Article explains Key provisions relating to transfer of shares by way of GIFT, Provisions on Transfer of Shares, Procedure for transfer of shares by way of Gift, Documents required to be prepared and Other key provisions relating to the transfer of shares by GIFT.

In general terms, the word transfer means a conveyance of property, especially stocks and shares, from one person to another. And one of the major features of a Company is ‘Free Transferability of shares’ subject to few restrictions on Private Companies prescribed under the Articles of Association of the Company.

Now, Transfer of Shares may be by way of Sale, Mortgage, Pledge, Gift, Death, Succession, Inheritance, Bankruptcy, etc. However, due to vastness of the provisions, I have limited the scope of this paper to Transfer of Shares by way of Gift.

Therefore, this research paper is prepared to investigate the scope of the transfer of shares by way of gift and its related provision.

In this research paper, divides into the following parts:-

1. Key provisions relating to Transfer of Shares by way of Gift

2. Procedure and Provisions on Transfer of Shares

3. Documents required to be prepared

4. Other key related provision

Page Contents

Before initiating the concept of transfer of shares by way of gift in accordance with Indian Laws, we would like to highlight certain key provisions which are directly related to this topic:-

What is a GIFT?

As per the provision of Section 122 of the Transfer of Property Act, 1882 defined “Gift” as —“Gift” is the transfer of certain existing moveable or immoveable property made voluntarily and without consideration, by one person, called the donor, to another, called the donee, and accepted by or on behalf of the donee.

How the transfer of movable property to effected by way of gift?

The provision of Section 123 of the Transfer of Property Act, 1882 prescribe that “For the purpose of making a gift of moveable property, the transfer may be effected either by a registered instrument signed as aforesaid or by delivery.”

What are Shares?

As per the provision of Section 2 (84) of the Companies Act, 2013, “share” means a share in the *share capital of a company and includes stock.

*What is Share Capital?

The word share capital is defined under the provision of Section 43 (1) of the Companies Act, 2013 as ‘The share capital of a company limited by shares shall be of two kinds, namely:—

(a) equity share capital—

(i) with voting rights; or

(ii) with differential rights as to dividend, voting or otherwise in accordance with such rules as may be prescribed; and

(b) preference share capital’

Whether shares are movable property or immovable property?

To determine that shares are movable or immovable, we require to consider the following provisions:-

As per Section 2 (26) of the General Clause Act, 1897 “immovable property” shall include land, benefits to arise out of the land, and things attached to the earth, or permanently fastened to anything attached to the earth.

As per Section 2 (36) of the General Clause Act, 1897 “movable property” shall mean property of every description, except immovable property.

Further, the provision of Section 2(7) of the Sales of Goods Act, 1930 defines the term ‘goods’ as follow:

“goods” means every kind of moveable property other than actionable claims and money; and includes stock and shares, growing crops, grass, and things attached to or forming part of the land which are agreed to be severed before sale or under the contract of sale;

In light of the above-stated provisions, we can conclude as the shares or share capital of the Company are movable property.

Transfer related provision under the Companies Act, 2013

Section 56 of the Companies Act, 2013

As per the provisions of Sub Section (1) of Section 56 of the Companies Act 2013, A company shall not register a transfer of securities of the company, or the interest of a member in the company in the case of a company having no share capital, other than the transfer between persons both of whose names are entered as holders of a beneficial interest in the records of a depository, unless a proper instrument of transfer, in such form as may be prescribed, duly stamped, dated and executed by or on behalf of the transferor and the transferee and specifying the name, address and occupation, if any, of the transferee has been delivered to the company by the transferor or the transferee within a period of sixty days from the date of execution, along with the certificate relating to the securities, or if no such certificate is in existence, along with the letter of allotment of securities:

Provided that where the instrument of transfer has been lost or the instrument of transfer has not been delivered within the prescribed period, the company may register the transfer on such terms as to indemnity as the Board may think fit.

As per the provisions of Sub Section (4) of Section 56 of the Companies Act 2013, Every company shall, unless prohibited by any provision of law or any order of Court, Tribunal or other authority, deliver the certificates of all securities transferred —

- within a period of one month from the date of receipt by the company of the instrument of transfer under sub-section (1) or, as the case may be, of the intimation of transmission under sub-section (2), in the case of a transfer or transmission of securities;

Rule 11 of the Companies (Share Captial and Debentures) Rules, 2014

- An instrument of transfer of securities held in physical form shall be in Form SH.4 and every instrument of transfer with the date of its execution specified thereon shall be delivered to the company within sixty days from the date of such execution.

