In this article, we are going to cover the following aspects related to Inquiry and Inspections conducted under Section 206 to 209 of the Companies Act, 2013. Article explains Scope of Inquiry and Inspection, Trigger Point of Inquiry and Inspection, Persons authorized for Inquiry and Inspection, Power of registrars to call Information in Inquiry, Power of Registrar’s for Inspection, Power of Civil Court enjoyed by Registrar and Inspector, Obligations of Company and its officers, Search and Seizure of Books and Paper, Returning of books seized by Registrar and Inspector, Report on Inquiry or Inspection, Disqualification of Director, Limitation for filing a complaint and Penalty for default and Compounding of Offence.

Page Contents

- 1. Introduction

- 2. Inquiry and Inspection

- 3. Scope of Inquiry and Inspection

- 4. Trigger Point of Inquiry and Inspection

- 5. Persons authorized for Inquiry and Inspection

- 6. Power of registrars in Inquiry

- 7. Power of Registrar’s for Inspection

- 8. Power of Civil Court enjoyed by Registrar and Inspector

- 9. Obligations of Company and its officers

- 10. Search and Seizure of Books and Paper

- 11. Returning of books seized by Registrar and Inspector

- 12. Report on Inquiry or Inspection

- 13. Disqualification of Director

- 14. Limitation for filing a complaint

- 15. Penalty for default

- 16. Compounding of Offence

1. Introduction

The provisions relating to “inspection, inquiry and investigation” have been incorporated in the Companies Act 2013 at one place nder chapter XIV which cover section 206 to 229 of the Companies Act 2013. this provision can be grouped under the following four parts:-

- Part A covers inspection and inquiry (section 206 to 209 of the Companies Act 2013);

- Part B relates to the investigation (section 210, 213 and 216);

- Part C relates to serious fraud investigation office (section 211 and 212 of the companies at 2013);

- Part D relates to general provisions covering inspection inquiry and investigations (sections 214 215 and 217 to 229 of the Companies Act, 2013.

Under this article, we’re going to cover part A relating to inspection and inquiry, as described above. The scheme of chapter XIV of the Companies Act 2013, relating to Part A, can be summarised as follow:-

- Section 206 of the Companies Act, 2013 empowers the registrar to call any further information or explanation or any further document relating to the company by written notice. However, the registrar has to record the reason for seeking any such information or explanation or any further document relating to the company.

- Upon receipt of the notice, the company and its officers shall be obligated to furnish all such information or explanation or any further documents relating to the company as required in the notice, including the officers in past.

- The Central Government is also empowered to direct inspection by an inspector appointed for this purpose or authorized any statutory authority, by general or special order, to carry out the inspections of books of a company or any class of companies.

- Severe penalties have been provided for disobedience of the order of the registrar and inspector under section 207 of the Companies Act 2013, who have been granted powers of Civil Code under Civil Procedure Code.

- Search and seizure can be carried out after obtaining an order from the special court. The registrar can retain the books and paper seized for 180 days. However, the registrar can call the books and papers for a further period of 180 days.

- Power under section 209 of the Companies Act, 2013 are not accessible by ROC in relation to body corporates other than companies unless notified by the central government.

- Registrar or inspector shall submit a report in writing to the C.G. along with document and recommendation for further investigation into the affairs is necessary giving his reasons in support.

2. Inquiry and Inspection

In general terms the term “inquiry” means ‘an act of asking for information’ and “inspection” means ‘carefully examination or scrutiny’. Similarly, the Companies Act, 2013

3. Scope of Inquiry and Inspection

The provisions related to Inquiry and Inspection is equally applicable to all companies irrespective of whether the Company is a Public Company, Private Company, Small Company, One Person Company (OPC), Government Company or Foreign Company.

