Case Law Details

Pankaj Enterprises Vs JCIT (ITAT Mumbai)

Held that as per the agreement there was only permissible possession given to the developer and the same cannot be treated as transferred under section 2(47)(4).

Facts-

The assessee is a partnership firm and during relevant years shown income under various heads including “income from house property” and “income from other sources”. The assessee disclosed LTCG of ₹21,08,973/- on the sale of development rights of a plot of land. The assessee treated total sale consideration on transfer of interest in Development Agreement (DA) based on the cost of constructed area at 42% of ₹5,46,27,440/- including ₹4,28,96,000/- for allowing loading of TDR, which was claimed as exempt.

AO held that taxability of the capital gain arises in AY 2009-10 as possession of the land was given to the developer in previous year corresponding to AY 2009-10. He rejected the computation of LTCG and assessed the same on protective basis. The assessment for AY 2009-10 was reopened. AO assessed capital gain at ₹9,37,03,413/- on substantive basis.

CIT(A) partly allowed the appeal by holding that capital gain is taxable in AY 2012-13 rather than AY 2009-10. Being aggrieved both assessee and revenue has preferred the present appeal.

Conclusion-

Held that it was clear from the agreement that possession was permissible possession and the developer was not authorised to exercise the right as owner thereof and enjoy such plot of land without interference on the part of the owner. In such circumstances, provisions of section 2(47)(4) are not attracted.

Hon’ble Supreme Court in the case of Seshasayee Steel (P) Ltd has held that permission is not possession under section 53A of the transfer of property Act.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

These appeals by the Revenue and the assessee and the cross-objection by the assessee are directed against two separate orders passed by the Ld. CIT(Appeals)-37, Mumbai [in short ‘the Ld. CIT(A)’] for assessment year 2012 -13 and 2009-10 respectively. Since the issue in dispute involved is common in both the assessment years, therefore these appeals and cross objection s have been heard together and disposed off by way of this consolidated order for convenience.

2. In these appeals, year of taxability on transfer of development rights in a plot of land as well as quantum of long-term capital gain thereon, have been disputed. The assessee offered the long-term capital gain on transfer of part interest in plot of land under development agreement in assessment year 2012 -13, whereas according to the Assessing Officer the transfer took place in previous year corresponding to assessment year 2009 -10 and therefore he has assessed the long-term capital gain on substantive basis in assessment year 2009 -10 and on protective basis in the assessment year 2012 -13. We find that assessment year 2012 -13 has been assessed first and thereafter assessment year 2009 -10 has reopened. The Ld. CIT(A) has also decided the issue in assessment year 2012-13 and therefore facts have been elaborated in assessment year 2012 -13, accordingly firstly, we are taking up the appeal and cross objection for assessment year 2012 -13 for adjudication. The grounds of the appeal of the Revenue in ITA No. 4876/Mum/2017 are reproduced as under:

1. On the facts and circumstances of the case and in law, the Ld. Commissioner of Income-tax(Appeals) has erred in not considering the fact that Sec. 2(47) (v) with Sec 53A of the Transfer of Property Act, 1882 clearly states that once ingress to the property is handed over to the transferee i.e. Vidhi Enterprises, the provisions of Sec 53A of Transfer of Property Act are attracted. In this case, clause 9B, 22(b) and 26 of the DA clearly establish that the Developer had complete access to the property and that he was liable for the actions thereon. Therefore, transfer has been effected in AY 2009 – 10 and not AY 2012-13.

2. On the facts and circumstances of the case and in law, the Ld. Commissioner of Income-tax(Appeals) has erred in not considering the fact the amount arrived at for calculating the consideration on registration of DA was based on the Stamp Duty paid which is a clear indication of the value attributed by the Land Revenue Department of the State Government at of Rs.18,74,74,699/- on transfer of the land and therefore the question of TDR

3. On the facts and circumstances of the case and in law, the Ld. Commissioner of Income-tax(Appeals) has erred in dividing the TDR /FSI and original plot bifurcation for the calculation of capital gains stating 50 C is not applicable on TR. However, the amount arrived at for calculating the consideration on registration of DA was based on the Stamp Duty paid which is a clear indication of the value attributed by the Land Revenue Department of the State Government at of Rs.18,74,74,699/- on transfer of the land and therefore the question of TR does not arise.

3. The sole ground raised in cross-objection by the assessee in CO No. 312/Mum/2018 in respect of the appeal of the Revenue has been withdrawn vide letter dated 15/06/22, therefore, same is dismissed as infructuous .

3.1 The assessee has also filed appeal separately for assessment year 2012-13 whi 3773/Mum/2017 and as under: has been registered as ITA No. the grounds raised in which are reproduced as under:

1. Ld. CIT(A) erred in holding that cost of construction of 42% of the area exchanged for transfer of appellant’s right under Development Agreement, being computed at 42% of Rs.18,74,74,699/- i.e. Rs.7,87, 73,911/-, without properly considering the components of cost of construction as determined by District Valuation Officer in its valuation report. Such cost of construction is consisting of:

| I | Cost of construction | ₹8,81,46,948/- |

| Ii | Incidental charges 10% of above | ₹88,14,695/- |

| Iii | Cost of TDR | ₹8,89,43,240/- |

| iv | Cost car to of 8 open parking be provided Development

Agreement

|

₹15,69,206/- |

| ₹18,74,74,089/- |

Ld. CIT(A) erred in not considering the fact that cost of construction is only ₹88146948/- and hence consideration under Development Agreement be computed with reference to said cost of construction being 42% there

2. Ld. CIT(A) erred in upholding disallowance of Rs.3,11,920/- out of interest paid by the appellant during the year on the plea that loan borrowed from ECL Finance Ltd is being utilised for improvement of house property to make it fit for earning rent in future, without properly appreciating the fact of the case and law applicable thereto.

3. Ld. CIT(A) erred in upholding the addition made by Ld. A.O. of Rs.1,30,000/- made u/s. 69C of the I.T. Act, without properly appreciating the fact that 3 payments amounting to Rs.- 1,30,000/ does not relate to the appellant, but to one of its partner Shri Suresh Patel and the said amount is not to be considered while making the assessment of the appellant.

4. The appellant pray that correct cost be determined for arriving at the consideration under Development Agreement and other additions made be deleted.

