Article Explains Basic Definition related to Apportionment of Credit and Blocked Credit under GST, Section 17(1) & 17(3) of CGST Act,2017, Section 17 (2) of CGST Act,2017 Read With Rule 42 and 43 of CGST Rules,2017, Section 17(4) of CGST Act,2017 Read With Rule 38 of CGST Rules,2017 and Section 17(5) of CGST Act,2017 (Block Credit).

Page Contents

Definition of ‘Capital goods’, ‘Input’, ‘Input Service’ & ‘Input Tax’.

- Sec.2 (19) “Capital Goods” means goods, the value of which is capitalized in the Books of Account of the person claiming the input tax credit and which are used or intended to be used in the course of furtherance of business.

- Sec.2 (59) “Input” means Goods other capital goods used or intended to be used by a supplier in course of furtherance of business.

- Sec.2 (60) “Input Service” means any service used or intended to be used by a supplier in the course of furtherance of business.

- Sec.2 (62) Input tax” in relation to a registered person, means Central tax, State tax, integrated tax, Union Territory Tax charged on supply of Goods or Services or both to him and includes IGST on imports, tax paid under reverse charge but does not include Tax paid under Composition Scheme.

(Will connect this under section 17(5) of CGST Act, 2017.)

Section 17- Apportionment of Credit and Blocked Credit under GST

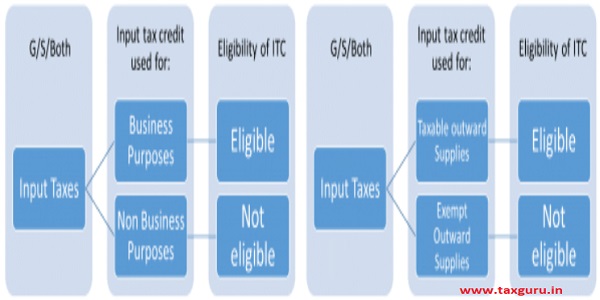

I. Input Tax Credit restricted to supplies for business purposes

Section 17(1) says that where the goods and/or services are used by the registered taxable person partly for the purpose of any business and partly for other purposes, the amount of credit shall be restricted to so much of the input tax as is attributable to the purposes of his business and remaining will not be available.

II. Section 17(3) determines only for this Chapter

Exempt supply (For the Purpose of This Chapter it Includes)

| Nil Rated Supply, Non Taxable supply, Wholly Exempted Supply | Transaction in security (1% of Transaction Value) | Stamp Duty Value on Sale of Land and Sale of Building (Subject to clause (b) of Paragraph 5 of Schedule II) | Supply Effected by Supplier on Which Tax is Payable on Reverse Charge Basis |

Further it has been clarified that it will not include the consideration represented in form of interest on deposit loans or advances and Expense representing freight of Goods transported from India to the place outside India.

Taxable Supply: – includes Zero Rated Supply as determined under section 16 of IGST Act, 2017.

III. Input Tax Credit restricted to taxable supplies

Section 17(2) says that where the goods and/or services are Used by the registered taxable person partly for effecting Taxable supplies including zero-rated supplies under this Act Or under the IGST Act, 2016 and partly for effecting exempt Supplies under the said Acts, the amount of credit shall be Restricted to so much of the input tax as is attributable to the said taxable supplies including zero-rated supplies.

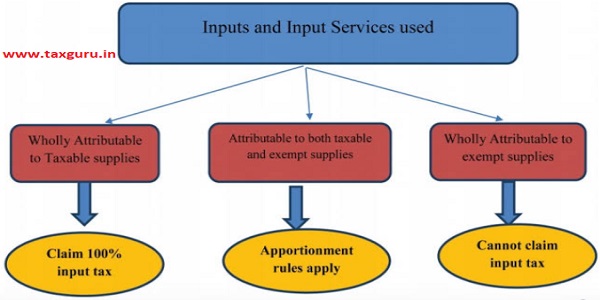

Before Moving Further Let’s Understand Rule 42 (Distributing Input Tax Credit Commonly used Input and Input Service) and Rule 43 for (Distributing Input Tax Credit for Commonly used Capital Goods)

Rule 42 of CGST Rules, 2017:- Manner of Determination of Input Tax Credit in respect of Inputs or Input Services Used Commonly for Effect Taxable as Well as Exempt Supply/ Non Business Supply and Reversal thereof will be as follows:

(a) The total input tax involved on inputs and input services in a tax period, be denoted as ‘T’;

(b) The amount of input tax, out of ‘T’, attributable to inputs and input services intended to be used exclusively for the purposes other than business, be denoted as ‘T1’;

(c) the amount of input tax, out of ‘T’, attributable to inputs and input services intended to be used exclusively for effecting exempt supplies, be denoted as ‘T2’;

(d) The amount of input tax, out of ‘T’, in respect of inputs and input services on which credit is not available under sub-section (5) of section 17, be denoted as ‘T3’;

(e) The amount of input tax credit credited to the electronic credit ledger of registered person, be denoted as ‘C1’ and calculated as

C1 = T- (T1+T2+T3);

(f) The amount of input tax credit attributable to inputs and input services intended to be used exclusively for effecting supplies other than exempted but including zero rated supplies, be denoted as ‘T4’;

(g) Input tax credit left after attribution of input tax credit under clause (f) shall be called common credit, be denoted as ‘C2’ and calculated as C2 = C1- T4;

| Particular | Amount | |

| Total Credit Available for all supplies (T) | XX | |

| Less: | Credit not directly related to business (T1) | XX |

| Less: | Credit related directly to exempt supply (T2) | XX |

| Less: | Credit Inadmissible u/s 17(5) (T3) | XX |

| Credit as per Ledger (A) (C1) | XX | |

| Less: | Credit related directly to Taxable Supplies (T4) | XX |

| Common Credit (B) (C2) | XX | |

| Less: | Credit attributable to exempt supplies (D1 ) | XX |

| Less: | Credit attributable to Non Business Services (D2) | XX |

| Total Credit Available from Common Credits | XX | |

- The amount of input tax credit attributable towards exempt supplies, be denoted as ‘D1’ and calculated as

D1= (E÷F) × C2

Where,

‘E’ is the aggregate value of exempt supplies during the tax period, and

‘F’ is the total turnover in the State of the registered person during the tax period

- Determine ITC related to Non-business purpose (say D2)

D2= C2 * 5%

Tax payable = D1+ D2 = Add to output tax liability

Final reconciliation to be made

Aggregate D1+D2 declared and finally computed on annual turnover before filing of return of September of following year. Make adjustment for Following

- If declared is more than computed, claim credit

- If declared is less than computed, pay tax along with interest.

For Example: –

- Taxable Turnover is Rs. 20,00,000/-

- Exempted Turnover is Rs. 5,00,000/-

- Total available Credit is Rs. 10,00,000/-

- Input Credit attributable to exclusively Non business purpose = Rs. 1,00,000/-

- Input Credit attributable to exclusively exempted business purpose = Rs. 1,50,000/-

- Input Credit attributable to exclusively for Blocked Credit = Rs. 50,000/-

- Input Credit attributable to exclusively for Business purposes = Rs. 5,00,000/-

| Particular | Amount | |

| Total Credit Available for all supplies (T) | 10,00,000/- | |

| Less: | Credit not directly related to business (T1) | (1,00,000) |

| Less: | Credit related directly to exempt supply (T2) | (1,50,000) |

| Less: | Credit Inadmissible u/s 17(5) (T3) | (50,000) |

| Credit as per Ledger (A) (C1) | 7,00,000/- | |

| Less: | Credit related directly to Taxable Supplies (T4) | (5,00,000) |

| Common Credit (B) (C2) | 2,00,000/- | |

| Less: | Credit attributable to exempt supplies (D1 ) #1 | (40,000) |

| Less: | Credit attributable to Non Business Services (D2) #2 |

(10,000) |

| Total Credit Available from Common Credits | 1,50,000/- | |

#1 :- ( 200000*500000/2500000).

#2 Assuming also commonly utilized some inputs for Business as well as Non Business Purpose In that Case Irrespective of Turnover Assessee needs reverse 5% of C2.

ITC Rules on Capital Goods under GST

Rule 43 of CGST Rules, 2017:- Manner of Determination of Input Tax Credit in respect of Capital Goods Commonly Used for effecting Taxable as well as Exempt Supply and Reversal thereof will be as follows:

On first instance, the amount of input tax in respect of capital goods used or intended to be used for effecting outward supplies:

1. Exclusively for non-business purposes or used or intended to be used exclusively for effecting exempt supplies – shall be disallowed.

