Introduction: Delve into the intricacies of the order DRC-07 issued by the Office of the Assistant Commissioner of Commercial Taxes, shedding light on tax demands, regulatory compliance, and implications for M/s Raja Likshmi Engg Works. This comprehensive summary elucidates the legal proceedings and financial obligations outlined in the order, providing valuable insights into the realm of commercial taxation.

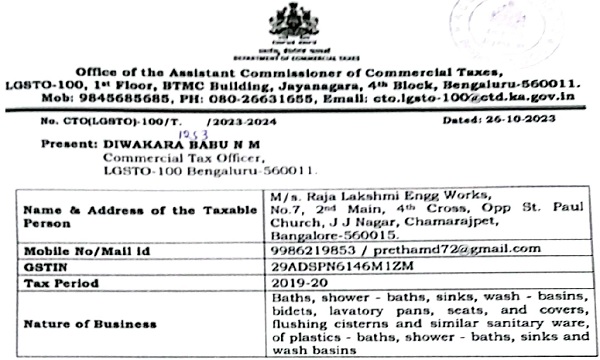

Office of the Assistant Commissioner of Commercial Taxes,

Ulf:TU.100, 1″ Floor, IITMC Building, Jayanagara, 4th Block, Bengaluru 560011.

Mob: 9845685685, PH: 080-26631655, cto.lgsto-100@ctd.ka.gov.in

CTO(LGSTO)-100/T.1953/2023 2024

Dated: 26-10-2023

FORM GST DRC-07

(See rule 100(1), 100(2), 100(3) & 142(5)1

Summary of the order

(Annexed separately)

1. Details of order:

(a) Order No 23/ORC-07/2023-24

(b) Order date 26-10-2021

(c) Financial year: 2019-20

(d) Tax period: Mar-2020

2. Issues involved: Eligibility and conditions for taking input tax credit

3. Description of goods / services (if applicable):

| Particulars | HSN | Description |

| Goods | 39221000 |

Baths, shower baths, sinks, wash basins, bidets, lavatory pans, seats, and covers, flushing cisterns and similar sanitary ware, of plastics baths, shower baths, sinks and wash basins |

4. Section(s) of the Act under which demand is created: Order Under Section 73 of the KGST Act 2017

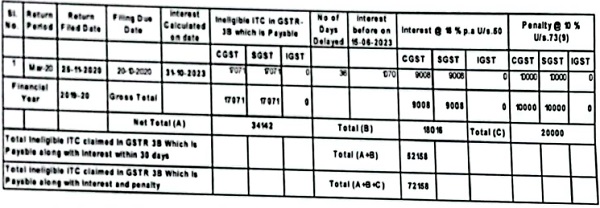

5. Details of demand Amount in Rs. 72,158/- (Inclusive of Interest and Penalty)

You are hereby directed to make the payment within 30 days of date of receipt of this order. failing which proceedings shall initiated against you to recover the outstanding dues.

(DIWAKARA BABU N M)

Commercial Tax Officer

LGSTO-100, Bengaluru

To,

M/s Raja Likshmi Engg Works,

No 7, 2’1 Main, 40, Cross, Opp St. Paul Church,

J J Nagar, Chamarajpet, Bangalore-560015.

29ADSPN6146M1ZN1

Mob: 9986219853

Email: prethamd72iqgmail.com

ORDER UNDER SECTION 73 OF THE KARNATKA GOODS AND SERVICES TAX ACT,2017 / ORDER UNDER SECTION 73 READ WITH SECTION 6 OF THE CENTRAL GOODS AND SERVICES TAX ACT, 2017 / ORDER UNDER SECTION 20 OF THE INTEGRATED GOODS AND SERVICES TAX ACT, 2017

Ref: 1) JDN Order No. ADCOM (Audit)/JDN/CR-174/2021-22, dated 07-12-2021

2) Assignment No: JCCT(A)/DGTS0-03/A-73/156/2023-24, dated 04.05-2023

3) ASMT-10 notice issued on 23-12-2021 through e-mail.

