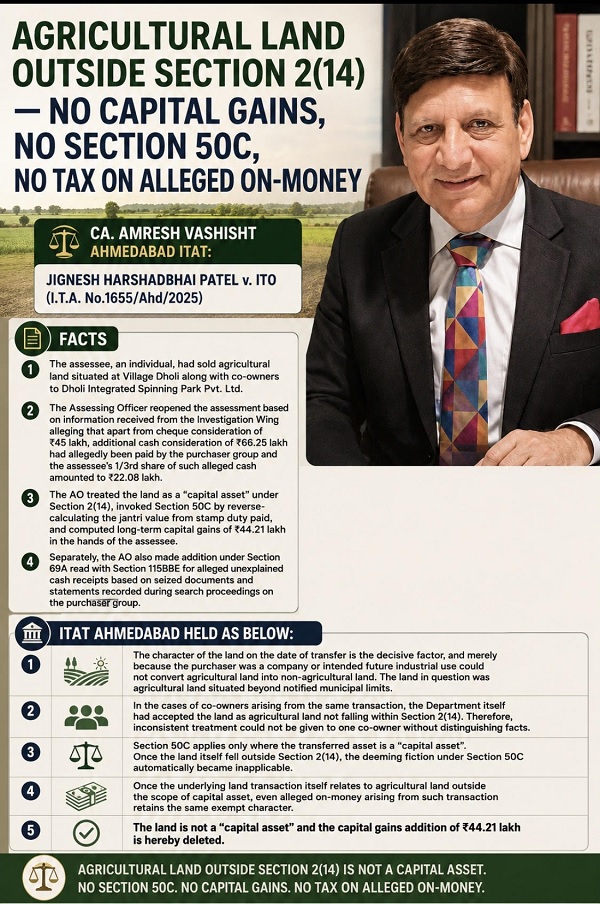

The ITAT Surat in Jignesh Harshadbhai Patel Vs ITO examined whether agricultural land is excluded from the scope of “immovable property” under Section 56(2)(x) of the Income-tax Act in cases where land is purchased for inadequate consideration. The Tribunal held that agricultural land squarely falls within the expression “any land or building or both” used in Section 56(2)(x), and therefore the difference between stamp duty value and actual consideration is taxable where it exceeds prescribed tolerance limits. The ITAT clarified that Section 56(2)(x) operates independently of the definition of “capital asset” under Section 2(14), and exemptions available under capital gains provisions cannot automatically apply to this charging section. The ruling emphasized that the legislature intentionally adopted broad language without excluding rural or agricultural land. The decision has major implications for family settlements, undervalued agricultural land sales, distress transactions, and rural land purchases, reinforcing that anti-abuse deeming provisions can apply even to agricultural land transactions involving lower-than-stamp-value consideration.

Core Issue: Whether agricultural land falls outside the scope of “immovable property” for the purposes of Section 56(2)(x) of the Income-tax Act, 1961.

Tribunal’s Ruling: The ITAT Surat held that agricultural land is also an “immovable property” within the meaning of Section 56(2)(x). Accordingly, where agricultural land is purchased for inadequate consideration, the difference between stamp duty value and actual consideration can be taxed under Section 56(2)(x), subject to statutory tolerance limits.

Legal Position Explained:

Section 56(2)(x) taxes specified properties received:

* without consideration, or

* for consideration lower than stamp duty value beyond prescribed limits.

The definition of “immovable property” under the Explanation to Section 56(2)(x) includes:

* land,

* building, or

* both.

The provision does not carve out any blanket exclusion for agricultural land.

Therefore, once agricultural land qualifies as “land” and is capable of transfer for stamp valuation purposes, it falls within the statutory ambit unless specifically excluded by law.

Findings of the Tribunal:

The Tribunal observed that:

1. The legislature intentionally used broad terminology such as “any land or building or both.”

2. Section 56(2)(x) does not distinguish between:

* capital asset agricultural land,

* rural agricultural land, or

* non-agricultural land.

3. Exemptions available under capital gains provisions cannot automatically be imported into Section 56(2)(x).

4. The charging mechanism under Section 56(2)(x) operates independently of the definition of “capital asset” under Section 2(14).

5. Once stamp duty valuation exceeds permissible variation limits, the differential amount becomes taxable.

Important Principle Emerging:

The ruling reinforces an important interpretational principle:

Exemptions or exclusions under one charging provision cannot automatically control or restrict another independent charging section unless expressly incorporated by statute.

Thus, merely because certain agricultural lands may be excluded from “capital asset” definition under Section 2(14), it does not mean they automatically escape Section 56(2)(x).

Practical Implications:

This decision becomes highly relevant in cases involving:

* family transfers of agricultural land,

* distress sales,

* undervalued sale deeds,

* rural land transactions,

* intra-family settlements,

* or purchases at values significantly below stamp valuation.

Taxpayers dealing in agricultural land must therefore carefully evaluate:

* stamp duty valuation,

* safe harbour limits,

* valuation disputes,

* and applicability of Section 50C/43CA/56(2)(x) interplay.

Broader Tax Impact:

The judgment indicates that anti-abuse deeming provisions under the Act are being interpreted expansively where undervaluation of immovable properties is involved. Even agricultural land transactions may attract scrutiny where consideration appears substantially below circle rate or stamp valuation benchmarks.

Author Bio