2. Exclusively for effecting supplies other than exempted supplies but including zero-rated supplies – shall constitute eligible credit.

3. Then, amount of input tax in respect of capital goods not covered under clauses (a) and (b), denoted as ‘A’, shall be credited to the electronic credit ledger and the useful life of such goods shall be taken as Sixty Months from the date of the invoice for such goods.

Total common ‘Tc’ credit shall be Sum of all Common credits.

Provided that where any capital goods earlier covered under clause (1) is subsequently covered under Common Use then the value of ‘A’ arrived at by reducing the input tax at the rate of five percentage points for every quarter or part there of shall be added to the aggregate value ‘Tc’; and will also be Credited to Electronic Credit Ledger along with other Credits.

Provided Further that where any capital goods earlier covered under clause (2) is subsequently covered under Common Use then the value of ‘A’ arrived at by reducing the input tax at the rate of five percentage points for every quarter or part there of shall be added to the aggregate value ‘Tc’.

Step 1: Common credit ‘Tm’ per month would be ‘Tc’/ 60 months

Step 2: the amount of input tax credit at the beginning of a tax period on all common capital goods whose useful life is to be divided by be denoted respective factor and shall be the aggregate with ‘Tm’ and total will be Denoted as ‘Tr’

Step 3: the amount of common credit attributable towards exempted supplies, be denoted as ‘Te’, and calculated as: Te= (E÷ F) x Tr. This Te shall be stated as ineligible credit out of the common-credit.

Where,

- ‘E’ is the aggregate value of exempt supplies, made, during the tax period, and

- ‘F’ is the total turnover of the registered person during the tax period.

Thus, input taxes exclusively used for effecting supplies other than exempted supplies and Balance input taxes out of common credit after deducting ineligible credit out of the common credit, shall be termed as eligible credit with respect to capital goods.

Note:

A)The amount ‘Te’ shall, during every tax period of the useful life of the concerned capital goods, is added to the output tax liability of the person making such claim of credit.

Summarizing this Rule in Table will be As Follows

| Particular | Amount | |

| Total Credit Available for both Exempt & taxable supplies | xxxxx | |

| Less: | Credit not directly related to business | xxxx |

| Less: | Credit related directly to exempt supply | xxxx |

| Less: | Credit Inadmissible u/s 17(5) | xxxx |

| Less: | Credit related directly to Taxable Supplies | xxxx |

| Add: | Amount of Credit (Reduced By Specific %) on Capital Goods Previously Purchased and used for purpose other than Taxable Supply including Zero Rated Supply, being now Commonly Used. | xxxx |

| Amount of Credit (Reduced By Specific %) on Capital Goods Previously Purchased and used for purpose Taxable Supply including Zero Rated Supply, being now Commonly Used.( Not to be Credited to Credit Ledger as Credit is Already Taken). | xxxx | |

| Amount of Common Credit Denoted as ‘Tc’ | xxxx | |

| ‘Tc’ to be Divided By 60 Months to get ‘Tm’ Per Month | xxxx | |

| ‘Tm’ of Current Period to be Aggregated with Opening ‘Tm” to Get ‘Tr’ | xxxx | |

| ‘Te’ = Tr*E/F (To be Added To output Tax liability) | xxxx | |

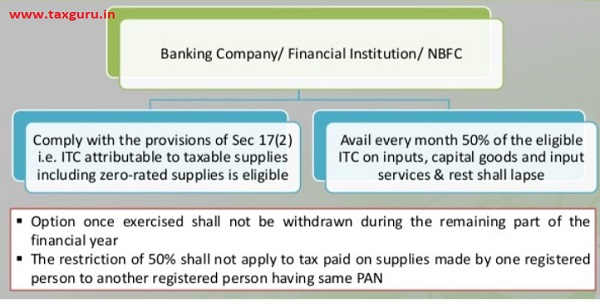

IV. Input Tax Credit – Banking Sector

Section 17(4) read with Rule 38 of CGST Rules says that a banking company or a financial institution including a non-banking financial company, engaged in supplying services by way of accepting deposits, extending loans or advances shall have the option to either comply with the provisions of section 17(2), or avail of, every month, an amount equal to 50% of the eligible input tax credit on inputs, capital goods and Input services in that month; Further Banks will be allowed to take 100% credit of Supply under Same PAN. An explanation to section 17(3) says that the option once exercised shall not be withdrawn during the remaining part of the financial year.

OPTION FOR BANKING COMPABY: SEC 17(4)

Blocked Credit- Section 17(5) under CGST

- (i)Motor vehicles for Transportation of persons having approved seating capacity of not more than 13 persons (including the driver)Amendment; Including Services of general insurance, servicing, repair and maintenance of aforesaid motor vehicles.

However when such motor vehicles are used for following Purpose then ITC on such will be available

i) Further supply of such vehicles or

ii) Transportation of passengers or

iii) Imparting training on driving of such motor vehicles.

iv) Transportation of Goods

- (ii)Vessels and Aircraft; Including Services of general insurance, servicing, repair and maintenance of aforesaid Vessels and Aircraft.

When such Vessels and Aircraft are used for

i) Further supply of such Vessels and Aircraft or

ii) Transportation of passengers or

iii) Imparting training on navigating / flying such vessels / aircraft.

iv) Transportation of goods.

Further ITC would be admissible when Motor vehicle/ Vessel or Aircraft is taken on Lease or on Rent for above said purposes.

E.g.

i) ITC on Trucks Purchased by Company for Transportation of its finished goods is allowed.

ii) ITC on Aircraft Purchased by a Manufacturing Company for its official use of its CEO is blocked.

(iii) The following supply of goods or services or both

- Food and beverages,

- Outdoor catering,

- Beauty treatment,

- Health services,

- Cosmetic and plastic surgery (Not Covered Under Exemption List),

- Leasing,renting or hiring of motor vehicles, vessels or aircraft referred in clause (a) or (aa) except when used for purposes specified therein,

- Lifeinsurance & health insurance,

- Membership of Club, health and fitness center,

- Travelbenefits extended to employees on vacation such as leave or home travel concession (Read with Schedule III Clause 1 and Schedule I Clause 1).

Exceptions, where ITC allowed

Proviso – Provided that the input tax credit in respect of such goods or services or both shall be available where in inward supply of such goods or services or both is used by a registered person for making an outward taxable supply of the same category of goods or services or both or as an element of a taxable composite or mixed supply.

Proviso – Provided that the input tax credit in respect of such goods or services or both shall be available, where it is obligatory for the employer to provide the same to its employees under any law for time being in force.

E.g. Whether Credit can be availed on Inward Supply of outdoor catering to a manufacturing company for celebrating its 25 years of success.

Ans. No Company Cannot Avail ITC. As in the given case, it is not used by the registered person for making outward supply of same category of services & is used for its own company.

E.g. Whether Credit can be availed on Inward Supply of beauty treatment services by a Film Production?

Ans. No as such Inward Supply of beauty treatment services by a Film Production as in the given case, it is not used by the registered person or making outward supply of same category of services & is used for its own company.

- (iv) Works contract services when supplied for construction of an immovable property (other than plant and machinery)

Exception: – Where it is an input service for further supply of works contract service.

- (v)Goods or services or both received by a taxable person for construction of an immovable property (other than plant or machinery) on his own account including when such goods or services or both are used in the course or furtherance of business. The term “construction” includes re-construction, renovation, additions or alterations or repairs, to the extent of capitalization, to the said immovable property;

Further the expression “plant and machinery” means apparatus, equipment, and machinery fixed to earth by foundation or structural support that are used for making outward supply of goods or services or both and includes such foundation and structural supports but excludes— (i) Land, Building or any other Civil structures; (ii) Telecommunication towers; and (iii) Pipelines laid outside the factory premises.

(vi) Goods or services or both received by a non-resident taxable person except on goods imported by him;

(vii) Goods or services or both used for personal consumption Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples;

(viii) It may noted here that under composition scheme the tax cannot be charged by supplier from the recipient and accordingly question ITC availment by recipient does not arise.

(ix) Any tax paid in accordance with the provisions of sections 74 (Tax not / short paid due to fraud etc), 129 (Detention, seizure and release of goods and conveyance in transit) and 130 (confiscation of goods or conveyance and levy of penalty).

Note: – Views/Opinion expressed in article is limited to author’s knowledge and interpretation; it may be interpreted in different manner.

Author details- Name: – Jigar R. Mansatta, Qualification: – Chartered Accountant, Email:- Jigarmansata25@gmail.com

Author Bio

Sir, In that case you can avail the benefit provided to Banking Sector and can exercise option to avail 50% of credit.

We are NBFC and and paid 100% RCM Tax how much amount will take ITC