Securities and Exchange Board of India has released a consultation paper proposing to permit netting of funds for cash market transactions by Foreign Portfolio Investors (FPIs) to improve operational efficiency and reduce funding costs. Currently, FPIs must settle purchases and sales on a gross basis, even when same-day buy and sell values offset, leading to temporary liquidity strain, forex slippage, and higher funding costs—especially during index rebalancing. The proposal would allow netting only for outright transactions (securities with either buy or sell, not both, in a settlement cycle), while continuing gross settlement for non-outright transactions to mitigate market risk. Securities settlement, STT, and stamp duty would remain delivery-based. SEBI discussed potential operational and clearing risks with market participants and outlined mitigants, including existing default safeguards and system upgrades by custodians. Public comments are invited by 6 February 2026 to finalize the framework and related regulatory amendments.

Securities and Exchange Board of India

Consultation Paper on proposal to permit netting of funds for transactions done by Foreign Portfolio Investors (FPIs)

1. Objective

1.1. In terms of Regulation 20(4) of SEBI (FPI) Regulations, 2019, FPIs are required to transact in securities in India only on the basis of taking and giving delivery of securities purchased or sold.

1.2. In terms of SEBI’s Master Circular for Stock Exchanges and Clearing Corporations dated December 30, 2024, institutional investors are not allowed to do day trading i.e., square-off their transactions intra-day. All transactions are grossed at custodians’ level and investors are required to fulfill their obligations on a gross basis. The custodians, however, settle their deliveries on a net basis with the clearing corporations (CCs).

1.3. SEBI has received feedback regarding review of the current practice in order to enhance operational efficiency and reduce cost of funding for FPIs.

1.4. It is proposed to permit netting of funds for transactions done by FPIs in cash market. The objective of this consultation paper is to seek comments, views and suggestions from the public on the captioned proposal.

2. Need for review:

2.1. SEBI is in receipt of suggestions that the current practice of gross settlement of transactions done by FPIs is leading to additional liquidity demand and inefficiency for FPIs. For example, suppose an FPI has purchased stock A worth Rs. 100 crores and sold stock B worth Rs.100 crores. FPI would need to deliver stock B as well as make available Rs.100 crores towards purchase of stock A. As a part of the pay-out, FPI would receive stock A and receive back Rs.100 crores towards consideration for sale of stock B. It may be argued that this pay-in obligation of Rs. 100 crores results in FPI being underinvested to the amount of Rs. 100 crores for at least 1 day, which otherwise could have been adjusted against the settlement proceeds of the sale transaction.

2.2. Further, there are potential costs involved due to slippage between buying and selling forex to fulfill their obligations.

2.3. Additionally, in case of FPIs who rely on global custodian credit lines, there is an additional cost of funding for at least one additional day.

2.4. The issues highlighted above gain more importance during days of index rebalancing, wherein there are large inflows and outflows in index constituents and the cost of funding the same increases significantly.

2.5. In view of the above, in order to enhance operational efficiency and reduce cost of funding for FPIs, there is a case for reviewing the existing practice of gross settlement and permitting ‘netting of funds’ for transactions done by FPIs in cash market.

2.6. ‘Netting of funds’ in this context shall mean using the proceeds of sale transactions in cash market on a particular day to fund the purchase transactions in cash market done by an FPI on the same day, thereby requiring FPI to fulfill only the net fund obligation.

3. Discussions with market participants

3.1. The proposal regarding netting of funds for transactions done by FPIs in cash market (‘proposed scenario’) was discussed with market participants namely custodians, CCs and stock exchanges.

3.2. During the said discussions, the following potential risks or operational challenges were highlighted:

3.2.1. Potentially higher rejections

a. In the current scenario, an FPI needs to provide funds toward purchase transactions independent of sale transactions. As a result, in case there are any issues in confirmation of sale transactions, buy transactions are confirmed independently.

b. In the proposed scenario, the confirmation of purchase transactions would be contingent on the confirmation of sale transactions. Any issues with confirmation of sale transactions may lead to rejection of purchase transactions as well. In such a scenario, the obligation for settlement would devolve on the executing broker.

c. It is also pertinent to note that the representation for netting is for addressing high liquidity requirement on days such as index rebalancing, but these are the same days where the transaction volumes is high and system slowness or other operational issues are more likely to arise.

d. In the current system, no margins are collected from the brokers or the custodians in case of FPI trades in cash market. Any rejections of large value of trades can put the CC, and thereby the system, at risk.

