Summary: The article explains the TDS obligations applicable to individual tenants under Section 194-IB of the Income-tax Act, 1961, where monthly rent exceeds ₹50,000. It clarifies that tenants who are not liable to tax audit must deduct TDS at 2% and deposit it through the prescribed challan-cum-statement mechanism without obtaining a TAN. The article highlights that, in cases of jointly owned properties, the threshold should be examined separately for each co-owner based on ownership share or agreed allocation, which may avoid TDS liability if each share remains below ₹50,000 per month. It further outlines the one-time annual deduction mechanism, procedural steps for filing Form 141 (earlier Form 26QC), and deductor and deductee compliance requirements under theIncome Tax Act 2025 framework. The piece warns that non-compliance may result in interest, penalties, notices, and other consequences, especially with increasing digital reporting and PAN-based compliance monitoring by tax authorities.

Paying house rent is a routine financial commitment for many individuals. However, what often goes unnoticed is that the Income-tax law may also cast a TDS compliance obligation on the tenant. Even individual tenants may be required to deduct tax at source where the prescribed conditions are satisfied.

Lack of awareness about this compliance requirement can result in interest, late fees, Income Tax Notices and unnecessary hassles.

This article seeks to decode the provision from a tenant’s practical perspective.

TDS provisions applicable to an individual paying house rent

Section 194-IB of the Income Tax Act, 1961 requires an individual / HUF (not liable to tax audit) paying rent exceeding Rs. 50,000 for a month or part of a month to deduct tax at source at the prescribed rate of 2%.

Higher TDS consequences may arise in specified cases where a valid PAN is unavailable, subject to the applicable legal provisions.

What if the rented property has multiple co-owners?

If the rented property is jointly owned by two or more persons, the tenant should consider the rent payable to each landlord individually, rather than the total rent for the property. Therefore, if rent paid to each owner remains within the prescribed threshold, TDS under section 194-IB may not be applicable.

Illustration:

Suppose the monthly rent for a residential property is ₹90,000, and the property is jointly owned by Mr A and Mrs B, each having an equal 50% share. In such a case, rent attributable to each co-owner would be ₹45,000 per month. Since the rent payable to each individual landlord does not exceed the prescribed threshold of ₹50,000 per month, TDS under section 194-IB may not be attracted, subject to the underlying ownership arrangement and supporting documentation.

Rent allocation among Co-owners:

If the rented property is jointly owned by multiple landlords, the tenant should evaluate the TDS threshold based on the rent payable to each landlord separately. Such allocation should be based on the respective ownership shares or on an agreed rent-sharing agreement among the co-owners.

When should the tenant deduct TDS?

TDS is required to be deducted in March (being the last month of the financial year). However, if the tenancy ends earlier, TDS should be deducted in the last month of the tenancy.

Thus, unlike many other TDS provisions, deduction is generally a one-time annual compliance rather than a monthly obligation.

TAN not required – a welcome relief for tenants

Unlike many other TDS provisions, Section 194-IB does not require the tenant to obtain a TAN for deducting tax on rent. Compliance can be completed using the tenant’s PAN through the prescribed challan-cum-statement mechanism (Form 26QC under the existing law / corresponding Form 141 under the new law).

Important Note: Since the Income-tax Act, 2025, becomes effective from 1 April 2026, the screenshots in this article reflect the updated portal architecture, section references and Form nomenclature. Accordingly, references to section 194-IB / Form 26QC should be read alongside the corresponding provisions under the new law, i.e., section 393(1) / Form 141, wherever applicable.

Step-by-Step Procedure to File Form 141 (Earlier Form 26QC) for TDS on Rent

Once TDS has been deducted, the tenant is required to deposit the same with the Government by filing Form 26QC (Challan cum statement). Since many first-time users may find the process slightly technical, the step-by-step procedure is explained below with a screenshot for ease of reference:

Step 1 – Log in to the Income Tax Portal

Path:

Login → e-File → e-Pay Tax.

