1. Introduction to Buyback Tax and Its Evolution (Budget 2026 Perspective)

Share buybacks have become a common method for companies to return surplus cash to shareholders. Instead of paying dividends, companies repurchase their own shares, which reduces the number of shares in the market and may improve earnings per share (EPS). While this approach is financially efficient, it is regulated and taxed to ensure fairness and prevent misuse.

Buyback taxation was introduced to address the difference between dividend taxation and capital gains taxation. In the past, dividends were taxed more heavily, while buybacks allowed certain investors especially promoters and large shareholders to benefit from lower capital gains tax. This encouraged companies to prefer buybacks mainly for tax advantages rather than genuine financial reasons.

To mitigate this imbalance, governments implemented a buyback tax regime, wherein companies undertaking share repurchases are taxed on the distributed income. This income is generally calculated as the difference between the buyback price and the original issue price of the shares. Over time, the regulatory framework has undergone several amendments to refine its scope, enhance transparency, and ensure fair tax treatment.

As part of Budget 2026, revised buyback tax provisions have been introduced with the objective of strengthening compliance, curbing tax arbitrage, and aligning the taxation of buybacks more closely with dividend distribution. Effective from April 1 of the applicable financial year, these changes carry significant implications for corporate financial strategies, investor returns, and the overall efficiency of capital markets.

2.Key Provisions Effective from April 1 (Budget 2026)

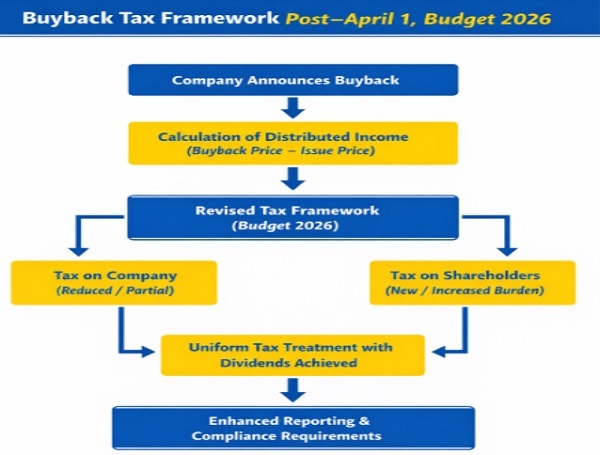

The revised buyback tax framework introduced under Budget 2026, effective from April 1 of the relevant financial year, brings significant structural changes aimed at improving tax equity, transparency, and regulatory oversight. The key provisions are outlined below:

1. Tax Incidence Shift

A fundamental reform is the reallocation of tax liability. Under the earlier regime, companies were responsible for paying buyback tax on distributed income. The revised framework introduces a shift whereby the tax burden may now be partially or fully borne by shareholders, depending on the applicable structure and jurisdiction.

This approach aligns the taxation of buybacks with the dividend taxation system, where shareholders are taxed on income received, thereby ensuring consistency in treatment.

2. Uniform Tax Treatment

The reform eliminates tax arbitrage between dividends and share buybacks. Previously, companies often preferred buybacks due to favourable tax treatment. The updated provisions ensure that both mechanisms of profit distribution are taxed in a comparable manner, encouraging companies to base decisions on financial and strategic considerations rather than tax advantages.

3. Expanded Scope of Applicability

The scope of buyback taxation has been broadened significantly. Earlier provisions were often limited to unlisted companies or specific categories. Under the revised framework, the applicability now extends to a wider range of entities, including listed companies, thereby addressing regulatory gaps and closing potential loopholes.

4. Tax Rate Adjustments

The effective tax rates applicable to buybacks have been revised in line with current fiscal policy objectives. This may include the application of surcharge and cess, which increases the overall tax burden on distributed income. The revised rates aim to ensure fairness while maintaining revenue neutrality for the government.

5. Enhanced Reporting and Compliance Requirements

To strengthen governance and transparency, companies undertaking share buybacks are now subject to stricter compliance obligations. These include:

- Detailed disclosure of source of funds

- Justification of buyback pricing

- Information on shareholder participation

- Timely and accurate regulatory filings

These measures are intended to prevent misuse, improve accountability, and enhance investor confidence.

3. Impact of Buy back Tax Changes on various segments.

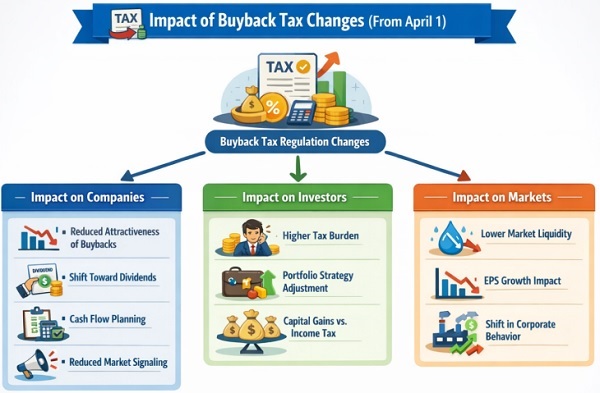

The changes in buyback tax regulations from April 1 have far-reaching consequences:

A. Impact on Companies

- Reduced Attractiveness of Buybacks: With increased tax liability, buybacks may no longer be as tax-efficient as before.

