GST on Directors: Complete Guide to Director Remuneration, Rent, Guarantees and Company Transactions

Summary: GST on transactions involving directors depends on the capacity in which the director deals with the company rather than the designation. Employee services covered under Schedule III, such as salary paid to managing, whole-time or executive directors under an employer-employee relationship with TDS under Section 192, are outside GST, while services by independent or non-employee directors, including sitting fees, commission and professional fees, are taxable under reverse charge under Section 9(3) read with Notification No. 13/2017-CT(R), Entry 6. The article explains GST treatment for rent, loans, sale of assets, reimbursements, personal guarantees and corporate guarantees, referring to relevant provisions including Section 7, Schedule I, Schedule III, Rule 28(2), Sections 16 and 17(5), CBIC Circular Nos. 140/10/2020-GST, 204/16/2023-GST and 225/19/2024-GST, and Notifications No. 09/2024-CT(R) and 12/2024-CT. It also discusses valuation, forward charge and reverse charge mechanisms, practical compliance checkpoints, and states that corporate guarantees remain subject to litigation. The article concludes that GST treatment should be determined transaction-wise based on the director’s capacity, the nature of the transaction and applicable statutory provisions.

1. Introduction

A director may wear more than one hat. He may be an employee, independent professional, landlord, lender, guarantor, promoter, shareholder, consultant or supplier of goods/services. GST does not tax the designation “director”; it taxes the real nature of transaction.

The key question is always:

In which capacity is the director dealing with the company?

If the transaction is under employer-employee relationship, it is outside GST. If it is a service by a non-employee director to the company, reverse charge may apply. If it is rent, loan, sale of assets or guarantee, separate rules apply.

2. Types of Directors and GST Relevance

| Type of director | Common position | GST relevance |

| Managing Director / Whole-time Director | May be employee or non-employee depending on contract | Salary under employment not taxable; professional fee taxable |

| Executive Director | Generally employee | Schedule III protection if salary/TDS u/s 192 |

| Independent Director | Not employee | Sitting fee/commission taxable under RCM |

| Non-executive Director | Usually not employee | Director services taxable under RCM |

| Nominee Director | Depends on who receives fee and relationship | Examine contract and beneficiary |

| Additional / Alternate / Resident / Woman / Small-shareholder Director | Companies Act classification | GST depends on capacity, not title |

CBIC Circular No. 140/10/2020-GST recognises this distinction and clarifies that whole-time directors may also have dual capacity, while independent/non-employee directors remain outside the employee exclusion.

3. Core GST Legal Framework

| Provision | Relevance |

| Section 7, CGST Act | Defines “supply” |

| Schedule I, Entry 2 | Related person supplies in business may be taxable even without consideration |

| Schedule III, Entry 1 | Employee services to employer are neither goods nor services |

| Section 9(3), CGST Act | Reverse charge on notified supplies |

| Notification No. 13/2017-CT(R), Entry 6 | Services by director to company/body corporate taxable under RCM |

| Section 15 and Rule 28 | Valuation between related persons |

| Rule 28(2), CGST Rules | Special valuation for corporate guarantees |

| Section 16 and 17(5) | ITC eligibility and blocked credits |

Schedule III protects only services by an employee to employer in the course of employment; other dealings between the same persons can still be taxable on their own merits.

4. Transaction-wise GST Matrix: Director and Company

| Transaction | GST position | Charge |

| Salary to MD/WTD/executive director, booked as salary and TDS u/s 192 | Not supply under Schedule III | No GST |

| Sitting fees to independent/non-executive director | Taxable director service | RCM by company |

| Commission to non-employee director | Taxable director service | RCM by company |

| Professional/advisory fee to director outside employment | Taxable service | Generally RCM if supplied by director to company |

| Reimbursement to non-employee director | Part of taxable value unless pure-agent conditions met | RCM |

| Commercial property rent by registered director in personal capacity | Renting service | Forward charge by director |

| Commercial property rent by unregistered director to registered company | Taxable under RCM w.e.f. 10-10-2024 | RCM by company |

| Residential dwelling rented to registered company | Taxable under RCM w.e.f. 18-07-2022 | RCM by company |

