The Reserve Bank of India (RBI) has released the Master Direction – Reserve Bank of India (Commercial Paper and Non-Convertible Debentures of original or initial maturity up to one year) Directions, 2024, vide Notification No. FMRD.DIRD.10/14.02.001/2023-24 dated January 03, 2024. This directive follows the comprehensive review of money market directions as outlined in the Statement on Developmental and Regulatory Policies dated June 06, 2019. The Directions, effective from April 01, 2024, empower the RBI to regulate Commercial Papers (CPs) and Non-Convertible Debentures (NCDs) issued by various entities. The guidelines encompass eligibility criteria for issuers and investors, detailed terms for primary and secondary market transactions, credit enhancement, reporting requirements, and the roles of key participants like Issuing and Paying Agents, Debenture Trustees, and Credit Rating Agencies. This article delves into the key facets of the Master Direction, shedding light on its implications for the financial markets.

Reserve Bank of India

RBI/FMRD/2023-24/109

FMRD.DIRD.09/14.02.001/2023-24 Dated: January 03, 2024

To

All Eligible Market Participants

Madam/Sir

Master Direction – Reserve Bank of India (Commercial Paper and Non-Convertible Debentures of original or initial maturity upto one year) Directions, 2024

Please refer to paragraph 6 of the Statement on Developmental and Regulatory Policies, announced as a part of the second Bi-monthly Monetary Policy Statement for 2019-20 dated June 06, 2019 regarding Comprehensive Review of Money Market Directions. Accordingly, the draft Directions on Call, Notice and Term Money, Certificate of Deposit and the Commercial Paper and Non-Convertible Debentures of original or initial maturity upto one year markets were released for market feedback on December 04, 2020. The Master Direction – Reserve Bank of India (Call, Notice and Term Money Markets) Directions, 2021 and the Master Direction – Reserve Bank of India (Certificate of Deposit) Directions, 2021 were issued on April 01, 2021 and June 04, 2021 respectively.

2. The Directions on Commercial Paper and Non-Convertible Debentures of original or initial maturity upto one year have been reviewed based on market feedback and the Master Direction – Reserve Bank of India (Commercial Paper and Non-Convertible Debentures of original or initial maturity upto one year) Directions, 2024 are being issued herewith.

3. These Directions have been issued in exercise of the powers conferred under section 45J, 45K, 45L and 45W of the Reserve Bank of India Act, 1934 read with section 45U of the Act and of all the powers enabling it in this behalf.

Yours faithfully,

(Dimple Bhandia)

Chief General Manager

FINANCIAL MARKETS REGULATION DEPARTMENT

Notification No. FMRD.DIRD.10/14.02.001/2023-24 dated January 03, 2024

Master Direction – Reserve Bank of India (Commercial Paper and Non-

Convertible Debentures of original or initial maturity upto one year) Directions, 2024

In exercise of the powers conferred under section 45J, 45K, 45L and section 45W of the Reserve Bank of India Act, 1934 (hereinafter called the Act) read with section 45U of the Act and in supersession of Notification No. FMD.MSRG.49/02.13.016/2010-2011 dated July 28, 2010, Section IV of FMRD. Master Direction No. 2/2016-17 dated July 07, 2016 and Direction No. FMRD.DIRD.01/CGM (TRS) – 2017 dated August 10, 2017, the Reserve Bank of India (hereinafter called the Reserve Bank) hereby issues the following Directions.

1. Short title, scope and commencement

(a) These Directions shall be called the Master Direction – Reserve Bank of India (Commercial Paper and Non-Convertible Debentures of original or initial maturity upto one year) Directions, 2024.

(b) These Directions shall be applicable to all persons/agencies dealing in Commercial Paper and/or Non-Convertible Debentures of original or initial maturity upto one year.

(c) These Directions shall come into force with effect from April 01, 2024.

2. Definitions

(a) For the purpose of these Directions, unless the context otherwise requires:

(i) All India Financial Institution (AIFI) shall include: (a) Export Import Bank of India, (b) National Bank for Agriculture and Rural Development, (c) National Housing Bank, (d) Small Industries Development Bank of India and (e) National Bank for Financing Infrastructure and Development.