Upon selecting e-Pay Tax, the portal displays the available options under:

- Income-tax Act, 1961

- Income Tax Act 2025

Select Income-tax Act, 2025.

Step 2 – Initiate New Payment

After selecting Income-tax Act, 2025, click “New Payment” to proceed.

| e-pay Tax | +New Payment |

Step 3 – Select Form 141 and Type of Assessee

Under the available payment/statement options, select: Form 141 – Challan-cum-Statement for TDS. Thereafter, select the applicable Type of Assessee (e.g., Corporate / Non-Corporate, as applicable) to proceed further.

Step 4 – Enter Basic Transaction Details:

Enter the tax year of the transaction & the month of deduction.

Select the applicable Nature of Transaction from the dropdown menu.

Step 5 – Enter Property / Rent Transaction Details

Provide the property details, including the type of property (land/building / both) and the property address.

Step 6 – Enter Deductor (Tenant) Details:

Although the tenant’s PAN and name are auto-filled based on the login credentials, the proportion of rent attributable to the tenant must be entered manually by selecting “Edit.” In the case of a sole tenant, the share should ordinarily be entered as 100%, as the system does not allow progression with a blank allocation.

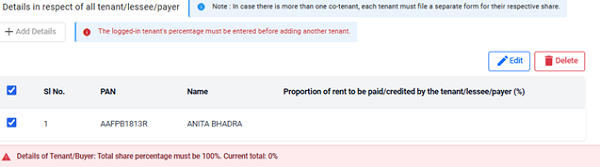

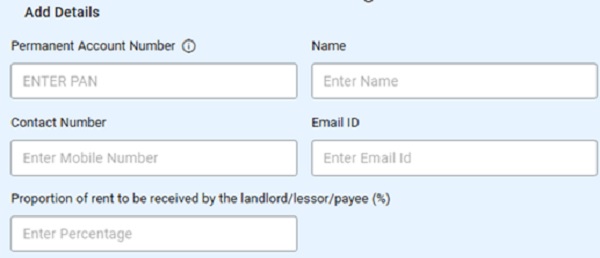

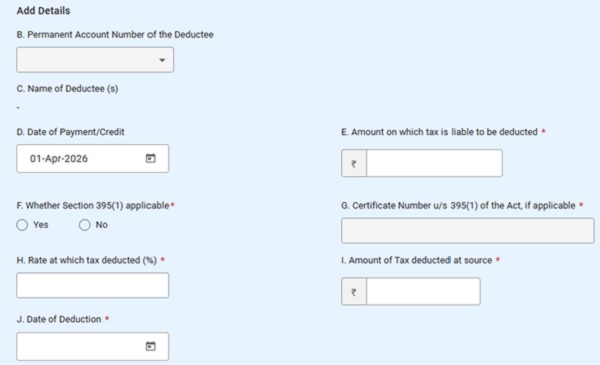

Step 7 – Enter Deductee ( Landlord) Details:

Click “Add Details” and enter the particulars of the landlord/lessor/payee, including PAN, name, contact details, email ID and proportion of rent receivable. When the property is jointly owned, each co-owner’s share should be carefully entered, ensuring the aggregate allocation totals 100%.

| Note: In cases involving multiple landlords, deductee-wise TDS details should be entered separately for each deductee in accordance with the rent share allocation. |

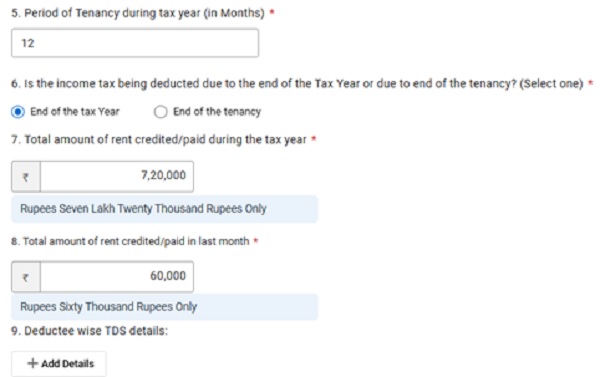

Step 8 – Enter Rent Transaction Details:

