Input Service Distributor (ISD) Mechanism Under GST Law: A Comprehensive Legal Analysis (As Amended Up To April 2026)

ABSTRACT

The Input Service Distributor (ISD) mechanism has been a cornerstone of the credit distribution architecture under the Goods and Services Tax (GST) framework since its inception on 1st July, 2017. Having been inherited from the erstwhile Service Tax regime, the ISD mechanism enables a registered office of a business enterprise to receive tax invoices pertaining to common input services and distribute the embedded Input Tax Credit (ITC) to its constituent branches and distinct persons registered under the same Permanent Account Number (PAN). Following a prolonged period of legislative deliberation and administrative uncertainty, a watershed transformation has been ushered in by way of the Finance Act (No. 1), 2024, and the Finance Act, 2025, read with Notification No. 16/2024-Central Tax dated 6th August, 2024, whereby the ISD mechanism has been rendered mandatory with effect from 1st April, 2025. The Act amendments (Sections 2(61) and 20) were brought into force w.e.f. 1st April, 2025 by Notification No. 16/2024-Central Tax dated 6th August, 2024, while the corresponding Rule 39 amendments (notified vide Notification No. 12/2024-Central Tax dated 10th July, 2024) were brought into force w.e.f. 1st April, 2025 by the separately issued Notification No. 09/2025-Central Tax dated 11th February, 2025. The present article offers an exhaustive analysis of the ISD mechanism, tracing its statutory evolution, the legislative architecture as amended, the procedural compliance framework, the ISD vis-à-vis cross-charge dichotomy, treatment of Reverse Charge Mechanism (RCM) under ISD, relevant circulars, FAQs, advance rulings, and critical judicial and quasi-judicial perspectives, as obtaining on the date of this publication.

I. LEGISLATIVE HISTORY AND CONCEPTUAL GENESIS

The concept of an Input Service Distributor is not of recent origin. It was first introduced under the Finance Act, 1994, governing the Service Tax regime, and was codified under Rule 7 of the CENVAT Credit Rules, 2004. Under the erstwhile regime, the ISD was permitted to distribute CENVAT credit of service tax paid on input services to its manufacturing plants or service-providing units through a prescribed distribution mechanism. The GST Council, in its wisdom, retained and refined this concept while incorporating it into the central statute, recognising the commercial reality that large enterprises procure certain services at a single centralised location — typically the Head Office (HO) — the benefit of which accrues to multiple distinct registrations across the country.

Since the rollout of GST on 1st July, 2017, the ISD mechanism was governed by Section 2(61) and Section 20 of the Central Goods and Services Tax Act, 2017 (hereinafter, the “CGST Act”), read with Rule 39 and Rule 54(1) of the Central Goods and Services Tax Rules, 2017 (hereinafter, the “CGST Rules”). However, the legislative architecture initially rendered the ISD mechanism merely optional — an alternative to the cross-charge mechanism — leading to widespread commercial practice of distributing common ITC through the cross-charge route, often without obtaining a separate ISD registration.

This state of affairs underwent a fundamental transformation through an incremental series of legislative and administrative actions, the most critical being the amendments introduced by the Finance Act (No. 1), 2024, the Finance Act, 2025, and the consequential notifications and amendments to the CGST Rules, 2017. The cumulative effect of these changes has been to transform the ISD mechanism from a voluntary compliance tool into a mandatory statutory obligation, with effect from 1st April, 2025.

II. STATUTORY FRAMEWORK — PROVISIONS OF LAW

2.1 Definition of Input Service Distributor — Section 2(61) of the CGST Act

The term “Input Service Distributor” is defined under Section 2(61) of the CGST Act, 2017. The definition, as substituted by the Finance Act (No. 1), 2024, with effect from 1st April, 2025, reads as follows:

“‘Input Service Distributor’ means an office of the supplier of goods or services or both that receives tax invoices towards the receipt of input services, including invoices in respect of services liable to tax under sub-section (3) or sub-section (4) of section 9, for or on behalf of distinct persons referred to in section 25, and liable to distribute the input tax credit in respect of such invoices in the manner provided in section 20.”

The above definition, as substituted by the Finance Act, 2024 (Act No. 8 of 2024), w.e.f. 1st April, 2025, incorporates the following critical expansion vis-à-vis the pre-amendment definition: the explicit inclusion of invoices in respect of services liable to tax under the Reverse Charge Mechanism (RCM) under sub-sections (3) and (4) of Section 9 of the CGST Act (i.e., CGST-RCM transactions). Prior to this amendment, the definition referred only to “tax invoices issued under Section 31 towards the receipt of input services” — a phrase that was widely interpreted to exclude RCM invoices.

