When only service charges are billed and no goods are supplied as part of the invoice, Rule 138 does not mandate E-Way Bill generation. As per Schedule II of the Central Goods and Services Tax Act, 2017, these are classified as services, and there is no movement of goods pursuant to the supply. Accordingly, such service-only activities are outside the scope of E-Way Bill provisions.

3. After-Sale Support Services (Repairs, AMC)

After-sale support services such as annual maintenance contracts (AMC), servicing, and repairs are primarily labour-oriented activities, often involving negligible or no movement of parts. Where only service charges are billed or any spares used are of insignificant value and do not individually cross the threshold of ₹50,000, E-Way Bills are not mandatory under Rule 138. As the dominant nature of the supply is service, and any incidental goods used are not separately invoiced as outward supplies, these transactions do not trigger the requirement to generate an E-Way Bill.

4. Walk-in Consumers Carrying Goods Themselves — Legal PerspectiveUnder Rule 138 of the CGST Rules, 2017, every registered person is legally obligated to generate an E-Way Bill for any outward movement of goods where the consignment value exceeds ₹50,000, irrespective of whether the supply is GST B2B or B2C. The obligation arises solely on the basis of value and movement, not on who arranges the transport or the physical size of the goods.Accordingly, even in walk-in sales where the customer personally collects and transports the goods, the supplier is deemed to cause the movement as part of the supply transaction. In such instances, the supplier is expected to generate the e-way bill by selecting “Self” as mode of transport and, where possible, indicating the vehicle number or marking “hand delivery”. The fact that many suppliers do not practically generate e-way bills for small, high-value items (e.g., jewellery, electronics) does not dilute this legal requirement.

Therefore, if a customer purchases, for example, a gold necklace worth ₹8,00,000 and carries it home in their own vehicle, the legal requirement still mandates the supplier to generate an e-way bill because the transaction involves the movement of goods of value exceeding the prescribed threshold.

5. E-Way Bill Compliance: Threshold Applicability in Intra-State and Inter-State Movement

Under Rule 138 of the CGST Rules, 2017, the requirement to generate an e-way bill is linked to the nature of supply and the value of goods. For intra-state transactions, an e-way bill becomes mandatory only when the consignment value exceeds ₹50,000, although some States have prescribed higher limits. In contrast, for inter-state movement of goods, there is no threshold exemption—an e-way bill must be generated irrespective of the value involved. Certain specified goods and cases notified under Rule 138(14), such as exempt goods or movement by non-motorised conveyance, are excluded from this requirement.

6. Stock Transfers Without Physical Movement: Legal Logic, Practical Scenarios, and E-Way Bill Implications

In certain situations, a stock transfer may occur without the physical movement of goods. This generally arises in two ways:

1.Transfers between distinct persons under Section 25(4) of the CGST Act – where ownership is shifted between GST registrations even though the goods remain in the same warehouse.

2. Business models involving out-of-state procurement with in-state warehousing – where a buyer procures goods from another state but chooses to retain stock at the supplier’s or a rented warehouse in that state to cater to local customers directly.

Since there is no physical movement of goods, the generation of an e-way bill is not required. However, this often results in a mismatch between outward e-way bill data and the total sales reflected in GSTR-9C, because certain transactions (like stock transfers without movement) appear in returns but not in the e-way bill system. Therefore, suppliers are generally required to reconcile such differences and provide clarifications during departmental scrutiny to substantiate that the outward tax liability has been correctly discharged, even if the corresponding E-Way Bills are absent.

7. E-Way Bill Exemption for Short-Distance Movement (Within 20 km)

As per Rule 138(14)(d) of the CGST Rules, 2017, no e-way bill is required when goods are transported for a distance of up to 20 kilometers from the place of business of the consignor to a weighbridge for weighment or from the weighbridge back to the consignor’s premises, provided such movement is accompanied by a delivery challan.

Further, several states (through respective notifications) have also relaxed the requirement of generating e-way bills for intra-state movements within a 20 km radius, particularly in cases of movement to and from transporters’ godowns or for temporary storage.

Thus, when the supplier is located within 20 km, and the movement falls within these notified relaxations, the generation of an e-way bill is not mandatory. This exemption is intended to ease compliance for short-distance movement and avoid unnecessary procedural burden while ensuring traceability through delivery challans.

Chart 01

8. Clerical Errors and Lack of Coordination as a Cause for Mismatches

Discrepancies between outward supplies reported in GSTR-1 and corresponding E-Way Bill data often arise from clerical mistakes and inadequate inter-departmental coordination rather than deliberate non-compliance. While Section 37 of the CGST Act, 2017 read with Rule 59 of the CGST Rules, 2017 requires accurate reporting of outward supplies, and Rule 138 of the CGST Rules, 2017 mandates e-way bill generation for goods above the threshold, operational lapses such as incorrect invoice values, wrong vehicle details, or missing linkages often create mismatches between the GSTN and E-Way Bill System.

Because these two systems function independently without automated reconciliation, even minor errors can trigger departmental scrutiny under Section 61 of the CGST Act, 2017 or audits under Section 65 of the CGST Act, 2017. To prevent such issues, taxpayers should adopt robust internal controls, inter-departmental checks, and periodic reconciliations, enabling them to substantiate that tax liabilities have been properly discharged despite any apparent gaps in e-way bill compliance.