4. Trigger Point of Inquiry and Inspection

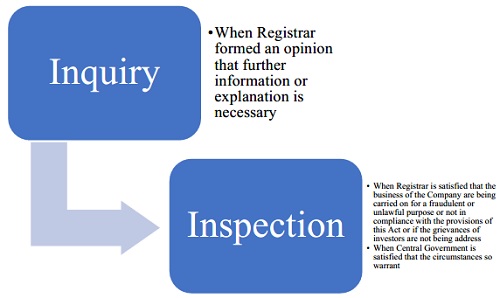

The trigger point for any Inquiry is the opinion formed or made by the registrar after scrutiny of any document filed by a company or on the basis of any other information received by him and accordingly the registrar must be of the opinion that further information or explanation is necessary.

The trigger point for any Inspection is:-

- the opinion formed or made by the registrar after an inquiry conducted that the business of a company is being carried on for a fraudulent or unlawful purpose or not in compliance with the provisions of this Act or if the grievances of investors are not being addressed; or

- When Central Government is satisfied that the circumstances so warrant.

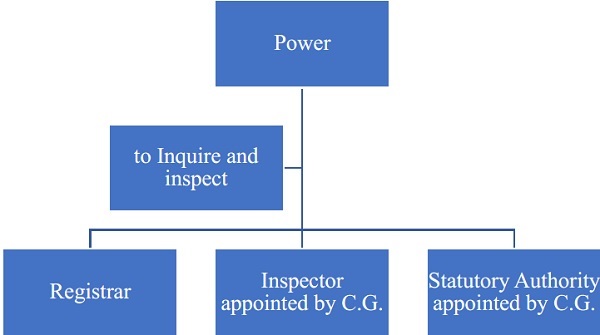

In accordance with the provision of Sub-section (1) (4), (5) and (6) of the Companies Act, 2013, the

following persons are authorized for Inquiry and Inspection:-

1. Registrar; or

2. Inspector appointed by Central Government; or

3. Statutory Authority appointed by Central Government.

6. Power of registrars in Inquiry

Once the trigger point for an inquiry was made, the registrar may issue a written notice requiring the company to furnish in writing such information or explanation or to produce such documents within such reasonable time as specified in the said written notice.

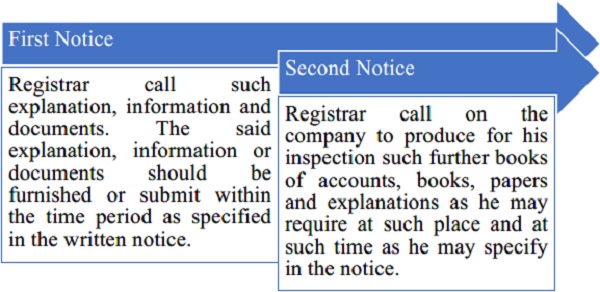

- First Notice: It is issued under the provision of Sub-section (1) of Section 206 of the Companies Act, 2013. This provision empowers the registrar, on forming his opinion, that further information or explanation or documents need to be called for, he may a written notice call such explanation, information and documents. The said explanation, information or documents should be furnished or submitted within the time period as specified in the written notice.

- Second Notice: It is issued under the provision of Sub-section (3) of Section 206 of the Companies Act, 2013. This provision hit or second notice is issued under the following circumstances, where the registrar may, by another written notice, call on the company to produce for his inspection such further books of accounts, books, papers and explanations as he may require at such place and at such time as he may specify in the notice:-

- If no information or explanation is furnished to the Registrar within the time specified under first notice; or

- if the Registrar on an examination of the documents furnished is of the opinion that the information or explanation furnished is inadequate; or

- if the Registrar is satisfied on a scrutiny of the documents furnished that an unsatisfactory state of affairs exists in the company and does not disclose a full and fair statement of the information required.

The power of the registrar has been amplified not only to seek information but even to direct the production of books and records.

However, before issuing any second notice, the registrar shall record his reasons in writing for issuing such notice.