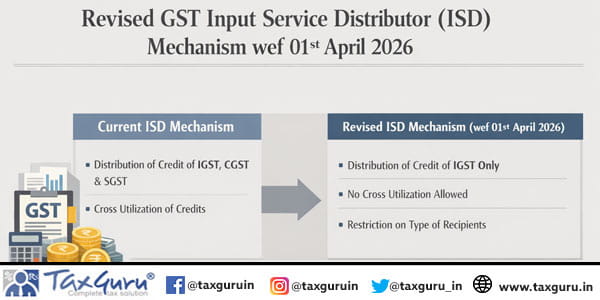

Further, the Finance Act, 2025 has amended Sections 20(1) and 20(2) of the CGST Act to additionally insert a reference to sub-sections (3) and (4) of Section 5 of the Integrated Goods and Services Tax Act, 2017 (hereinafter, the “IGST Act”), thereby explicitly enabling the ISD to distribute credit in respect of inter-State supplies liable to RCM (i.e., IGST-RCM transactions) as well. These amendments are effective from 1st April, 2025, and the official text of Section 20 as currently published by the CBIC already reflects this expansion as in-force law. Rule 39(1A) correspondingly covers both CGST-RCM and IGST-RCM credit distributions with effect from the same date.

2.2 Distribution Mechanism — Section 20 of the CGST Act

Section 20 of the CGST Act, as substituted by the Finance Act (No. 1), 2024 (effective 1st April, 2025), is the foundational provision governing the manner of distribution of ITC by an ISD. Section 20(1) directs that any qualifying office of a supplier shall be required to be registered as an Input Service Distributor under clause (viii) of Section 24 of the CGST Act — it is Section 24(viii) that constitutes the actual compulsory-registration hook, with Section 20(1) providing the operative mandate to obtain that registration. Section 20 continues to contain the core statutory rules on ISD obligations, including the registration requirement, the direction to distribute ITC in the prescribed manner, and the tax-type split between Central Tax and Integrated Tax. What Section 20(3) delegates to Rule 39 is the detailed procedural mechanics — the distribution formula, the conditions governing allocation, and the treatment of credit notes and debit notes. The two provisions therefore operate together: Section 20 supplies the substantive framework; Rule 39 supplies the computational procedure.

The said Section, inter alia, provides that:

- Every qualifying office shall be required to be registered as an ISD under Section 24(viii) of the CGST Act.

- Every ISD shall distribute the ITC available for distribution in a manner and subject to conditions as may be prescribed under Rule 39.

- The ITC on account of Central Tax is required to be distributed as Central Tax or Integrated Tax, and that on account of Integrated Tax shall be distributed as Integrated Tax — the tax-type distribution rules are anchored in Section 20(3) read with Rule 39.

2.3 Rule 39 of the CGST Rules, 2017 — Distribution Formula and Conditions

Rule 39 of the CGST Rules, as substituted vide Notification No. 12/2024-Central Tax dated 10th July, 2024, and brought into force w.e.f. 1st April, 2025 by Notification No. 09/2025-Central Tax dated 11th February, 2025, lays down the detailed procedure, formula, and conditions for distribution of ITC by an ISD. The following are the critical limbs of Rule 39:

(a) Distribution Formula

The ITC is distributed on a pro rata basis based on the turnover of the recipient branches in the relevant period, using the following formula:

C1 = (t1 ÷ T) × C Where: C1 = Amount of ITC to be distributed to recipient R1 t1 = Turnover of recipient R1 during the relevant period T = Aggregate turnover of all recipients to whom the service is attributable C = Total credit available for distribution

(b) Conditions of Distribution

- Credit available for distribution in a given month must be distributed within the same month — deferment is impermissible.

- Credit distributed must not exceed the credit available for distribution.

- Eligible and ineligible ITC must be distributed separately.

- ITC attributable to a specific recipient must be distributed only to that recipient, even if the recipient is unregistered or engaged in making exempt supplies.

- ITC attributable to common use across multiple recipients is distributed pro rata based on turnover.

(c) Tax Type Segregation Rules

The manner of distribution based on the type of tax is as follows:

| Nature of ITC in the hands of ISD | Location of Recipient vis-à-vis ISD | Tax Type for Distribution |

| CGST + SGST/UTGST | Same State / UT as ISD | CGST + SGST/UTGST (as is) |

| CGST + SGST/UTGST | Different State / UT | IGST |

| IGST | Any State / UT | IGST (always) |

(d) Relevant Period

The ‘relevant period’ for computing the pro-rata turnover is defined as the preceding financial year. Where no turnover data is available for the preceding financial year, the last quarter for which returns have been filed shall be considered.

(e) Sub-Rule (1A) — Transfer of RCM Credit to ISD

A new sub-rule (1A) has been inserted in Rule 39, which enables a registered person (having the same PAN and State Code as the ISD) to issue an invoice, credit note, or debit note to transfer the credit of common input services subject to reverse charge to the ISD. This provision caters to the practical scenario where the RCM liability is discharged by a regular registrant (e.g., the Head Office), and the corresponding ITC, after availing, needs to be routed through the ISD for equitable distribution.

