The National Financial Reporting Authority (NFRA) has issued guidance under its Auditor–Audit Committee Interaction Series focusing on the audit of provisions, contingent liabilities, and contingent assets in line with Ind AS 37 and relevant auditing standards. The document emphasizes the importance of robust communication between auditors and those charged with governance, particularly audit committees, to enhance audit quality and financial reporting reliability. It highlights that provisions must be recognized only when a present obligation exists, with probable outflow and reliable estimation, while contingent liabilities are disclosed but not recognized. The guidance also stresses the role of auditor judgment, evaluation of management estimates, use of external confirmations, and assessment of risks such as litigation, environmental liabilities, and restructuring obligations. Additionally, it underlines compliance with Companies Act, 2013 and SEBI LODR requirements, encouraging detailed disclosures and scrutiny of assumptions to prevent management bias and ensure transparency.

National Financial Reporting Authority

Auditor= Audit Committee* Interactions Series 5 dealing with Audit of Provisions Contingent Liabilities and Contingent Assets: Ind AS 37, SA 540 and SA 501 etc.

*NFRA does not set standards and codes for Corporate Governance, Board of Directors and Audit Committees.

Publish Date : March 31, 2026

Introduction

1. In course of NFRA’s enforcement, review and monitoring activities, auditor’s communication with Those Charged with Governance (TCWG) (including the Audit Committees) has been variously highlighted. A need has been felt through these activities towards reinforcing the ways and means of communication between the Statutory Auditors and the Audit Committees in particular drawing upon the requirements in the Companies Act 2013 (CA 2013), the two relevant Standards on Auditing (SA 260 (R)1 and 2652), other related SAs and the Standard on Quality Control (SQC 1).

2. Therefore, in accordance with NFRA’s obligations to suggest measures for improvement in overall audit quality and to promote awareness and significance of accounting and auditing standards, auditor’s responsibilities, audit quality, and keeping in view NFRA’s objectives of protecting public interest and investor protection, NFRA had commenced with this series of Auditor-Audit Committee Interactions, which are being issued on significant areas of accounting and auditing, from time to time.

3. Preparation and Presentation (including Disclosures) of financial statements require management to make estimates and judgements in the recognition/measurement of assets, liabilities, income and expenses.

Such areas could be impairment of nonfinancial assets, expected credit loss (ECL) for financial assets, provisions for litigations & claims, contingent liabilities, recognition/measurement of deferred tax assets and so on. Some of these could be complex requiring special attention by the Preparers, Audit Committee and the Auditors.

4. This series of Audit Committee-Auditor Interactions draws the attention of the auditors to the potential questions the Audit Committees/Board of Directors may ask them in respect of their audit of provisions, contingent liabilities and contingent assets (Ind AS 37).3

What do Financial Reporting Standards require?

5. The objective of Ind AS 37 is to ensure that appropriate recognition criteria and measurement bases are applied to provisions, contingent liabilities, and contingent assets, and that sufficient information is disclosed in the notes so that users can understand their nature, timing, and amount. Ind AS 37 provides principles for determining when a provision should be recognized, how it should be measured, and what disclosures are required, establishing a framework for transparent and reliable accounting that ensures financial statements accurately reflect obligations and potential risks.

6. An important aspect to note here is that the scope of Ind AS 37 includes liability arising from ‘constructive obligations’ as well as those arising from `legal or contractual obligations’.

7. Ind AS 37 does not apply to items specifically covered by other Ind ASs, disclosure of tax- related contingent liabilities and contingent assets4, However, Ind AS 37 applies to accounting for provisions for onerous contracts arising from contracts with customers5 , obligations arising from certain special transactions/events viz. restructuring of business6, decommissioning, restoration or similar liabilities, participation in decommissioning, restoration & environmental rehabilitation funds8, liabilities for waste management under EU Directive on Waste Electrical & Electronic Equipment9 and Levies other than Income Taxes and penalties for breaches of the law, and certain product liabilities in addition to normal product warranty provisions.

