Illuminating insertion /amendments made in TDS provisions under Income Tax Act, 1961

Recently in Finance Bill, 2020; amendment as well as insertion has been made in various section of Income Tax Act,1961. Some new sections has been inserted under chapter XVII along with amendments in earlier provisions.

Accordingly, from now under section 194A,194C,194H,194I,194J of Income Tax Act,1961; The following words i.e. the monetary limits as specified under clause (a) or clause (b) of section 44AB”, are substituted by the words “one crore rupees in case of business or fifty lakh rupees in case of profession”. Therefore now if we interpret above provision Individual/HUF will be liable to deduct tax at source even in case they are not liable to audit, but they are exceeding above Limit.

This will create puzzling situation in mind because their is also insertion of new section i.e. 194M in union Budget 2019 being effective from 1st Sep,2019; therefore we need to take some examples to understand the combined reading of both the provisions

Illustrations:

Question 1: Mr. R having turnover of 90 lakhs from his business during F.Y.2020-21, and he has received 30 lakhs as professional receipt during said year. He has decided to declare income complying 44AD /44ADA of Income Tax Act, 1961. Various payment has been made by Mr. R and amount of such payment is exceeding limits specified under 194C and 194J. Under which section Mr. R is required to deduct TDS? Whether he will be required to obtain TAN? What if such payment is was in nature of personal payment?

Answer: Firstly, Irrespective of whether TDS is deducted under 194C/194J or 194M it is applicable only when payment has been made to resident, if payment is made to Non-resident the above provision are not applicable and section 195 will come into play. Further, as neither professional receipt nor gross turnover from business is exceeding limits specified in 194C and 194J. Therefore now, as 194C/194J is not applicable we have to deduct TDS if payment are exceeding limit of 194M (i.e. 50 Lakhs) at 5%, irrespective whether payment is in personal nature or for business purpose 194M will be applicable and if 194M is applicable there is relaxation in relation to obtaining TAN. Wording of section 194M is very clear and it says other than those who are required to deduct income-tax as per the provisions of section 194C, section 194H or section 194J; Therefore 194M has its own applicability along with own threshold limit.

Conclusion: In the given case tax will be deducted if payment are exceeding limit as specified in section 194M and assessee will not be required to obtain TAN.

There is one more amendment under section 194J i.e. small change in rate of deduction when payment made is for fees for technical services (not being a professional service) instead of 10% now tax will be deducted at rate of 2% provided payment shall not be for professional service.

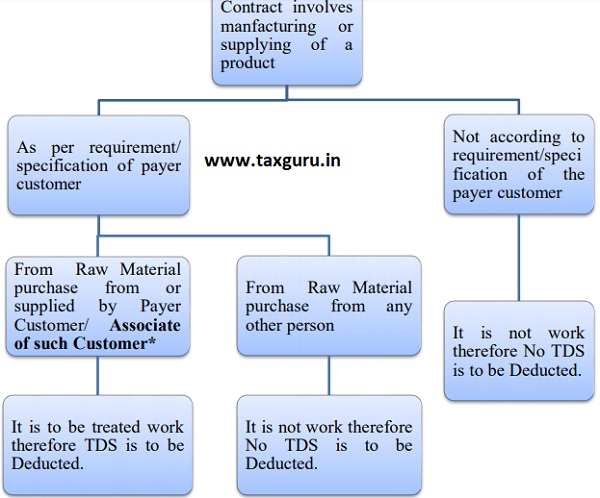

Another amendment is there under section 194C i.e.

Here the word associate of such customer is included meaning thereby being a person placed similarly in relation to such customer as if the person placed in relation to the assessee under the provisions contained in clause (b) of sub-section (2) of section 40A of Income tax Act, 1961. Therefore to understand this and interpret the above provision if we take examples

Illustration 2: Mr. T having turnover of 110 lakhs from his business during the previous year. Mr. T has given contract to Mr. X to Manufacture steel plates in accordance with specification as provided by Mr. T for this Mr. X has to procure Steel from S & Trading Co. which is related party of Mr. T in accordance with provisions contained in clause (b) of sub-section (2) of section 40A of Income tax Act, 1961. Whether Mr. T is liable to deduct TDS when payment is made to Mr. X ?