4. Briefly stated facts of the case are that the assessee is a partnership firm and during relevant year shown income under various heads including “income from house property” and “income from other sources”. The assessee filed return of income for the year under consideration on 28/07/2012 declaring total income at ₹8,21,584/- which was revised on 30/07/2012. The return of income was further revised on 23/03/2013 declaring total income at ₹ 29,30,557/-. The return of income filed by the assessee was selected for scrutiny and statutory notices under the Income-Tax Act, 1961 (in short ‘the Act’) were issued and complied with. During the year, the assessee disclosed long-term capital gain (LTCG) of ₹21,08,973/- on sale of development rights of a plot of land . The assessee treated total sale consideration on transfer of interest in Development Agreement ( 42% of ₹5,46,27,440/ DA) based on cost of constructed area at of TDR, which was claimed as exempt. The computation of capital gain of the assessee is reproduced as under:

| Particulars | Area (sq ft) | Amount (₹) |

| Total Land Areas held by the as on | 55,166 | |

| 01/04/1981 | ||

| The Fair Market Value as on 01/04/1981 | 24,82,493/ – | |

| Land (FSI) available for out of the above areas) and its FMV as on 01.04.1981 | 13,966 | 6,28,476/ – |

| TDR available (as per DCR 1991) | 51,067 | NIL |

| Total Area available for development | 65,033 | |

| Out of Land FSI of 13966 | 13,966 | |

| A. Parted to Developers (58%) | 8,100 | |

| B. FMV as on 01/04/1981 | 3,64,516 | |

| Indexed Cost (3,64,516/100*551) | 20,08,467 | |

| Land FSI to Assessee – (42%) | 5,866 | |

| Out of TDR (FSI) of 51067 | 51,067 | |

| Parted to Developer – (58%) | 29,619 | |

| TDR FSI to Assessee – (42%) | 21,448 | |

| Consideration amount received/receivable

by assessee being cost of areas |

5,866 | 1,17,31,440 |

| 2,000/- | ||

| On account of TDR cost of construction @ | 4,28,96,000 | |

| ₹2,000/- per sq ft | 5,46,27,440 | |

| Less : Consideration on account of TDR FSI | 4,28,96,000 | |

| Less : Indexed cost of land developer | 20,08,467 | |

| Less : Cost of Basement Demolition 8460 sq ft @ 900/- per sq ft | 76,14,000/- | 5,25,18,467 |

| Long Term Capital Gain liable for taxation | 21,08,973 |

4.1 However, in the scrutiny assessment completed under section 143(3) of the Act on 26/03/2015 , the Assessing Officer held that taxability of the capital gain arises in the assessment year 2009 -10.

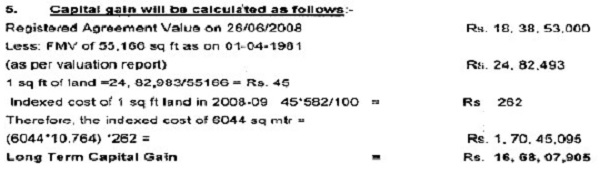

According to him, under the registered development agreement, possession of land was given to the developer in previous year corresponding to AY 2009 -10 and therefore in terms of section 2(47) of the Act read with section 53A of Transfer of Property Act, the capital gain arises in AY 2009-10. He also rejected the computation of LTCG i.e. the sale consideration and cost of acquisition and computed the quantum of LTC G at ₹ 16,68,07,905/-based on stamp duty value of ₹18,38,53,000/- and assessed the same on protective basis. The computation of capital gain by the Ld . AO for AY 2012-13 (on protective basis) is reproduced as under:

4.2 The Ld. AO also made addition of ₹1,30,000/- for unexplained expenditure based on the documents found during the course of the survey carried on 21/11/2012 at the premises of the assessee firm. The ld. Assessing Officer also made disallowance of interest paid on loan amounting to ₹15,06, 920/-as loans not used for the purpose of the business and interest was paid to family members.

4.3 The assessment for AY 2009 -10 was reopened. As the valuation of stamp value authorities was objected by the assessee, matter of valuation was referred by the AO to District Valuation Officer (DVO), who valued the interest of the assessee in DA at ₹10,01,28,000/-. The AO accordingly, assessed the capital gain at ₹9,37,03,413/- on substantive basis. The computation of capital gain by the AO in para 8.6 of the assessment order for AY 2009 -10, is reproduced as under:

| Registered Agreement Value on 26.06.2008 | ₹18,38,53,000 | |

| Value of Development agreement in view of

valuation report dated 29.01.2016 |

10,01,28,000 | |

| Indexed cost of land to Developer Cost of basement demolished (58%) | ₹20,08,467 | |

| ₹44,16,120 | ||

| Long Term Capital Gains | ₹9,37,03,413/- |

5. The Ld CIT(A) held that capital gain is taxable in AY 2012 -13 rather than in AY 2009 -10. He held that capital gain is chargeable on the cost of construction as contained in the report of the DVO at ₹18,74,74,089/-, being 42% thereof ₹7,87,73,911/ – and consideration relatable to load ing TDR will not be liable to capital gain. For AY 2009 -10 held that capital gain was taxed on substantiative basis in AY 2 012-13, so no separate adjudication was required in AY 2009-10.

6. Aggrieved, both the assessee and Revenue are in appeal before us. During the course of the hearing both sides have filed paperbook and written submissions and made oral arguments.

7. The ground No. 1 of the appeal of the Revenue relates to the year of the taxability of the capital gain. In support of the grounds Revenue has submitted that the developer was given complete access to the property in the previous year corresponding to assessment year 2009 -10 and therefore the capital gain was liable to be taxed in the assessment year 2009-10.

7.1 The facts in relation to the issue in dispute have been mentioned elaborately by the Assessing Officer. For understanding the issue, brief as how the property came into existence and then transferred to the developer, are summarized as under:

(i) Mr. Jethabhai G Shah was carrying business in the name and style of M/s Pankaj enterprise. He was absolute owner of plot No. one of industrial subdivision of survey No. one and two ad measuring 5127.36 m2. M/s Pankaj enterprise was granted exemption in the year 1979 for industrial use of the said property.

