By CMA Himanshi Thakur

Amendments, corrections, redrafting, deletion, edition of sections, sub-sections, proviso, schedules and rules have been continuing in GST since its inception. Many a section added to CSGT Act, 2017 but never notified and finally deleted without implementation.

Major impact of such amendments is on GST portal which could not align itself with GST laws. Taxable person under GST also effected equally and litigation increased many folds.

Vide section 138 of Budget 2024, as enacted on 16.08.2024, section 73 & 74 got deleted and new section 74A wef 01.04.2024 has been introduced.

Why Section 74A?

Section 74 A was introduced to ease the compliances for the taxpayers under GST. It is effective from the FY 2024-25 and onwards.

It simplified and standardized

√ the way in which the notices are issued,

√ how demands are raised,

√ any penalty reliefs to be given

Irrespective of any willful misstatement, frauds or any fact suppression.

- Key objectives of introduction of Section 74A

> Easy understanding: Section 74 made it easy for the users to understand the rules and regulations to be followed and the penalties that could be levied in case of non-compliance.

> Merger: Section 73 & 74 have been merged to replace them with newly introduced section 74A. It will deal with fraud as well as non-fraud cases simultaneously.

> Simplified procedure: It specifies clear guidelines regarding non-compliances and penalties without creating any confusion.

It simplifies the complications that were faced under Section 73 & 74.

Section 74A has made understanding as well as compliances easier.

Key Points related to Section 74A

> Threshold Limit: No notice to be issued under this unless tax liability is above ₹1000.

> Evidences: It mandates evidence to support any allegations of fraud or misstatement.

> Notice time limit: The limit to issue notice under Section 74A is 42 months from the date of the erroneous refund, excess input tax credit, or the due date of the annual return in which fraud, suppression, or willful misstatement occurred.

> Order time limit: The order is to be issued within 12 months from the issuance of notice.

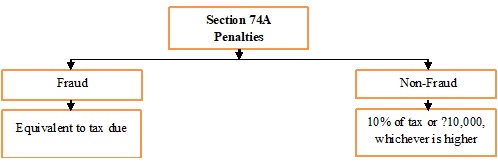

> Penalties payable:

1. Tax dues paid before issuance of notice non-fraud cases:

√ Penalty relief.

√ In case there is no intentional wrongdoing the penalty payable will be the higher of: 10% of the tax due or ₹10,000

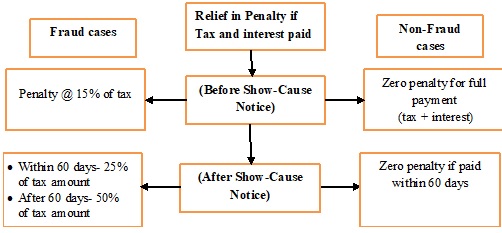

> Relief in Penalty:

1. In case there is no intentional wrongdoing the penalty payable will be

√ Zero-penalty if tax and interest is paid.

2. In case there is intentional wrong doing the penalty payable will be

√ equivalent to the tax dues.

3. In case of voluntary payment where there is no fraud and no show cause notice has been issued:

√ Zero-penalty if tax and interest is paid.

4. In case of voluntary payment where there is fraud before issue of show cause notice :

√ 15% of the tax amount will be imposed.

4. In case of voluntary payment where there is no fraud and paid within 60 days from the issuance of show cause notice:

√ Zero-penalty if tax and interest is paid.

5. In case of voluntary payment where there is fraud and within 60days from the issuance of show cause notice:

√ 25% of the tax amount will be imposed.

6. In case of voluntary payment is made, where there is a fraud and payment is made after 60 days from the issuance of show cause notice:

√ 50% of the tax amount will be imposed.

Brief differentiation between Section 74A, Section 73 and Section 74 under CGST Act.

| Aspect | Section 74A | Section 73 | Section 74 |

| Purview of Applicability | Any tax liability, whether fraud/misstatement or not | Tax liability other than fraud or misstatement | Tax liability from alleged fraud or misstatement |

| Subject to Notice | On the basis of material evidence, including fraud | On the basis of tax officer’s assumption | On the basis of tax officer’s suspicion |

| Time Limit to issue Notice | 42 months | 3 months before the expiry of 3 years | 6 months before the expiry of 5 years |

| Time Limit to issue Order | Within 12 months from the notice | Within 3 years | Within 5 years |

| Penalty Rate | -Higher of 10% of tax or ₹10,000, (for wrongdoing), -equivalent to tax due in fraud cases | – Higher of 10% of tax or ₹10,000 | -Equivalent to tax due in case of fraud or misstatement |

| Penalty Relief (Before Show-Cause Notice) | –Zero penalty for full payment (tax + interest) in non-fraud cases -Penalty @ 15% of tax in fraud cases | 15% penalty in fraud cases | No penalty for full payment (tax + interest) |

| Penalty Relief (After Show-Cause Notice) | -Zero penalty if paid within 60 days (non-fraud cases) -Penalty @ 25% (within 60 days) and 50% (after 60 days) in fraud cases | -25% penalty if paid within 60 days; 50% penalty after 60 days | -25% penalty if paid within 30 days; 50% penalty after 30 days |

Although section 74A focuses on the simplified and unified framework for fraud as well as non- fraud cases and the penalties simultaneously, but as we all are well aware that section 73 of CGST act deals with the cases where there is no suspicion of fraud, wilful misstatement or suppression of facts and section 74 of CGST Act deals with the cases where there is suspicious of fraud, wilful misstatement or suppression of facts. With the introduction of section 74A, every taxable person can be deemed to be taxable person in default despite of the actual reason as the notice under section 74A will be issued irrespective of fraud, wilful misstatement or suppression of facts. Now the taxable person has to justify himself by providing different documentation in order to prove that he is not the taxable person in default which will lead to more complex compliance for every taxpayer registered under the GST law. The person doing a minor mistake and someone doing intentional fraud, both will be kept in the same category. It will be kind of mental torture for someone who has not done anything wrong until the final result arrives.

Earlier the process followed was smooth and taxable person has to only focus on the monthly /annual compliances only but with the introduction of section 74A once again the taxable person has to deal with more complicated provision.

Author Bio