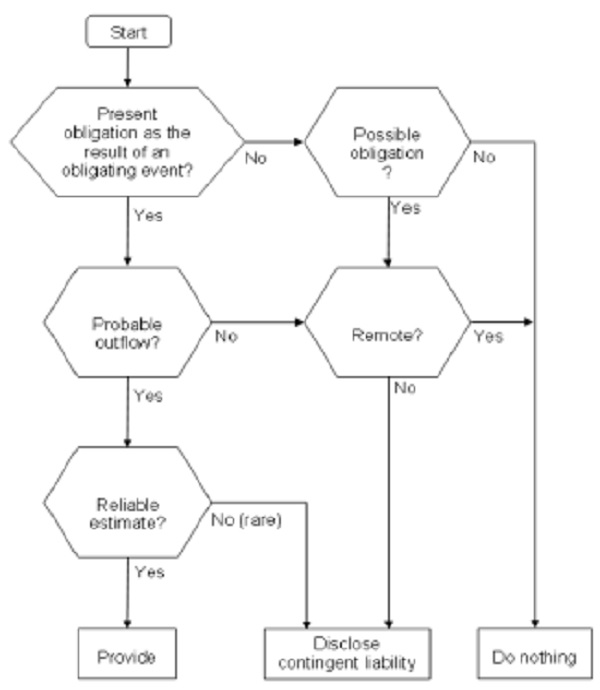

8. A provision is a liability of uncertain timing or amount that arises from a past event and is expected to be settled by an outflow of resources. Provisions should be recognized when there is a present obligation (legal or constructive), it is probable that an outflow of resources will be required to settle the obligation, and a reliable estimate of the amount can be made.

9. An obligating event is a past event that creates a current responsibility for an entity, leaving it with no real option but to settle that obligation. This happens when the duty to settle arises either because it is legally enforceable or because the entity’s own past actions, commitments, or practices have led others to reasonably expect that it will meet the obligation. In essence, such an event makes it unavoidable for the entity to act, either by law or through expectations it has itself created.

10. If it is more likely that no present obligation exists at the end of the reporting period, the entity discloses a contingent liability unless the possibility of an outflow of resources embodying economic benefits is remote.

11. Provisions shall be measured at the best estimate of the expenditure required to settle the present obligation at the end of the reporting period. The best estimate shall consider all available information, including risks and uncertainties. Further, where the provision being measured involves a large population of items, the obligation is estimated by weighing all possible outcomes by their associated probabilities (Expected Value Method).

12. Where the effect of the time value of money is material, the amount of a provision shall be the present value of the expenditures expected to be required to settle the obligation. The discount rate (or rates) shall be a pre-tax rate (or rates) that reflect(s) current market assessments of the time value of money and the risks specific to the liability. The discount rate(s) shall not reflect risks for which future cash flow estimates have been adjusted.

13. Provisions shall be reviewed at the end of each reporting period and adjusted to reflect the current best estimate. Any changes in the provision shall be recognized as an expense or as a reduction in the provision.

14. A provision is different from other liabilities such as trade payable and accruals because there is uncertainty about the timing or amount of the future expenditure required in settlement.

15. Contingent liabilities are not recognized as provisions but only disclosed. Similarly, Ind AS 37 prohibits recognition of contingent assets and disclosure is permitted only if the inflow of economic benefits is probable. Future operating losses are not recognized howsoever likely those are, but such an expectation may indicate impairment of certain assets.

16. Entity may be entitled for reimbursement from a third party in respect of its obligations. Such reimbursements are treated as separate assets but recognized only when the reimbursement is virtually certain.

17. In case of onerous contract , the least net cost of exiting the contract, which is the lower of the cost of fulfilling it and any compensation or penalties for non-fulfilment, is recognized as a provision. Only direct costs of fulfilling the contract are considered for measuring the provision. An onerous contract is one where the unavoidable costs of fulfilling contractual obligations exceed the economic benefits expected to be received.

18. Contingent liabilities and Contingent assets are assessed continually to ensure that developments are appropriately reflected in the financial statements.

19. To summarize the requirements, the following decision tree can be helpful:

20. Ind AS 37 involves significant accounting estimates and management judgments in recognizing and measuring provisions, contingent liabilities, and contingent assets. Accordingly, certain Standards on Auditing (SAs) such as SA 540, SA 501 and SA 505 provide guidance on auditors’ responsibilities related to accounting estimates.

What do Standards on Auditing (SAs) require?

21. SA 540″ deals with the auditor’s responsibilities regarding accounting estimates and related disclosures in an audit of financial statements. Examples of accounting estimates in Para A6 of SA 540 includes items within the scope of Ind AS 37 such as warranty obligations, financial obligations/costs arising from litigation settlements/judgments.

22. Para 18 of SA 540 states that the auditor shall evaluate, based on the audit evidence, whether the accounting estimates in the financial statements are either reasonable in the context of the applicable financial reporting framework, or are misstated.

23. Para 19 of SA 540 states that the auditor shall obtain sufficient appropriate audit evidence about whether the disclosures in the financial statements related to accounting estimates are in accordance with the requirements of the applicable financial reporting framework.

24. Para 20 of SA 540 states that for accounting estimates that give rise to significant risks, the auditor shall also evaluate the adequacy of the disclosure of their estimation uncertainty in the financial statements in the context of the applicable financial reporting framework.

