The tab/ option Communicate with Taxpayers under GST login assuming far reaching significance from 01st January 2022. Now, this option would be widely used between the taxpayers.

2. With the de-implementation of Rule 36(4) of CGST rules for additional 105% of ITC claim by the recipient. Wef 01-01-2022; wherein the receiver can take the ITC benefit on reflection of GST Sales transaction in GSTR 1 of the Supplier and subsequently reflection in GST 2B of the receiver, GSTN takes a major step for smooth transition of the ITC from supplier to the recipient.

3. Dear Taxpayer, 07xxxxxxxxxxK1Z9, a notification has been received from 03xxxxxxxxxP1ZD XxxxxxCALS PVT. LTD.. Log on to GST Portal for details. GSTN

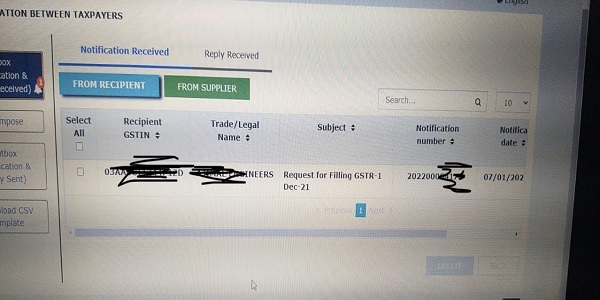

4. An option has been enabled wherein the Recipient can request the Supplier to file GST 1 so as to avail ITC benefit.

5. A notification number dated xx/xx/xxxx is received on the registered mobile number and e mail I’d of the recipient to make the supplier aware of the impending request by the recipient.

6. The supplier can take timely action on the basis of this notification and can ensure to file GST 1 within the deadline of 11th/13th of Next month so that the recipient can take timely ITC credit since the presumptive additional ITC of 5% has been curtailed wef 01st January 2022.

7. This innovative GSTN enabling can allocate a timely responsibility on the supplier if he fails to furnish his GST 1 or IFF within the due dates.

8. The recipient can claim to have the evidence/ basis on this notification, if the supplier still fails to furnish his GST returns in spite of this notification.

9. The recipient can withhold the GST tax payment to the tune of the GST charged, if the supplier fails to file his GST returns.

10. The recipient can have the basis, now to withhold the GST charged on the tax invoice and can release the GST amount only when it reflects in his GST 2B.

11. Pls find below the screenshot

12. Similarly, credit notes, debit notes request can be made by the supplier / recipient.

Sh. Jatin Ji. Pl correct point no 4., I think it should be like this ” An option has been enabled wherein the Recipient can request the Supplier to file GST 1 so as to avail ITC benefit.

Rightly marked Sir. It’s a Typing mistake.

Correction in Point 4th – recipient should request the supplier to file Gstr1.

How to handle EWB part when my supplier delivers goods on my behalf to my customers.