Introduction

The complexities of GST compliance present formidable challenges, especially for taxpayers grappling with financial instability. To alleviate these challenges, the GST framework offers a crucial remedy through Section 80 and Rule 158 of the CGST Act: deferred payment options. These provisions empower taxpayers to address tax liabilities methodically, enabling instalment payments with accrued interest as governed by Section 50 of the CGST Act.

This article delves into the strategic application of Section 80, highlighting its pivotal role in easing immediate financial burdens for taxpayers. It explores the procedural nuances of filing Form GST DRC-20, essential for initiating deferred payment plans subsequent to the issuance of a Recovery ID against a Demand ID. Furthermore, the discussion extends to the application of Section 80 and Rule 158 in contexts such as orders under Section 74 of the CGST Act, elucidating maximum instalment allowances and requisite information for completing Form DRC-20.

By offering comprehensive insights and practical alternatives under Section 80, this article equips taxpayers with actionable strategies to navigate GST obligations effectively. It underscores the importance of leveraging these provisions judiciously to foster financial resilience and ensure steadfast adherence to GST regulatory frameworks.

To enhance clarity, we will examine the following topics:

I. Case Study

II. Section 80 and Rule 158 of the CGST Act

III. Filing Form GST DRC-20 after generating a Recovery ID against a Demand ID

IV. Application of Section 80 and Rule 158 to orders issued under Section 74 of the CGST Act

V. Understanding the Maximum Instalments Allowed Under Section 80 of the CGST Act

VI. Essential Information to be Filled in Form DRC-20

VII. Applicability of Section 50 of the CGST Act for Deferred Payment Under Section 80 of the CGST Act 2017

VIII. Alternative remedies to Form GST DRC-20 under Section 80 of the CGST Act

(i) Case Study

Case Background:

Background

Mr. A runs a steelmaking business. In January 2022, he incurred an output tax liability amounting to ₹3,11,000/-. Mr. A successfully filed the GSTR-1 within the due date but failed to file the GSTR-3B return due to financial struggles. Furthermore, his buyer did not release the full payment, exacerbating his financial situation. Due to these challenges and the impact of COVID-19, Mr. A was unable to pay the tax liability.

Cancellation of GST Registration

The GST department, after issuing notices, issued an order under Section 73 on 01.05.2024 to Mr. A to pay the outstanding tax liability along with a penalty and interest totalling ₹70,000 (making the total due ₹3,81,000), and proceeded to cancel his GST registration.

Legal Proceedings

The department issued an order under Section 73 of the CGST Act, accompanied by a show cause notice. Following this, a demand ID was generated, and subsequently, a recovery ID was also generated.

Consultation

In light of these developments, Mr. A approached a tax consultant to explain his situation and seek advice on how to proceed.

(ii) Section 80 and Rule 158 of the CGST Act:

Section 80. Payment of tax and other amount in instalments. –

On an application filed by a taxable person, the Commissioner may, for reasons to be recorded in writing, extend the time for payment or allow payment of any amount due under this Act, other than the amount due as per the liability self-assessed in any return, by such person in monthly instalments not exceeding twenty-four, subject to payment of interest under section 50 and subject to such conditions and limitations as may be prescribed:

Provided that where there is default in payment of any one instalment on its due date, the whole outstanding balance payable on such date shall become due and payable forthwith and shall, without any further notice being served on the person, be liable for recovery.

Rule 158. Payment of tax and other amounts in instalments. –

(1) On an application filed electronically by a taxable person, in FORM GST DRC- 20, seeking extension of time for the payment of taxes or any amount due under the Act or for allowing payment of such taxes or amount in instalments in accordance with the provisions of section 80, the Commissioner shall call for a report from the jurisdictional officer about the financial ability of the taxable person to pay the said amount.