(ii) In the year 1980, Mr . Jethabhai entered into an agreement with M/s Master Clock and watch works P Ltd ( in short ‘the Master clock’) for forming a partnership, wherein Mr. Jethabhai agreed to bring said property as his capital contribution and the master clock to bring monetary capital, which will be required for carrying on the partnership business of M/S Pankaj enterprises. On the execution of the agreement, the said property became the asset and property of partnership firm M/s Pankaj enterprises.

(iii) Subsequent to that by way of different deeds of partnership and deeds of retirement several changes made in the Constitution of the firm from time to time. Accordingly in terms of the last such deed of reconstitution of the partnership dated 03/04/2007, the present partners of the partnership firm are the Master clock, Mr. Suresh Ishwarlal Patel and Mr . Nirmal Suresh Patel.

(iv) Out of the total plot area of 5127.05 m2, the land area of 381.14 m2 was under encroachment by illegal occupants and 10% of the area (512.70 m2 ) was to be left open i.e. amenity space, and thus the net plot area available for construction of the said property was 4233.21 m2.

(v) The assessee firm des ired to construct an industrial estate on the said property and after obtaining approval in the year 1995 from the competent authorities, commenced construction of industrial building on the said property divided into “Wing A” and “Wing B”. The Wing A was built partially comprising of a basement having net floor area of 8460.80 ft2. This portion of Wing A which was under construction and not occupied, was assessed as land under construction under Municipal Ward. The Wing B was complete with ground and two upper floors and occupation certificate was issued in 1999.

(vi) The partnership firm desire d to construct and develop information technology park on Wing A admeasuring plot area having FSI of 6044.1 m2, which was worked out as under:

| Plot Area | Sq Mtr |

| Total Plot Area | 5127.05 |

| Less: Area under encroachment | 381.14 |

| Less: Amenity Space | 512.70 |

| Net Plot Area | 4233.21 |

| Total Permissible FSI | 8979.21 |

| Less: FSI Consumed in Wing B which is retained by the Owners | 2935.00 |

| Balance Plot including FSI | 6044.21 |

(vii) Thereafter, the assessee i.e. owner of the land, entered into an agreement With M/s V idhi Enterprises i.e. Developer, for development of the plot wherein they agreed to share the constructed property in the ratio of 42:58 i.e. the owners will get 42% share of the constructed property free of cost. This agreement was entered into in the financial year 2007 -08, but was registered in the financial year 2008 -09.

(viii) the assessee obtained possession of its share of constructed property in the previous year corresponding to assessment year 2012 -13. According to the assessee in view of the possession of the property received in assessment year 2012 -13, the long-term capital gain arose in the case of the assessee in assessment year 2012 – 13 and offered accordingly.

8. In background of the above facts, the Assessing Officer held that long-term capital gain on transfer of development rights should be charged on the basis of the registered development agreement entered into between the assessee i.e. the owner and M/s Vidhi enterprise i.e. developer , in the financial year 2008 -09 i.e. the assessment year 2009 -10. The relevant finding of the Ld. Assessing Officer is reproduced as under:

“Year of Chargeability

The assessee in the course of hearing has stated that agreement was executed in the FY 2007-08 and hence the chargeability year should be FY 2007-08 relevant to AY 2008-09.

The contention of the assessee is not acceptable as provisions of section 53A of Transfer of Property Act was amended in the year 2001 by which additional condition of registration of the written agreement was introduced and in the instant case the agreement was registered in the FY 2008-09 and therefore, the chargeability should be FY 2008-09 relevant to AY 2009-10. Long-term Capital Gain on transfer of development rights should be charged on the basis of registered agreement entered into between Pankaj Enterprises i.e. the Owner and M/s Vidhi Enterprises in the FY 2008-09 i.e. AY 2009-10 as the year of chargeability of income.

Under Section 2(47) (v),any transaction involving allowing of possession to be taken over or retained in part performance of a contract of the nature referred to in Section 53A of the Transfer of Property Act would core within the ambit of Section 2(47)(v). That, in order to attract Section 53A,the following conditions needs to be fulfilled There should be a contract for consideration; it should be in writing; it should be signed by the transferor; it should pertain to transfer of immovable property; the transferee should have taken the possession of the property lastly, the transferee should be ready and willing to perform his part of the contract. That even arrangements confirming privileges of ownership without transfer of title could fall under Section 2(47) (v).Section 2(47) (v) was introduced in the Act from the assessment year 1988-89 because prior thereto, in most cases, it was argued on behalf of the assessee that no transfer took place till execution of the conveyance. Consequently, the assessee used to enter into agreements for developing properties with the builders and under the arrangement with the builders, they used to confer privileges of ownership without executing conveyance and to plug that loophole, Section 2(47) (v) came to be introduced in the Act.

The scope of Section 2(47) (v) reads as under:

“2(47)…

(v)(With effect from April 1,1988) any transaction involving the allowing of the possession of any immovable property (as defined) to be taken o r retained in part performance of a contract of the nature referred to in Section 53A of the Transfer of Property Act, 1882.

(vi) (With effect from April 1, 1988) any transaction (whether by way of becoming a memberof, or acquiring shares in, a co-operative society ,company or other association of persons or by way of any agreement or any arrangement or in any other manner whatsoever; which has the effect of transferring or enabling the enjoyment of, any immovable property(as defined).”

The above two clauses were introduced with effect from April 1, 1988. They provide that “transfer” includes ()any transaction which allows possession to be taken/retained in part performance of a contract of the nature referred to in section 53A of the Transfer of Property Act, and(in)any transaction entered into any manner which has the effect of transferring or enabling the enjoyment of any immovable property. Therefore, in these two cases, capital gains would be taxable in the year in which such transactions are entered into, even if the transfer of immovable property is not effective or complete under the general law.

The assessee in its submission has stated that no rights are being transferred to developers till such time entire building is constructed as per the terms of the Development Agreement.

The department would like to state that transfer of developmental rights had taken place and Sec 2(47) would be applicable and to further corroborate our point, the extracted portion of the agreement is placed below:

Point No 9B of the Agreement states: The developers shall be liable to remove, settle all legitimate defects, claims to the said property or any part thereof received from any person lawfully claiming from the owners at any time till the entire development project is completed within a period of 30 days of it becoming known.