Enter the period of tenancy during the relevant tax year (in months) and select the reason for deduction, i.e., end of the tax year or end of tenancy, as applicable. Thereafter, furnish the total rent credited/paid during the tax year, the rent pertaining to the last month, and click “Add Details” to enter deductee-wise TDS particulars.

Upon selecting “Add Details,” enter the TDS particulars for each deductee. Select the relevant PAN from the dropdown (the corresponding name is auto-populated). Thereafter, furnish the taxable amount, applicable TDS rate, tax deducted and relevant dates.

| If the deductee possesses a valid certificate under section 395(1) authorising lower or nil deduction of tax, the relevant details should be furnished in the specified field. |

Step 9 – Payment of Tax

After verifying the challan-cum-statement details, proceed to pay the applicable tax using the available payment modes on the portal (such as net banking / other permitted electronic payment options). Upon successful payment, the challan acknowledgement/transaction details should be downloaded and retained for record purposes.

After successful filing/payment, the tenant should also ensure that the applicable TDS certificate is generated/issued for the landlord within the prescribed timeline.

TDS Compliance Responsibility Ultimately Rests with the Tenant

Merely paying rent does not discharge the statutory obligation where tax deduction provisions are applicable. The responsibility to deduct tax at source and deposit the same with the Government within the prescribed timeline rests with the tenant/payer.

Failure to comply may attract consequences such as:

- Interest for non-deduction / delayed deduction of tax

- Interest for delay in deposit of the deducted tax

- Penalty / other consequences under the applicable provisions of the Income-tax Act

Practical Reality – A Common Compliance Gap

A frequent practical misconception is that individual tenants claiming House Rent Allowance (HRA) and reporting rent payments in salary/tax records often assume that disclosing rent payments alone is sufficient compliance.

However, where the applicable threshold and conditions for TDS are satisfied, mere disclosure of rent payments or HRA claims does not discharge the obligation to deduct and deposit tax.

With increasing data integration through PAN-based reporting, AIS/tax information systems, salary disclosures, and digital compliance tracking, practical instances are increasingly being observed in which taxpayers receive communications/notifications regarding non-compliance with TDS obligations on rent payments.

Common Practical Compliance Mistakes

Assuming HRA disclosure is sufficient compliance

- Ignoring TDS because rent is paid to an individual landlord

- Missing TDS where rent exceeds threshold

- Incorrect allocation in case of multiple co-owners

- Delayed filing of challan-cum-statement

Quick FAQs

Q1. Is a monthly TDS deduction required?

Ans: No. Under section 194-IB, deduction is generally required in the last month of the financial year or tenancy, as applicable.

Q2. Is TAN required?

Ans: No.

Q3. If rent is paid to co-owners, should the threshold be checked jointly?

Ans: As a general principle, the threshold should be examined with reference to each co-owner separately..

Q4.What if TDS was not deducted earlier?

Ans: Delay in deduction or deposit may attract interest and other consequences under the applicable provisions. Appropriate corrective action should be considered at the earliest.

Conclusion:

Paying rent is one compliance event; deducting and depositing tax, where legally required, is a separate statutory obligation. Ignoring this distinction may prove costly.

Disclaimer: This article is intended solely for educational and informational purposes and should not be construed as professional advice.

The author can be approached at caanitabhadra@gmail.com

Author Bio

What is code of TDS on Contract (freight paid to Individual) and were found in challan generation

Hai, I am going to USA next month to seems son, sone persons are saying that we have to submit form 156 or so before going to USA if so details and format of form no 156 or so,I checked in website i didn’t find please