| Loan by director to company | Principal is money; interest generally exempt if only interest/discount | No GST on principal/interest exemption |

| Processing/guarantee/commission fee charged by director | Taxable service | RCM/FCM depending capacity |

| Personal guarantee by director to bank for company without consideration | Supply, but value normally nil due RBI restriction | No tax if nil value |

| Personal guarantee with direct/indirect consideration | Taxable on consideration | RCM by company |

| Corporate guarantee by holding/related company | Taxable as related-party service as per CBIC; litigation exists | FCM if domestic, RCM if foreign |

| Sale of goods/assets by director to company | Taxable only if in course/furtherance of business | FCM if supplier registered |

| Employee perquisites under employment contract | Generally outside GST | No GST, subject to facts |

Entry 6 of Notification No. 13/2017-CT(R) covers services supplied by a director of a company/body corporate to the said company/body corporate, where the company is liable under reverse charge.

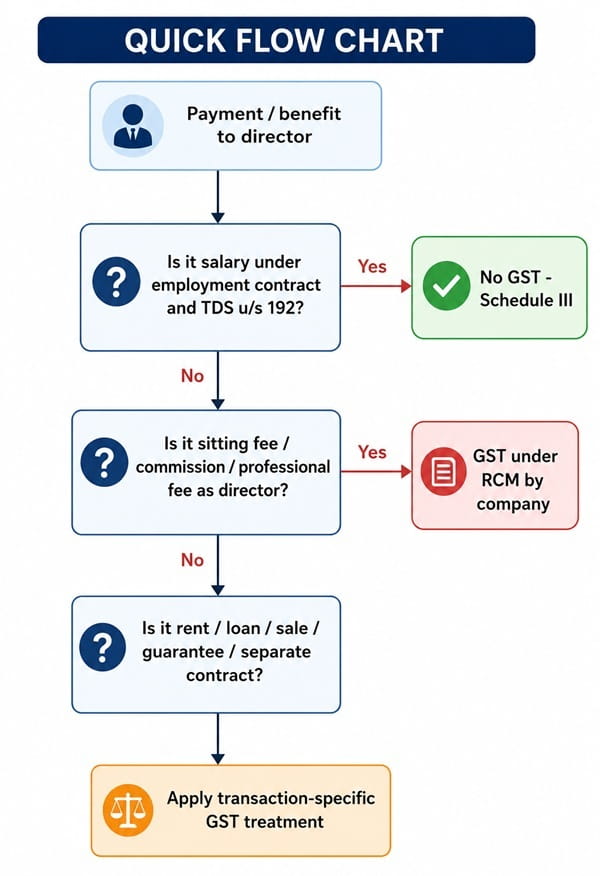

5. Quick Flow Chart

6. Director Remuneration: The Most Important Issue

A. Salary to employee director

If remuneration is declared as salary in the books and TDS is deducted under Section 192 of the Income-tax Act, the payment is treated as consideration for employee services. Such services fall under Schedule III and are outside GST.

This typically covers managing directors, whole-time directors and executive directors where there is a real employer-employee relationship.

B. Sitting fee / commission to independent director

Independent directors and non-executive directors are generally not employees. Sitting fees, commission and similar payments to them are taxable as services.

The company must pay GST under RCM under Entry 6 of Notification No. 13/2017-CT(R) . The applicable rate is generally 18% for professional/business support type services under service rate Notification No. 11/2017-CT(R).

c. Dual capacity

A director can act in two capacities:

Same individual

├── Employee capacity → salary → no GST

└── Professional/director capacity → fee/commission → RCM

The Supreme Court in Ram Pershad v. CIT, (1972) 2 SCC 696 recognised that a managing director may have dual capacity and may also be an employee depending on the terms of engagement. This principle supports the GST distinction between “contract of service” and “contract for service.”

7. Rent Paid by Company to Director

Rent transactions should be examined separately from director remuneration.

A. Commercial property

If a director lets out commercial property to the company in his personal capacity:

| Director status | GST treatment |

| Registered under GST | Director charges GST under forward charge |

| Unregistered and company is registered | Company pays GST under RCM from 10-10-2024 under Entry 5AB |

Notification No. 09/2024-CT(R) inserted Entry 5AB for renting of property other than residential dwelling by an unregistered person to a registered person, effective 10-10-2024.