4) Form GST DRC-01A issued on 19-05-2023.

5) DRC-01 and Show cause notice dated 18-07-2023.

M/s. Raja Lakshmi Engg Works having place of business at No.7, 2nd Main, 4th Cross, Opp St. Paul Chruch, J J Nagar, Chamarajpet, Bangalore-560015 is the proprietorship concern and registered with GSTIN: 29AJEPJ0767A1Z11 under the jurisdiction of LGSTO-100, Karnataka GST authority.

The GSTR3B furnished by the taxable person for the tax period APR-2019 to Mar-2020 was scrutinized by the undersigned under powers vested under Section 61 of Central /State Goods and Service Tax Act-2017/Karnataka Goods and Services Tax Act, 2017. On such scrutiny it was noticed that the taxable Person being registered under the Act and by virtue of whit authorized to collect the taxes on behalf of the government, hold the tax and remit hack such amounts collected to government account following the procedure prescribed under various provisions of the Act and Rules made their under The Person is required to file the outward supply statement in form GSTR 01 prescribed under section 37 within 10 days of the end of the tax period and the returns of his turnover and pay tax by filing the form GSTR-3B prescribed under section 39 within 20 days or any extended period from the end of the tax period as may notified by the government as per provisions of section 49 of the Act. The Person has filed the returns in form GSTR-311 for the tax periods of Mar-2020 during the financial year 2019-20 on 25-11-2020 and thereby the person is not eligible to claim any input tax on such returns filed beyond the due date of filing of the returns in form OSTR-313 for the tax period of September of the following financial year or the notified date of filing the annual return related to said financial year as governed under the provisions of section 16(4) of the Act.

The details of such input tax credits which were claimed in contravention of section 16(4) detailed as under:

As per Section 61 of Central /State Goods and Service Tax Act-2017 Read with rule 99(1) of the Central /State Goods and Service Tax Rules-2017. The above discrepancies were intimated to Taxable Person by issuing Form GST-ASMT-10, dated 23-12-2021 through the registered e-mail address provided to the Department, seeking the explanation to be filed in form GST ASNIT-11 within 30-days from the date of receipt of the Form GST-ASMT-10, dated 23-12-2021. Also, an opportunity to discharge such amounts of the tax along with applicable interest under section 50(1) of the Act. The person has failed to provide any reply as required under the Act. The undersigned has obtained the sanction of the jurisdictional Joint Commissioner of Commercial Taxes to determine the amount of tax, Interest and Penalty payable under section 73/74 of the Act vide No. JCCT(A)/DGSTO-3/A-73/ 156/2023-24, dated:04-05-2023.

Thereafter, Intimation of Tax/Penalty/Interest ascertained as being payable under section 73(5) of Central /State Goods and Service Tax Act-2017 was intimated to Taxable Person by issuing and serving a statement in FORM GST DRC-OlA (Part-Al dated: 19-05-2023 to the e-mail address provided to the Department. An opportunity was provided to discharge the amount of such tax so determined along with Interest. Further opportunity was also provided to file any submission with regarding to the Tax/Interest ascertained in FORM GST DRC-01A (Part-B) within Thirty days from the receipt of the statement. The Taxpayer has not responded to the pre-show cause notice proceedings afforded in DRC-01A.

In view of the above, the undersigned is of considered opinion that the person has no intention to pay the tax amounts due to the government has issued a show cause notice in the form GST DRC 01 dated 18-07-2023 under section 73(5) Read with Rules 100(2) and 142(1)(a) of Central /State Goods and Service Tax Act/Rules-2017 (Form GST DRC-01), the same was served by sending to the e-mail address provided to the Department and by providing one more opportunity to pay the tax/interest/penalty within 30 days from the date of receipt of show-cause notice. The said Show Cause Notice was also sent through boweb on 18-07-2023 vide reference No:

ZD2907230182891.

