Vanshika Trivedi & Pooja Jaiswal (CMA Finalist)

Have you ever thought that ISD is a game changer for businesses running in different states across India? Under GST, the ISD (Input Service Distributor) mechanism is made available for the distribution of common Input Tax Credit (ITC) among different branches on their turnover basis. In ISD mechanism, the head-office of the business receives invoices related to the input services procured commonly for branches. Here, the responsibility for the payment of the invoice along with GST falls on ISD or the head-office, which later on allocates the ITC to its different branches on the basis of their turnover. The common services may include IT services, professional services, audit, advertising and marketing services etc.

As per section 2(61) of CGST ACT 2017 “Input Service Distributor means an office of the supplier of goods or services or both which receives tax invoices issued under section 31 towards the receipt of input services and issues a prescribed document for the purposes of distributing the credit of central tax, State tax, integrated tax or Union territory tax paid on the said services to a supplier of taxable goods or services or both having the same Permanent Account Number as that of the said office; ISD”.

This further explains in Rule 39 read with Rule 60 and 65 of the CGSTACT, 2017, which provide detailed provision on the distribution of ITC by the Input Service Distributor (ISD) and form and manner of furnishing details of inward supplies.

To understand the ISD in a simpler way we can understand through an example;

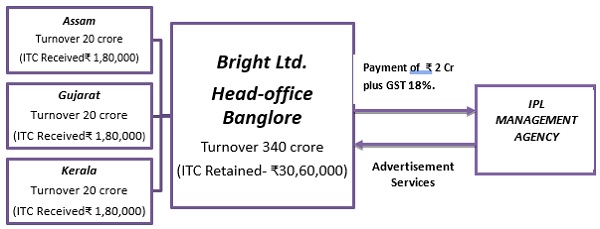

Bright Ltd., head-office in Bangalore having turnover of Rs. 340 Crore and branches in Assam, Gujarat and Kerala with turnover of 20 Crore each. Bright Ltd availed advertisement services of their energy drink for ₹ 2.00 Crore by signing a contract with IPL Management Agency. On the basis of turnover, the ITC received on such advertisement expenses @18% i.e., ₹ 36,00,000 will be distributed among Bangalore, Assam, Gujarat and Kerala states. Therefore, Assam, Gujarat and Kerala will receive ITC of ₹ 1,80,000 (0.18*20/400) each and head office in Bangalore will retain ITC of Rs. 30,60,000 (0.18*340/400) to itself on turnover basis under ISD mechanism.

Bright Ltd., head-office in Bangalore having turnover of Rs. 340 Crore and branches in Assam, Gujarat and Kerala with turnover of 20 Crore each. Bright Ltd availed advertisement services of their energy drink for ₹ 2.00 Crore by signing a contract with IPL Management Agency. On the basis of turnover, the ITC received on such advertisement expenses @18% i.e., ₹ 36,00,000 will be distributed among Bangalore, Assam, Gujarat and Kerala states. Therefore, Assam, Gujarat and Kerala will receive ITC of ₹ 1,80,000 (0.18*20/400) each and head office in Bangalore will retain ITC of Rs. 30,60,000 (0.18*340/400) to itself on turnover basis under ISD mechanism.

Why government has made ISD mandatory?

ISD has been made mandatory because now it will align with the principle of GST, which is a consumption and destination-based tax. This will beneficial in tracking of how the ITC is allocated across different branches/states/UTs or distinct persons. This will safeguard the interest of other branches/units/states that has also availed the common ITC services and to prevent the accumulation of ITC in the hands of one Unit i.e. Head Quarter

Previously, ISD registration was an optional registration but now it has been made mandatory from 1st April, 2025.This is because to make sure that the businesses distribute the common ITC availed on common input services uniformly, standardizing the process and proper allocation and utilization of common ITC as GST is consumption-based tax.

As it has been made mandatory, there are some rules and requirements that must be followed;

- It is mandatory to have separate registration for the ISD unit or its branches, who procured common services

- ISD registration should be separate from the main GST registration of business.

- The application for the registration as an ISD is done through form GST REG-1 and there is no threshold limit for registration for an ISD,

- The ISD cannot distribute credit ITC more than the available credit for the relevant month

- The ISD must file GSTR-6 by the 13th of the subsequent month to report the ITC distribution.

- An ISD shall distribute the ITC of RCM in the same manner of normal ITC on basis of turnover.

- The distributed ITC will be visible in GSTR-2B (Part-A) of the receiving branch/unit by the 14th of subsequent month, which is auto-populated based on the GSTR-6 filled by ISD.

- The recipient branch/unit can utilize the ITC in the GSTR-3B returns.

- An ISD is not required to file GSTR-9

If the above-mentioned rules are not followed, it will lead to following consequences:

- A penalty of up to ₹10,000/- or the amount of tax involved (whichever is higher) may be imposed.

- Interest at 18% per annum may be levied on the amount of ITC wrongly distributed

- If the ITC is not distributed correctly, the recipient branches/units may lose the benefit of ITC.