B. Residential dwelling

Renting of residential dwelling to a registered person is covered under RCM from 18-07-2022. Therefore, if a company takes a residential house from a director, GST is payable by the company under RCM.

ITC should be examined carefully. If the house is used for personal residence or personal consumption, Section 17(5)(g) may block ITC. If used as business guest house, facts and documentation become crucial.

8. Loans, Interest and Securities

A loan by director to company is not a supply of goods or services to the extent it is merely money. Interest on loans, deposits or advances is generally exempt when consideration is represented only by interest or discount.

However, separate charges like processing fee, guarantee commission, documentation charges or facilitation fee may become taxable.

Loan principal → Not goods/services

Interest only → Generally exempt

Separate fee/commission → Taxable

9. Personal Guarantee by Director

This has been specifically clarified by CBIC in Circular No. 204/16/2023-GST.

A director and company are related persons. Therefore, personal guarantee by a director for securing credit facilities for the company can be treated as supply even without consideration under Section 7 read with Schedule I.

However, RBI guidelines say that personal guarantees of directors should not be used as a source of income. Banks should obtain undertakings that no consideration by way of commission, brokerage fee or any other form is paid directly or indirectly to the guarantor.

Therefore, CBIC clarified that where no consideration is paid, open market value may be treated as zero, and no GST is payable. If any consideration is paid directly or indirectly, GST is payable on such consideration.

10. Corporate Guarantee by Directors / Related Companies

Corporate guarantee is different from personal guarantee.

Where a holding company or related company provides corporate guarantee to banks/financial institutions for another related company, CBIC treats it as taxable supply under Schedule I even without consideration.

Rule 28(2) valuation

From 26-10-2023, Rule 28(2) provides a special valuation mechanism:

| Situation | Value |

| Corporate guarantee to bank/FI for related person located in India | 1% per annum of guarantee amount or actual consideration, whichever is higher |

| Period less than one year | Proportionate value |

| Fixed guarantee for 5 years | 1% × 5 years, or actual consideration, whichever higher |

| Full ITC available to recipient | Invoice value deemed value due retrospective amendment |

Rule 28(2) was amended retrospectively by Notification No. 12/2024-CT w.e.f. 26-10-2023, and Circular No. 225/19/2024-GST clarified important operational issues.

FCM or RCM?

| Corporate guarantee provider | GST payment |

| Domestic related company / holding company | Forward charge by guarantor company |

| Foreign/overseas related entity for Indian company | RCM by Indian recipient |

| Multiple co-guarantors | Proportionate valuation |

| Loan not disbursed or partly disbursed | Value based on guarantee amount, not actual loan disbursal |

CBIC clarified that domestic intra-group corporate guarantees are under forward charge, while guarantees by foreign/overseas related entities for Indian recipients are under RCM.

Litigation note

The Bombay High Court, Nagpur Bench, judgment in M/s D.P. Jain & Co. Infrastructure Private Limited v. Union of India & Ors., Writ Petition No. 2087 of 2025 dated 06.05.2026, held that corporate guarantees without consideration were not taxable on the facts before it, relying also on the Supreme Court’s in Commissioner of CGST & Central Excise v. M/s Edelweiss Financial Services Ltd., Civil Appeal No. 1769 of 2023 / Civil Appeal Diary No. 5258 of 2023, dated 17.03.2023; reported as 2023 (73) G.S.T.L. 4 (S.C.).. However, the Court did not strike down Rule 28(2). This issue may still travel further in litigation.