Point No. 22 (b) of the agreement states: The Developers shall be fully responsible for any contravention, violation, non-compliance of any laws, rules, regulations, terms of sanction/approvals and for all aspects of the development of the said new building and the Owners will in no way or manner be concerned or be made a party to any such contravention, violation/non-compliance or default even if the Developers commits any irregularities and/or defaults/violation in respect thereof. The Developers shall in this respect keep the owners full and effectually indemnified.

Point No. 26 of the agreement states: The aforesaid consideration being Owners Area is all inclusive consideration for grant of development rights to the Developers in the manner envisaged herein in respect of the said property and nothing further shall be due and payable by the Developers towards the Developers Area and/or the conveyance of the said property in favour of the common organization to be formed of all the premises purchasers.”

9. Before the Ld. CIT(A), the assessee contested the finding of the Ld. Assessing Officer on the ground that in assessment year 2009 – 10, only permissive possession was given to the developer for carrying out acts and deeds, which was necessary for development of the said property and no possession of the property was given. The construction of the property was completed only in financial year 2011-12 and therefore exchange/barter of the property happened only in the previous year corresponding to the assessment year 2012 -13. Hence, the long-term capital gain was taxable in the assessment year 2012 -13.

9.1 Ld. CIT(A) after considering various clauses of the development agreement , and power of attorney executed between the assessee and the developer, which was registered on 26/06/2008, concluded that there is no transfer of property in the assessment year 2009 -10, within the meaning of section 2(47) of the Act and the assessee received 42% of the total constructed area in assessment year 2012 -13 i.e. in which the exchange took place , therefore capital gain has to be taxed in the assessment year 2012 – 13. The relevant finding of the Ld. CIT(A) is reproduced as under:

“5.16 I have gone through the development agreement and find that Clauses 14, 16, 24(c), 24(A), the provision of these clauses are reproduced here below:-

(i.) CI. 14 of the agreement provides “developer shall be deemed to have been allowed to enter upon the said property as developers for the purpose of construction of said new building thereon in accordance with plan to be sanction with amendment thereto if any, by the Municipal Corporation of Greater Mumbai”. The developer is allowed 10 construct a temporary site-office (CI. 14(in). The developer is also permitted to put hoarding/sign boards (CH 14(iii).

(ii) Cl. 16 provides for execution of power of authority infavour of developer. Clause 16 “‘immediately upon execution of presents persons the owners have granted in favour of developer or their nominees, an irrevocable power of attorney to do all acts deeds, matters and things as necessary for development of said property and which power of attorney shall be registered simultaneously with this development agreement”

(iii) CI. 24 (c) provides “the developers shall be entitled to put the purchaser of the developer’s area, in possession of the respective premises as and & when occupation certificate in respect of the said new building is obtained by developers, provided however, the developer shall not handover possession of developer’s area to anybody or allow or use the premises in the developers area on any basis whatsoever, unless and until the developers shall have offered to the owner, the owner’s area duly completed in all respect and contemplated herein in writing and IS days have elapsed.

(iv) C1. 24(A) run as “Immediately upon the owners being offered possession of the owner’s area, owner shall execute an irrevocable power of authority in favour of developers and/or their nominees to execute the vesting documents/declaration under Maharashtra Apartment Ownership act”.

5.17 I have also gone through the details of the power of attorney executed by the appellant in favour of the builder and the same was registered on 26/06/08. Broadly speaking, it turns out that power of attorney authorizes the builder to do the following:-

(a) To carry out development work on the said property including construction and completion of building (C1.2)

(b) To represent the appellant before all gov- ernment/semi government revenue, local or other bodies in relation to development of the said property (C1.6)

(c) To file necessary application to Municipal Corporation of Bombay, Development Control Board and to prepare development plan and any amendment thereto, to approach the executive engineer and to obtain IOD and CC, to appoint Architect to fuifill the condition of commencement certificate (cl.9).

(d) To obtain the necessary FSI, right by way. TDR of other property and utilise for the purpose of construction (cl. 12).

(e) To represent before the Ministry of Commerce and other departments of Industrial Policy & Promotion (Cl.13).

(f) To apply to Municipality for water supply, city survey officer and to obtain the required sanctions and confirmation under Environment Act, pollution Act, Aviation authority.

(g) Under C1.31, the developer is allowed to sale on ownership basis or to grant lease on leave & license, out of his potion of construction area, subject to conditions under the development agreement.

5.18 It is clear from above facts and judicial decisions that in case of development agreement, if the developer is merely allowed to enter the property for the construction of the building, it cannot be deemed to be a possession for the purposes of Section 2(47) r.w.s. 53A of Transfer of Property Act. The terms and conditions of the development agreement between the appellant and M/s. Vidhi Enterprises clearly indicate that only a permissive possession for the construction work was handed over to the developer, the developer was never enjoying rights of ownership over the land as is evident from the fact that the developer is not entitled to transfer/sale his portion of developed area. It can be safely held that possession of land was not handed over to the builder in F.Y. 2008-09. The construction was completed in terms of development agreement only in F.Y.2011 -12 and the exchange of property between the appellant and the developer took place in that financial year 2011 – 12. The sum and substance can be summarized in following words:-

(a) That the capital assets was converted into stock-in -trade on 01/04/07

(b) That the development agreement was entered into on 17/04/07 and development agreeme nt was registered on 26.06.08.

(c) That neither provision of development agreement nor of the power of attorney has given right of possession to the developer. The builder is only entitled to enter and do all the necessary construction.

(d) The right to enter for necessary construction only amount to permissive possession.

(e) The appellant’s interest in plot of land is exchanged for constructed area in the AY 2012-13.

5.19 After considering the totality of facts, rival submissions, the applicable law and on the basis of discussion mentioned above, I find force in the argument of the appellant. I am of the clear opinion that no income accrues in A.Y. 2009 -10 as there is no transfer within the meaning of Section 2(47) of I.T Act as no possession has been given in terms of Section 53A of Transfer of Property Act. The appellant received 42% of the total area constructed by builder in financial year relevant to AY. 2012-13 i.e. the year in which exchange took place. Therefore, capital gains cannot be taxed in A.Y. 2009-10 and has to be taxed in A.Y. 2012 -13. In terms of these findings, Ground Nos. 1 to 3 are hereby allowed.”

