Case Law Details

Surya Prakash Kacham Vs DCIT (ITAT Hyderabad)

Income Tax Appellate Tribunal Deletes Additions Based Solely on Third-Party Seized Tally Data & Unsigned JDA Entries

Hyderabad ITAT Deletes Additions Based on Third-Party Tally Data – Unsigned JDA Entries & No Cash Trail, No Tax u/s 56

The Hyderabad ITAT deleted additions of ₹50 lakh and ₹3.49 crore made u/s 56, holding that mere Tally data and loose documents seized from the premises of a developer cannot justify additions in the hands of the assessee without independent corroborative evidence. The Tribunal noted that the assessee had consistently denied receipt of cash and the seized documents neither carried the assessee’s signature nor any acknowledgment of cash receipt.

The Tribunal held that presumptions under sections 132(4A) and 292C apply primarily against the person from whose premises documents are seized and cannot automatically be invoked against third parties. Since the Revenue failed to establish any cash trail, bank withdrawals, confirmations or independent evidence showing movement of cash from the developer to the assessee, the additions were held unsustainable.

The ITAT also accepted the alternative argument that even assuming any amount was received pursuant to the Joint Development Agreement (JDA), such receipt could not be taxed under section 56 as “Income from Other Sources”. The Bench observed that issues arising from a JDA must be examined, if at all, under the capital gains provisions by determining whether a “transfer” u/s 2(47) had actually taken place and the correct year of taxability under section 45.

Relying on earlier Hyderabad Tribunal rulings and Telangana High Court principles on JDAs, the Tribunal reiterated that mere execution of a JDA and handing over possession for limited development purposes does not automatically trigger taxable capital gains.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

These two appeals are filed by Shri Surya Prakash Kacham (“the assessee”), feeling aggrieved by the separate orders passed by the Learned Commissioner of Income Tax (Appeals)-11, Hyderabad (“Ld. CIT(A)”) both dated 01.09.2025 for the A.Ys.2022-23 & 2023-24 respectively. Since the assessee is same and identical issues are raised in both these appeals, for the sake of convenience, these two appeals were heard together and are being disposed of by this common and consolidated order.

2. The assessee has raised the following grounds of appeal:

“1. The order of the Ld. CIT(A) is erroneous in law as well as facts of the case.

2. The Ld. CIT(A) has dismissed the appeal without considering the facts and circumstances of the case.

3. The Ld. CIT(A) has erred in sustaining the additions made by the Ld.AO u/s. 56 of the Act.

4. The Ld. CIT(A) erred in sustaining the additions even though the provisions of sec.56 will not be applicable to the present case of the appellant.

5. The Ld. CIT(A) ought to have observe the fact that the Ld. AO has not bought any corroborative evidence on record and made addition of Rs.50,00,000/-, and therefore the additions made are bad in law.

6. The Ld. CIT(A) ought to have observe the fact that the Ld. AO has erred in sustaining the addition merely on the basis of Tally data found during the search, without establishing that such data constituted incriminating material showing undisclosed income of the appellant.

7. The Ld. CIT(A)ought to have observe the fact that the Ld. AO has erred in making the addition without considering the submissions made by the Appellant and the failure to consider such submission is not valid.

8. The Ld. CIT(A) ought to have observed that the Ld. AO has not offered to cross-examine the witness, which is not valid.

9. Any other ground will be raised at the time of hearing.”

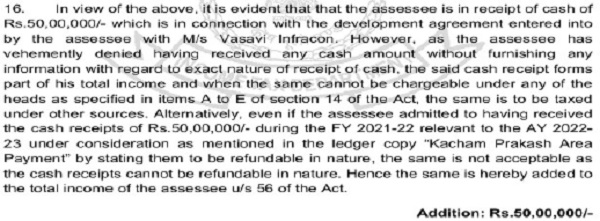

3. The brief facts of the case are that the assessee is an individual who filed his return of income for Assessment Year 2022–23 on 30.12.2022 declaring total income of Rs.91,51,060/-. The assessee had entered into a Joint Development Agreement -Cum- Irrevocable General Power of Attorney (“JDA”) with Vasavi Infracon (“the developer”) on 25.05.2022. Subsequently, a search and seizure operation under section 132 of the Income Tax Act, 1961 (“the Act”) was conducted in the case of Vasavi Group, Hyderabad on 17.08.2022. During the course of search, certain documents were seized from the premises of Vasavi Group. During the post search proceedings, statement under section 131 of the Act was recorded from the assessee on 02.02. 2023. Based on the seized material and the statement of the assessee, the Learned Assessing Officer (“Ld. AO”) formed a belief that an amount of Rs.50,00,000/- was received by the assessee in connection with the JDA, which had escaped assessment. Accordingly, proceedings under section 147 of the Act were initiated in the case of the assessee and notice under section 148 of the Act dated 12.10.2023 was issued. After considering the submissions of the assessee, the Ld. AO completed the assessment under section 147 of the Act vide order dated 14.02.2025, making an addition of Rs.50,00,000/- under section 56 of the Act as “Income from Other Sources”, and assessed the total income of the assessee at Rs.1,41,51,060/-.