(ii) Bank means a banking company (including a Payment Bank and a Small Finance Bank) as defined in clause (c) of Section 5 of the Banking Regulation Act, 1949 (10 of 1949) or a “regional rural bank”, a “corresponding new bank” or “State Bank of India” as defined in clauses (ja), (da) and (nc), of section 5 respectively thereof, or a “cooperative bank” as defined in clause (cci) of Section 5 read with Section 56 of the said Act.

(iii) Body corporate means any entity incorporated by or under any Statute for the time being in force but does not include a co-operative society registered under any law relating to co-operative societies.

(iv) Commercial Paper (CP) means an unsecured money market instrument issued in the form of a promissory note.

(v) Company means a company as defined in Section 2 (20) of the Companies Act, 2013 (18 of 2013).

(vi) Co-operative society shall have the meaning as assigned to it under clause (cciia) of Section 5 of the Banking Regulation Act, 1949 read with Section 56 of the said Act.

(vii) Delivery versus Payment (DvP) means a settlement mechanism which stipulates that transfer of funds from the buyer of securities is made simultaneously with the transfer of securities by the seller of securities.

(viii) Depository shall have the meaning as assigned in Section 2 (e) of the Depositories Act, 1996 (22 of 1996).

(ix) Debenture Trustee means an entity registered with SEBI as debenture trustee under the SEBI (Debenture Trustees) Regulations, 1993.

(x) Electronic Trading Platform (ETP) shall have the meaning as assigned in paragraph 2(1) (iii) of the Electronic Trading Platforms (Reserve Bank) Directions, 2018 dated October 05, 2018 or as modified from time to time.

(xi) Financial Benchmark Administrator (FBA) means a person who controls the creation, operation and administration of financial benchmark(s) authorized under the Reserve Bank of India (Financial Benchmark Administrators) Directions, 2023, dated December 28, 2023, as amended from time to time.

(xii) Group entities means an arrangement involving two or more entities related to each other through any of the following relationships: (a) subsidiary – parent (defined in terms of Ind-AS 110/AS 21); (b) joint venture (defined in terms of Ind-AS 28/AS 27) ; (c) associate (defined in terms of Ind-AS 28/AS 23); (d) Promoter-promotee (as provided in the SEBI (Acquisition of Shares and Takeover) Regulations, 1997) for listed companies; (e) common brand name or (f) investment in equity shares of 20 per cent and above.

(xiii) Infrastructure Investment Trust (InvIT) means a business trust as defined in sub-clause (i) of clause 13A of section 2 of the Income-tax Act, 1961.

(xiv) Issuing and Paying Agent (IPA) means a Scheduled Commercial Bank undertaking duties and responsibilities specified under paragraph 7(a) of these Directions.

(xv) Limited liability partnership shall have the meaning as assigned in Section 2(n) of the Limited Liability Partnership Act, 2008 (6 of 2009).

(xvi) Money market instruments shall have the meaning as assigned in Section 45(U) (b) of the Reserve Bank of India Act, 1934.

(xvii) Non-Banking Financial Company (NBFC) means a company as defined in Section 45 I (f) of the Reserve Bank of India Act, 1934.

(xviii) Non-Convertible Debenture (NCD) means a secured money market instrument with an original or initial maturity upto one year.

(xix) A Non-resident shall mean a ‘person resident outside India’ and shall have the meaning as assigned to it in section 2 (w) of Foreign Exchange Management Act, 1999 (42 of 1999).

(xx) Over-the-Counter (OTC) markets refers to markets where transactions are undertaken in any manner other than on recognised stock exchanges and shall include those undertaken on electronic trading platforms (ETPs).

(xxi) A Promoter shall have the meaning as assigned in Section 2(69) of the Companies Act, 2013.

(xxii) Real Estate Investment Trust (REIT) means a business trust as defined in sub-clause (ii) of clause 13A of section 2 of the Income-tax Act, 1961.