Answer: In this case under old provision i.e. for F.Y. 2019-20 or before that assessee was not liable to deduct TDS; in case material is procured from related party of payer customer. However from F.Y. 2020-21 due to above amendment assessee will be liable to deduct TDS under section 194C in relation to said contract.

| Section | Applicability | Threshold Limit | Rate of Deduction |

| 194K | Person responsible for paying to resident any income in respect of : (a) units of a Mutual Fund specified under clause (23D) of section 10; or(b) units from the Administrator of the specified undertaking; or(c) units from the specified company. |

Exceeding Rs. 5000/- | 10% |

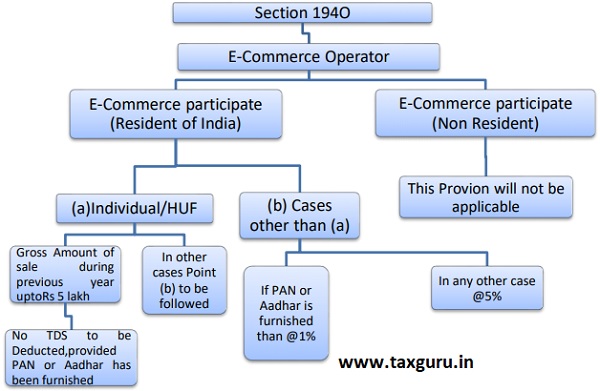

Another section that has been introduced in Finance Bill, 2020; is 194O. The provision is requiring e-commerce operator to deduct TDS @1% at the time of credit of the amount of sale of goods/services, or both to the account of an e-commerce participant or at the time of making payment to an e-Commerce participant (must be Resident of India) by any other mode, whichever is earlier.

E-commerce operator is not required to deduct TDS if the gross amount of sale of goods, services, or both during the previous year does not exceed Rs 5 lakhs (only in case of Resident Individual or HUF) and if the e-Commerce participant has furnished his PAN or Aadhaar. However if PAN or Aadhaar is not furnished TDS is to be deducted at the rate of 5%.

Note:- Views/Opinion expressed in article is limited to author’s knowledge and interpretation; it may be interpreted in different manner.

Author Bio

Dear Vivekji,

In that case as turnover of Mr. T is exceeding the triggering limit as specified in section 194C and from now purchase from related party is also covered, Mr.T will be required to deduct TDS under 194C if payments are more than amount specified in it. Further the transaction that Mr.X is required to collect TCS is independent transaction and is not been seen while determining liability of Mr. T to deduct TDS. I hope your query is resolved.

Note :- Provision are Interpreted here under after amendment, i.e. for F.Y. 2020-21 to thebest of author’s knowledge. Further this doesn’t lead to any financial advise

Please help to Answer after change in below illustration.

llustration 2: Mr. T having turnover of 110 lakhs from his business during the previous year. Mr. T has given contract to Mr. X to Manufacture IMFL (Indian Made Foreign Liquor) in accordance with specification as provided by Mr. T for this Mr. X has to procure Steel from S & Trading Co and R & Trading Co. which are related party of Mr. T in accordance with provisions contained in clause (b) of sub-section (2) of section 40A of Income tax Act, 1961. X is Charging TCS of final Product on sale to Mr T. Whether Mr. T is liable to deduct TDS when payment is made to Mr. X ?

Qurey for Illustration 2. I am changing question.

Mr. T having turnover of 110 lakhs from his business during the previous year. Mr. T has given contract to Mr. X to Manufacture IMFL (Indian Made Forign Liquor) in accordance with specification as provided by Mr. T for this Mr. X has to procure packging Material and Raw Material from S & Trading Co. and R & Trading which are related party of Mr. T in accordance with provisions contained in clause (b) of sub-section (2) of section 40A of Income tax Act, 1961. X is charging TCS on final product at the time of sales to Mr T. Whether Mr. T is liable to deduct TDS when payment is made to Mr. X ?

https://taxguru.in/income-tax/demystifying-amendments-related-residential-status-individual.html

#Amendment in Residential Status

A Good article, the author has tried to cover each and every corner of amendment of TDS. Actually chapter TDS it self is very tedious.