Further, an opportunity was also provided to file any submission for the Tax/Penalty/Interest quantified in the show-cause notice in writing and/or in person. The person has not responded to the said show cause notice in DRC-01 along with SCN notice.

SPECIFIC RESPONSES FOR THE ARGUMENTS RAISED:

1. The plausibility of form GSTR-3B being a return is already addressed by the Hon’ble Supreme Court of India in UOI v. AAP & Co. Civil Appeal No (s). 5978/2021 dated December 10, 2021 in line with UOI v. Bharti Airtel Limited CIVIL APPEAL NO. OF 2021 (ARISING OUT OF SLP (C) NO. 8654 OF 2020) dated October 28, 2021. The seamless utilization of input tax credit is available to the persons through retums prescribed under section 39(9) of the act read with Rule 61 of the Rules made thereunder.

2. The claim of input tax credit is not an absolute vested right. It is conditionally vested right and filing of the return is in a prescribed form and manner specified under the section 39 of this Act and Rules made thereunder. The same needs to be supported by the documents and books of accounts maintained under the relevant provisions of this Act is mandatory.

3. The taxpayer is collecting the taxes on behalf of the government being a registered person under the provision of this Act, holding the amount and he needs to furnish the returns in time setting off the said amounts against amount of tax paid on the inward supplies received in terms of the provisions of this Act and Rules made thereunder as specified under section 49. It is a civil liability fasted on the person being a registered person holding the amounts belonging to the government. At no point of time the right to claim is denied if the claims are as per the provisions of this Act and Rules made thereunder.

4. Section 16/4) is existed from the date of enactment of the Act, i.e., from 1st July 2017. Selectively picking and choosing the provisions of the Act or relevant Sections/Rules. The very Chapter No. V INPUT TAX CREDIT as enacted by the Parliament contains 6 Sections L.e., S.16 to S.21. The very definition of section 16 is Eligibility and conditions for taking input tax credit. Section17 Apportionment of credit and blocked credits, Section.18-.Availability of credit in special circumstances. Section.19. Taking input tax credit in respect of inputs and capital goods sent for Job work. 20. Manner of distribution of credit by Input. Service Dist briutor and Section21. Manner of recovery of credit distributed in excess. This amply proves that the input tax credit as enacted by the Parliament is conditional Right and not an absolutely vested right.

5. The provisions of Section16(2) which includes a non-obstante clause (2) “Notwithstanding anything contained in this section” is to be read as even though the other provisions of Section 16 were satisfied it is mandatory to satisfy the Section16(2). The reading of the provisions as the provisions of Section 16(2) is satisfied no other conditions needs to be satisfied is totally wrong and the same is not the intent of legislature. The Person needs to satisfy other underlying provisions/conditions stipulated under Sections 16, 17, 18, 19, 20 & 21 in addition to satisfying the provisions of S 16(2).

6. The provisions of Section 16(4) clearly specifies input tax credit in respect of any invoice or debit notes in relation to any tax period is allowed beyond the due date of filing the returns for the September of next financial year or furnishing of relevant annual returns. The input tax credits are lying in the person’s account but to utilise them the person needs to file the returns under S.39 i.e., form GSTR-3B within stipulated time to claim without which the same cannot be reflected into his Electronic Credit Ledger. The same is espoused in the case of UOI v. Bharti Airtel Limited CIVIL APPEAL NO. OF 2021 (ARISING OUT OF S.L.P. (C) NO. 8654 OF 2020) dated October 28, 2021. Such being the case the input tax credit claimed beyond the relevant dates are not admissible. The provisions as under:

A registered person shall not be entitled to take input tax credit in respect of any invoice or debit note for supply of goods or services or both after the due date of furnishing of the return under section 39 for the month of September following the end of financial year to which such invoice or (******141 debit note pertains or furnishing of the relevant annual return, whichever is earlier.