- Shift Toward Dividends: Companies may prefer dividend payouts, especially if tax treatment becomes comparable.

- Cash Flow Planning: Firms must carefully evaluate their capital allocation strategies, considering both tax implications and shareholder expectations.

- Market Signaling: Buybacks often signal confidence in a company’s future. Changes in tax policy may reduce the frequency of such signals.

B. Impact on Investors

- Tax Burden: Investors may now face higher taxes on income received through buybacks, depending on the structure.

- Portfolio Strategy: Long-term and short-term investors may need to reassess their strategies, especially regarding capital gains versus income taxation.

- Reduced Arbitrage Opportunities: The alignment of tax treatment reduces the advantage of structuring returns through buybacks.

C. Impact on Markets

- Liquidity Considerations: Reduced buyback activity could affect market liquidity and stock price support.

- Valuation Metrics: Changes in EPS growth due to fewer buybacks may influence valuation models.

- Corporate Behavior: Companies may focus more on reinvestment or debt reduction instead of returning cash.

4. Challenges in Implementation

While the revised buyback taxation framework introduced in Budget 2024 aims to improve neutrality and fairness in the taxation of corporate distributions, its implementation presents several practical and structural challenges:

Valuation Complexities and Disputes.

Determining the issue price of shares especially for legacy holdings acquired prior to dematerialization or corporate restructuring can be highly complex. This creates scope for disputes between taxpayers and authorities regarding the computation of distributed income, particularly in cases involving mergers, bonus issues, or stock splits.

- Risk of Economic Double Taxation.

Although the reform shifts the tax burden from the company to shareholders, there remains a possibility of economic double taxation. Income distributed through buybacks may be taxed as dividend income in the hands of shareholders, while capital invested may have already been subject to tax at earlier stages, reducing overall tax efficiency.

- Increased Compliance and Administrative Burden

The revised regime requires detailed reporting, tracking of cost of acquisition, and proper classification of income. This increases compliance costs for companies and shareholders alike, particularly for institutional investors and foreign portfolio investors who must navigate cross-border tax rules.

- Impact on Corporate Financial Strategy.

Companies may need to reassess their capital allocation strategies, as buybacks are no longer as tax-efficient as they were under earlier frameworks (e.g., post-2019 buyback tax regime). This could lead to a shift toward dividends or reinvestment, affecting financial planning and shareholder expectations.

5. Critics vs Supporters of Buyback Tax Policy

The revised buyback taxation framework has generated mixed reactions among stakeholders:

Critics vs Supporters of Buyback Tax Policy

| S. No | Critics Argue | Supporters Contend |

| 1. | Reduced Efficiency in Capital Allocation.

The increased tax burden may discourage companies from using buybacks as a flexible tool for returning excess cash, potentially leading to suboptimal capital allocation. |

Enhanced Tax Equity and Neutrality

The reform aligns the taxation of buybacks with dividends, ensuring consistency across different modes of profit distribution. |

| 2. | Adverse Impact on Investor Returns Since buyback proceeds are taxed in the hands of shareholders, post-tax returns may decline, particularly affecting minority and retail investors. |

Reduction in Tax Arbitrage Opportunities

Earlier, companies could structure payouts via buybacks to minimize tax liability; the new framework curtails such practices |

| 3. | Policy Uncertainty and Frequent Changes Repeated amendments (from 2019 to 2024) create uncertainty, making long-term financial and investment planning more difficult |

Improved Transparency and Accountability Taxation at the shareholder level increases visibility and ensures income is taxed in the hands of the ultimate beneficiary. |

| 4 | Disproportionate Impact on Certain Investor Classes.

Foreign investors and high-net-worth individuals may face additional complexities due to treaty interpretations and varying tax treatments. |

Augmented Government Revenue.

By broadening the tax base, the policy contributes to a more stable and equitable revenue system. |

By broadening the tax base, the policy contributes to a more stable and equitable revenue system.

7. Conclusion

The changes in buyback taxation, including reforms up to Budget 2026, show the government’s effort to create a fair and balanced tax system. These reforms help reduce tax avoidance and make buybacks similar to dividend taxation, but they also make the system more complex.

The success of this policy depends on clear rules, stable tax laws, and how well companies and investors adjust to the changes. It is important to keep a balance between fairness and ease of compliance so that buybacks remain a useful financial tool.

Companies may need to rethink how they use their funds, while investors must plan their taxes and investments more carefully. In the long run, the policy will succeed if it maintains a balance between government revenue, market efficiency, and investor confidence.

Author Bio