Further, the registrar or inspector, u/s 207(2) of the Companies Act, 2013, have been given all due powers to conduct inquiry and inspection u/s 206 of the Companies Act, 2013 can:-

1. make or cause to be made copies of books of account and other books and papers; or

2. place or cause to be placed any marks of identification in such books in token of the inspection haven made.

7. Power of Registrar’s for Inspection

Once the trigger point for an inquiry was made, the registrar may after informing the company of the allegations made against it by written order, call on the company to furnish in writing any information or explanation on matters specified in the order within such time as he may specify therein and carry out such inquiry as he deems fit after providing the company with a reasonable opportunity of being heard.

Further, the registrar or inspector, u/s 207(2) of the Companies Act, 2013, have been given all due powers to conduct inquiry and inspection u/s 206 of the Companies Act, 2013 can:-

1. make or cause to be made copies of books of account and other books and papers; or

2. place or cause to be placed any marks of identification in such books in token of the inspection haven made.

8. Power of Civil Court enjoyed by Registrar and Inspector

Power of Civil Court is vested to Registrar and Inspector of Civil court are lies with the non-obstante section as its starts with “Notwithstanding anything contained in any other law for the time being in force or in any contract to the contrary”. The Registrar or inspector shall have all the powers as are vested in a civil court under the Code of Civil Procedure, 1908, while trying a suit in respect of the following matters, namely:-

a) the discovery and production of books of account and other documents, at such place and time as may be specified by such Registrar or inspector making the inspection or inquiry;

b) summoning and enforcing the attendance of persons and examining them on oath; and

c) inspection of any books, registers and other documents of the company at any place.

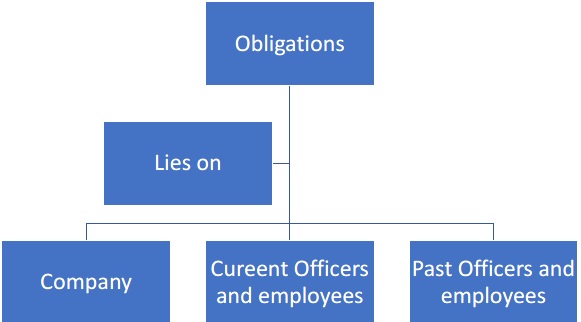

9. Obligations of Company and its officers

The provision of Sub-section (2) of Section 206 of the Companies Act, 2013 makes it obligatory on part of the Company and its officers (including past Officers) to furnish information or explanation as mentioned in the notice issued by the registrar within the time stipulated in the notice and to the best of their knowledge and power.

Further, the provision of Sub-Section (1) of Section 207 of the Companies Act, 2013 imposes an obligation on every director, officer or other employees of the company to produce all such documents to the Registrar or inspector and furnish him with such statements, information or explanations in such form as the Registrar or inspector may require and shall render all assistance to the Registrar or inspector in connection with such inspection.

10. Search and Seizure of Books and Paper

The provision of Section 209(1) of CA, 2013 provides the power to search and seizure of Books and Paper of a company or relating to the Key Managerial Personnel or any director or auditor or practicing Company secretary, if the Company does not have CS in employment.

As per Section 209(1), where, upon information in his possession or otherwise, the Registrar or inspector has reasonable ground to believe that the books and papers of a company, or relating to the key managerial personnel or any director or auditor or company secretary in practice if the company has not appointed a company secretary, are likely to be destroyed, mutilated, altered, falsified or secreted, he may, after obtaining an order from the Special Court for the seizure of such books and papers,—

(a) enter, with such assistance as may be required, and search, the place or places where such books or papers are kept; and

(b) seize such books and papers as he considers necessary after allowing the company to take copies of, or extracts from, such books or papers at its cost.

It is pertinent to note that an order from the special court is necessary for any search and seizure of books and papers by the Registrar or Inspector.

The provisions of the Code of Criminal Procedure, 1973 relating to searches or seizures shall apply, mutatis mutandis, to every search and seizure made U/s 207.