(2) Upon consideration of the request of the taxable person and the report of the jurisdictional officer, the Commissioner may issue an order in FORM GST DRC- 21 allowing the taxable person further time to make payment and/or to pay the amount in such monthly instalments, not exceeding twenty-four, as he may deem fit.

(3) The facility referred to in sub-rule (2) shall not be allowed where-

(a) the taxable person has already defaulted on the payment of any amount under the Act or the Integrated Goods and Services Tax Act, 2017 or the Union Territory Goods and Services Tax Act, 2017 or any of the State Goods and Services Tax Act, 2017, for which the recovery process is on;

(b) the taxable person has Not been allowed to make payment in instalments in the preceding financial year under the Act or the Integrated Goods and Services Tax Act, 2017 or the Union Territory Goods and Services Tax Act, 2017 or any of the State Goods and Services Tax Act, 2017;

(c) the amount for which instalment facility is sought is less than twenty-five thousand rupees.

Compliance with Rule 158: Assessing Mr. A’s Eligibility for Deferred Payment under Section 80

Based on Section 80 and Rule 158 of the CGST Act, Mr. A fulfils all the necessary conditions to apply for deferred payment under Form GST DRC-20.

Firstly, Mr. A has maintained a clean record by not defaulting on any payments under the CGST/IGST/UTGST/SGST Act, 2017, where the recovery process is ongoing. This demonstrates his compliance with tax payment obligations.

Secondly, according to Rule 158, the due amount of ₹3,81,000 as of FY 2021-2022 does not relate to the preceding financial year (FY 2023-2024). This distinction is crucial because Rule 158 specifies that the deferred payment option is intended for liabilities from the earlier financial years, not from the directly preceding financial year. Therefore, Mr. A’s tax liability due from FY 2021-2022 is considered under the category of “previous financial year” rather than “preceding financial year,” aligning with the rule’s conditions.

Thirdly, Rule 158(2) mandates that the amount due must exceed ₹25,000 for eligibility to apply for deferred payment. In Mr. A’s case, the outstanding amount of ₹3,81,000 significantly surpasses this threshold, meeting the financial criteria set forth in the rule.

In summary, Mr. A meet all the conditions specified in Rule 158 of the CGST Act: no defaults on payments, due amount not related to the directly preceding financial year but to a previous financial year, and the amount due exceeding ₹25,000. Therefore, he is eligible to proceed with applying for deferred payment of his tax liabilities through Form GST DRC-20.

(iii) Filing Form GST DRC-20 after generating a Recovery ID against a Demand ID

When a demand ID is followed by a recovery ID, it marks the beginning of the recovery process for outstanding tax dues. At this point, taxpayers may feel unsure about their options, particularly if they wish to request deferred payment terms. The key point to understand is that the CGST Act, through Section 80 and Rule 158, provides a framework for deferred payments without restricting eligibility based on the issuance of a recovery ID. This framework allows taxpayers to seek relief through instalment payments, thus providing a viable path to manage financial obligations even at the initial recovery stage.

Moreover, the issuance of Form GST DRC-09 does not preclude the taxpayer from applying for deferred payment. The Commissioner of GST has the discretionary power to permit the filing of Form GST DRC-20, which is essential for taxpayers seeking to defer their tax payments. This means that the process remains open and flexible, allowing taxpayers to approach the Commissioner with their request for deferred payment regardless of the stage in the recovery process.

In situations where the recovery ID has been generated and the taxpayer cannot apply for Form GST DRC-20 online, the taxpayer should not assume they are ineligible. Instead, they should approach the Commissioner of GST, providing the necessary documents that demonstrate their financial instability. The Commissioner, upon review and the recommendation of a judicial officer, has the discretion to permit the filing of Form GST DRC-20.

The CGST Act ensures that taxpayers have multiple avenues to manage their tax liabilities, emphasizing fairness and flexibility in tax administration.