2.4 Rule 54(1) of the CGST Rules — ISD Invoice

Rule 54(1) of the CGST Rules, 2017 prescribes the form and content of the ISD invoice. An ISD invoice must specifically state that it is issued for the purpose of “distribution of Input Tax Credit”. The particulars to be mentioned in an ISD invoice include:

- Name, address, and GSTIN of the ISD (distributor)

- Consecutive serial number, not exceeding sixteen characters

- Date of issue

- Name, address, and GSTIN of the recipient

- Amount of ITC distributed — separately for CGST, SGST/UTGST, and IGST

- Signature or digital signature of the authorised signatory

It is pertinent to note that an ISD invoice does not involve a charge of GST — it merely evidences the distribution of credit. Accordingly, it is not required to be reported in GSTR-1 or GSTR-3B of the ISD. An ISD credit note must be issued to reduce credit previously distributed, wherever applicable.

2.5 Mandatory Registration — Section 24(viii) of the CGST Act

Section 24(viii) of the CGST Act, 2017 mandates compulsory registration for an Input Service Distributor, irrespective of the quantum of turnover. Accordingly, there is no threshold limit for ISD registration — once the qualifying conditions are met, registration becomes legally obligatory.

Key aspects of ISD registration are:

- Application in Form GST REG-01 — the applicant must check ‘Yes’ against Serial No. 14 (ISD).

- A separate ISD registration is required even if the applicant is already registered as a regular taxpayer in the same State — an ISD registration is specific to credit-distribution activity and cannot be merged with a regular taxpayer registration.

- Multiple offices of the same entity may separately register as ISD in their respective States, provided that not more than one ISD registration is obtained per State for a given legal entity.

- There is no turnover threshold for ISD registration — the obligation arises solely upon satisfaction of the qualifying conditions under Section 20 read with Section 24(viii).

III. LEGISLATIVE MILESTONES — A CHRONOLOGICAL ANALYSIS

| Date / Reference | Legislative Instrument | Key Development |

| 1st July 2017 | CGST Act, 2017 — Original Enactment | ISD mechanism introduced under Sections 2(61) & 20. Registration voluntary. Cross-charge permitted as alternative. |

| 11th July 2023 | 50th GST Council Meeting | Council recommended making ISD mandatory prospectively. Cross-charge to co-exist for internally generated services. |

| 17th July 2023 | CBIC Circular No. 199/11/2023-GST | Clarified that ISD is not mandatory under existing provisions; HO may choose either ISD or cross-charge for third-party common services. |

| 7th October 2023 | 52nd GST Council Meeting | Recommended amendments to Sections 2(61) and 20 of CGST Act, and Rule 39 of CGST Rules, to implement mandatory ISD. |

| 1st February 2024 | Finance Bill (No. 1), 2024 (Interim Budget) | Introduced proposed amendments to Sections 2(61) and 20 — inclusion of RCM invoices under ISD scope; mandatory ISD framework proposed. |

| 15th February 2024 | Finance Act (No. 1), 2024 | Amendments to Sections 2(61) and 20 received Presidential assent. |

| 10th July 2024 | Notification No. 12/2024-Central Tax | Rule 39 of CGST Rules substituted — new ITC distribution procedure, formula, and tax-type segregation rules; Sub-rule (1A) inserted for RCM credit transfer to ISD. Commencement date separately notified. |

| 6th August 2024 | Notification No. 16/2024-Central Tax | Appointed 1st April, 2025 as the effective date for the CGST Act amendments — substitution of Sections 2(61) and 20 of the CGST Act, 2017. |

| 1st February 2025 | Finance Act, 2025 | Sections 20(1) and 20(2) further amended to explicitly include inter-State RCM under Section 5(3)/5(4) of the IGST Act within ISD scope — effective 1st April, 2025. Official text and Rule 39(1A) now reflect this expansion as in-force law. |

| 11th February 2025 | Notification No. 09/2025-Central Tax | Appointed 1st April, 2025 as the commencement date for the Rule 39 amendments notified vide Notification No. 12/2024-Central Tax, separately bringing into force the new ISD distribution procedure under the CGST Rules. |

| 1st April 2025 | Effective Date of all Amendments | ISD mechanism becomes mandatory. Common input service ITC to be distributed through ISD. Cross-charge remains applicable for internally generated services and intra-group supplies not governed by the mandatory ISD framework. |

IV. ISD MECHANISM vs. CROSS-CHARGE: A POST-AMENDMENT ANALYSIS

Prior to the Finance Act (No. 1), 2024, the distribution of ITC in respect of common input services procured from third parties could be accomplished through either of the following two mechanisms:

a. Input Service Distributor mechanism under Section 20 of the CGST Act read with Rule 39.

b. Cross-charge mechanism involving issuance of a tax invoice by the HO to the Branch Office (BO) under Section 31 read with Section 15 of the CGST Act.

