Case Law Details

SCMS Maritime Training Institute Vs Ward 25(1)(1) (ITAT Mumbai)

Income Tax Appellate Tribunal (ITAT), Mumbai Bench, has provided relief to SCMS Maritime Training Institute, a trust, by ruling that its gross receipts cannot be fully subjected to tax even if it loses its exemption under Section 11 of the Income Tax Act, 1961. The Tribunal, in its order dated May 27, 2025, remitted the case back to the Assessing Officer for re-computation, emphasizing that only the net surplus, after allowing legitimate expenditure and depreciation, can be taxed.

The appeal was filed by the assessee against an order passed by the National Faceless Appeal Centre (NFAC), Delhi, dated September 24, 2024, which confirmed an assessment by the Centralized Processing Centre (CPC), Bengaluru. The dispute pertained to Assessment Year 2022-23.

SCMS Maritime Training Institute, a trust registered with the Charity Commissioner, Maharashtra, operates with the objective of imparting education and pursuing other charitable activities, specifically training merchant navy candidates at subsidized rates. The trust had initially obtained registration under Section 12AA of the Act on November 1, 2010.

However, a significant amendment introduced by the Finance Act, 2021, mandated all registered trusts to apply for renewal or fresh registration under the newly inserted Section 12AB of the Act. The assessee failed to comply with this requirement for Assessment Year 2022-23. Despite this non-compliance, the trust filed its return of income claiming exemption under Section 11, albeit by mentioning its old 12AA registration number. The return reported a net surplus of Rs. 1,86,512/-.

The CPC, upon processing the return, determined the total income at Rs. 32,27,675/-, effectively disallowing the Section 11 exemption and taxing the entire gross receipts. The assessee sought rectification from the CPC under Section 154, but this application was rejected. Subsequently, an appeal was filed before the Commissioner of Income Tax (Appeals), which was dismissed ex-parte without providing an opportunity of hearing to the assessee.

Before the ITAT, the assessee’s counsel presented the provisional registration granted under Section 12A and Section 80G dated January 5, 2024, for the period from AY 2024-25 to AY 2026-27. While admitting that the Section 11 exemption was not available for the year under consideration due to the lack of renewed registration, the counsel argued that taxing the entire gross receipts was incorrect. He contended that only the net surplus, after deducting expenses and depreciation incurred for carrying out charitable activities, should be brought to tax.

The Departmental Representative argued that in the absence of a valid Section 12A registration, the assessee’s income was indeed subject to tax.

The ITAT, after considering both sides, first noted that the CIT(Appeals) had passed an ex-parte order without addressing the merits of the case, which is a procedural lapse. On the substantive issue of taxation, the Tribunal concurred that the assessee was not eligible for Section 11 exemption for the relevant year due to non-renewal of registration. However, the ITAT strongly disagreed with the CPC’s action of taxing the entire gross receipts.

Applying the principle of “commercial prudence,” the Tribunal held that even if the exemption is denied, the corresponding expenditure incurred by the assessee to carry out its activities, along with depreciation, must be allowed as deductions. Only the actual net surplus can be subjected to tax. This aligns with the fundamental principles of income computation under the Income Tax Act, where income is generally computed after allowing for expenses incurred to earn that income. While no specific judicial precedent was cited in the order, this principle has been consistently upheld by various courts and tribunals, emphasizing that even if an exemption is lost, the income cannot be arbitrarily assessed on a gross basis without considering the costs of earning it.

Consequently, the ITAT remitted the matter back to the Jurisdictional Assessing Officer (JAO) with directions to verify the assessee’s records, allow the claimed expenditure and depreciation, and tax only the net surplus for the year. The JAO was also directed to provide the assessee a reasonable opportunity of being heard. The appeal was allowed for statistical purposes, meaning the procedural aspects were addressed, and the substantive re-computation will occur at the AO level.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

This appeal filed by the assessee is against the order of National Faceless Appeal Centre (NFAC), Delhi, vide order no. ITBA/NFAC/S/250/2024-25/1069046121(1), dated 24.09.2024 passed against the assessment order/notice by Centralized Processing Centre (CPC) u/s. 154 of the Income-tax Act, 1961 (hereinafter referred to as the “Act”), dated 24.09.2024 for Assessment Year 2022-23.

2. Grounds taken by the assessee are reproduced as under:

1. On the facts, and in circumstances of the case, and in law, learned Commissioner of Income-tax (Appeal) disposed of the appeal without fixing hearing and giving opportunity of being heard.

2. On the facts, and in circumstances of the case, and in law, learned Commissioner of Income-tax (Appeal) erred in upholding action of the Centralized Processing Centre (CPC), Bengaluru in disallowing claim of exemption under section 11 of the Income Tax Act, 1961 without assigning any particular reason, and merely on the basis of providing old registration number allotted under section 12AA instead of providing new registration number to the trust under new section 12AB of the Income Tax Act, 1961.

3. On the facts, and in circumstances of the case, and in law, learned Commissioner of Income-tax (Appeal) erred in upholding action of the Centralized Processing Centre (CPC), Bengaluru in bringing to tax an amount of RS. 3,227,675 comprising of Gross Receipts of RS. 3,041,163 in as much as net surplus of RS. 186,512 in place of only net surplus of RS. 186,512 to tax.