(xxiii) Recognised stock exchanges shall have the meaning as assigned in Section 2 (f) of the Securities Contracts Regulation Act, 1956 (42 of 1956).

(xxiv) Related parties shall have the same meaning as assigned to it under Indian Accounting Standard (Ind AS) 24 – Related Party Disclosures or International Accounting Standard (IAS) 24 – Related Party Disclosures or any other equivalent accounting standards.

(xxv) Resident shall mean a ‘Person resident in India’ and shall have the same meaning as assigned to it in Section 2 (v) of the Foreign Exchange Management Act, 1999 (42 of 1999).

(b) Words and expressions used but not defined in these Directions shall have the meaning assigned to them in the Reserve Bank of India Act, 1934.

3. Eligible issuers

(a) CPs and NCDs may be issued by the following entities subject to the condition that all fund-based facilities availed, if any, by the issuer from banks/ AIFIs / NBFCs are classified as Standard at the time of issue:

(i) Companies;

(ii) NBFCs, including Housing Finance Companies (HFCs);

(iii) InvITs and REITs;

(iv) All India Financial Institutions (AIFIs);

(v) Any other body corporate with a minimum net-worth of ₹100 crore, provided that the body corporate is statutorily permitted to incur debt or issue debt instruments in India; and

(vi) Any other entity specifically permitted by the Reserve Bank.

(b) Co-operative societies and limited liability partnerships with a minimum net-worth of ₹100 crore, may also issue CPs under these Directions, subject to the condition that all fund-based facilities availed, if any, by the issuer from banks/ AIFIs / NBFCs are classified as Standard at the time of issue.

4. Eligible investors

(a) All residents are eligible to invest in CPs and NCDs.

(b) Non-residents are eligible to invest in CPs and NCDs to the extent permitted under Foreign Exchange Management Act (FEMA), 1999 or the rules/regulations framed thereunder.

Provided that no person, resident or non-resident, can invest in CPs and NCDs issued by related parties either in the primary or through the secondary market.

5. General Guidelines

(a) Primary Issuance

(i) CPs and NCDs shall be issued in dematerialised form and held with a depository registered with SEBI.

(ii) CPs and NCDs shall be issued in minimum denomination of ₹5 lakh and in multiples of ₹5 lakh thereafter.

(iii) The tenor of a CP shall not be less than seven days or more than one year. The tenor of an NCD shall not be less than ninety days or more than one year.

(iv) Issuance of a CP/NCD with options (call/put) is not permitted.

(v) Issuance of a CP/NCD is not permitted to be underwritten or co-accepted.

(vi) The offer documents for the issue of CPs and NCDs shall, at the minimum, include disclosures as given in Annex I.

(vii) The primary issuances of CPs and NCDs, including both payment of funds to the issuer and issue of CPs and NCDs to the investors, shall be settled within a period not exceeding T+4 working days, where T represents the deal date, i.e., the date on which the trade details, including price/rate are agreed by the issuer and the investor(s).

(viii) Total subscription by all individuals, including Hindu Undivided Families, in any primary issuance of CPs or NCDs shall not exceed 25 per cent of the total amount issued.

(b) Discount/Coupon Rate

(i) CPs shall be issued at a discount to the face value.

(ii) NCDs shall be issued at a discount to the face value or with fixed or floating rate coupon.

(iii) The coupon on floating rate NCDs shall be linked to a benchmark published by a Financial Benchmark Administrator or approved by the Fixed Income Money Market and Derivatives Association of India (FIMMDA) for this purpose. FIMMDA shall ensure that any floating rate approved by them for this purpose is determined transparently, objectively and in arms’ length transactions. The coupon on floating rate NCDs can also be linked to policy rates published by the Reserve Bank.

(c) Credit Enhancement

(i) Banks and AIFIs may, based on their commercial judgement and subject to prudential guidelines issued by Department of Regulation, RBI, choose to provide stand-by assistance/credit, back-stop facility, etc., by way of credit enhancement for a CP/NCD issue.