The CBIC, vide Circular No. 199/11/2023-GST dated 17th July, 2023, had categorically clarified that both mechanisms were permissible, and that the ISD route was not compulsory under the then-prevailing law. This clarity was extended as a result of protracted litigation and conflicting departmental positions on the issue.

4.1 Position After 1st April, 2025

With effect from 1st April, 2025, the following dichotomy applies:

| Parameter | ISD Mechanism (Post 01.04.2025) | Cross-Charge (Residual Scope) |

| Applicability | Mandatory for all common third-party input services procured centrally for multiple GSTINs under same PAN. | Applicable only for internally generated services (e.g., services rendered by HO employees for benefit of BOs). |

| Registration Needed | Yes — separate ISD registration compulsory. | No separate registration; existing registration suffices. |

| Invoicing | ISD invoice under Rule 54(1) — no GST charged. | Tax invoice under Section 31 — GST charged at applicable rate. |

| ITC in Recipient | Auto-populated in GSTR-2B of recipient; claimed in GSTR-3B. | Recipient claims ITC on tax invoice of cross-charge, subject to Sections 16 and 17. |

| Return Filing | Monthly GSTR-6 by ISD. | GSTR-1 and GSTR-3B by HO; GSTR-3B by BO. |

| Valuation | Only credit amount distributed — no cost allocation. | Valuation as per Section 15 read with Rule 28 (open market value / cost-plus basis). |

It bears emphasis that the mandatory ISD framework under Section 20 and Rule 39 is specifically tied to the distribution of ITC in respect of common input services — it does not create a blanket obligation covering every category of intra-group credit. Cross-charge continues to apply for internally generated services (such as services provided by HO employees to branches), and its broader applicability to intra-group supplies that fall outside the ISD framework is a matter that turns on the nature of the underlying supply. What the amended law unambiguously mandates is that wherever an ISD-qualifying situation arises — i.e., centrally received third-party input service invoices attributable to multiple GSTINs under the same PAN — the ISD route is the only permissible mechanism. Any continued use of cross-charge for such transactions from 1st April, 2025, carries the risk of ITC denial in the hands of the recipient and potential demand under the applicable provisions of the CGST Act.

V. ISD AND THE REVERSE CHARGE MECHANISM — A CRITICAL NEXUS

One of the most consequential amendments introduced by the Finance Act (No. 1), 2024, is the explicit inclusion of RCM invoices within the ambit of the ISD mechanism. Prior to this amendment, an ISD was not entitled to avail ITC in respect of services on which tax was paid on reverse charge basis, as the liability to discharge RCM tax and avail corresponding ITC vested individually in each registered person.

5.1 Pre-Amendment Position (Before 1st April, 2025)

Under the original framework, if the Head Office of a multi-state enterprise was the sole registered person discharging RCM liability on behalf of all branches (e.g., on legal consultancy, import of services, manpower supply, etc.), only the HO was entitled to avail ITC on such RCM invoices. The credit could not be distributed through ISD to other branches, and the cross-charge route was the only available mechanism for credit migration — itself fraught with valuation and eligibility disputes.

5.2 Post-Amendment Position (Effective 1st April, 2025)

The amended Section 2(61) and Rule 39(1A) now provide a clear pathway for RCM credit distribution through ISD. The operative mechanism is as follows:

1. The entity that discharges the RCM liability avails ITC upon payment of tax and filing of GSTR-3B. It is important to note that Rule 39(1A) permits this RCM credit transfer only by a distinct person registered in the same State as the ISD — an entity in a different State cannot route its RCM credit to the ISD under this sub-rule.

2. The said distinct person (e.g., the HO, if registered in the same State as the ISD) then issues an invoice, credit note, or debit note under Rule 39(1A) to transfer the RCM credit to the ISD. Where the ISD registration and the RCM-paying entity are co-located in the same State, the HO effectively transfers the credit to itself as ISD before distributing it downstream.

3. The ISD distributes the credit to the recipient units in the prescribed manner under Rule 39.

Furthermore, the Finance Act, 2025 has amended Sections 20(1) and 20(2) of the CGST Act to explicitly provide for distribution of ITC in respect of inter-State supplies subject to RCM under sub-sections (3) and (4) of Section 5 of the IGST Act, 2017. These amendments are effective from 1st April, 2025, and the official text of Section 20 as currently published by the CBIC confirms this expansion as in-force law — not a pending proposal. Rule 39(1A) likewise covers both CGST-RCM and IGST-RCM distributions from the same date. This closes the earlier legislative gap wherein cross-border RCM transactions attracting IGST were not explicitly covered under the ISD distribution framework, thereby ensuring a complete and seamless statutory architecture for all RCM credit distributions through the ISD mechanism.

VI. COMPLIANCE FRAMEWORK — RETURN FILING AND PROCEDURAL OBLIGATIONS

6.1 Form GSTR-6 — Monthly Return

An ISD is required to file a monthly return in Form GSTR-6 by the 13th day of the month succeeding the month in which the ITC is received. The return captures:

- Details of ITC received from vendors (inward supplies).