(iv) Application of Section 80 and Rule 158 to orders issued under Section 74 of the CGST Act

Section 74. Determination of tax not paid or short paid or erroneously refunded or input tax credit wrongly availed or utilised by reason of fraud or any wilful- misstatement or suppression of facts. –

Section 74 sub section (1) Where it appears to the proper officer that any tax has not been paid or short paid or erroneously refunded or where input tax credit has been wrongly availed or utilised by reason of fraud, or any wilful-misstatement or suppression of facts to evade tax, he shall serve notice on the person chargeable with tax which has not been so paid or which has been so short paid or to whom the refund has erroneously been made, or who has wrongly availed or utilised input tax credit, requiring him to show cause as to why he should not pay the amount specified in the notice along with interest payable thereon under section 50 and a penalty equivalent to the tax specified in the notice.

Section 80 of the CGST Act provides taxpayers with the option to request deferred payment of their tax dues in instalments. Rule 158(2) further outlines the conditions under which such requests can be made. Importantly, neither Section 80 nor Rule 158(2) restricts eligibility based on the nature of the order—whether it is issued under Section 73, which deals with non-fraud cases, or Section 74, which pertains to fraud cases.

This means that taxpayers facing severe financial difficulties can still seek relief by applying for deferred payment in instalments, regardless of whether the tax demand was a result of fraud or not. The Commissioner of GST retains the discretion to grant this request based on an assessment of the taxpayer’s financial situation, ensuring that the option for deferred payment remains accessible to all eligible taxpayers.

(v) Understanding the Maximum Instalments Allowed Under Section 80 of the CGST Act

Rule 158 of Section 80 within the CGST Act allows taxpayers to seek deferred payment of their tax liabilities through instalment plans. According to this rule, taxpayers can request up to twenty-four instalments to spread out their payments, providing flexibility and easing the financial burden of lump-sum payments.

However, the Commissioner of GST retains discretionary authority in determining the number of instalments. This discretion is guided by several factors, including a report from a judicial officer assessing the taxpayer’s financial stability and the submission of relevant financial documents by the taxpayer. These documents typically include income statements, balance sheets, and other financial records that provide insight into the taxpayer’s ability to meet their tax obligations.

In practice, while the rule permits up to twenty-four instalments, it is more common for the Commissioner to approve a smaller number, often ranging between 5 to 7 instalments. This pragmatic approach ensures that instalment plans are manageable for taxpayers while still ensuring timely collection of taxes by the government and minimizing administrative burdens.

The limitation to 5 to 7 instalments strikes a balance between providing relief to taxpayers and maintaining effective tax administration. It ensures that instalment plans are structured to support taxpayer compliance and financial stability while aligning with the regulatory framework of the CGST Act.