(ii) Non-bank entities (including corporates) may provide unconditional and irrevocable guarantee for credit enhancement of CPs and NCDs issued by a group entity subject to making appropriate disclosures as set out in Annex I.

(d) End-use

(i) Funds raised through CPs and NCDs shall ordinarily be used to finance current assets and operating expenses. The end-use of the funds raised through a CP or an NCD shall be disclosed in the offer document.

(ii) Where funds raised are used for purposes other than financing current assets and operating expenses, the exact/ specific end-use shall be disclosed in the offer document.

(iii) The issuer shall submit a certificate from the Chief Executive Officer/Chief Financial Officer (CEO/CFO) to the IPAs concerned that the proceeds of CPs and NCDs have been used for the disclosed purposes and that all other provisions of these Directions and conditions of the offer document have been adhered to. The certificate shall be provided to the IPA within 3 months of the issue of CP/NCD or on maturity of the issue, whichever is earlier.

(e) Rating Requirement

The minimum credit rating, assigned by a Credit Rating Agency (CRA), for the issuance of CPs and NCDs shall be ‘A3’ as per rating symbol and definition prescribed by SEBI.

(f) Primary Market – Other Conditions

(i) An IPA shall be appointed for each issuance of a CP and an NCD. A Debenture Trustee shall also be appointed for each issuance of an NCD.

(ii) The subscription to the primary issue of a CP/NCD shall be routed through the IPA.

(iii) The aggregate amount of CPs and NCDs which can be issued by an issuer shall be within such limits as may be approved by the Board of Directors or its equivalent body. The aggregate amount which can be issued by an issuer regulated by a financial sector regulator shall also be subject to the limits, if any, specified by the regulator concerned.

(g) Secondary Market-Trading venue and settlement

(i) CPs and NCDs shall be traded either in OTC markets, including on ETPs, or on recognised stock exchanges, approved by the Reserve Bank for the purpose.

(ii) The settlement cycle for OTC trades in CPs and NCDs shall be either T+0 or T+1.

(iii) All OTC secondary market transactions in CPs (including transactions undertaken on ETPs) shall be settled on a DvP basis through the clearing corporation of any recognised stock exchange, or any other mechanism approved by the Reserve Bank.

(iv) All OTC secondary market transactions in NCDs (including transactions undertaken on ETPs) shall be settled bilaterally, or on a DvP basis through the clearing corporation of any recognised stock exchange, or any other mechanism approved by the Reserve Bank.

(h) Buyback

Issuers of CPs and NCDs are permitted to buyback the CPs and NCDs before maturity. Such buybacks shall be subject to the following conditions:

(i) The buyback of CPs can be made only after seven days from the date of issue. The buyback of NCDs can be made only after ninety days from the date of issue.

(ii) The buyback offer shall be extended to all investors in a particular issue on identical terms and conditions. The investors shall have the option to accept or reject the buyback offer.

(iii) Buyback of CPs and NCDs shall be at the prevailing market price.

(iv) The issuer of a CP/NCD shall inform the details of the buyback to the IPA on the date of buyback. In the case of NCDs, the details shall also be informed to the Debenture Trustee.

(v) The payment for the buyback of the CP/NCD by the issuer shall be routed through the IPA.

(vi) CPs and NCDs bought back, partially or in full, shall be extinguished on the date of buyback.

(i) Repayment of CPs / NCDs

(i) There will be no grace period for repayment of CPs/NCDs.

(ii) The issuer shall make the funds for redemption available to the IPA by 3:00 P.M. on the redemption date.

(iii) The repayment of a CP/NCD, including coupon payments, shall be routed through the IPA.

(j) Default

(i) The issuer who has defaulted on the repayment of a coupon/redemption, partially or in full, of a CP and/or NCD shall inform the details of any default in payments related to a CP/NCD to the IPA before 5:00 pm on the date of the default. In the case of NCDs, the details shall also be informed to the Debenture Trustee.

(ii) Information about any default in payments related a CP/NCD shall be publicly disseminated (e.g., through its website) by the issuer. Default details shall also be publicly disseminated on the F-TRAC Trade Repository Platform of Clearing Corporation of India Ltd (‘F-TRAC platform’) as specified under Para 6(d) of these Directions.