4. Aggrieved by the order of the Ld. AO, the assessee preferred an appeal before the Ld. CIT(A). The Ld. CIT (A) confirmed the addition made by the Ld. AO. Accordingly, the Ld. CIT (A) dismissed the appeal of the assessee.

5. Aggrieved with the order of the Ld. CIT (A) , the assessee is in appeal before the Tribunal. At the outset, the Learned Authorized Representative (“Ld. AR”) submitted that though multiple grounds have been raised, the core issue involved in the present appeal relates to the addition of Rs.50,00,000/- made by the Ld. AO under section 56 of the Act. The Ld. AR submitted that Ground Nos. 5 to 7 relate to the addition made on merits. The Ld. AR submitted that the entire addition made by the Ld. AO is based solely on a document seized from the premises of a third party, namely the developer, without bringing any corroborative evidence on record. Further, the Ld. AR invited our attention to the copy of the JDA placed in the paper book, particularly referring to the relevant clauses placed at page no. 34 of the paper book, and submitted that as per the terms of the JDA, the assessee has not received any monetary consideration. It was submitted that the consideration agreed between the parties is in the form of built-up area receivable in future. The Ld. AR further invited our attention to the seized document reproduced by the Ld. AO at page no. 4 of the assessment order and submitted that the said document is merely a dumb document found from the premises of the developer. He submitted that the said document does not bear the signature of the assessee, nor does it contain any acknowledgment of receipt of cash by the assessee. The Ld. AR further submitted that during the course of statement recorded under section 131 of the Act on 02.02.2023, the assessee has categorically denied having received any cash from the developer. He submitted that despite such categorical denial, the Ld. AO has proceeded to make the addition without bringing any material to contradict the statement of the assessee. The Ld. AR further submitted that the Ld. AO has failed to bring on record any evidence regarding movement of cash from the developer to the assessee. No evidence such as withdrawal of cash, confirmation, or any independent material has been brought on record. The Ld. AR also submitted that the presumption under section 132(4A) and section 292C of the Act is not applicable in the hands of the assessee in respect of documents found from the premises of a third party. In support of his contention, the Ld. AR relied upon the decision of the Coordinate Bench of this Tribunal in the case of SVS Projects India Pvt. Ltd. in ITA Nos. 2139 to 2141/Hyd/2025 dated 30.04.2026 and specifically referred to para no. 15 of the said order. He submitted that under similar facts, the Tribunal has held that addition made solely on the basis of third-party documents without corroborative evidence cannot be sustained.

6. Without prejudice, the Ld. AR further raised an alternative legal argument under Ground Nos. 3 and 4. He submitted that even assuming, without admitting, that any amount was received, the same cannot be taxed under section 56 of the Act. In this regard, he submitted that the Ld. AO erred in treating the alleged receipt of Rs.50,00,000/- as income under section 56 of the Act. It was submitted that the said addition pertains to the JDA and any income arising therefrom is liable to be taxed, if at all, under the head “Capital Gains” and not under “Income from Other Sources”. The Ld. AR invited our attention to the copy of the JDA placed at page nos. 34 to 66 of the paper book and submitted that the JDA was executed on 25.05.2022 and no monetary consideration was received by the assessee during the year under consideration, except the right to receive built-up area in future. It was further submitted that the possession given to the developer was only for the limited purpose of development and does not constitute a “transfer” within the meaning of section 2(47) of the Act so as to attract taxation under section 45 of the Act in the year of execution of the JDA. The Ld. AR placed reliance on the decision of the Hyderabad Bench of the Tribunal in the case of Sahodhar Reddy Vs. DCIT in ITA No. 1619/Hyd/2025, dated 16.01.2026 for Assessment Year 2016–17, and submitted that under similar circumstances, it has been held that mere execution of JDA does not result in taxable capital gains unless conditions of transfer are satisfied. It was thus contended that the addition made by the Ld. AO under an incorrect head of income and without determining the correct year of taxability is not sustainable in law and is liable to be deleted. Accordingly, the Ld. AR prayed that the addition made by the Ld. AO be deleted.