- Details of ITC distributed to recipient units (ISD invoices and credit/debit notes issued).

- Bifurcation of eligible and ineligible ITC.

- Segregation by tax type: CGST, SGST/UTGST, IGST.

GSTR-6 must be filed even if there is no ITC to distribute in a given month (Nil return requirement). The due date for GSTR-6 is the 13th day of the month succeeding the tax period. As a practical portal matter, GSTR-6 is typically filed on the basis of GSTR-6A (auto-populated inward supply data from vendors’ GSTR-1), and taxpayers generally await vendor GSTR-1 filings before proceeding — however, there is no express statutory bar on filing GSTR-6 at any point before the 13th.

6.2 Auto-Population and Recipient GSTR-2B

The ITC distributed by the ISD through GSTR-6 is auto-populated in the GSTR-2A (Part B) and GSTR-2B of the respective recipient units. The recipient units claim the distributed ITC in their GSTR-3B for the corresponding tax period. ISD invoices are not to be reported in GSTR-1 or GSTR-3B of the ISD itself.

6.3 No Annual Return for ISD

An ISD is not required to file an annual return under Section 44 of the CGST Act. This is because GSTR-6 itself consolidates the receipt and distribution details on a monthly basis, obviating the need for a separate annual reconciliation return.

6.4 Late Fees

Late filing of GSTR-6 attracts a late fee under Section 47 of the CGST Act, 2017. The general late fee under Section 47 for returns filed under Section 39 is Rs. 100 per day per Act (i.e., Rs. 200 per day in aggregate under CGST and SGST). However, vide Notification No. 07/2018-Central Tax, the CBIC reduced the late fee for delayed filing of GSTR-6 to Rs. 25 per day under CGST and Rs. 25 per day under SGST (Rs. 50 per day in aggregate), subject to a maximum of Rs. 10,000 in aggregate, for returns with tax liability. It is important to note that no separate reduced rate has been notified for Nil GSTR-6 returns as of the date of this article — accordingly, the same Rs. 50/day (aggregate) rate, as reduced by Notification No. 07/2018-CT, applies to Nil GSTR-6 returns as well, subject to the maximum cap. Readers are advised to verify any subsequent waiver notifications before relying on these figures for any particular period.

VII. ILLUSTRATIVE EXAMPLES

Example 1: Distribution of Common Input Service (Same-State and Inter-State)

ABC Limited (HO in Delhi, registered as ISD in Delhi) receives an invoice from a software company for IT maintenance services amounting to Rs. 10,00,000 with GST at 18% (IGST Rs. 1,80,000). The services are used by its three branches: Delhi (Branch A), Maharashtra (Branch B), and Karnataka (Branch C). Turnovers for the preceding financial year:

| Branch | Turnover (Rs.) | Proportion |

| Branch A — Delhi | 50,00,000 | 50/200 = 25% |

| Branch B — Maharashtra | 80,00,000 | 80/200 = 40% |

| Branch C — Karnataka | 70,00,000 | 70/200 = 35% |

| Total (T) | 2,00,00,000 | 100% |

ITC Distribution: Since the ISD received IGST credit, it must distribute the credit as IGST irrespective of the location of recipients:

- Branch A (Delhi): Rs. 1,80,000 × 25% = Rs. 45,000 (IGST)

- Branch B (Maharashtra): Rs. 1,80,000 × 40% = Rs. 72,000 (IGST)

- Branch C (Karnataka): Rs. 1,80,000 × 35% = Rs. 63,000 (IGST)

Example 2: Distribution of CGST + SGST (Delhi) to Same-State and Different-State Recipients

If in the above scenario the invoice had been for a localised legal service attracting CGST + SGST (Delhi) instead of IGST, the distribution would be:

- Branch A (Delhi) — same State as ISD: CGST + SGST (Delhi) distributed as-is.

- Branch B (Maharashtra) — different State: CGST + SGST (Delhi) converted and distributed as IGST.

- Branch C (Karnataka) — different State: CGST + SGST (Delhi) converted and distributed as IGST.

VIII. CBIC CIRCULARS, FAQs AND ADMINISTRATIVE GUIDANCE

8.1 Circular No. 199/11/2023-GST dated 17th July, 2023

This circular, issued pursuant to the decisions of the 50th GST Council Meeting, addressed the inter-relationship between ISD and cross-charge. The CBIC categorically clarified the following:

1. The ISD mechanism for distribution of ITC on common input services procured from third parties was not mandatory under the then-prevailing provisions.

2. The HO could either adopt the ISD mechanism or issue a cross-charge tax invoice to the BO for attribution of ITC on common third-party services.

3. For internally generated services (such as services rendered by HO employees to BOs), the cross-charge mechanism was applicable.