11. Returning of books seized by Registrar and Inspector

The registrar or inspector shall return the books and paper seized U/ss (1) of Section 2019 of CA, 2013 as soon as may be and in any case not later than 180 days after such seizure, to the company from whose custody or power such books or papers were seized.

However, the registrar or inspector may call for the books and papers for a further period of 180 days by an order in writing if they are needed again.

Further, the Registrar or inspector may take copies of, or extracts from them or place identification marks on them or any part thereof or deal with the same in such other manner as he considers necessary.

12. Report on Inquiry or Inspection

After the inspection of the books of accounts or an inquiry U/s 206 of CA, 2013 and other books and papers of the Company U/s 207 of CA, 2013 has been completed, the registrar or inspector shall submit a report in writing to the Central Government together with the following:-

1. Relevant documents to be attached:- The report shall be submitted along with relevant documents, if any.

2. Report may contain recommendation:- Inspection report may also include a recommendation that further investigation into the affairs of the Company is necessary or not. However, reasons in support of such recommendation shall have to be given by the registrar or inspector in his report. It may be essential to note that this report may form the basis for an investigation to be ordered by Central Government under section 210 or 212 of the CA, 2013 by the SFIO. Therefore, the report to be submitted by Inspector or Registrar is an important document containing a recommendation for further investigation duly setting out the reasons for such recommendation.

It is pertinent to note that the registrar or the Central Government doesn’t need to disclose to the company reasons for conducting an inspection, nor is it necessary to come to any conclusion regarding the existence of certain circumstances as is necessary before ordering an investigation into the affairs of a company. In case a recommendation is made for further investigation, the Central Government may look into the recommendations and take an appropriate decision.

13. Disqualification of Director

If a director or an officer of the company has been convicted of an offence under the provision of section 207 of the Companies Act, 2013, the director or the officer shall, on and from the date on which he is so convicted, be deemed to have vacated his office as such and on such vacation of office, shall be disqualified from holding any office in any company.

14. Limitation for filing a complaint

The limitation for filing a complaint begins to run when the registrar gets knowledge of the offence on inspection of the company’s records. The receipt of the report by the registrar operates as the date of knowledge of the registrar. Complaint filed within six months from that date was held to be within time. (Registrar of Companies v. Fairgrowth Agencies Ltd., (2006) 133 Com Cases 314 (Karn).

The offence is not a continuing one and is deemed to be committed on a particular date. Limitation begins to run on that date. A prosecution launched more than one year after the date of the offence of the offence is barred by limitation. State v. S. Seshamal Pandia, (1986) 60 Com Cases 889 (Mad).

15. Penalty for default

If a Company is failed to submit furnish any information or explanation or produce any document required under the provision of Section 206 of the Companies Act, 2013, the Company and every officer of the Company (who is in default) shall be punishable with a fine which may extend to one lakh rupees and in the case of a continuing failure, with an additional fine which may extend to five hundred rupees for every day after the first during which the failure continues.

However, where the business of a company has been or is being carried on for a fraudulent or unlawful purpose, every officer of the company who is in default shall be punishable for fraud in the manner as provided in section 447.

Further, if any director or officer of the company disobeys the direction issued by the Registrar or the inspector under the provision of section 207 of the Companies Act, 2013, the director or the officer shall be punishable with imprisonment which may extend to one year and with fine which shall not be less than twenty-five thousand rupees but which may extend to one lakh rupees.

16. Compounding of Offence

As the offence made under section 206 of the Companies Act, 2013 is punishable only with a fine. Therefore, the offence would be compoundable U/s 441 of the Companies Act, 2013. However, if any default is made under the provision of Section 207 of the Companies Act, 2013 is not compoundable.

Further, where the officer has defaulted under the provision of Section 447 of the Companies Act, 2013, the said charge is not compoundable.

Author Bio