(iii) Repayments of obligations under a defaulted CP or NCD can be made directly to the investor/s by the issuer or can be routed through the IPA or Debenture Trustee. Partial repayments, if any, of a CP/NCD shall be distributed to investors of the CP/NCD in proportion to the investment made in the CP /NCD.

(iv) Details of the repayment of the obligations related to defaulted CPs/NCDs shall be informed to the IPA and the Debenture Trustee by the issuer on the date of the repayment.

(v) In the event of a CP/NCD, being converted into another financial instrument after default, as part of any bilateral / multilateral agreement or restructuring scheme, the CP/NCD shall stand extinguished on the date of its conversion.

(vi) In the event of default of a CP / NCD, the issuer shall not be allowed to issue CPs or NCDs till full repayment of the defaulted obligation or six months after the date of default, whichever is earlier.

(vii) Any event of conversion of a CP/NCD into another financial instrument shall be reported by the issuer to the IPA and the Debenture Trustee.

(k) Market timing

Primary issuance and secondary market trading hours shall be between 9:00 AM and 5:00 PM on a working day or as specified by the Reserve Bank from time to time.

(l) Market Practices and Documentation

Participants / agencies in the CP and NCD markets shall follow any standardised procedures and documentation which may be prescribed by FIMMDA, in consultation with the Reserve Bank, for smooth functioning of the markets.

6. Reporting requirements

(a) Primary issuances: Details of all issuances in primary markets of the CPs and NCDs shall be reported by the IPA on the F-TRAC platform by 5:30 PM on the day of issuance.

(b) Secondary market transactions: All secondary market transactions in CPs and NCDs, executed in the OTC market and/or on the recognised stock exchanges, shall be reported with time stamp within 15 minutes of execution (the time when price is agreed) on the F-TRAC platform by each counterparty to the transaction.

(c) Buybacks: Details of buybacks of CPs and NCDs shall be reported by the IPA on the F-TRAC platform by 5:30 PM on the buyback date.

(d) Default: Instances of default and repayment of defaulted obligation shall be reported by the IPA on the F-TRAC platform by 5:30 PM on the day of default or the day of repayment of defaulted obligations, as the case may be.

(e) Reporting by depositories: The depositories shall report to the Reserve Bank, the details of the CPs and NCDs held with them in the dematerialised form, in the prescribed format furnished in Annex II, at fortnightly intervals (on the 15th day and on the last day of the month) or as and when called upon to do so by the Reserve Bank.

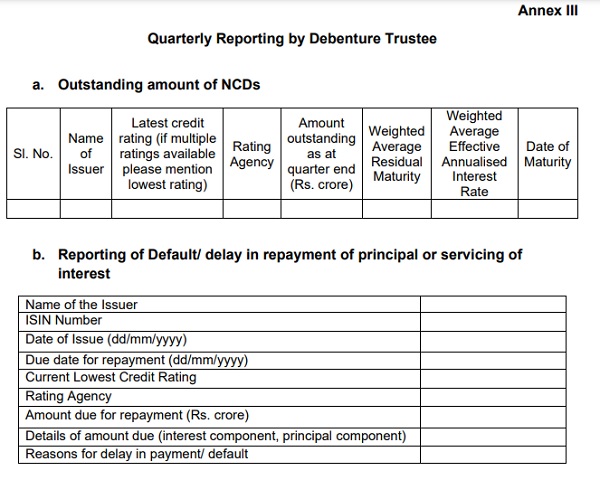

(f) Reporting by Debenture Trustee: The Debenture Trustee shall report the details of the outstanding amount of NCDs and the particulars of default in repayment of NCD, at quarterly intervals (within 15 days from the end of the quarter), in the format prescribed in Annex III to the Reserve Bank through email (reportfmd@rbi.org.in).