4. Consistent with the recommendation of the 50th GST Council, the circular acknowledged that the ISD mechanism would be made mandatory prospectively for third-party common input services — the specific effective date of 1st April, 2025 was subsequently notified separately by Notification No. 16/2024-Central Tax dated 6th August, 2024 and Notification No. 09/2025-Central Tax dated 11th February, 2025, and was not part of Circular No. 199/11/2023-GST itself.

8.2 FAQs on Banking and Financial Services (CBIC)

The CBIC FAQs on Banking and Financial Services had, prior to the 2024 amendments, clarified that cross-charge was an equally valid alternative to the ISD mechanism for distributing ITC on common services. These FAQs, to the extent they conflict with the post-April 2025 mandatory ISD framework, must be read subject to the overriding legislative amendments.

8.3 A Note on Circular No. 225/19/2024-GST

It is important to clarify a potential source of confusion: Circular No. 225/19/2024-GST pertains to the valuation of corporate guarantees between related persons under GST — it does not address ISD or cross-charge. It should not be treated as an ISD clarification circular. Practitioners should be cautious not to conflate this circular with the ISD framework. The principal circular governing the ISD vs. cross-charge question remains Circular No. 199/11/2023-GST dated 17th July, 2023.

IX. ADVANCE RULINGS — JUDICIAL AND QUASI-JUDICIAL PERSPECTIVE

While the ISD mechanism itself has not generated as extensive a body of advance rulings as some other provisions of the CGST Act, certain rulings and judicial observations have shaped its interpretation:

9.1 ISD vs. Cross-Charge — The Core Debate

Prior to the 2024 amendments, the question of whether ISD was mandatory or whether cross-charge was permissible as an alternative had been debated in multiple proceedings. The position, as clarified by Circular No. 199/11/2023-GST, is that both were permissible prior to 1st April, 2025. Post that date, the legislative mandate is unambiguous: third-party common services must be routed through ISD.

9.2 ITC Eligibility in the Hands of the Recipient

The distributed ITC is eligible in the hands of the recipient unit to the extent permitted under Sections 16 and 17 of the CGST Act. The distribution by the ISD does not, by itself, override the restrictions under Section 17(5) (blocked credits). If the underlying service is ineligible for ITC in the hands of the recipient, the distributed credit cannot be availed by such recipient.

9.3 Treatment of Ineligible ITC

Rule 39 mandates that eligible and ineligible ITC must be distributed separately. This requires the ISD to undertake an eligibility analysis at the point of receipt of the invoice and classify the credit accordingly before distribution. Failure to make this distinction may result in the recipient units availing ineligible credit, attracting interest and penalty proceedings.

9.4 Excess Distribution

Rule 39 unequivocally prohibits the distribution of credit in excess of credit available with the ISD. Any excess distribution — even if inadvertent — would constitute wrong availment of ITC by the recipient. For demands pertaining to the period up to and including FY 2023-24, recovery may be initiated under Section 73 (non-fraud) or Section 74 (fraud, suppression or wilful misstatement) of the CGST Act. For demands pertaining to FY 2024-25 onwards — which encompasses ISD non-compliance from 1st April, 2025 — the applicable provision is Section 74A of the CGST Act (inserted by the Finance (No. 2) Act, 2024), which provides a unified time limit for issuance of demand notices and orders irrespective of the nature of the default.

X. KEY ISSUES AND PRACTICAL CHALLENGES

10.1 Identification of Common Services

The first practical challenge is determining which services qualify as “common input services” warranting ISD treatment. Services that are exclusively consumed by a single branch should not be routed through ISD — the relevant ITC must be directly attributed to the consuming branch by billing in its name. Only services consumed across multiple branches require ISD distribution.

10.2 Vendor Master Amendment

Upon obtaining ISD registration, the enterprise must notify all relevant vendors to issue future invoices against the ISD GSTIN. This requires amendment of vendor master data, update of purchase orders and service agreements, and coordination with vendor billing teams — a non-trivial operational exercise particularly for large enterprises with hundreds of common service vendors.

10.3 ERP and Accounting System Readiness

ERP systems need to be reconfigured to accommodate a separate ISD entity, ISD invoice generation, credit distribution entries, and reconciliation with GSTR-6A. The procurement module, financial accounting module, and indirect tax module must all be aligned with the ISD workflow.

10.4 Handling of State-Specific Invoices

A practical invoicing issue can arise in the following scenario: a vendor registered in State A supplies a service to a business whose ISD is registered in State B. Under the general place-of-supply rules for services supplied to a registered person, Section 12(2) of the IGST Act ordinarily fixes the place of supply at the location of the recipient — i.e., the State of the ISD’s registration. Where the place of supply is in a different State from the supplier’s location, the supply attracts IGST, not CGST + SGST of the supplier’s State. It is therefore incorrect to treat such a scenario as generating an entitlement to CGST + SGST of the supplier’s State in the ISD’s hands. The mismatch, where it occurs, is a consequence of incorrect invoicing under the general GST framework — specifically an error in applying the place-of-supply rules — and is not a restriction created by the ISD provisions themselves. Enterprises should ensure that vendors understand the applicable place-of-supply rules and issue invoices with the correct tax type, and should seek professional advice where the place-of-supply determination is not straightforward.