10. We have heard rival submission of the parties on the issue in dispute and perused the relevant material on record. The assessee has by way of registered deed of conveyance, which was entered into in FY 2008-09 (i.e. corresponding to assessment year 2009-10), for developing its plot of land into an industrial estate as per the maps/floor approved by the competent authority. The said industrial estate got constructed in financial year corresponding to assessment year 2012 -13 i.e. the year under consideration. The dispute between the parties is regarding the year of taxability of capital gain. According to the assessee it is liable to be taxed in assessment year 2012 -13, but according to the Revenue the capital gain is liable to be taxed in assessment year 2009 -10. According to the Assessing Officer transfer of development right took place under section 2 (47) of the Act on the date of development agreement. The department relied upon clause No. 9B, 22(b) and clause no.26 of the development agreement. The said clauses of the agreement have been reproduced by the AO in his order, which we have extracted above. It is the contention of the revenue that while part performance of the agreement, possession was handed over to the developer and therefore it amounted to transfer in terms of section 2(47)(4) of the Act. Before us, it is the contention of the Ld. Counsel of the assessee that only permissible ingress was provided for carrying out construction and no ownership rights were transferred under the development agreement dated 02/04/2006, which was registered on 26/06/2008. The assessee relied on the clauses quoted by the Ld. CIT(A) in para 5.16 of the impugned order. It was further submitted that in terms of development agreement, a general power of attorney was executed which was also registered on 26/06/2008 and relevant clauses which have been referred by the Ld. CIT(A) in para 5.17 of the impugned order, which we have extracted above.

10.1 The Ld. counsel in support of the proposition that mere ingress being allowed for carrying development on plot of land is not handing over possession within the meaning of section 2(47) of the Act, and hence, no transfer, relied on following decisions:

1. CS Atwal Vs CIT 378 ITR 244 ( P &H)

2. Binjusari Properties P Ltd. Vs ACIT 164 TTJ 417 (Hyedearbad)

3. Dilip Anand Vazirani Vs ITO 167 TTJ 194(Bom)

4. Shri Sadia Shaikh Tax Appeal No. 11 of 2013 dated 02/12/13 ( Karnataka)

5. Balveer Singh Maini 398 ITR 531 (SC)

6. Faradin Khan 304 CTR 299 (Bom)

10.2 In the case of CS Atwal (supra), Hon’ble High Court observed legislative intent behind incorporating clause (v) to section 2(47) of the Act. The relevant part of the observation of the Hon’ble High Court is reproduced as under:

“The legislative intent behind incorporating clause (v) to Section 2(47) of the Act from assessment year 1988-89 as discernible from CBDT circular is to embrace within its ambit those transactions of sale of property where assessee enters into agreements for developing properties with builders and the seller confers the rights and privileges of ownership to the buyer without executing/registering a formal conveyance deed in order to avoid capital gains tax. In order to thwart such tendencies, transactions where the possession is given or allowed to be retained in part performance of contract of the nature referred to in Section 53A of 1882 Act is held to be “transfer” by fiction of law though under general law it would not be considered to be “transfer”. In other words, by deeming fiction, “transfer” is assigned extended meaning for taxation purposes by incorporating and including that where possession of any immovable property is taken or GURBAX SINGH 2015.07.23 15:30 I attest to the accuracy and integrity of this document High Court Chandigarh retained in part performance of a contract of the nature referred to in Section 53A of 1882 Act. ”

10.3 The Tribunal in the case of Binusaria properties Private Limited (supra), held as under:

“In the present case, admittedly, what has been executed by the assessee is a ‘Development Agreement-cum-General Power of Attorney’. A reading of the said agreement indicates that what was handed over by the assessee to the developer is only a ‘permissive possession’. Clause 5 of the said agreement dated 2nd February, 2006, on page 3 thereof, specifically provides that ‘First party on signing of this agreement has permitted the developer to develop the scheduled land’ (emphasis added). As per Clause 9 of the said agreement, consideration receivable by the assessee from the developer is ‘38% of the residential part of the developed area’ (which was later reduced to 33%, by virtue of a supplementary agreement executed on 18.10.2007). That being so, it is only upon receipt of such consideration in the form of developed area by the assessee in terms of the development agreement, the capital gains becomes assessable in the hands of the assessee. We are supported in this behalf by the decision of the Third Member Bench of the Tribunal in the case of Vijaya Productions Pvt. Ltd. V/s. Addl. CIT (134 ITD 19).”

10.4 In the case of Dilip Anand Vazirani (supra) , the Tribunal held as under:

“Thus, ITAT had noticed that the Assessee had received advance amounts much earlier to the execution of development agreement, probably on the strength of the MOU. The property was encumbered with tenancy rights of many persons and the release of tenancy right was completed only in January, 2005. Further, the approval from municipal corporation was also got delayed and the plans were revised subsequent to AY 2000 -01. The surrounding circumstances show that the developer does not started the work of development in the year relevant to AY 2001-02. As per the terms of development agreement, the Assessee had given only license to enter into the property, meaning thereby the possession was not given in the year relevant to AY 2001-02. In view of the peculiar facts narrated above, the Assessee had contended that the tax authorities was not correct in holding that the transfer of property took place in the year relevant to AY 2001-02. The various case laws discussed above also support the view taken by the Assessee. Hence, TAT agreed with the contentions of the Assessee in this regard.

Accordingly, ITAT hold that the transfer of property does not took place on the date of executionof development agreement”.

10.5 In the case of Saida Shaikh (supra), the Hon’ble High court observed as under:

“‘It can thus be seen that Commissioner of Income Tax (Appeals) as well as the learned Tribunal upon basis of the factual material placed before it and upon interpretation of the agreement entered between the assessee and the developer has found that the assessee was liable to pay capital gain in the year 2008-09, in as much as there was no possession handed over to the developer under Section 53A of the Transfer of Property Act in the assessment year 2003 – 04.”