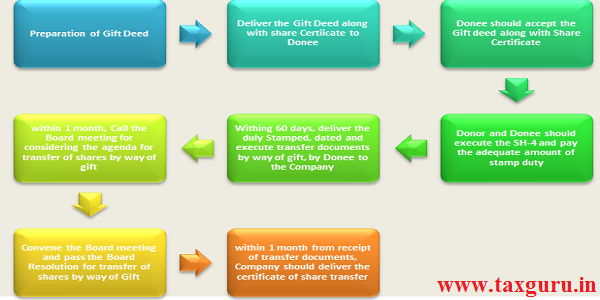

1. Preparation of Gift Deed for transfer of Equity share or Preference Shares;

2. Delivery of Gift Deed along with share certificate by Donor in favour of Donee;

3. Gift Deed along with share certificate should be accepted by or on behalf of Donee;

4. Execution of SH-4 and payment of an adequate amount of stamp duty;

5. Delivery of duly Stamped, dated and execute transfer documents by gift, by Donor or Donee to the Company within 60 days from the date of its execution;

6. The company should call the Board meeting, which is required to be convened within a period of 1 month from the receipt of transfer documents by way of Gift;

7. Convene the meeting and pass the Board Resolution for transfer of shares by way of Gift;

8. The company should deliver the certificate of share transfer within one month from the receipt by the Company of the transfer documents by gift.

Documents required to be prepared

- Gift deed;

- Hand over the position of Share Certificate of the Company;

- Execution of SH-4;

- Board Resolution.

Stamp Duty

What is the applicable stamp duty on transfer of shares?

Companies Act, 2013 requires that where share transfer form is delivered to the Board it should be duly stamped, with adequate value, and dated and cancelled as per section12 of the Indian Stamp Act. Generally, the transferee is responsible for the payment of the stamp duty.

Being the transfer of Shares are subject to the central Stamp duty, accordingly, as per the provision of Article 62 (a), Schedule I of Indian Stamp Act, 1899, the transferee is required to pay stamp duty at the rate of Rs 0.25 for every Rs 100 of the value of the share. Special adhesive stamps bearing the word “share transfer” shall be used for stamping for share transfers.

How to determine the valuation of shares to affix stamps on the transfer deed happens?

In the case of listed companies, it is very easy to find out the price of the shares from the stock exchanges. However, in case of private companies, the value of the shares are difficult to obtain, in such cases, the value of the shares to determine the stamp duty, will be taken based on the average market value of the shares at the time of transfer or the agreed price between the seller and the buyer, whichever is higher. However, generally, the Articles of a private company might contain provisions which provide that the shares must be sold at a fair price determined by the directors or the company’s auditors.

DISCLAIMER: The article is based on the relevant provisions and as per the information existing at the time of the preparation. In no event, I shall be liable for any direct and indirect result from this article. This is only a knowledge-sharing initiative.

The author – CS Mohit Singhal can be reached through csmohitsinghal@gmail.com or 9650066558 or 011-40112793.

Author Bio

Is SEBI approval is necessary to transfer shares by a promoter to another promoter if the same is more than 5% of total equity.

I have gifted shares of 4lacs Rs to my sister. How much stamp duty I have to paid? What amount of stamp paper require? Section of stamp paper of gift under stamp act? Transferor is liable to pay capital gain?

If I gift shares to my daughter ,what sell price will be considered for computing capital gain in my return

What is the procedure when shares are held in demat account. Filing of Delivery Instruction slip is enough? How to make payment for stamp duty ? IS the transfer of multiple companies done instantly or each company takes it time

Can a gift deed be made to confirm to a recent already completed gift transaction

In a pvt. Ltd company gift of shares is possible one share holder to another. In all share holders company is family hold co. any restrictions like blood relations etc.?

If i gift shares worth Rs 150000/ to my spouse, the gift deed for the same, required notary?

Since transfer of physical shares of unlisted public company (w.e.f 2nd October 2018) and listed public company (w.e.f 1st April 2019) has been restricted by law, transfer by way of gift will also not be allowed for shares held physically right ?

At 306 price band shares are allotted to my account present it was trading at 455 price if I gift all shares to my friend means at what price he will get that shares either 306 or present trading value.

Thank you very much for your help sir

How much stamp duty shall be paid for executing gift deed?

0.25 % of amount as duty.

Is this transaction taxable as LTCG or STCG?

No gain. But when receiver sells then (s)he has to pay LTCG/STCG as per applicable rates.

Hello Sir, please let me know who can help to complete the share transfer with complete guidence?

Dear Mohit Sir,

Article is very useful and informative. Please also guide us about What will be Stamp Duty on Gift Deed executed for Gift of shares ?

I read your atricle to find it useful although it does not talks about what if i wish to transfer the share or change the name from joint holding to 1st name holding only. will it be considred transfer and how to do. option 2- transfer/gift to son. Thanks in advance for the reply to both options above.

This is really an informative article for us

is there stamp duty payable on gift of shares in a private limited company?

very informative, thanks

Thank You Mohit. This article is of great help on such a vulnerable topic.