Possible mitigation:

e. The risk of FPI transactions getting rejected (on account of failure in reconciliation or shortfall of funds/securities), and thereby devolving the settlement obligation on the executing broker, exists even today. In this regard, necessary safeguards by way of default waterfall mechanism, Core Settlement Guarantee Fund (Core SGF), etc. have been put in place.

f. In the proposed mechanism, it may be appreciated that funds obligations from FPIs on account of netting shall reduce, which may likely reduce the possibility of rejection of purchase transactions on account of shortfall of funds.

g. Further, in order to address any operational issues or system slowness that may arise on account of implementation of instant proposal, custodians would be mandated to upgrade their systems to support the same.

3.2.2. Credit / Clearing System risk

a) There are a few hours gap between the pay-in done by the clearing members to the CCs and the pay-out done by the CCs to the clearing members. Due to time gap between pay-in and pay-out, the clearing and settlement risk of custodian would increase to the extent of netting in the revised framework. Today, this risk is borne by the FPI while in the revised framework this risk would shift to the custodian. Further, Rules/Regulation/Byelaws of CC is not clear on the exact proceedings in a CC default scenario, on whether a CC liquidator would ask for gross or net settlement. In case custodians are required/ called upon to fulfill pay-in obligation on a gross basis, but custodians only collect net funds from their clients, then it would add incremental risk to the banking system.

Possible mitigation:

b) As noted earlier, CCs in India have a robust mechanism in place to deal with default scenarios, including default waterfall, Core SGF, etc.

c) Further, currently, custodians settle their obligations on a net basis with CCs. In the proposed mechanism, the obligations shall continue to be settled on a net basis between custodians and CCs, and there would be no change in the funds and securities paid to / received from CC by custodian. Therefore, there may not be any change in the risk arising from non-receipt of pay-out from CC.

d) Also, SEBI’s Master Circular for Stock Exchanges and Clearing Corporations dated December 30, 2024 mandates CCs to have a winding down policy clearly articulating the procedure to be followed in the scenario of winding down of its critical operations and services. The said Circular also specifies that “The provisions of SECC Regulations, 2018 and various circulars and guidelines issued thereunder, shall continue to apply during the entire period of winding down of critical operations and services of CCs”, which includes netting.

3.3. It was also clarified that no operational changes are being envisaged in the current procedures being followed at CC for confirmation and settlement process. Further, while the validations that custodians need to perform before confirmation of trades shall undergo a change in order to facilitate confirmation on the basis of netted obligations, no changes are being envisaged to the procedure for reconciliation for confirmation of trades and validation of holdings.

3.4. Further, in order to operationalize the proposal, certain amendments have to be carried out in the regulatory frameworks issued by SEBI and RBI.

Question for public comments

1. Do you agree with the proposal to permit netting of funds for transactions done by FPIs in cash market?

2. Do you agree with the potential mitigants cited above in response to the potential risks or operational challenges highlighted by the market participants?

4. Proposal:

4.1. Based on detailed discussions held including with the advisory committee of SEBI, it is proposed to permit netting of funds for outright transactions done by FPIs in cash market. ‘Outright transactions’ shall mean those transactions done by an FPI where there is either a purchase or a sale transaction, but not both, in a security in a particular settlement cycle.

4.2. The proposed mechanism for such netting of funds is detailed below:

4.2.1. The transactions in securities with only outright sell or outright purchase shall be netted to arrive at a net fund obligation for outright transactions.

4.2.2. The transactions in those securities where there are both buy and sell transactions for a given FPI in a particular settlement cycle shall be excluded from netting. Therefore, netting of intra-day transactions in same securities shall be excluded and such non-outright transactions shall continue to be confirmed on gross basis, as per the current procedure.

4.2.3. Further, if value of outright sell does not exceed the value of outright buy, then the residual amount along with non-outright buy obligations shall be funded by the FPI.

4.2.4. However, if value of outright sell exceeds the value of outright buy, then excess outright sell shall not be adjusted towards non-outright buy obligations.

4.3. An illustration of the obligations of FPI as per existing practice and under proposed model, along with pictorial depiction, is given at Annexure A.

4.4. Further, it is clarified that settlement of securities shall continue to be carried out on gross basis between FPIs and custodians. Accordingly, Securities Transaction Tax (STT) and stamp duty shall continue to be charged on delivery basis.

4.5. The above proposal would help in reducing cost of funding for FPIs, especially on index rebalancing days, considering there would be outright purchases or sales in incoming or outgoing stocks in an index. At the same time, considering that non-outright transactions are proposed to be confirmed on gross basis, this would address the risk of swaying of markets by FPIs holding large quantities of securities.