11. Circulars and Rulings on Directors

| Reference | Principle |

| Circular No. 140/10/2020-GST | Salary to employee director not taxable; independent/non-employee director remuneration taxable under RCM |

| Circular No. 204/16/2023-GST | Personal guarantee by director: value generally nil if no consideration due RBI restriction; corporate guarantee taxable as related-party supply |

| Circular No. 225/19/2024-GST | Corporate guarantee valuation, FCM/RCM, co-guarantees, renewal, time period and ITC clarification |

| Alcon Consulting Engineers (India) Pvt. Ltd., Karnataka AAR, Order No. KAR/AAR/83/2019-20 dated 25.09.2019 | Director remuneration examined under RCM |

| Clay Craft India Pvt. Ltd., Advance Ruling No. RAJ/AAR/2019-20/33 dated 20.02.2020; reported as 2020 (35) G.S.T.L. 580 (A.A.R. – GST – Raj.) | Earlier broad ruling modified by appellate approach after CBIC Circular; salary vs non-salary distinction |

| Anil Kumar Agrawal, Karnataka AAR, Order No. KAR/ADRG/30/2020 dated 04.05.2020 | Executive director salary not taxable; non-executive director remuneration taxable under RCM |

Advance rulings are binding only on the applicant and jurisdictional officer, but they remain useful persuasive guidance for audits and litigation.

12. Supreme Court Support

| Judgment | Use in GST director disputes |

| Ram Pershad v. Commissioner of Income Tax, New Delhi, (1972) 2 SCC 696; AIR 1973 SC 637; (1973) 86 ITR 122 (SC) | Director can have dual capacity; helps distinguish salary from professional/director fee |

| Commissioner of CGST & Central Excise v. M/s Edelweiss Financial Services Ltd., Civil Appeal No. 1769 of 2023 / Civil Appeal Diary No. 5258 of 2023, order dated 17.03.2023; 2023 (73) G.S.T.L. 4 (S.C.) | Corporate guarantee without consideration not taxable under service tax; persuasive for guarantee disputes |

| Union of India & Ors. v. VKC Footsteps India Pvt. Ltd., Civil Appeal No. 4810 of 2021, judgment dated 13.09.2021; (2022) 2 SCC 603; AIR 2021 SC 4407 | Tax credit and GST benefits are governed by statute; useful reminder that ITC must satisfy statutory conditions |

| Union of India & Anr. v. M/s Mohit Minerals Pvt. Ltd., Civil Appeal No. 1390 of 2022, judgment dated 19.05.2022; (2022) 10 SCC 700 | GST levy must fit statutory charging framework; helpful in challenging artificial valuation/levy beyond charging provisions |

These judgments do not override specific GST notifications by themselves, but they provide principles of employment relationship, consideration, statutory levy and tax certainty.

13. Practical Compliance Checklist

| Checkpoint | Action |

| Employment contract | Keep appointment letter, board resolution and payroll records |

| TDS section | Section 192 supports no GST; Section 194J supports taxable service |

| Director invoices | Needed where director is registered and transaction is under FCM |

| RCM payment | Pay in cash; claim ITC only if eligible |

| Rent agreements | Clearly mention whether property is let in personal capacity |

| Guarantees | Preserve bank sanction terms, guarantee deed and no-consideration declarations |

| Corporate guarantee | Track issue date, renewal date, guarantee amount and period |

| Related-party valuation | Apply Rule 28 and keep ITC eligibility evidence |

| Litigation position | For corporate guarantee without consideration, evaluate whether to follow CBIC circular or litigate based on High Court/Supreme Court support |

14. Conclusion

GST on directors is not a one-line issue. The correct approach is capacity-based.

Employee director salary → No GST

Independent / non-employee director fee → RCM

Rent / loan / sale → Nature-specific treatment

Personal guarantee without consideration → Value nil, no tax

Corporate guarantee → Rule 28(2), subject to litigation

The safest professional approach is to document the capacity of the director, maintain separate agreements for separate roles, apply TDS correctly, and review all director-ledger transactions during GST audit.

*****

About the Author: CA Rajender Arora is a Chartered Accountant with 24 years of professional experience. He is a GST faculty, speaker and consultant, actively engaged in GST research, advisory, litigation support, drafting of replies, opinions and professional training.

Disclaimer: This article is for professional education and general guidance only. GST implications may change depending on facts, agreements, accounting treatment, TDS classification, registration status, place of supply, ITC eligibility and subsequent judicial developments. Readers should examine the latest law, notifications, circulars and judicial precedents before taking any tax position. This article should not be treated as legal opinion for any specific case.

Author Bio