10.6 In the case of Fardin Khan (supra), where the Hon’ble High Court has also considered Balveer Singh Maini (supra), the assessee entered into development agreement with Godrej properties Ltd. on 20 th April, 2007 and paid ₹13.75 crore as deposit, and further to receive ₹550,000,030 percent of the sale proceeds. This agreement was not registered and a general power of attorney was given. The possession of property was given to developer for a specific purpose to develop the property. The Hon’ble High Court, dismissing the appeal of the Revenue held that possession of the property was given to the developer for a specific purpose to develop the property. The amount received was shown as deposit. The Hon’ble High Court observed that the agreement makes it clear that Godrej properties Ltd. has been granted license to enter upon and develop the property and possession of the land continued with the assessee. Further, the development agreement provided that nothing contained in the agreement shall be construed as grant of possession in part performance of the agreement under section 2 (47)(v) and 2(47)(vi) of the Act. The Hon’ble High Court held that tax ability of the capital gain will be examined the year in which the transfer of the land as a stock in trade has taken place.

10.7 Thus the dispute precipitated before us is to whether possession of plot of land was handed over to the developer within the meaning of section 53A of the Transfer of Property Act, at the time of entering the DA or possession was handed over at the time of completion of construction of the property.

10.8 The clause 2 of the development agreement provided that subject to retention of FSI retained by the owner, the owner appoint developer for construction and development of the said plot. The clause 5 provides for consideration which will be 42% constructed area, including loading of TDR, in lieu of constructed area retained by the developer, which will be 58% along with 58% land area. Further, clause 14(1) has provided that “developer shall be deemed to have been allowed to enter upon the said property developer for the purpose of the construction o f the said new building thereon”. The developer was specifically allowed to construct a temporary site office only. Further, clause 24C provided that developer shall not give possession to any of the party to whom he allotted any areas out of the developer shares, without first giving possession of owners area to owners and the developer was allowed to give possession only after 15 days thereof . Under the power of au thority also authorisation was given only for facilitation of the construction activity to the developer and no authority was given to exercise rights as owner of the land.

10.9 In view of the various clauses of the development agreement, it transpires that possession was given merely for carrying out construction work on the plot of land i.e. the permissible possession and the developer was not authorised to exercise the right as owner thereof and enjoy such plot of land without interference on the part of the owner. In such circumstances, provisions of section 2(47)(4) are not attracted in the case of the assessee.

10.10 Further we find that in the case of Infinity Infotech Parks Ltd 407 ITR 137( Cal), also possession of the land was given to the developer for construction, wherein the agreement envisaged that developer would construct upon the land and in lieu of such work undertaken by the developer, the developer would be entitled to retain 61% of the land and the proportionate constructed area while the balance 39% of the land together with construction thereon would belong to the assessee i.e . owner of land. In the facts of the above case, Hon’ble High Court held as under:

“There could be rare situations where the transfer may be simultaneous with the execution of the agreement, but where the owner retains any right in the constructed area that may come up in future, it would scarcely be a case of a transfer taking place at the time of the execution of the agreement. The matter may be viewed from another perspective. Merely because de facto possession of the land is made over to a mason or a civil engineer for the purpose of making a construction thereon, it would not imply that possession is made over to the mason or the civil engineer for their enjoyment of the property. Such persons would be in de facto possession under the de jure possession of the owner and only for the purpose of undertaking the construction at the land in question.

Till such time that the construction came up and 39% of the constructed area was made over to the assessee, it could not be said that possession of the balance land, in the sense that the expression carries in Section 2(47)(v) of the Act, had been made over by the assessee to the developer.

It is true that the developer could have retained possession of the land and declined to return possession thereof to the assessee since the developer was in physical control thereof. But such resistance of the developer would not have been protected under Section 53A of the Act of 1882. It was only after the apportionment of the areas upon the construction on the land being completed that the developer could have rightfully retained possession of the developer’s 61% share and resisted dispossession by discharging his obligation under the agreement and seeking refuge in terms of Section 53A of the Act of 1882 despite the formal conve eyanc pertaining to the developer’s entitlement not having being executed. In any view of the matter, the right of the developer to retain possession and protect such possession under Section 53A of the Act of 1882 could never have arisen prior to the construction being completed and the apportionment effected.”

10.11 Further we find that Hon’ble Supreme Court in the case of Seshasayee Steel (P ) Ltd. 115 Taxman.com 5 (SC) considered a development agreement granting permission to start advertising, selling and construction and permitted to execute sale agreements to developer. The Hon’ble court held that such permission is not possession under section 53A of the transfer of property Act. In para 14 the Hon’ble court held that “ possession within meaning of section 53A, which is a legal concept and which denotes control over the land and not actual physical occupation of the land. This being the case, the section 53 of the Transfer of Property Act cannot possibly be attracted.

10.12 Respectfully following the finding of the Hon’ble Supreme Court and other High Court, we hold that the capital asset of the assessee cannot be treated as transferred under section 2(47)(4) of the Act read with section 53A of the Transfer of Property Act in assessment year 2009 -10. We do not find any error in the finding of the Ld. CIT(A) on the issue in dispute and accordingly, we uphold the same as far as the year of taxability of capital gain is concerned. The ground no. 1 of the appe al of the Revenue is accordingly dismissed.

11. Now we come to the second issue of quantum of the capital gain to be taxed in the hand of the assessee , which has been raised by the revenue in ground No. 2 and 3 of the appeal as well as raised by the assessee in ground No. 1 of its appeal.

12. The assessee in its computation of long-term capital gain has treated the consideration received in the form of constructed area to the extent relatable to loading of TDR a s not taxable. The Ld. Assessing Officer however considered it to be a taxable item. The Ld. CIT(A) in para 6.8 of the impugned order following the decision of the Tribunal in the case of Voltas Ltd (supra) has held that provisions of section 50C are not applicable on transfer of development rights. The said finding of the Ld CIT(A) is reproduced as under :

“6.8 Recently the Hon’ble ITAT in the case of Voltas Ltd. ITA No.5330/Mum/2009 ITA No.5331 of 2009 vide dated 16 -09 -2016 is held that Section 50C be applicable to a transfer by assessee of capital assets being “land or building” or both. Capital assets transferred by assessee being development rights “in land” and “not the land”, the provisions of Section 50C is inapplicable for said conclusion. Reliance has been placed on Section 269UA by Hon’ble ITAT. Under the said provisions “rights in land and building” was specifically included, as such, “right in land and building” have been cleariy understood and treated as independent of “land and building”. The Tribunal finally held that “rights in land or building” will not be covered u/s.50C. ”

