As per the provisions of Sec 54 of the CGST Act, 2017 read with Rule 89(4) of the CGST Rules, refund of ITC is allowed in case of zero rated supplies made without payment of tax under LUT. As per the formula given under this rule, refund amount is calculated as follows:

Refund Amount = (Turnover of zero-rated supply of goods + Turnover of zero-rated supply of services) x Net ITC ÷Adjusted Total Turnover

Where, –

(A) “Refund amount” means the maximum refund that is admissible;

(B) “Net ITC” means input tax credit availed on inputs and input services during the relevant period other than the input tax credit availed for which refund is claimed under sub-rules (4A) or (4B) or both;

(C) “Turnover of zero-rated supply of goods” means the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking or the value which is 1.5 times the value of like goods domestically supplied by the same or, similarly placed, supplier, as declared by the supplier, whichever is less, other than the turnover of supplies in respect of which refund is claimed under sub-rules (4A) or (4B) or both

In simple terms, if a taxpayer has 50% zero rated supplies in a month, he is entitled to refund of 50% of ‘Net ITC” availed on inputs and input services during the month. If the ITC availed on inputs and input services during the month is Rs 1,00,000/-, the taxpayer would be entitled to cash refund of Rs.50,000/-.

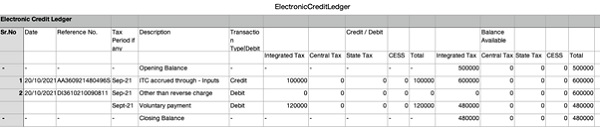

In the above example, let us assume if the taxpayer has availed ITC of Rs.1,00,000/- on inputs and input services, but he decided to reverse some ineligible credit of Rs.1,20,000/- pertaining to earlier period while filing GSTR 3B of current month. (no exports were made and no refund claims were filed in that period). The net ITC in GSTR 3B is shown as (-)20,000/-. The screen of Net ITC in GSTR 3B looks as under:

The entries in electronic credit ledger are posted as under:

In the above scenario, he cannot file any refund claim as the Net ITC auto populated in the refund application from the electronic credit ledger is shown as “0” and the portal does not allow him to proceed further.

Alternatively, if the taxpayer decides to reverse Rs.1,20,000/- through DRC 03, but not through GSTR 3B, the Net ITC availed in GSTR 3B would remain Rs.1,00,000/- and he will be in a position to claim refund of Rs.50,000/- as portal allows it. The entries in credit ledger are posted as under:

So, the question is whether the ‘Net ITC” for the purpose of Rule 89(4) is to be computed after reducing the reversal of any credit pertaining to previous period or only the credit availed during the month without reversal? There is nothing in Rule 89(4) to suggest that the Net ITC is after reversal of any ITC during the tax period, but as per GSTN, the Net ITC is arrived at only after reversals.

Finally, your refund eligibility depends on whether you decide to reverse any ineligible credit in GSTR 3B or reverse it separately through DRC 03. If you reverse through GSTR 3B, you don’t get any refund, but if you reverse it through DRC 03, you get refund. Welcome to tax administration with robust IT infrastructure.

Disclaimer – The views expressed are personal views of the author.

I have company where Inverted Refund and Export refund in same company.

for period 01-01-2024 to 30-06-2024 i have NET ITC 50 lakhs in that 35 lakhs Inverted ITC and 15 Lakhs Export ITC. I have claimed Inverted Refund for said period but when they add export turn over in Adjusted turnover so my actual Refund receivable reduce in big margin.

Now i tought it will be cover in export refund .

SO in export refund formula There is NET ITC means 50 lakhs i should take or 15 Lakhs ?

This is my main question

Sir,

Please confirm for computing “net ITC”, whether the reversal under Rule 42 to be excluded.

As there is no such mention in definition of “net ITC”.

Please guide,

Thanks

Yes. Reversal under Rule 42 has to be excluded as the value of exempt supplies is excluded to arrive at Adjusted total turnover ( denominator in the formula).