4. Your Appellant craves leave to add to, amend, alter, modify, and/or delete any of the above grounds of appeal at or before final disposal of appeal.

3. Brief facts of the case are that assessee is a trust registered with Charity Commissioner, Maharashtra, Mumbai. It is stated that object of the assessee trust is to impart education and pursue other charitable objects. Assessee is engaged in imparting and training merchant navy candidates by running various courses at subsidized rates. Assessee was granted registration u/s.12AA by DIT(Exemption) vide Registration No.42018 dated 01.11.2010. Owing to amendment brought in by Finance Act, 2021, registered trust were required to make application for renewal of their registration u/s.12AB of the Act. Without complying with the requirement to make fresh application as required under the amended law, assessee filed its return of income for the year under consideration reporting total income at Rs.1,86,512/- after claiming exemption u/s.11 of the Act, by mentioning the old registration number. CPC processed the return whereby total income was determined at Rs.32,27,675/-. Assessee filed an application before CPC u/s. 154 of the Act, claiming for rectification of mistake apparent from record which was processed and order was passed on 24.08.2023 against which assessee went in appeal before the Ld. CIT(A).

3.1 Assessee claims that CPC has denied exemption u/s.11 of the Act, resulting into addition of the entire gross receipts. According to the assessee, without prejudice, it was claimed that even on commercial prudence, entire gross receipts cannot be brought to tax. Corresponding expenditure incurred by the assessee to carry on its activities during the year ought to be allowed as a deduction against the gross receipts of the year. It is only the net which alone can be brought to tax. Ld. CIT(A) had passed an ex-parte order dismissing the appeal against which assessee is in appeal before the Tribunal.

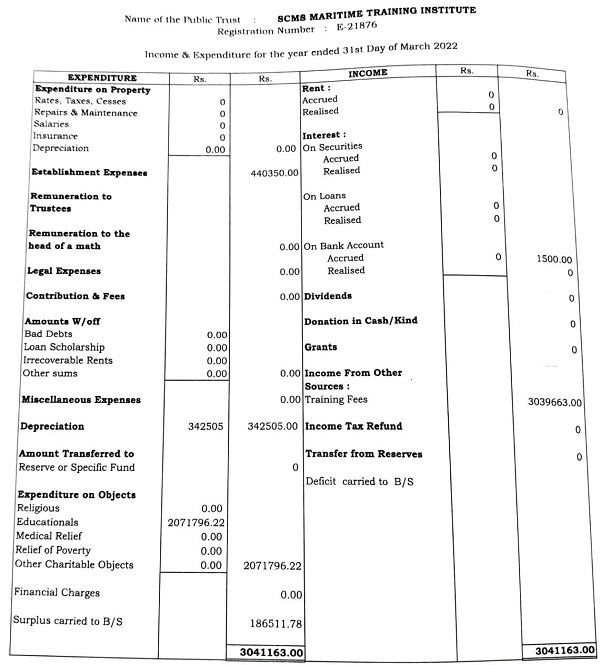

4. Before us, Ld. Counsel for the assessee placed on record, provisional registration granted to it u/s.12A and u/s.80G vide Form No.10AC. The date of provisional registration granted is 05.01.2024 for the period from AY 2024-25 to AY 2026-27. Assessee also placed on record its computation of total income and tax liability to demonstrate that total receipts for the year are Rs.30,41,163/- and after incurring expenditure on the charitable activities undertaken by it as well as depreciation, the surplus remained for the year is Rs.1,86,512/-. Thus, according to the assessee, what can be brought to tax for the year under consideration in absence of renewed registration u/s.12A is the surplus of Rs.1,86,512/- alone. In this regard, the income and expenditure statement for the year under consideration is extract below for ready reference:

5. Per contra, Ld. Senior DR submitted that there is no registration available with the assessee u/s.12A to justify claim of exemption u/s.11 of the Act. Accordingly, its income is subjected to tax for the year under consideration.

6. We have heard both the parties and perused the material available on record. We note that Ld. CIT(A) has passed an ex-parte order without dealing with the merits of the case. Admittedly, it is a fact on record that assessee does not have the renewed registration u/s.12A of the Act for the year under consideration. Ld. Counsel for the assessee admitted that in absence of such registration for the year under consideration, claim of exemption u/s.11 of the Act, is not available, but at the same time what can be brought to tax is the net income for the year after allowing expenditure and depreciation for caring out its activities during the year.

6.1. Taking into account the facts of the case, we hold that gross collection for the year cannot be taxed as income as done by CPC while processing the return of the assessee. Commercial prudence requires to allow deduction for matching expenditure incurred by the assessee in caring out its activities during the year. Accordingly, we find it appropriate to remit the matter back to the file of ld. Jurisdictional Assessing Officer (JAO) for the purpose of verification of records and details of the assessee to allow claim of expenditure and deprecation made by it so as to bring to tax the net surplus for the year. Needless to say that assessee be given reasonable opportunity of being heard and make any other submission as required to substantiate its claim. Accordingly, grounds raised by the assessee are allowed for statistical purposes.

7. In the result, appeal of the assessee is allowed for the statistical purposes.

Order is pronounced in the open court on 27th May, 2025

Author Bio