25. Para 21 of SA 540 states that the auditor shall review the judgments and decisions made by management in the making of accounting estimates to identify whether there are indicators of possible management bias.

26. Para 22 of SA 540 states that the auditor shall obtain written representations from management and, where appropriate, those charged with governance whether they believe significant assumptions used in making accounting estimates are reasonable.

27. SA 501 requires the auditor to seek direct communication with entity’s external legal counsel if the auditor identifies risk of material misstatement regarding litigation etc.12Further, as per SA 50513 obtaining external confirmations can be relevant and useful when auditing provisions and contingent liabilities. External confirmations provide independent evidence that can corroborate management’s assertions about the existence, completeness, and measurement of provisions, especially where estimates involve obligations with counterparties outside the entity or contingent liabilities such as legal claims, guarantees, and disputes.

Consideration of Subsequent Evente

28. The auditors should consider events that occur after the reporting date but before the issuance of the fmancial statements. For example, a subsequent event may provide evidence of existence of a contingent liability14 at the reporting period or need for recognition of a provision may arise15. However, announcement of restructuring after reporting period is a non-adjusting event i.e., do not require provision at reporting date.16

What do Companies Act 2013 (CA 2013) and SEBI (LODR) require from Audit Committee/Board of Directors?

29. As per Section 134(5), Board of Directors (BOD) are required to state in the Directors’ Responsibility Statement in the Board’s Report, that is part of Annual Report, that they had selected such accounting policies and applied them consistently and made judgements and estimates that are reasonable and prudent to give a true and fair view of the state of the affairs of the company.

30. Schedule IV to CA 2013 lays down code for Independent Directors. Clause 4 of Part II of this code requires the Independent Directors to satisfy themselves with the integrity of financial information and that financial controls and the system of risk management are robust and defensible.

31. SEBI LODR’7 specifically mandates Audit Committee’s review of major accounting entries involving estimates based on the exercise of judgment by management. It also explicitly recognizes Audit Committee role in the matters included in the Director’s Responsibility Statement to be included in the Board Report.

Potential Questions the Audit Committee May Pose to Auditors

Fundamental areas and Internal controls

32. Has the auditor evaluated and tested internal control over following critical areas?

♦ Identification of constructive obligations, onerous contracts, restructuring events, contingent obligations due to litigations, liabilities due to special events like participation in overseas jurisdictions attracting waste management liabilities, environmental restoration obligations, etc.

♦ Measurement of best estimate of the expenditure to settle present obligations; Discount rates, estimation of future cash outflows, adjustment for nonperformance risk.

33. Has the auditor considered litigation or other claims as risk of material misstatement or other audit procedures indicate possible material litigation or claims? If yes, did the auditor have direct communication with entity’s external legal counsel? If not, what alternative audit procedures are being performed?

35. What audit procedures are performed to ensure completeness of provision for constructive obligations, and litigations and claims?

36. Has the auditor considered use of Independent Legal Counsel, if there are complex litigations and claims?

37. What is the auditor’s view18 on the entity’s disclosures regarding contingent liabilities, litigation and claims?

Best estimate of cash outflows

38. Is the measurement approach used by the management for estimating and quantifying provisions appropriate i.e., whether statistical methods such as `expected value method’ are used for large population of items say product warranty obligations?

39. Are there cases of single obligation of large impact such as environmental damage, tax avoidance litigation liabilities, etc.? Is the approach used for estimating provision or contingent liability reflects best estimate out of possible range of outcomes?

39. Are there any provisions where the cash outflows are expected over longer period, therefore, time value of money is material? In such cases, how has the auditor ensured the following?

> discount rates are reasonable and appropriate i.e., based on current market assessment of time value of money and capture risks specific to the liability.

> Cash outflows or discount rates consider risks and uncertainties19. There is no double counting of impact of these in estimated cash outflows and discount rates.

> Whether gains from the expected disposal of assets and reimbursements from a third party are excluded?20

Reimbursements

40. In case the company has recognised any asset for reimbursement from any third party, how has the auditor checked that the reimbursement is virtually certain?

Onerous contracts

41. Has the auditor checked whether entity has considered executory contracts also21 in evaluating need for provision for onerous contracts?

42. Has the auditor evaluated need for recognition of impairment loss also on any of entity’s operating assets?

Restructuring

43. Has the auditor performed following procedures to ensure completeness and correctness of recognition of restructuring provision by the entity?

> review of events/contracts such as binding negotiations/agreement with employee unions for Voluntary Retirement Schemes22 leading to restructuring or discontinuation of business operations, change in the ownership or management of the entity or applicability of new laws/regulations imposing binding legal obligations?