Let’s understand the process of filling returns,

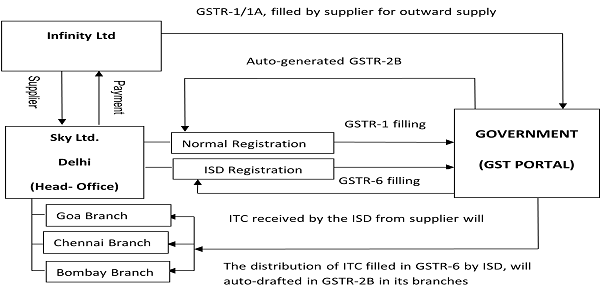

> The supplier shall upload the details of outward supply invoices in GSTR-1 by 11th or 13th (in case of IFF) of the following month.

> The details of invoices uploaded in GSTR-1 shall be made available in GSTR-6A of Input Service Distributor (ISD), which is an auto-populated statement of inward supply of ISD. This return is updated on the portal on the time when supplier submitted their GSTR-1/1A or GSTR-5 (for non-resident) as the case may be.

> Now, ISD shall file the return in GSTR- in Table 3& 4 for the distribution of ITC by 13th of the following month.

> The details of ITC distributed by ISD shall reflect in the recipient branches/units in his GSTR-2B by 14th of following month.

An Important Question arises here:

In the month of filling return,

- In case of Normal scheme, the due date for filling GSTR-1 by supplier is 11th and ITC will be made available in GSTR-6A to ISD by 12th allowing them to file GSTR-6 on time by 13th of the following month.

- In case of QRMP scheme, the due date of filling IFF by supplier is 13th which means GSTR-6A is made available on 14th for such cases, after the filing GSTR-6, which was on 13th.

Thus, the QRMP scheme’s (IFF) timing creates a delay in ITC distribution, which may impact the branches, especially if they need to use the ITC in the same month.

So, if we read rule 65 it allows us addition, deletion and corrections of GSTR-6A which means by 13th ISD can add such invoices and can claim ITC for QRMP (IFF) invoices also. Rule 65 is reproduced as under:

Rule 65, Form and manner of submission of return by an Input Service Distributor–

Every Input Service Distributor shall, on the basis of details contained in FORM GSTR-6A, and where required, after adding, correcting or deleting the details, furnish electronically the return in FORM GSTR-6, containing the details of tax invoices on which credit has been received and those issued under section 20, through the common portal either directly or from a Facilitation Centre notified by the Commissioner.

Under GST, the ISD mechanism only distributes the Input Tax Credit (ITC) related to input services, but it cannot distribute the ITC related to input goods and capital goods. This means if business purchases some input or capital goods such as machinery, furniture, raw material then the ITC related to these goods cannot be distributed through ISD mechanism, the ITC must be claimed by the branches individually. Further, recent amendments to the GST provision tightened the ISD mechanism, now it is strictly related to internal allocation of ITC within the business, rather than allowing distribution to the outsourced manufactures and service providers.

Have you ever thought why business always confuses between Cross charge with Input Service Distributor? The reason is that both are related to the distribution of ITC among its branches but they function in different ways. Cross charge refers to the distribution of ITC across its branches on internally generated and consumed services. The services are more operational and day to day in nature such as HR, accounting and administrative services etc. Whereas, in ISD external vendor provides services. In cross charge value of actual service along with GST applied is being transferred whereas in ISD only ITC of common service is being distributed.

To better understand the distinction between ISD and Cross Charge, consider the following examples:

CROSS CHARGE:

Starlight Pvt. Limited, headquartered in Chandigarh and its branches in Delhi, Chhattisgarh, Jharkhand, Manipur, provides computer software services to its branches. Since, this service is an internal service covered under cross-charge mechanism. As per GST regulations, it shall be required to supply an appropriate invoice and allocate the value of cross charge accordingly to its branches.

ISD (INPUT SERVICE DISTRIBUTOR):

XYZ Ltd having head office in Delhi and branches across India contacted VHP and Associates for the Audit of the company and its branches. VHP and Associates charges ₹5,00,000 plus 18% GST. The ITC for service of ₹90,000 received by head-office. This service is common input services related to ISD mechanism under GST. This mechanism allowed its branches and head-office to distribute the ITC on the basis of turnover. The distribution process can only be possible if the head-office has ISD Registration.

Through the above example; we can clearly understand the difference between the ISD and cross charge, that ISD is related to the externally availed services whereas cross charge relates to internally generated services.

This mechanism provides several key benefits which includes ensuring proper and efficient allocation of ITC for common services, it helps in better management of cash flows, it reduces the administrative burden, provide an accurate reporting and helps to reduces the risk of penalties due to proper allocation of ITC. However, the ISD mechanism has many advantages but business should also aware of the challenges or limitation it can bring such as: distribution of ITC among its branch can be complicated in nature. Also, businesses have to deal with multiple GST registration numbers, which may increase the workload and paperwork. It could be time consuming and if ITC is wrongly allocated it may lead to interest charges of 18% p.a. along with the penalties.

In the conclusion, GST Council is paying attention towards smooth operation of the tax process across the businesses in India and the concept of ISD is one of the steps. Earlier, ISD is optional but making it mandatory would better for the ITC distribution process and it will eliminate the multiple payments for the common services provided.

Vanshika Trivedi |

Pooja Jaiswal |

****

Authors:

Author Bio