7. The acknowledgement of the returns in form GSTR-3B with late fee and taxes any, if thereon also a subject matter of the said provisions and scrutiny of returns under Section 61 and proceedings u/s 73/74 of the Act on later date for which the undersigned is duly empowered with.

8. The Judgment of Hon’ble Supreme Court in the case of State of Uttar Pradesh & ors vs. M/ s Kay Pan Fragrance Pvt. Ltd. in Civil Appeal No.8942/2019 & 8944/2019 is relevant at this juncture and relevant paras of the judgement are reproduced as under:

“the orders passed by the High Court which are contrary to the stated provisions shall not be given effect to by the authorities. Instead, the authorities shall process the claims of the concerned assessee afresh as per the express stipulations in Section 67 of the Act read with the relevant rules in that regard In terms of this order, the competent authority shall call upon every assessee to complete the formality strictly as per the requirements of the stated provisions disregarding the order passed by the High Court in his case, if the same deviates from the statutory compliances. “.

Hon’ble Supreme Court also ordered:

“We reiterate that any order passed by the High Court which is contrary to the stated provisions need not be given effect to in respect of all the cases referred in the affidavit by the State Government before this Court and fresh cases which may have been filed or likely to be filed before the High Court in connection with the subject matter of these appeals, by all concerned and are deemed to have been set aside/modified in terms of this order. “

9. The liability of tax being absolute and therefore the interest proposed to be levied under section 50(1) by virtue of which the tax liability was reduced which is against the inherent provisions the Act and Rules made thereunder.

10. The proceedings carried under section 73 and are based on the data furnished by the person and therefore, the penalty is applicable under the provisions of Section 122(2) payable under the terms and timelines prescribed under the provisions of section 73(8) & 73(9).

11. Therefore, the demand imposed is in order. The taxpayer has collected the tax and not paid the taxes so collected by furnishing a valid return in time. He has further failed to claim the relevant input tax credit in time as per the provisions of the Act and Rules made thereunder by filing the returns in time and discharge the tax thereon.

CONCLUSION:

In spite of sufficient opportunities extended, taxable person has not discharged the amount of tax so wrongly utilised. In view the above it is abundantly clear that the person has no objections to the said show cause notice proposing to determine the amount of input tax wrongly utilised, amount of interest payable on such wrongful availment of the input tax credit and applicable penalty as provided under section 73 of the Act since the details are gleamed from the returns filed by the person.

Also, the person has no intention to discharge the input tax credit amount claimed and utilised in contravention of section 16(4) of the Act. Therefore, the undersigned has no other option but to confirm the propositions made in the show cause notice and to recover the said amounts by fasting a valid demand as provided under the Act. Hence the following order:

I the undersigned proper officer by virtue of the powers vested in me hereby determines the amount of tax as provide under provisions of section 73 of the Act, amount of Interest as provided under section 50(1) of the Act and amount of Penalty as provided under section 122 of the Act as proposed and detailed below. The above Tax/Penalty/Interest payable by the Taxable Person required to be paid as self-assessed tax/interest/penalty as per section 50 of Central /State Goods and Service Tax Act-2017, therefore by virtue of Section 78 Central /State Goods and Service Tax Act-2017, in the interest of the Government revenue, undersigned is hereby directing the Taxable Person to pay the above tax/interest/penalty within 30-days of date of receipt of this order failing which recovery action under section 79 of the Central /State Goods and Service Tax Act-2017 shall be initiated against the Taxable Person to recover the outstanding dues.

Note: Further Interest will be Calculated till the date of payment of tax.

Since the taxpayer has not discharged the proposed tax, interest and penalty, the undersigned is here by concluding the order under section 73 (9) of the CGST/SGST Act 2017 for the period Apr-2019 to Mar-20 in Form of DRC-07 by creating a valid demand under the Act.

Commercial Tax Officer

Local GST Office-100, Bangalore.