10.5 Transitional Challenges

Entities that were previously relying exclusively on cross-charge for third-party common services had to transition to the ISD framework by 1st April, 2025. Any cross-charge invoices issued after that date for third-party common services carry the risk of ITC denial for the recipient branches, pending further clarity on transitional treatment from the CBIC.

10.6 Ineligible ITC Identification and Distribution

The obligation to separately distribute ineligible ITC creates an additional compliance burden. For instance, if a common input service is used partly for construction of immovable property (blocked under Section 17(5)(d), other than plant and machinery) and partly for legitimate business use, the ISD must bifurcate and distribute the ineligible and eligible portions separately, requiring a prior apportionment exercise before issuance of ISD invoices. It may be noted that the Finance Act, 2025 has substituted the expression “plant or machinery” with “plant and machinery” in Section 17(5)(d) — this is now an enacted change, not a proposal — and the current official text of Section 17 reflects this substitution.

XI. ACTIONABLE COMPLIANCE CHECKLIST FOR FY 2025-26

| No. | Compliance Action | Statutory Reference |

| 1. | Obtain separate ISD registration in Form GST REG-01 (check Serial No. 14) for the relevant State. | Sections 24(viii) & 25, CGST Act; Rule 8, CGST Rules |

| 2. | Identify all common third-party input services and segregate exclusively attributable services from common services. | Section 2(61), Rule 39 |

| 3. | Amend vendor master and notify vendors to issue invoices against ISD GSTIN. | Rule 39, Rule 54(1) |

| 4. | Bifurcate eligible and ineligible ITC at invoice level; maintain supporting documentation. | Section 17, Rule 39(1) |

| 5. | Issue ISD invoices for each recipient each month; separately for CGST, SGST/UTGST, and IGST. | Rule 54(1), Rule 39 |

| 6. | Issue ISD credit notes for credit notes received from vendors; distribute proportionately. | Rule 39(1)(n) |

| 7. | File GSTR-6 by 13th of every succeeding month; file Nil return if no distribution. | Section 39, Rule 65 |

| 8. | Reconcile GSTR-6A (auto-populated inward supplies) with vendor invoices and ISD books. | Rule 36, Rule 39 |

| 9. | For RCM credit under Rule 39(1A), ensure the discharging entity transfers credit to ISD through prescribed invoice/debit note before distribution. | Rule 39(1A), Amended Section 2(61) |

| 10. | Update ERP systems for ISD entity maintenance, ISD invoice generation, and GSTR-6 reporting. | General Compliance |

| 11. | Train the finance and tax teams on the revised ISD framework, turnover ratio computation, and GSTR-6 filing. | General Compliance |

| 12. | Route all centrally received third-party common input service invoices (attributable to multiple GSTINs) through ISD from 1st April, 2025. Cross-charge remains applicable only for internally generated services and intra-group supplies not qualifying as ISD transactions. | Section 20, Rule 39; Circular No. 199/11/2023-GST |

XII. PENAL CONSEQUENCES OF NON-COMPLIANCE

Non-compliance with the mandatory ISD provisions from 1st April, 2025 may attract the following adverse consequences:

- Denial of ITC to the recipient branch, on the ground that the ITC was not distributed through the prescribed ISD mechanism, thereby constituting an irregular availing of credit under Section 16(2) of the CGST Act.

- Recovery proceedings under Section 73 (for non-fraud cases) or Section 74 (where fraud, suppression or wilful misstatement is alleged) for the period up to and including FY 2023-24. For the period FY 2024-25 onwards (which encompasses ISD non-compliance post 1st April, 2025), proceedings shall be governed by the newly inserted Section 74A of the CGST Act (inserted by Finance (No. 2) Act, 2024), which provides a unified time limit for issuance of demand notices irrespective of the nature of the default.

- Interest liability at 18% per annum under Section 50 of the CGST Act on wrongly availed ITC in the hands of recipients.

- Penalty under Section 122 of the CGST Act — up to Rs. 10,000 or an amount equivalent to the tax, whichever is higher — for taking or utilising ITC without actual receipt or in contravention of the provisions.

- Late fee under Section 47 of the CGST Act for delayed filing of GSTR-6 — reduced to Rs. 25/day under CGST and Rs. 25/day under SGST (Rs. 50/day aggregate) as per Notification No. 07/2018-Central Tax, subject to a maximum of Rs. 10,000 in aggregate.

