Recently in Finance Bill, 2020; amendment as well as insertion has been made in section 6 of Income Tax Act,1961. Therefore for checking residential status of Individual for A.Y. 2021-22 (F.Y. 2020-21) new provision is to be seen.

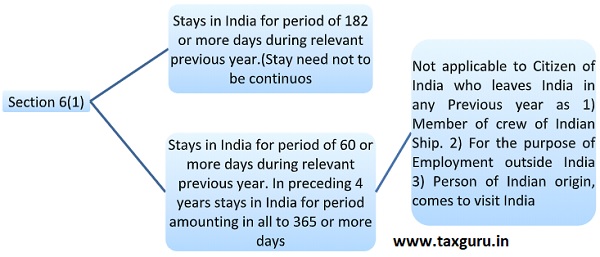

Old Provision Related to Residential Status of Individual for Financial Year 2019-20

Individual will be Resident if:

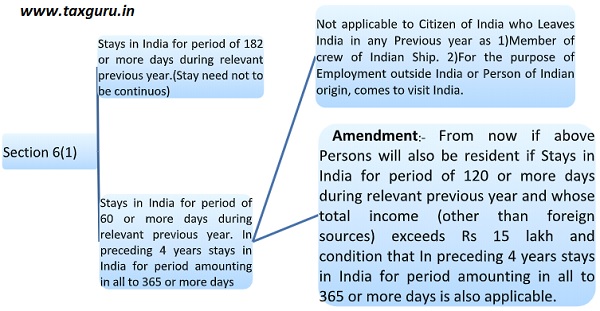

New Provision Related to Residential Status of Individual for Financial Year 2020-21 & Onwards:

Illustration According to New Provision Related to Residential Status of Individual for Financial Year 2020-21 & Onwards:

Illustration:

Question 1 : Mr. X an Indian Citizen stayed in India during relevant financial year for a period of 129 days after that he went U.K. for the purpose of employment. During immediately preceding 4 previous years he has stayed in India for 460 days whether Mr X. is resident in India ?

Ans. Before amendment (For F.Y. 2019-2) Mr. X has not stayed in India for period of 182 days, though he has stayed more than 365 days in preceding 4 previous years he will not be treated as resident. However now has per Finance Act, 2020. Mr X. will be treated as resident of India if total income (other than foreign sources*) exceeds Rs 15 lakhs as he has stayed in India for more than 120 days during relevant previous year and other condition of 365 days in immediately preceding 4 years is also completed.

*(Income from foreign source means income accurse or arisen outside India except the income derived from a business controlled in or profession set up in India)

Conclusion: Mr X. will be treated as Resident in F.Y.2020-21 if total income (other than foreign sources*) exceeds Rs 15 lakhs.

Now Question arise what is provison for being RORI i.e. resident and ordinary resident individual ,as per Finance Act, 2020; Clause 6 of section 6 of Income Tax Act,1961 is also amended and now according to new section individual will not be treated as ordinary resident if :

1) Non-resident in India in seven out of the ten previous years preceding that year, and

2) During the seven previous years preceding that year been in India for a period of, or periods amounting in all to, seven hundred and twenty-nine days or less.

Therefore now if individual is to be treated as ROR then he shall be resident as per section 6(1) in relevant previous year and also he shall be resident in 4 years out of 10 years immediately preceding relevant previous year and stays in India for 730 or more days in immediately preceding 7 years relevant to previous year.

Illustrations:

Question 1: Mr Y. an Indian Citizen has stayed in India for 166 days during relevant previous year after that he left for employment to USA. During immediately preceding 7 previous years he has stayed in India for 860 days and in immediately preceding 4 previous years he has stayed in India for 460 days. His income from India amounts to 19 lakhs during this period, and he was Resident in India for 2 years out of immediately 10 previous year preceding relevant previous year. Whether Mr Y. is resident in previous year 2020-2021?

Ans. Here as Mr. Y has fulfilling the condition of 6(1) he will be resident (i.e. stays in India for more than 120 days during relevant previous year and stays in India for more than 365 days during preceding 4 previous year also his income from India exceeds the threshold of 15 lakhs. However as per Amendment to clause 6 of section 6 Mr.Y is not ordinary resident as he is Non-resident in India in seven out of the ten previous years preceding that year.

Question 2: What if in above example Mr. Y is Resident in India for 4 years out of immediately 10 previous year preceding relevant previous year ?

Ans. In that case Mr, Y will become RORI i.e. resident and ordinary resident Individual.

Further New clause has been inserted in section 6 of Income Tax Act, 1961. From A.Y. 2021-22 i.e. from P.Y.2020-21 clause (1A) has been introduced which determines Notwithstanding anything contained in clause (1) an Individual will be deemed to treated as resident of India if he is citizen of India, and he is not liable to tax in any other country or territory by reason of his domicile or residence or any other criteria of similar nature. Further here also condition that total income (other than foreign sources) should exceed Rs 15 lakhs is applicable.

According to this amendment as Clause (1A) is overriding clause (1) and if we take liberal interpretation , Individual not liable to tax in any other country or territory by reason of his domicile or residence or any other criteria of similar nature will be deemed to be treated as Resident in India irrespective of his stay in India during relevant previous year. This amendment has raised lot many questions that who will be covered and what Income will be taxed; and immediately government has to come of clarification.

Government has clarified that in case of an Indian citizen who becomes deemed resident of India under this proposed provision, income earned outside India by him shall not be taxed in India unless it is derived from an Indian business or profession.

Therefore now it is clear that in case of deemed resident income which will be taxed is Income which is derived from India. It is important to note the difference between income derived from India and income attributable to India. Expression attributable to India is wider than derived from India.

There are also question that in case of deemed resident whether liable to pay tax in other country is sufficient or actual payment is necessary to claim the relief.

Note:- Views/Opinion expressed in article is limited to author’s knowledge and interpretation; it may be interpreted in different manner.

Author Bio

The laws need to be simple and readable by lay men. But they are unable to say in words what they intent to say.

They should clearly define:

1. Resident

2. Not Ordinarily Resident

3. Non Resident

Without interlocutory conditions.

Simply put to understand it. Less than and or less, funny wordings. Upto and less than is a easy word of readable.

You go to different CAs with a problem of this you surely get totally different interpretation.

We need simple worded laws, instead of the law giving a visiting to see a CA or lawyer.