> validation of fulfilment of critical recognition criteria such as existence of detailed formal plan of restructuring and it has raised valid expectation of its implementation. A management or board decision before the reporting period alone is not adequate to create constructive obligation of restructuring provision.23

44. Has the auditor ensured that the composition of restructuring provision recognised is as per Ind AS 37 prescriptions given below:

> it includes direct expenditures only,

> it excludes costs like retraining/relocating staff, marketing, investment in new systems, future operating costs and losses. Future operating losses upto the date of restructuring and gains on expected disposal of assets, even if the sale is envisaged as part of the restructuring, are excluded.24

Decommissioning, Restoration and Environmental Rehabilitation Funds (Restoration & Rehabilitation Fund)

45. If the entity is a party to Restoration & Rehabilitation fund, whether the auditor has ensured the following?

> Obligation to pay decommissioning costs and interest in the fund are accounted separately.

> Are the funds where the entity has control or joint control or significant influence over the fund, consolidated as per Ind AS 11025 or accounted using Ind AS 11126 or Ind AS 2827, as the case may be.

> In case the entity has obligation to make additional contributions in the event of bankruptcy of another contributor or decline in value of the investments of the fund, whether need for provision evaluated based on probability of additional liability?

Liabilities for waste management under EU Directive on Waste Electrical & Electronic Equipment (WE&EE Liability)

46. Has the auditor checked whether the entity has incurred any obligation under EU Directive on Waste Electrical and Electronic Equipment? If yes, whether the timing of provision recognition is as prescribed in Appendix B to Ind AS 37 i.e., when the entity reaches a market share as prescribed in national legislations and not when the goods are manufactured or sold.

Extended Producer Responsibility (EPR Liability) under Plastic Waste Management Rules 2016, E-Waste (Management) Rules, 2022, Battery Waste Management Rules, 2022 or similar laws and rules.

47. Has the auditor checked whether the company has incurred any EPR liability and accounted for environmental compensation, if any?

48. Has the auditor verified whether the reasonableness of assumptions used in estimating environmental compensation payable and verified the company’s assertions regarding potential refund of the environmental compensation already paid?

Disclosures

49. Has the auditor verified the adequacy and appropriateness of the disclosures of movement in provision balances, contingent liabilities, contingent assets and interests in restoration and rehabilitation funds? Disclosure exception permitted for cases expected to prejudice the entity in legal dispute is availed only in extremely rare cases.28

50. Has the auditor reviewed movements in provision balances with sufficient professional skepticism to identify any management bias or susceptibility for earnings management?

Has the auditor validated that the contingent assets are disclosed only when the inflow of economic benefits is probable i.e., probability that the event will occur is greater than the probability it will not? Has the auditor verified whether the disclosure is not misleading to indicate the likelihood of income arising?

Acknowledgments

NFRA acknowledges the contributions of subject matter experts Shri D Sundaram, Shri Nawshir Mirza, Shri P R Ramesh and Shri R.Anand, in developing this publication.

Disclaimer: This publication by NFRA Staff is intended purely towards promotion of awareness of auditing and accounting standards and audit quality as part of NFRA’s education, training, seminar and advocacy initiatives. NFRA and the subject matter experts do not accept any responsibility or liability for any loss caused to any person or any entity, howsoever arising from the use of or refraining from the use of the contents of this document. This document is not a policy/standard/recommendation/statement of Executive Body of NFRA, the Authority or the Government and is not issued as a substitute for any obligations of Auditors, Management, TCWG including Audit Committees, as are provided in law, rules, and regulations.

Notes:-

1 SA 260 (Revised), Communication with Those Charged with Governance

2 SA 265, Communicating Deficiencies in Internal Control to Those Charged with Governance and Management

3 Ind AS 37, Provisions, Contingent Liabilities and Contingent Assets

4 Para 88 of Ind AS 12, Income Taxes

5 Para 5(g) & 66-69 of Ind AS 37

6 Para 70-83 of Ind AS 37

7 Appendix A of Ind AS 16, Property, Plant and Equipment

8 Appendix A of Ind AS 37

9 Appendix B of Ind AS 37

1° Appendix C of Ind AS 37

11 SA 540, Auditing Accounting Estimates, Including Fair Value Accounting Estimates, and Related Disclosures

12 Para 10 of SA 501, Audit Evidence-Specific Considerations for Selected items

13 SA 505, External Confirmations

17 SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, Regulation 18 and Schedule II, Part C

18 Para 16, A19 -A20 of SA 260 (Revised)

25 Ind AS 110, Consolidated Financial Statements

26 Ind AS 111, Joint Arrangements

27 Ind AS 28, Investments in Associates and Joint Ventures

28 Para 92 of Ind AS 37