7. Per contra, the Learned Departmental Representative (“Ld. DR”) strongly supported the orders of the lower authorities. The Ld. DR submitted that the seized document clearly evidences payment of Rs.50,00,000/- by the developer to the assessee. He submitted that the document contains complete details including the name of the payer, name of the recipient, date, and amount of payment. The Ld. DR contended that in view of the detailed nature of the entries in the seized document, the same cannot be treated as a dumb document. He further submitted that the existence of the JDA corroborates the transaction reflected in the seized document and therefore no further corroboration is required. He also submitted that the reliance placed by the assessee on the decision of the Tribunal in the case of SVS Projects India Pvt. Ltd.(Supra) is misplaced as the facts of the present case are distinguishable.

8. Further, with regard to the alternative argument, the Ld. DR submitted that the receipts arising out of a JDA are not always taxable under the head “Capital Gains” and depending on the nature of the receipt, the same can be taxed under the head “Income from Other Sources”. Accordingly, the Ld. DR prayed that the addition made by the Ld. AO be sustained.

9. We have heard the rival submissions and perused the material available on record including the case laws relied upon. At the outset, we find that Ground Nos. 1, 2 and 9 of the appeal of the assessee are general in nature and do not require any specific adjudication. Further, ground no. 8 has not been pressed by the assessee at the time of hearing. Accordingly, ground nos. 1, 2, 8 and 9 are dismissed being no separate adjudication is required.

10. Ground Nos. 5 to 7 of the assessee relates to the arguments of the assessee on merits. The primary issue for adjudication is whether the addition of Rs.50,00,000/- made by the Ld. AO on the basis of a document seized from the premises of a third party can be sustained. We have gone through the seized document reproduced by Ld. AO at page no. 4 of the assessment order. Without going into the issue, whether the seized document is a dumb document or not, the crucial issue is whether such a document which has been seized from the premises of a third party in the absence of corroborative evidence, can be made the sole basis for making an addition in the hands of the assessee. In this regard, we have gone through para no. 5 of the order of the Ld. AO wherein the Ld. AO has recorded the facts related to the statement of the assessee recorded under section 131 of the Act on 02.02.2023, which is to the following effect:

11. On perusal of the above, we find that the assessee has categorically denied having received any cash from the developer. We further find that the seized document does not bear the signature of the assessee, nor is there any acknowledgment or receipt evidencing actual receipt of cash. We also find that the Ld. AO has not brought on record any independent evidence to establish the movement of cash from the developer to the assessee. No corroborative material such as bank withdrawals, confirmation, or any cash trail has been brought on record. We have gone through para no. 15 of the order of the Coordinate Bench of this Tribunal in the case of SVS Projects India Pvt. Ltd. (Supra), which is to the following effect:

“15. We have gone through the relevant arguments of learned counsel for the assessee and we found that, the additions made by the AO are on the basis of documents found from the premises of a third party. It is a well-established principle of law by the decisions of various Courts that the documents found from the premises of a third party, the rebuttable presumption as per ITA Nos.2139 to 2141 and 2358 to 2360/Hyd/2025 S.V.S. Projects India Private Limited section 132(4A) and section 292C of the Act, is not applicable. Therefore, it is necessary for the AO to support the addition with further corroborative evidence in cases, where any addition is made on the basis of third-party information. In case there is no corroborative evidence, then there is no scope for making addition on the basis of third-party evidence, because the presumption under section 132(4A) is not applicable and the assessee is not required to explain the said documents. This principle is supported by the decision of the Hon’ble Gujarat High Court in the case of PCIT Vs. Gaurang Bhai Pramod Chandra Upadhyay (supra), wherein the Hon’ble High Court clearly held that since the documents were not found or recovered from the premises of the assessee, no presumption under section 132(4A) r.w.s 292C of the Act, could be drawn against the assessee in such circumstances. A similar view has been taken by the Hon’ble High Court of Patna in the case of Dharmaraj Prasad Bibhuti Vs. ITAT, Patna reported in (2019) 109 taxmann.com 388 (Patna), wherein it was held that the presumption under section 292C of the Act, can only be drawn against such person from whose possession or control any books of accounts or other documents, money, etc. are found during the ITA Nos.2139 to 2141 and 2358 to 2360/Hyd/2025 S.V.S. Projects India Private Limited course of search. The sum and substance of the ratio laid down by various courts is that the rebuttable presumption under section 132(4A) r.w.s. 292C of the Act, cannot be pressed into service against the assessee with regard to material seized during the course of search from the premises of a third party, unless there is corroborative evidence. Therefore, in our considered view, the addition made by the AO on the basis of third-party evidence without any corroborative evidence cannot be sustained.”

