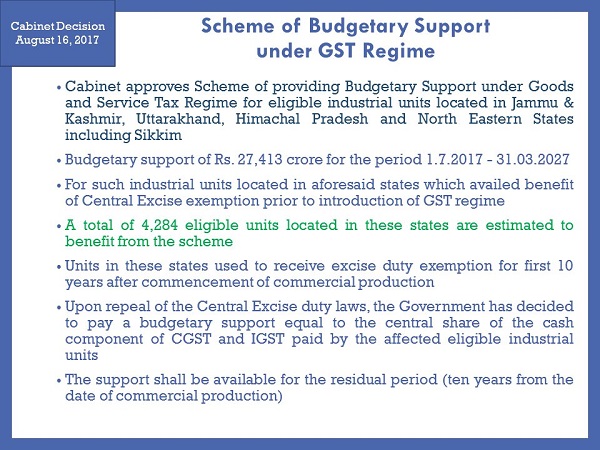

Cabinet approves Scheme of Budgetary Support under GST Regime to the eligible units located in States of Jammu & Kashmir, Uttarakhand, Himachal Pradesh and North Eastern States including Sikkim

The Cabinet Committee on Economic Affairs chaired by the Prime Minister Shri Narendra Modi today has given its approval to the Scheme of providing Budgetary Support under Goods and Service Tax Regime for the eligible industrial units located in State of Jammu & Kashmir, Uttarakhand, Himachal Pradesh and North Eastern States including Sikkim. Budgetary support of Rs. 27,413 crore for the said Scheme has been approved for the period from 1.7.2017 till 31.03.2027 for such industrial units located in aforesaid States which availed the benefit of Central Excise exemption prior to coming into force of GST regime.

The Government of India was implementing North East Industrial and Investment Promotion Policy (NEIIPP), 2007 for North Eastern States including Sikkim and Package for Special Category States for Jammu & Kashmir, Uttarakhand and Himachal Pradesh to promote industrialization. One of the benefits of the NEIIPP, 2007 and Package for Special Category States was excise duty exemption for first 10 years after commencement of commercial production. Upon repeal of the Central Excise duty laws, the Government has decided to pay a budgetary support equal to the central share of the cash component of CGST and IGST paid by the affected eligible industrial units. The support shall be available for the residual period (ten years from the date of the commercial production) in the States of North Eastern region and Himalayan States. DIPP will notify the Scheme, including detailed operational guidelines for implementation of the scheme within 6 weeks. It is estimated that total number of 4284 eligible units located in the State(s) of Jammu & Kashmir, Uttarakhand, Himachal Pradesh and North Eastern States including Sikkim will benefit from the above scheme.

Kindly Refer to

Privacy Policy &

Complete Terms of Use and Disclaimer.