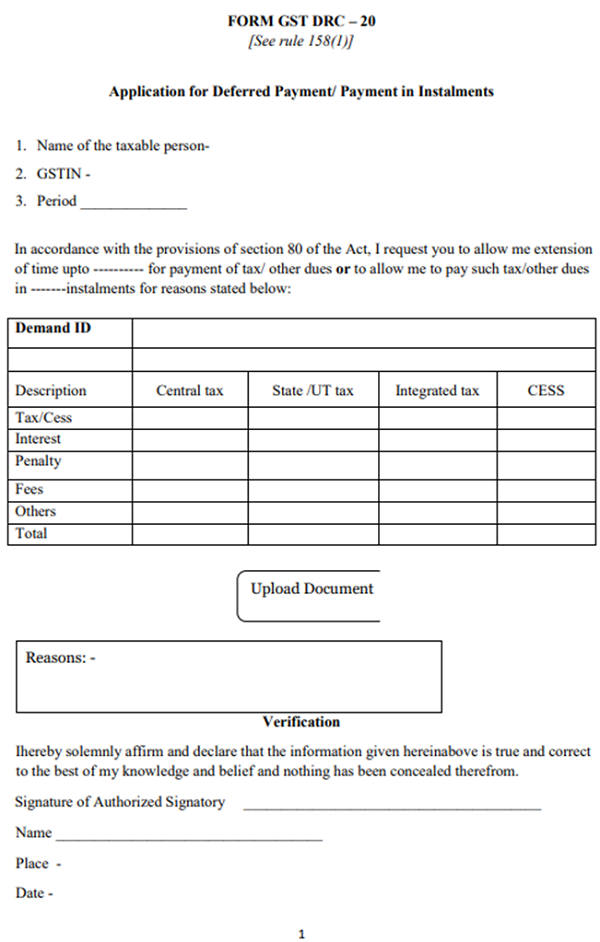

(vi) Essential Information to be Filled in Form DRC-20

Name and GST Number: Ensure that the details provided match those registered with the GST authorities to avoid discrepancies.

Number of Instalments Requested: This should be a realistic number based on the taxpayer’s financial situation and should consider the guidelines provided by the GST Commissioner.

Amount Due as CGST, SGST, IGST: Break down the total due amount into its components (CGST, SGST, IGST) accurately to reflect the tax liabilities under each category.

Reason for Deferred Payment: Provide a clear and concise explanation for why deferred payment is being requested. This explanation helps the GST Commissioner understand the circumstances and make an informed decision.

Signature of the Authorized Signatory: The authorized signatory should sign the form to authenticate the request. This ensures accountability and compliance with GST regulations.

Submitting Form GST DRC-20 with accurate and complete information increases the likelihood of approval for deferred payment, providing relief to taxpayers facing financial challenges while ensuring compliance with tax obligations.

(vii) Applicability of Section 50 of the CGST Act for Deferred Payment Under Section 80 of the CGST Act 2017

Section 50. Interest on delayed payment of tax. –

(1) Every person who is liable to pay tax in accordance with the provisions of this Act or the rules made thereunder, but fails to pay the tax or any part thereof to the Government within the period prescribed, shall for the period for which the tax or any part thereof remains unpaid, pay, on his own, interest at such rate, not exceeding eighteen per cent., as may be notified by the Government on the recommendations of the Council:

Provided that the interest on tax payable in respect of supplies made during a tax period and declared in the return for the said period furnished after the due date in accordance with the provisions of section 39, except where such return is furnished after commencement of any proceedings under section 73 section 74 in respect of the said period, shall be levied on that portion of the tax that is paid by debiting the electronic cash ledger.

(2) The interest under sub-section (1) shall be calculated, in such manner as may be prescribed, from the day succeeding the day on which such tax was due to be paid.

(3) Where the input tax credit has been wrongly availed and utilised, the registered person shall pay interest on such input tax credit wrongly availed and utilised, at such rate not exceeding twenty-four per cent. as may be notified by the Government, on the recommendations of the Council, and the interest shall be calculated, in such manner as may be prescribed

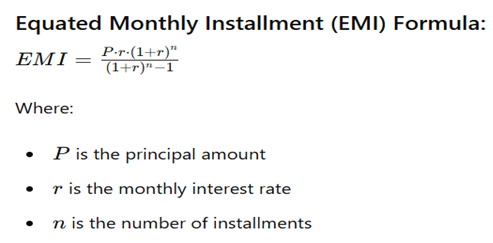

For example: Mr. A applied for deferred payment as per Section 80 and filed Form GST DRC-20 with the Commissioner of GST. The Commissioner of GST accepted the application and replied with Form GST DRC-21, approving 10 instalments at the rate of 18% on the total tax liability of Rs. 3,81,000.

Here we are going to work on finding the monthly instalment (Principal + Interest) for a period of 10 months.