12. On perusal of the above, we find that under similar facts, the Tribunal has held that where documents are found from the premises of a third party, the presumption under section 132(4A) read with section 292C of the Act cannot be applied against the assessee and that addition made solely on the basis of such third-party documents without corroborative evidence cannot be sustained. Further, in the present case the Ld. AO has not conducted any independent inquiry to establish the alleged transaction of cash received by the assessee. Therefore, a mere entry in a loose sheet/document found unsigned from a third party in the absence of any corroborative evidence cannot be a basis for the addition in the hands of the assessee. Accordingly, respectfully following the order of the Tribunal, we hold that in the present case also, the presumption under section 132(4A) read with section 292C of the Act is not applicable in the hands of the assessee. Therefore, in the absence of corroborative evidence, the addition made by the Ld. AO solely on the basis of third-party material cannot be sustained. Accordingly, ground nos. 5 to 7 of the assessee are allowed.

13. Further, as far as the alternate argument of the assessee is concerned, we also find merit in the alternative contention of the assessee. The assessee has raised an alternative legal argument under Ground Nos. 3 and 4. The Ld. AR has submitted that even assuming, without admitting, that any amount was received, the same cannot be taxed under section 56 of the Act. In this regard, we have gone through the JDA placed at page nos. 34 to 66 of the paper book and on perusal of the same, we find that the assessee has entered into a JDA with the developer for development of land, wherein the consideration agreed is primarily in the form of built-up area receivable in future. We have also gone through para no. 16 of the order of the Ld. AO which is to the following effect:

14. On perusal of the above, we observe that the Ld. AO has made an addition of Rs.50,00,000/- treating the same as income from other sources under section 56 of the Act, alleging that the assessee has received cash consideration pursuant to the JDA. However, no cogent material has been brought on record by the Ld. AO to establish that such receipt is independent of or unrelated to the development agreement. It is a settled position of law that income arising from transfer of a capital asset under a JDA is to be examined in the context of section 2(47) read with section 45 of the Act. The taxability depends upon whether a “transfer” has taken place and the year in which such transfer is deemed to occur. In the present case, we find that the Ld. AO has neither examined the issue of “transfer” within the meaning of section 2(47) of the Act nor determined the correct year of taxability under section 45 of the Act. Instead, the Ld. AO has proceeded to tax the alleged receipt under section 56 of the Act, which, in our considered opinion, is not in accordance with law. We have also gone through para nos. 8 and 9 of the decision of the Coordinate Bench in the case of Sahodhar Reddy Vs. DCIT (Supra) relied upon by the Ld. AR, which is to the following effect:

not apply to the fact situation of the case. In. Harbour View (supra), the Division Bench of Kerala High Court on the facts of the case found that the possession of the property was handed over under Section 53A of the Transfer of Property Act, 1882. Therefore, the aforesaid decision also has no application to the fact situation of the case.”