12.1 Further in para, Para 6.9 of the impugned order, the Ld. CIT(A) has held the consideration corresponding to allowing loading of TDR as not taxable. The relevant finding of the Ld. CIT(A) is reproduced as under:

“6.9 After considering the totality of facts, rival submissions, the applicable law and on the basis of discussion mentioned above, I find force in the argument of the appellant and draw strength from the various decision given by the judicial High Court especially Bombay High Court decision in the case of Sambhaji Co-operative Housing Ltd and decision of Mumbai Tribunal ir the caseof Voltas Ltd. ITA No.5330/Mum/2009 ITA No.5331 of 2009 on identical facts. The provisions of section 50C are deeming provisions. It is settled law and well accepted rule of interpretation that deeming provisions are to be construed strictly. Thus, while interpreting deemirg provisions neither any words can be added nor deleted from language used expressly. In view of the above referred decision of jurisdictional High Court, I hold that consideration received in the form of constructed area to the extent relatable to loading TDR is not taxable.”

12.2 The amount of full value of consideration has been taken by the Assessing Officer in assessment year 2012-13 i.e. year under stamp value authorities at ₹18,38, 53,000/-. Subsequently, the Assessing Officer in assessment year 2009 -10 referred the matter to the Ld. DVO and on the basis of his valuation report full value of consideration has been taken at ₹10,01, 28,000/- as per valuation report dated 29/01/2016, on substantive basis.

13. Before the Ld. CIT(A) , the assessee contested for taking 42% of the value of the constructed area for determination of cost of consideration. The assessee relied on various decisions. After considering the decisions, the Ld. CIT(A) determined full value of consideration as 42% of the cost of construction of the area exchanged. The Ld. CIT(A) observed that cost of construction on the basis of the valuation report of the DVO is ₹18,74,74, 699/-and therefore 42% of said amount works out to ₹7,87,73, 911/-. The Ld. CIT(A) accordingly directed the assessee to compute the capital gain after excluding the consideration relatable to loading of the TDR. The relevant finding of the Ld. CIT(A) is reproduced as under:

“7.1 The Delhi ITAT in the case of Vasavi Pratapchand vs. DCIT 90 TTJ has discussed the identical issue. The facts of the case are that assessee in this case was owning a plot of land admeasuring 2.85 acre in Delhi. Assessee entered into a development agreement with the builder under which assessee got 56% of the total constructed area as his share against 44% of the land transferred. The question for consideration was how the consideration for 44% of the assessee’s interest in land be calculated. The Bench held in para 9:-

“As far as consideration part is concerned, we are of the view that value of 44 per cent of land was equal to the cost of construction of 56 per cent built up area. The sale consideration to the seller and cost of acquisition to the buyer are two sides of the same coin. Both the parties to the agreement knew as to what was being transferred and what was being received. In the case of exchange, the price of both the assets would be the same. So, when the assessees had agreed to transfer 44 per cent of land, it must have kept in mind the value of construction of 56 per cent of built up area. Therefore, we are of the considered opinion that consideration for the transfer of 44 per cent land was the cost of construction of 56 per cent built up area which was to be incurred by the builder. This very sum would also amount to investment by assessee in the construction of flats and, therefore, the cost of construction of the flats by the builder would also amount to the cost of acquisition of the flats by assessees.

7.2 In case of CIT vs. Jai Trikanand Rao – 60 SOT 0189(Mumbai). The Bombay ITAT also considered a similar issue. In this case, assessee was owning a plot of land and entered into a development agreement as per which the developer was to bear the cost of demolition of old structure and construction of the building and in view thereof the developer agreed to give 50% of the constructed area in the form of flats in the building. Under development agreement, a interest free security deposit was given of Rs.1 crore to the assessee which was refundable after giving possession of the constructed area to the assessee on completion of the building, total constructed area came to Rs.2166.2 Sq. Meter out of which assessee got constructed area of Rs.1082.7 Sq. Meter in the forrn of flat. Assessee sold certain flats out of such area received. Question for consideration was how to compute taxable income on sale of flats and development agreement. The Bench held. in para 11.

“Now coming to the matter in controversy before us, as observed above, the 50% of the market value of the total land in question together with value of additional FSI, if any, on the date of agreement would be deemed to be the cost of construction of the constructed area which falls in the share of the assessee as per the development agreement. Assessee thus is entitled 10 proportionately claim deduction for cost of construction while faxing capital gains arrived from the sale of two fats.”

7.3 In case of CIT vs. Khivraj Motors 380 ITF. 215(Karnataka). In this case assessee was occupying the premises as tenant, taken on lease for a long period and agreed to vacate in consideration of undivided interest in property and constructed area for 65 years of lease under agreement, the cost of construction was specified at Rs.800 Per Square Feet and hence consideration for Rs.22100 Square Feet constructed area received by assessee was taken at Rs.17,68,800. The Assessing Officer, in principle, accepted the cost of construction as consideration, but on receiving information from the developer who informed to have incurred the construction cost of Rs.19,42,79,237/-, calculated cost of construction accordingly. The court held that cost of construction as per agreement on the date of development agreement be adopted. Thus on principle, the High Court of Karnataka adopted consideration as cost of construction.

7.4 I have duly considered the judicial authorities and have no hesitation in holding that consideration under development agreement to be decided based on cost of construction area as consideration under development agreement. The consideration for calculation of capital gain to be computed based on cost of construction of area received by appellant under agreement. A reference to the valuation report of DVO clearly reflects that cost of construction is at Rs.18,74,74,699/-. Hence, 42% of the cost of construction of the area exchanged be adopted at Rs.7,87,-. 73,911/ Accordingly, it is held that consideration received by appellant under development agreement is R 7,87,73,911/-. Further, in view of the discussion mentioned in pa ras 6 the consideration relatable to loading of TDR is not taxable. The assessing officer is directed to calculate the capital gain accordingly. The ground is partly allowed.”