7. Roles and responsibilities

The roles and responsibilities of the IPA, Debenture Trustee and Credit Rating Agency (CRA) with respect to the operations in CP and NCD markets are set out below:

(a) Issuing and Paying Agent: The IPA for an issuance shall:

(i) Ensure that the issuer of a CP/NCD is authorised to borrow through CPs and/or NCDs and that the issuance is in compliance with these Directions.

(ii) Verify and hold certified copies of original documents and/or digitally signed documents related to the issuance in its custody.

(iii) Issue an IPA certificate that all information and documents submitted by the issuer are in order.

(iv) Make available the IPA certificate in electronic form on the website of the depositories for the CPs or NCDs issued.

(v) Obtain the certificate referred to in Para 5(d)(iii) of these Directions from the CEO/CFO of the issuer.

(vi) Ensure that the reporting obligations specified in these Directions are complied with.

(vii) The Reserve Bank may, in the event of an IPA violating any provision of these directions, or any other directions/ regulations/guidelines issued by the Bank from time to time in this regard, disallow an entity from acting as IPA for CP/NCD issuances for a period, as may be decided by the Reserve Bank.

(b) Debenture Trustee

(i) The roles, responsibilities, duties and functions of the Debenture Trustees shall be guided by the Securities and Exchange Board of India (Debenture Trustees) Regulations, 1993, the provisions of Companies Act, 2013 related to Debenture Trustees, as applicable, the trust deed and the offer document.

(ii) The Debenture Trustee shall ensure that the reporting obligations specified in these Directions are complied with.

(iii) The Debenture Trustee shall submit to the Reserve Bank any information regarding NCDs, as may be required by the Reserve Bank from time to time.

(iv) The Reserve Bank may, in the event of a Debenture Trustee violating any provision of these directions, or any other directions/ regulations/guidelines issued by the Bank from time to time in this regard, disallow an entity to act as Debenture Trustee for an NCD issuance for a period, as may be decided by the Reserve Bank.

(c) Credit Rating Agency

(i) A CRA registered with SEBI and accredited by the Reserve Bank as External Credit Assessment Institution (ECAI) for assigning bank loan ratings shall be eligible to rate CPs and NCDs.

(ii) CRAs shall abide by the guidelines issued by SEBI as applicable to securities mutatis mutandis for ratings of CPs/NCDs. They shall also abide by any guidelines issued from time to time by the Reserve Bank in this regard.

(iii) CRAs may also abide by any directions/regulations/guidelines issued by any regulator or other authority in respect of rating of CPs and NCDs provided that such directions/regulations/guidelines do not conflict with these Directions or any guidelines issued from time to time by the Reserve Bank in this regard.

(iv) A CRA which has been deregistered by SEBI or dis-accredited by the Reserve Bank as an ECAI for assigning bank loans ratings, shall no longer be eligible to rate CPs/ NCDs. The Reserve Bank may also, in the event of a CRA violating any provision of these directions, or any other guidelines issued by the Bank from time to time in this regard, disallow the CRA from rating CPs / NCDs for a period, as may be decided by the Reserve Bank.

8. Obligation to provide information sought by the Reserve Bank: The Reserve Bank may call for any information or seek any clarification from any agency involved in the CP and NCD markets, including but not limited to, issuers, investors, IPAs, debenture trustees, CRAs, depositories, the clearing corporations and the stock exchanges, which in the opinion of the Reserve Bank is relevant and the agency shall furnish such additional information and clarification within the time frame specified.

9. Dissemination of data: The Reserve Bank or any other agency authorised by it, may, in public interest, publish any anonymised data related to primary and secondary market transactions in CPs and NCDs.

10. Violation of Directions: In the event of any person violating any provision of these Directions, the Reserve Bank may, in addition to taking any penal or regulatory action in accordance with law, disallow that person from participating in the CP and NCD markets for a period not exceeding one month at a time, after providing reasonable opportunity to the entity to defend its actions, and such action would be made public by the Reserve Bank.

11. Applicability of other laws, directions, regulations or guidelines: Participants in the CP and NCD markets shall abide by the provisions of any direction, regulation, or guideline issued by any other regulator or authority, that may be applicable, in respect of issue of or investment in CPs and NCDs, provided that such directions, regulations or guidelines do not conflict with these Directions. In case of any conflicts, the provisions of these Directions shall prevail.