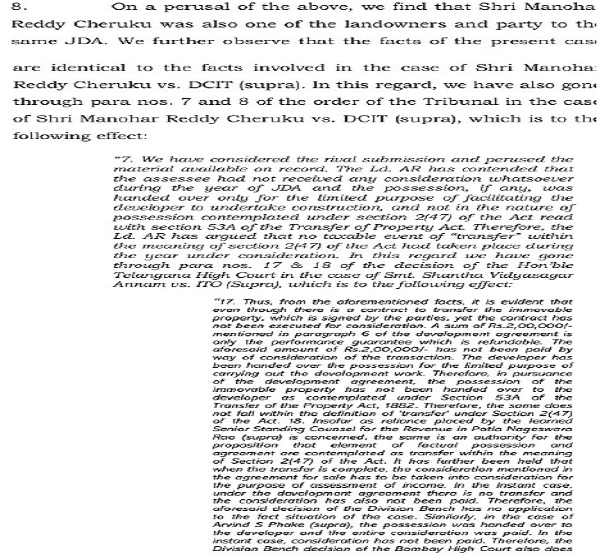

8. On a perusal of the above, we find that the Hon’ble High Court after considering the judgment in Potla Nageswara Rao (supra), has held that unless consideration is received or accrues to the assessee, or unless possession is handed over in the manner contemplated under section 53A of the Transfer of Property Act, no transfer can be said to have occurred for the purpose of section 45 of the Act. In the present case, the revenue has not brought on record any material to show that the assessee received any consideration, monetary or otherwise, during the year of execution of JDA; or the assessee handed over possession to the developer otherwise than for the limited purpose of development. In absence of such essential conditions, the very foundation of invoking section 45(1) of the Act in the year of JDA fails. Respectfully following the binding judgment of the Hon’ble Telangana High Court in the case of Smt. Shantha Vidyasagar Annam vs. ITO (supra), we hold that no taxable capital gains arise in the hands of the assessee during the year under consideration. We therefore find no justification to sustain the addition of Rs.3,65,904/ – made on account of alleged long-term capital gains. Accordingly, we set aside the order passed by the Id. CIT(A) and direct the Ld. AO to delete the addition made on account of long term capital gains?

9. On a perusal of the above, we find that this Tribunal, after relying upon the judgment of the Hon’ble Telangana High Court in Smt. Santha Vidyasagar Annam vs. ITO (supra), held that, if the possession given by the landowners to the developer was only for the limited purpose of development and that no consideration had been received during the year of execution of the JDA, no taxable capital gains arose under section 45(1) of the Act in that year. Respectfully following the principle of consistency and the decision of this Tribunal in the case of Shri Manohar Reddy Cheruku vs. DCIT (supra), we hold that no taxable capital gains arose in the hands of the assessee during the year under consideration. Accordingly, we direct the Id. AO to delete the addition of Rs.3,65,904/- made on account of long-term capital gains.

15. On perusal of the above, we find that the Tribunal has held that unless the conditions of transfer are satisfied, execution of a JDA does not automatically result in taxable capital gains. Further, we find merit in the contention of the Ld. AR that the Ld. AO has not recorded any finding that the impugned amount was received by the assessee for any purpose other than in connection with the JDA. In the absence of such a finding, the characterization of the receipt as “Income from Other Sources” is without basis. Under these circumstances, without going into the issue of taxability of income of the assessee out of the JDA, we are of the considered view that the addition made by the Ld. AO under section 56 of the Act suffers from legal infirmity. The proper course for the Ld. AO was to examine the issue, if at all, under the provisions relating to capital gains by determining the existence and timing of transfer. Therefore, we hold that the addition made under section 56 of the Act is legally unsustainable. Accordingly, ground nos. 3 & 4 of the assessee are also allowed.

16. In the result, the appeal of the assessee in ITA No. 2082/Hyd/2025 for the A.Y. 2022-23 is allowed.

ITA No. 2083/Hyd/2025 for A.Y. 2023-24:

17. The assessee has raised the following grounds of appeal:

“1. The order of the Ld. CIT(A) is erroneous in law as well as facts of the case.

2. The Ld. CIT(A) has dismissed the appeal without considering the facts and circumstances of the case.

3. The Ld. CIT(A) has erred in sustaining the additions made by the Ld.AO u/s. 56 of the Act.

4. The Ld.CIT(A) erred in sustaining the additions even though the provisions of sec.56 will not be applicable to the present case of the appellant.

5. The Ld.CIT(A) ought to have observe the fact that the Ld. AO has not bought any corroborative evidence on record and made addition of Rs.3,49,09,950/-, and therefore the additions made are bad in law.

6. The Ld.CIT(A) ought to have observe the fact that the Ld. AO has erred in sustaining the addition merely on the basis of Tally data found during the search, without establishing that such data constituted incriminating material showing undisclosed income of the appellant.

7. The Ld. CIT(A)ought to have observe the fact that the Ld. AO has erred in making the addition without considering the submissions made by the Appellant and the failure to consider such submission is not valid.

8. The Ld. CIT(A) ought to have observed that the Ld. AO has not offered to cross-examine the witness, which is not valid.

9. Any other ground will be raised at the time of hearing.”

18. The issues raised in the present appeal are identical to the issues raised in ITA No.2082/Hyd/2025 for the A.Y. 2022-23. Therefore, our observations and findings recorded therein shall apply mutatis mutandis to the present appeal as well. Since we have allowed the appeal of the assessee in ITA No.2082/Hyd/2025 for the A.Y. 2022-23, the present appeal of the assessee is also allowed.

19. In the result, appeal filed by the assessee in ITA No.2083/Hyd/2025 for the A.Y 2023-24 is allowed.

20. To sum up, both the appeals of the assessee are allowed.

Order pronounced in the Open Court on 15th May, 2026.

Author Bio