A lot of confusion has been created pertaining to the remuneration paid by companies to their Directors as to whether it would fall under the ambit of entry in Schedule III of the Central Goods and Services Tax Act, 2017 (hereinafter referred to as the “CGST Act”) i.e. “services by an employee to the employer in the course of or in relation to his employment” or whether the same would be liable to be taxed in terms of notification No. 13/2017 – Central Tax (Rate) dated 28.06.2017 (entry no.6). Considering the difficulty faced by various decisions and recent notices CBIC has issued clarification vide Circular No. CBEC-20/10/05/2020 –GST dated June 10, 2020.

KEY TAKEAWAYS OF THE CIRCULAR:

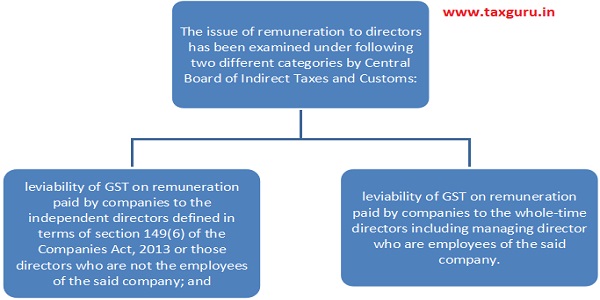

For understanding the levy of GST on Directors remuneration first And foremost is to identify whether the director is an employee of the company or not and secondly if the director is an employee of the company further examination is required as to whether all the activities performed by the director are in the course of employer-employee relation (i.e. a “contract of service”) or is there any element of “contract for service”.

In order to decide whether or not a Director is an employee of the Company the circular considered the following relevant provisions of the Companies Act, 2013:

> The definition of a Whole Time-Director under section 2(94) of the Companies Act, 2013 is an inclusive definition, and thus he may be a person who is not an employee of the company.

> The definition of Independent Directors under section 149(6) of the Companies Act, 2013, read with Rule 12 of Companies (Share Capital and Debentures) Rules, 2014 makes it amply clear that such director should not have been an employee or proprietor or a partner of the said company, in any of the three financial years immediately preceding the financial year in which he is proposed to be appointed in the said company.

Applicability of GST on remuneration paid by companies to Independent Directors or those Directors who are not employee of Company:

> Directors who are not the employees of the said company, the services provided by them to the Company, in lieu of remuneration as the consideration for the said services, are clearly outside the scope of Schedule III of the CGST Act and are therefore taxable.

> The remuneration paid to such independent directors, or those directors, by whatever name called, who are not employees of the said company, is taxable in hands of the company, on reverse charge basis.

Applicability of GST on remuneration paid by Companies to Directors, who are also an employee of Company:

> The part of Director’s remuneration which are declared as Salaries in the books of a company and subjected to TDS under Section 192 of the IT Act, are not taxable being consideration for services by an employee to the employer in the course of or in relation to his employment in terms of Schedule III of the CGST Act, 2017.

> The part of employee Director’s remuneration which is declared separately other than salaries in the Company’s accounts and subjected to TDS under Section 194J of the IT Act as Fees for professional or Technical Services shall be treated as consideration for providing services which are outside the scope of Schedule III of the CGST Act, and is therefore, GST shall be payable under Reverse Charge Mechanism.

Disclaimer: The entire contents of this article have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, we assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. We assume no responsibility for the consequences of use of such information. In no event shall we shall be liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information. This is only a knowledge sharing initiative and author does not intend to solicit any business or profession.

| Jaya Sharma Founder- Jaya Sharma & Associates jaya@jsa-cs.com |

Sunita Choudhary Jaya Sharma & Associates bodha@jsa-cs.com |