12. Non-applicability of Certain Other Directions: Nothing contained in the Master Direction – Non-Banking Financial Companies Acceptance of Public Deposits (Reserve Bank) Directions, 2016, as updated from time to time, shall apply to the raising of funds by issuance of CPs, by any NBFC when such funds are raised in accordance with these Directions.

13. These Directions shall apply to transactions in CPs and NCDs entered into from the date the Directions come into effect. Provisions of Section IV of FMRD. Master Direction No. 2/2016-17 dated July 07, 2016, Notification No. FMD.MSRG.49/02.13.016/2010-2011 dated July 28, 2010 and Direction No. FMRD.DIRD.01/CGM (TRS) – 2017 dated August 10, 2017 will continue to be applicable to the CPs and NCDs issued in accordance with the said Directions till the maturity of those CPs and NCDs.

(Dimple Bhandia)

Chief General Manager

Annex I

Minimum disclosure in the offer document by issuers of CP and NCD

i. Details of outstanding CPs, NCDs and other debt instruments as on date of offer letter, including amount issued, maturity date, amount outstanding, credit rating and name of credit rating agency for the issue, name of IPA and Debenture Trustee.

ii. Net-worth of the issuer as per the latest balance sheet.

iii. Shareholding of the issuer’s promoters and the details of the shares pledged by the promoters, if any.

iv. Long term credit rating, if any, obtained by the issuer.

v. Unaccepted credit ratings, if any, assigned to the issuer.

vi. Summary of audited financials of last three years, material litigation and regulatory actions related to the issuer. If the issuer has not been in existence for three years, the information of the issuer for the period such information is available shall be disclosed.

vii. Any material event/ development having implications for the financials/ credit quality resulting in material liabilities, corporate restructuring event which may affect the issue or the investor’s decision to invest in the CP/NCD.

viii. All details of credit enhancement including backstop facilities provided by the group entity including but not limited to (a) the net-worth of the guarantor, (b) the names of the companies to which the guarantor has issued similar guarantees, (c) the extent of the guarantees offered by the guarantor and (d) the conditions under which the guarantee will be invoked, etc.

ix. Details of default of CP, NCD or any other debt instrument and other financial indebtedness including corporate guarantee issued in the past five financial years including in the current financial year.

x. Details of statutory auditor and changes thereof in the last three financial years.

xi. Details of current tranche including amount, current credit rating for the issue, name of credit rating agency, its validity period and details of IPA and Debenture Trustee.

xi. Specific details of end-use of funds.

xiii. An issuer which is either an NBFC or an HFC shall disclose the residual maturity profile of its assets and liabilities in the following format:

Category |

Up to30/31 days |

>1 month– 2

|

>2 months –3 months |

>3 months –6 months |

>6months –1 year |

> 1 year – 3 years |

>3 years –5 years |

>5 years |

Total |

Deposit |

|||||||||

Advances |

|||||||||

Investments |

|||||||||

Borrowings |

|||||||||

ForeignCurrencyAssets(FCA) |

|||||||||

Foreign Currency Liabilities (FCL) |

Annex II

Details of the outstanding Commercial Papers (CPs) held with _____ as on date

Serial No. |

Name ofIssuer |

Issuer Code |

Issuer Category |

IS IN |

Security Descri ption |

Maturity Date |

Residual Tenor (Days) as on |

Name of IPA |

Inve stor Name |

Investor Scheme Name, if any |

Investor Categ ory |

Amount in ₹ Cr. (Face Value) |

Details of the outstanding Non-Convertible Debentures (NCDs) held with _____ as on date

Serial No. |

Name of Issuer |

Issuer Code |

Issuer Categ ry |

ISIN |

Security Desc ription |

Maturity Date |

Residual Tenor (Days) as on |

Name of Debe nture Trustee |

Investor Name |

Inve stor Scheme Name, if any |

Inve stor Cat egory |

Am ount in ₹ Cr. (Face Value) |

Annex III