XIII. CONCLUSION

The transformation of the ISD mechanism from an elective compliance tool to a mandatory statutory obligation marks one of the most structurally significant developments in the GST framework since its rollout in 2017. The amendments to Sections 2(61) and 20 of the CGST Act through the Finance Act (No. 1), 2024, the substitution of Rule 39 of the CGST Rules by Notification No. 12/2024-Central Tax, the appointment of 1st April, 2025 as the effective date for the Act amendments through Notification No. 16/2024-Central Tax, and the separate appointment of 1st April, 2025 for the Rule 39 amendments through Notification No. 09/2025-Central Tax dated 11th February, 2025, have collectively ushered in a paradigm shift in the manner in which multi-locational enterprises manage and distribute their Input Tax Credit in respect of common input services.

The inclusion of RCM invoices — both CGST-RCM under Section 9(3) and (4) and IGST-RCM under Section 5(3) and (4) of the IGST Act — within the ISD ambit, effective 1st April, 2025, represents a complete and mature legislative framework, closing a historically contentious gap in the law. The continued applicability of cross-charge to internally generated services and other intra-group supplies falling outside the mandatory ISD trigger ensures that the two mechanisms are clearly demarcated by the nature of the underlying supply, rather than by taxpayer preference.

For large corporate groups, particularly those having pan-India operations across dozens of GSTINs — such as diversified conglomerates with freight, logistics, supply chain, cold chain, and maritime divisions — the mandatory ISD framework calls for urgent and sustained attention to operational readiness, ERP reconfiguration, vendor communication, and monthly compliance discipline. The failure to transition timely carries not merely financial risk in the form of ITC denial and interest, but also reputational and litigation risks that may crystallise during GST audits and assessments.

In fine, the mandatory ISD mechanism is not merely a compliance obligation — it represents the legislative intent to ensure that each State receives its rightful share of GST revenues corresponding to the actual consumption of services within its jurisdiction, thereby preserving the federal fiscal architecture of GST. Enterprises would be well-advised to treat ISD compliance as an integral pillar of their GST governance framework.

XIV. SUMMARY OF KEY STATUTORY REFERENCES

| Provision | Subject Matter |

| Section 2(61), CGST Act | Definition of Input Service Distributor |

| Section 20, CGST Act | Manner of distribution of ITC by ISD (mandatory) |

| Section 24(viii), CGST Act | Compulsory registration for ISD |

| Section 16 & 17, CGST Act | Eligibility and apportionment of ITC (including blocked credits) |

| Rule 39, CGST Rules | Procedure, formula, and conditions for ITC distribution |

| Rule 39(1A), CGST Rules | Transfer of RCM credit to ISD |

| Rule 54(1), CGST Rules | Format and content of ISD invoice |

| Finance Act (No. 1), 2024 | Amendment to Sections 2(61) and 20 — ISD made mandatory; CGST-RCM invoices included in ISD scope |

| Finance Act, 2025 | Amendment to Sections 20(1) and 20(2) — IGST-RCM services under Section 5(3)/5(4) of IGST Act explicitly included; effective 1st April, 2025 |

| Notification No. 12/2024-CT | Substitution of Rule 39 — New ISD distribution procedure and formula (commencement separately notified) |

| Notification No. 16/2024-CT | Appointed 1st April, 2025 as effective date for Act amendments (Sections 2(61) and 20 of CGST Act) |

| Notification No. 09/2025-CT | Appointed 1st April, 2025 as commencement date for Rule 39 amendments (from Notification 12/2024-CT) |

| Circular No. 199/11/2023-GST | Clarification on ISD vs. Cross-Charge: both permissible pre-April 2025; ISD mandatory from 1st April, 2025 for third-party common input services |

| Note on Circular No. 225/19/2024-GST | This circular pertains to corporate guarantee valuation — it is NOT an ISD clarification circular and should not be cited in the ISD context |

| Section 47, CGST Act + Notification No. 07/2018-CT | Late fee for delayed GSTR-6: Rs. 25/day CGST + Rs. 25/day SGST (max Rs. 10,000 aggregate) as reduced from the standard Rs. 100/day per Act prescribed by Section 47 |

| Section 50, CGST Act | Interest on wrongly availed ITC |

| Section 73 & 74, CGST Act | Demand and penalty proceedings for ITC irregularities — applicable for periods up to FY 2023-24 |

| Section 74A, CGST Act | Unified demand proceedings for FY 2024-25 onwards (inserted by Finance (No. 2) Act, 2024) — applicable to ISD non-compliance from April 2025 onwards |

******

DISCLAIMER

This article has been prepared for the purposes of academic dissemination and professional guidance only. It is intended as a broad overview of the ISD mechanism under GST law as amended up to April 2026 and does not constitute legal advice. The provisions of the CGST Act, IGST Act, CGST Rules, notifications, and circulars are subject to further amendments, clarifications, and judicial interpretation. Readers are strongly advised to consult a qualified tax professional before taking any decision based on the contents hereof. The author and the publisher shall not be liable for any consequence arising from the use of this article.