Annual interest rate = 18% Therefore Monthly interest rate =(Annual interest rate / Month) 18%/12 = 1.5% (or) 0.015 per month

Principal amount Rs 3,81,000/-

Monthly Rate of Interest 1.5%

Number of Instalments 10

So substitute the value into the above formula we got a monthly instalment of Rs.41,235/-

| Instalment No. | Principal Payment | Interest Payment | Total Instalment | Remaining Principal |

| 1 | 35,520.88 | 5,715.00 | 41,235.88 | 3,45,479.12 |

| 2 | 36,053.69 | 5,182.19 | 41,235.88 | 3,09,425.43 |

| 3 | 36,594.50 | 4,641.38 | 41,235.88 | 2,72,830.93 |

| 4 | 37,143.42 | 4,092.46 | 41,235.88 | 2,35,687.51 |

| 5 | 37,700.57 | 3,535.31 | 41,235.88 | 1,97,986.94 |

| 6 | 38,266.08 | 2,969.80 | 41,235.88 | 1,59,720.86 |

| 7 | 38,840.07 | 2,395.81 | 41,235.88 | 1,20,880.79 |

| 8 | 39422.67 | 1813.21 | 41235.88 | 81458.12 |

| 9 | 40,014.01 | 1,221.87 | 41,235.88 | 41,444.11 |

| 10 | 40,614.22 | 621.66 | 41,235.88 | 829.89 |

Suppose Default in Payment of Sixth Instalment under Section 80 of the CGST Act

If Mr. A default in the payment of the sixth instalment as per Section 80 of the CGST Act, the entire outstanding balance becomes immediately due and payable on the date of default. According to the provisions, default in payment of any one instalment on its due date triggers the immediate demand for the whole outstanding balance. This balance becomes due without any further notice being served to the defaulter and is liable for recovery.

In this case, the whole outstanding balance payable on the date of default is Rs. 1,97,986.94.

(viii) Alternative remedies to Form GST DRC-20 under Section 80 of the CGST Act

The third option for Mr. A is to pay the demand amount partially over a period of 3 to 5 months, but this requires the prior approval of the assessing officer in GST. Instead of making fixed instalments, Mr. A need to ensure that the electronic cash ledger is topped up regularly, and the balance is used to set off against the demand ID within the given timeframe.

It’s important to note that while this option allows flexibility in payment, there is no specific legal provision that outlines a fixed time limit for such payments. The assessing officer has the discretion to decide the payment period. During this period, the assessing officer will closely monitor Mr. A to ensure that the demand ID is being set off as agreed. The absence of a formal legal provision means that the arrangement relies heavily on the assessing officer’s approval and continuous oversight to ensure compliance.

This discretionary power of the assessing officer means that while there is room for negotiation, Mr. A must maintain transparent communication and consistent payment to avoid any further complications. The assessing officer’s regular monitoring acts as a safeguard to ensure that the taxpayer is adhering to the agreed terms and making progress towards settling the outstanding demand.

Conclusion

The complexities of output tax liability under the GST regime requires a thorough understanding of relevant legal provisions and practical steps for compliance. The case of Mr. A highlight the severe consequences of defaulting on tax payments, such as accruing interest, penalties, and potential criminal prosecution. However, the CGST Act provides several remedies to manage outstanding liabilities, including immediate payment, deferred payment plans under Section 80, and topping up the electronic cash ledger. Businesses must be proactive in managing their tax liabilities to avoid the escalating repercussions of non-compliance. By adhering to the structured procedures and leveraging available remedies, taxpayers can mitigate financial strain and ensure adherence to GST laws.

****

Disclaimer: The information provided in this article is intended for general informational purposes only and does not constitute legal, tax, or professional advice. While efforts have been made to ensure the accuracy of the information, it is important to consult with a qualified tax professional or legal advisor to address specific circumstances and ensure compliance with the applicable laws and regulations. The examples and case study discussed, including the case of Mr. A, are illustrative and may not encompass all possible scenarios or variations under the GST regime. The provisions and procedures described are based on the CGST Act and relevant rules as of the time of writing, and any changes or updates to the law may affect the applicability of the information. The authors and publishers of this article are not responsible for any errors, omissions, or outcomes related to the use of this information.

Author Bio