Question for public comments

3. Do you agree with the proposed mechanism for permitting netting of funds for outright transactions done by FPIs in cash market, as stated above?

5. Public Comments

5.1. Considering the implications of the aforementioned matters on the market participants, public comments are invited on the above-detailed proposal. The comments/ suggestions should be submitted latest by February 06, 2026, through the following link: https://www.sebi.gov.in/sebiweb/publiccommentv2/PublicCommentAction.do?doPubl icComments=yes

5.2. Any technical issue in submitting your comment through web based public comments form, may be communicated through email to afdconsultation@sebi.gov.in with a subject: “Issue in submitting comments on Consultation paper on proposal to permit netting of funds for transactions done by Foreign Portfolio Investors (FPIs)”

Issued on: January 16, 2026

Annexure A

Illustration of obligations of FPI as per existing practice and under proposed model

1. Consider an example wherein on a particular day, an FPI has bought 10 shares of stocks A and B worth 1000 each and sold 20 shares of stocks B and C worth 2000 each. For the sake of simplicity, it is assumed that all the transactions are on account of the said FPI, and the custodian clears the transactions of only this single FPI. All transactions are assumed to be confirmed. The example is summarised in the table given below:

| Stock | Buy Quantity | Buy Value | Sell Quantity | Sell Value |

| A | 10 | 1000 | 0 | 0 |

| B | 10 | 1000 | 20 | 2000 |

| C | 0 | 0 | 20 | 2000 |

2. The obligations of FPI under the existing practice and proposed model is as under:

2.1. Existing Practice (Gross Settlement):

a. All the transactions of the FPI are settled on gross basis with the custodian.

b. The custodian, however, settles its obligations on a net basis with the clearing corporation (CC).

c. Accordingly, in the example given above, the pay-in and pay-out obligations of FPI towards the custodian and of custodian towards CC are given below:

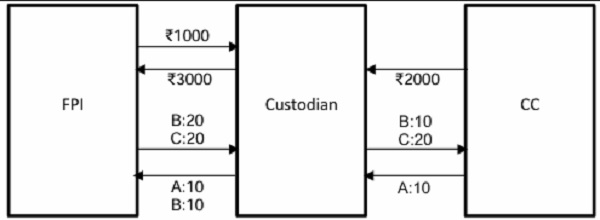

i. Obligation of FPI towards custodian

| Pay-in | Pay-out | |

| Funds | 2000 | 4000 |

| Securities | Stock B: 20 Stock C: 20 | Stock A: 10 Stock B: 10 |

ii. Obligation of custodian towards CC

| Pay-in | Pay-out | |

| Funds | 0 | 2000 |

| Securities | Stock B: 10 Stock C: 20 | Stock A: 10 |

iii. Pictorial depiction of the obligations of FPI, custodian and CC is given below:

2.2. Proposed Model (Netting of funds):

a. The transactions in securities with only outright sell or outright purchase shall be netted to arrive at a net fund obligation for outright transactions.

b. In the instant example, there is an outright purchase in stock A and an outright sale in stock C, therefore, they shall be netted to arrive at a net fund obligation for outright transactions.

c. Since stock B involves both purchase and sale under the same settlement cycle, it shall be settled as per the existing practice of gross settlement.

d. The excess outright sell value (on account of netting of funds for stocks A and C) shall not be adjusted towards non-outright buy obligations.

e. Further, the manner of settlement between custodian and CC shall remain unchanged.

f. Accordingly, in the example given above, the pay-in and pay-out obligations of FPI towards the custodian and of custodian towards CC are given below:

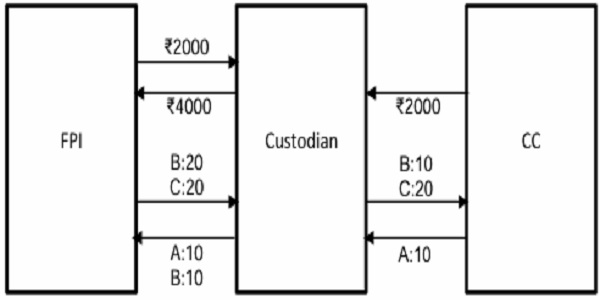

i. Obligation of FPI towards custodian

| Pay-in | Pay-out | |

| Funds | 1000 | 3000 |

| Securities | Stock B: 20 Stock C: 20 | Stock A: 10 Stock B: 10 |

ii. Obligation of custodian towards CC

| Pay-in | Pay-out | |

| Funds | 0 | 2000 |

| Securities | Stock B: 10 Stock C: 20 | Stock A: 10 |

iii. Pictorial depiction of the obligations of FPI, custodian and CC is given below: