Companies (Auditor’s Report) Order, 2020 (CARO) – Enlarging Auditors Responsibility

“Companies (Auditor’s Report) Order, 2020 (CARO) – Enlarging Auditors Responsibility”Recently Ministry of Corporate Affairs has come out with Companies (Auditor’s Report) Order, 2020; alongwith increase in scope of many clauses and insertion of new clauses, there is also deletion of single clause. Therefore in this article we will analyze such clauses along with various illustrations.Firstly it was applicable to F.Y. 2019-20 but now it is applicable from F.Y. 2020-21.

Accordingly lets look at what are insertion in it as per CARO, 2020;

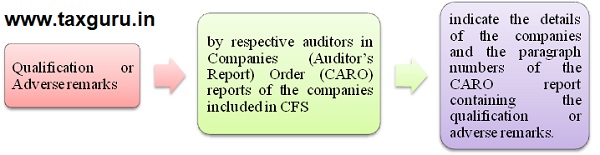

Illustration 1: Mr. A is auditor of consolidated financial statement, Mr. X, Mr. Y, Mr. Z are auditors of different component included in consolidated financial statement. Mr.X has made qualification in his main audit report, Mr. Y has expressed unmodified opinion in respect of component audited by him, Mr. Z has adverse remarks in relation to clause (iv) of Companies (Auditor’s Report) Order, 2020 (CARO). Identify the details/matters that are to be reported by different auditor ?

Answer: In the given case what is to be reported by Mr.A is adverse remark given by Mr. Z (in relation to component audited by him and which is included in CFS) by stating Name of component and paragraph number of the CARO report containing such qualifications or adverse remarks. Such reporting by Mr. A is to be done under clause (xxi) of Companies (Auditor’s Report) Order (CARO) reports.

Further now auditor is required to report in relation to following clauses

There is also change in clause (i) and clause (ii)

Firstly name of clause (i) is changed from Fixed Asset to Property Plant & Equipment and Intangible Assets. Therefore now auditor is required to report whether the company is maintaining proper records showing full particulars of intangible assets. Further, following additional points are required to be reported.

Auditor is also required to report whether any proceedings have been initiated or are pending against the company for holding any benami property under the Benami Transactions (Prohibition) Act, 1988. If yes, whether the company has appropriately disclosed the details in its financial statements.

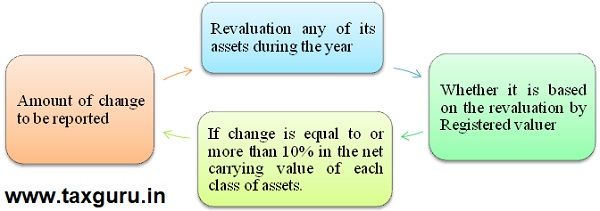

Illustration 2: Mr. R is auditor of XYZ Ltd. during the year it has revalued one of its asset based on report of registered valuer; amount of change is 15% of total net carrying value of such class of asset. It is also having dispute regarding holding of benami property under the Benami Transactions (Prohibition) Act, 1988. Company is of the view that as dispute is pending there is no reporting responsibility of company to disclose the same in financial statement. Determine what is the reporting responsibility of Auditor.

Answer: In the given case Mr.R is required to report under (i)(d) in relation to revaluation of asset along with amount of revaluation as it is equal to or more than 10% in the net carrying value of each class of assets. Further contention of company that it is not under any obligation to disclose about dispute relating to holding of benami property is not correct. Therefore auditor needs to give qualify/adverse remarks in relation clause (i)(e) as dispute has not been appropriately disclosed the details in its financial statements.

Further, now there is additional responsibility on auditor to determine

- Whether in his opinion the procedure and coverage of physical verification conducted by management is appropriate;

- Whether any discrepancies of 10% or more in aggregate has been noticed and if so, whether it has been properly dealt with in the books of account.

Also auditor has to report in case

Illustration 3: Mr. D is auditor of YZ Ltd. during the year working capital limit is sanctioned above Rs. 5 Crore on the basis of security of current assets. The quarterly returns or statements filed by the company with such banks or financial institutions are not in agreement with the books of account of the Company. Mr. D is of the view that since it is responsibility of company to file such statement in accordance books of account he is not required to verify the same at time of audit. Determine what is the reporting responsibility of auditor.

Answer: In the given case though it is responsibility of company to file such statement in accordance books of account, auditor is required to report under clause (ii) in case when such statement/returns are not in agreement with the books of account of the Company. Therefore in given case auditor is required to report the same and contention of auditor is not valid.

Illustration 4: What if in given case limit is sanctioned below Rs. 5 Crore, whether in such auditor is required to report such matter?

Answer: In such case auditor is not required to report under clause (ii), however if company’s balance sheet and profit and loss account dealt with in the report are not in agreement with books of account and returns then auditor is required to report as per section 143(3)(d).

There is insertion of new clause relating to unrecorded income i.e.

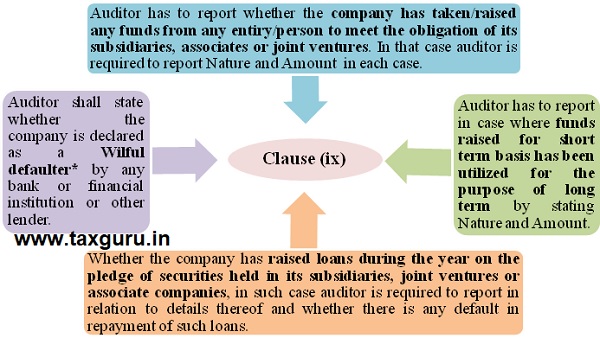

Now in revised clause (ix) (Default in repayment of Loans or other Borrowings) there are four additional points which is to be reported by auditor;

*Wilful Defaulter :- An entity or person that has not paid the loan back despite the ability to repay it.

Illustration 5: Mr. G is auditor of DF Ltd. during the year company has taken loan on the pledge of securities held by it, in its subsidiaries and has also defaulted in repayment of such loan ; however it has paid all the defaulted amount before the date of audit report. Further, funds earlier raised by the company for short term basis has been used to purchase fixed assets. Company is of the view that as amount of diversion is small auditor is not required to report the same and default is also rectified before date of audit report he is not required to report the same. Determine what are the reporting responsibility of auditor ?

Answer: In the given case as per clause (ix) of CARO, 2020; auditor is required to report in case where funds raised for short term basis has been utilized for the purpose of long term by stating nature and amount, irrespective of amount of default.Further when the company has raised loans during the year on the pledge of securities held in its subsidiaries, joint ventures or associate companies, in such case auditor is required to report in relation to details thereof and whether there is any default in repayment of such loans, irrespective of its date of rectification. Therefore contention of company in both the cases is invalid.

There are also change in clause (xvi) of CARO, 2016 by amending such clause auditor is required to report on some additional matters;

- Whether the company has conducted any Non-Banking Financial or Housing Finance activities without a valid Certificate of Registration (CoR) from the Reserve Bank of India.

- If company is a Core Investment Company (CIC), whether it continues to fulfill the criteria of a CIC, and in case the company is an exempted or unregistered CIC, whether it continues to fulfill such criteria.

- If group has more than one CIC as part of the group then indicate the number of CICs which are part of the group.

In CARO,2020 there is insertion of one of the troublesome clause i.e.clause (xix) in the said clause it is requiring auditor to analyze that whether company will be able to meet its liabilities, existing on balance sheet date as an when they will fall due within 1 year. For this auditor will be required to analyze Financial ratios, Ageing of financial assets and financial liabilities, Expected realization of those assets and liabilities. This clause requires auditor to comment on whether in his opinion any material uncertainty exists as on the date of the audit report that company is capable of meeting its liabilities existing at the date of balance sheet as and when they fall due within a period of one year from the balance sheet date.

Illustration 6: Mr. V is auditor of MD Ltd. during the year reserves company has been swallowed and also the cashflow of company are getting negative indicating doubt about going concern of company. The auditor is of the opinion that company will not be able to meet its liabilities, existing on balance sheet date as an when they will fall due within 1 year. Auditor is of the view that as same matter are to be considered and reported as per SA570 therefore there is no requirement to report the same under CARO; Determine whether the contention of auditor is correct ?

Answer: In the given case contention of auditor is not correct because reporting about any matter under CARO cannot be substituted because the same is covered under main report. As per clause (xix) CARO, 2020; auditor is required to report that whether in his opinion any material uncertainty exists as on the date of the audit report that company is capable of meeting its liabilities existing at the date of balance sheet as and when they fall due within a period of one year from the balance sheet date.

There is also insertion of clause which is relating to internal audit, the said clause was removed when CARO, 2016; was notified. Now the same has been inserted in CARO, 2020;

This has increased the responsibility of auditor because now he is liable to determine whether company has adequate in internal audit system and whether he has considered the report of internal auditor.

Illustration 7:Mr. K is auditor of FH Ltd. as per section 138 of Companies Act,2013; company was required to carry out internal audit however it has not appointed any person to carry out internal audit, whether auditor is required to report the same ?What if company is of the view that as a statutory auditor it is not his responsibility to report that whether internal audit is required or not, or it has efficient internal audit system ?

Answer:In the given case as per clause (xiv) auditor is required to report whether the company has an internal audit system commensurate with the size and nature of its business; Accordingly if company is requried to appoint internal auditor but it has not appointed the same then auditor shall report under above clause. Further if company has appropriate internal audit system then auditor also need to determine whether reports of the Internal auditors for the period under audit were considered by him or not. Contention of company that as a statutory auditor it is not his responsibility to report that whether internal audit is required or not, or it has efficient internal audit system is not correct; because as per clause (xiv) of CARO, 2020 the same is required to be reported.

Important point to be considered by auditor:

- Only one clause which has been deleted in Companies (Auditor’s Report) Order, 2020 (CARO); is clause (xi) of Companies (Auditor’s Report) Order, 2016 (CARO) which was relating to Managerial remuneration.

- Further clause (xiv) (Preferential Issue, Private Placement) of Companies (Auditor’s Report) Order, 2016 (CARO) is merged with clause (ix) (Utilization of IPO and Further Public Offer) of Companies (Auditor’s Report) Order, 2016 (CARO).

- In CARO, 2020; Auditor has to additionally report as perclause (xi) (Reporting of Fraud) that whether any report under sub-section (12) of section 143 of the Companies Act has been filed by the auditors in Form ADT-4 and in case if any complaints has been made by whistle-blower to the company during the year whether same has been considered by auditor.

- As per clause (xii) of CARO, 2020 it requires addtionally to report in case where Nidhi companies has defaulted in payment of interest on deposits or repayment thereof for any period during the year.

- New clause has been inserted i.e. clause (xx) of CARO, 2020; requiring auditor to report in relation to compliance with second proviso to sub-section (5) and sub-section (6) of section 135 of Companies Act, 2013.

- Clause (iv) (Loan to director and investment by the company), Clause (vi) (Cost Records), Clause(vii) (Statutory Dues now also includes GST), Clause(xiii) (Related Party Transactions) and Clause (xv) (Non Cash Transactions) of CARO, 2016 has been retained in CARO, 2020 without any changes.

Note:- Views/Opinion expressed in article is limited to author’s knowledge and interpretation; it may be interpreted in different manner.

Author details Email:- Jigarmansata25@gmail.com Contact:- +91- 7383651982/8160207724

Author Bio