Practical Illustration 01: Mismatch Due to Clerical Error & Coordination GapsBackground:XYZ Pvt Ltd is a registered dealer of industrial machinery. The company has multiple internal departments — Sales, Accounts, Logistics, and Taxation.

Transaction Scenario:

On 15 June 2024, the Sales team raises a tax invoice for ₹12,00,000 for supply of machinery to ABC Industries (a registered customer in another state).The Accounts team uploads the invoice in GSTR-1 under Section 37 of the CGST Act, 2017 and Rule 59 of the CGST Rules, 2017.The Logistics team generates the e-way bill under Rule 138 of the CGST Rules, 2017 but mistakenly enters ₹1,20,000 instead of ₹12,00,000 in the consignment value field.

The vehicle number is also wrongly entered as the transporter’s old registration number.

Resulting Mismatch:

In the GSTN system, the GSTR-1 shows outward supplies of ₹12,00,000.

In the E-Way Bill System, the movement reflects only ₹1,20,000 and has an invalid vehicle number. During scrutiny under Section 61 of the CGST Act, 2017, the department identifies a mismatch and suspects possible tax evasion because goods worth ₹12,00,000 appear moved without a valid e-way bill.

Root Cause:

The Accounts and Logistics teams did not coordinate, and there was no internal verification of e-way bill data before dispatch.

The error was purely clerical, not an attempt to evade tax. However, it triggered a departmental query.

| Reconciliation Methodology | |

| Particulars | Amount (₹) |

| Total Turnover as per GSTR-9C (Books) | XXXX |

| Less: Pure services supplied | (XXXX) |

| Less: Service related to goods (installation, testing, commissioning) | (XXXX) |

| Less: After-sale support services (repairs, AMC) | (XXXX) |

| Less: Invoices ≤ ₹50,000 (small supplies) | (XXXX) |

| Less: Local deliveries within 20 km using own vehicle/DC | (XXXX) |

| Less: Walk-in consumers carried goods themselves | (XXXX) |

| Less: Stock transfers without physical movement of goods (only book entry) | (XXXX) |

| Reconciled value (covered under E-Way Bill) | XXXX |

Reconciliation Methodology — Outward Supplies vs E-Way Bill CoverageThis reconciliation framework is designed to align the outward turnover reported in GSTR-9C with the values reported through the E-Way Bill system, ensuring compliance and data integrity.

1.Establish the Base Value

The reconciliation exercise begins with the total outward turnover as reported in the audited financial statements and GSTR-9C. This figure represents the comprehensive base value, encompassing all types of supplies made during the financial year, including goods, services, and stock transfers. Using this as a starting point ensures that the reconciliation covers the complete scope of outward supplies recorded in the books of accounts.

2. Identify and Eliminate Non-Movable Supplies

The next step involves isolating and excluding those elements of turnover that do not involve the physical movement of goods and therefore do not fall within the ambit of E-Way Bill requirements. This primarily includes pure services such as consultancy and annual maintenance contracts, service components linked to goods such as installation, testing, and commissioning, and after-sale support services where any movement of goods is incidental or negligible. These categories are treated as service income and are outside the operational purview of E-Way Bill compliance.

3. Apply Regulatory and Operational Exemptions

After removing service-related income, the reconciliation applies the specific exemptions prescribed under the E-Way Bill Rules. Certain supplies involving the movement of goods are not mandatorily covered under the E-Way Bill mechanism, such as supplies with invoice values below ₹50,000, local deliveries within 20 kilometres using the supplier’s own conveyance, and goods collected by walk-in customers themselves. These categories are legitimately excluded from the population of transactions expected to have E-Way Bills.

4. Remove Notional or Non-Physical Transfers

Additionally, the methodology excludes book adjustments that do not entail the actual movement of goods. This includes stock transfers recorded purely for accounting or internal valuation purposes without physical dispatch from one location to another. Since these transactions do not trigger any logistical movement, they are not relevant for E-Way Bill reporting and are removed from the reconciliation base.

5. Derive the E-Way Bill-Relevant Turnover

The residual value remaining after all these exclusions represents the segment of outward supplies that actually necessitate E-Way Bill generation. This figure reflects the genuine movement-based supplies and is expected to align with the outward supply data captured in the E-Way Bill portal. Reconciling this figure ensures that the records reported in statutory returns and those captured in the E-Way Bill system are consistent and reliable.

Objective of the Methodology

This structured methodology ensures that only eligible and movement-based outward supplies are considered while reconciling with the E-Way Bill system. It improves data accuracy between statutory filings and logistical documentation, establishes a robust audit trail to support departmental scrutiny, and facilitates the identification of potential gaps or non-compliance in E-Way Bill generation. Overall, it enhances the integrity and reliability of GST reporting and compliance processes.

Conclusion

Receiving an audit notice for differences between E-Way Bill data and GSTR-9C turnover can initially seem alarming. However, such mismatches are common and usually result from legitimate business activities that are either not required to be covered under E-Way Bill provisions or involve non-movement-based accounting entries. A properly prepared reconciliation statement, supported by documentary evidence, will help the taxpayer satisfactorily explain the difference to the audit officer and avoid any unnecessary tax demand or penalty. Timely and accurate reconciliation ensures compliance and builds trust during departmental audits.

Author Bio