14. Before us, the Ld. counsel of the assessee submitted that the assessee always retained and owned the plot of land and exchanged 58% of interest in 1828.80 m2 plot with 42% constructed area, which was developed by the developer at its cost, as per terms of DA. The assessee further submitted that it has permitted the developer to load TDR on its pre-constructed building on 2785 m2 plot and got 42% constructed area therefore receipt of 42% constructed area is exchanged against 58% area of the plot and 42% plot always belonged and continue to belong to the assessee. According to the assessee for evaluating full value of the consideration taxable for transfer under DA will be value of the 42% of the constructed area without any value of the land as land always belongs to the assessee. The Ld. counsel of the assessee relied on the decision of the Tribunal, which have already been considered by the Ld. CIT(A) in the impugned order.

15. The Ld. DR on the other hand submitted that full value of the consideration should be taken at ₹18,74,74,699/-as that is the value at which development rights have been transacted and value which has been taken by the stamp duty value authorities for a stamp duty purposes.

16. We have heard rival submission of the parties on the issue in dispute and perused the relevant material on record. We find that as far as non-applicability of section 50 C on the development right is concerned, the Ld. CIT(A) has followed the binding precedent of the Tribunal Mumbai Bench and therefore we do not find any error in the said finding of the Ld. CIT(A). Further regarding holding no capital gain arise on transfer of right to permit loading of TDR , also the Ld. CIT(A) has followed decision of the jurisdictional High Court in the case of Shailja cooperative Housing Society Ltd (supra) in para 6.7 of the impugned order. For ready reference said Para is extracted as under:

“6.7 The Jurisdictional High Court approved the decision of Shailaja Co-op. Housing Society Ltd (supra). In the said decision, the Hon’ble Bench held:

“The assessee was the owner of the land and building and continued to remain the same even after transfer of the said capital asset. Thus, the cost of the land and building of the existing structure could not be attributed to the additional FSI received by means of 1991 Rules. It is true that such right is a capital asset as per the provisions of s. 2(14) but in order to compute capital g ains apart from the existence of capital asset, there should be sale consideration accruing as a result of transfer of capital asset as well as the cost of acquisition of the asset along with the cost of any improvement thereto, if any. Sec. 48 sets out the mode of computation of income under the head capital gains by providing that the expenditure incurred wholly and exclusively in connection with the transfer of a capital asset along with the cost of acquisition and cost of any improvement, if any, shall be deducted from the full value of consideration received or accruing as a result of the transfer of capital asset Transfer of capital asset which does not have any cost of acquisition does not result into capital gains chargeable to lax under s. 45 The legisloture in its wisdom brought out certain categories of capital assets under s. SS(2) as having cost of acquisition at Rs. nil, where such assets have not been purchased by the assessee for consideration. The effect of th is sub-section is that when the assets so specified in sub-s. (2) of s. 55 are transferred, then the cost of acquisition has been taken at Rs. Nil except where the assessee had acquired such assets by means of purchasing from the previous owner, and the computation of the capital gain would be done accordingly. There is a difference in the situation when cost of acquisition is Rs. nil and where the cost of acquisition cannot be ascertained or no cost of acquisition has been incurred. The items of capital assets specified in s. 55(2) are those for which the cost of acquisition shall be taken at Rs. nil for computing capital gains. However if the assessee had not incurred any cost of acquisition on a capital asset and such capital asset does not fall in the category of the capital assets specified in s. S5(2) then no capital gain would be charged. it is abundantly clear that the assessee had not incurred any cost of acquisition in respect of the right which emanated from the 1991 Rules making the assessee eligible to additional FSI. The land and building earlier in the possession of the assessee continued to remain with it as such even after the transfer of the right to additional FSI for Rs. 48 96 lakhs. The Departmental Representative could not point cut any particular asset as specified in sub-S. (2) of s. 55, which would include the right to additional FSI. No capital gains conid be charged on tie transfer of the additional FSI by the assessee for sale consideration of Rs. 48-96 lakhs for the reason that it has no cost of acquisition.”

16.1 Since the Ld. CIT(A) has followed a binding precedent, therefore we do not find any infirmity in the finding of the Ld. CIT(A) in holding that consideration received in the form of constructed area to the extent relatable to loading of the TDR is not taxable.

16.2 As far as value of the 42% of constructed area is considered, the Ld. DVO has determined the cost of construction at ₹8,81,46,948/-. The said report of the DVO has been reproduced by the Assessing Officer in assessment order for AY 2009 -10 on page 8. In clause 13 of said report, cost of construction has been reported at ₹8,81,46,948/-. We respectfully following the decisions cited above, direct the Ld. Assessing Officer to restrict the full value of consideration received by the assessee at 42% of the cost of construction, which works out to ₹3,70,21,718/-. The ground No. one of the appeal of the assessee is accordingly allowed. As far as the argument of Ld. DR that property was converted into stock in trade in the financial year 2007 -08 and therefore should be taxed accordingly, the assessee has already withdrawn its cross objection and the lower authorities has decided the issue of transfer considering the property as capital asset and now the Ld. DR cannot raise new issue, without any ground of appeal. The arguments of the Ld. DR accordingly not relevant for adjudication of the issue -in-dispute. The ground No. 2 &3 of the appeal of Revenue are accordingly dismissed.

17. The Ground No. 2 (two), the appeal of the assessee relates to the disallowance of interest of ₹3,11,920/- related to ECL Finance Ltd.

18. The Assessing Officer disallowed the interest of ₹15,06,920/-holding the same as not incurred for the purpose of the business, wherein the Ld. CIT(A) looking to the past history has treated part of the interest as allowable under the head income from house property, whereas disallowed the amount of ₹3,11,920 /- which was used for improvement of the house property to make it fit for earning rent in future. The Ld. CIT(A) has summarised the facts related to issue in dispute is under:

8. In ground no.9, appellant has challenged disallowance of interest of Rs.15,06,920/- claimed by the appellant while computing the property income. The AO had dealt with the issue in para -7 of the order. It is stated that appellant has claimed interest as being paid to

| (i) | ECL Finance Ltd. | ₹3,11,920/- |

| (ii) | Shobha M. Desai | ₹6,00,000/- |

| (iii) | Suresh I. Patel (HUF) | 5,95,000/- |

| Total | ₹15,06.920/ – |

The A.O. stated that such loans on which interest is claimed are not used for the purpose of business; therefore the same are disallowable. The appellant, during the course of appellate proceedings, stated that appellant has claimed deduction against house property. It is also stated that such interest paid is being allowed in all the past years from AY 06 -07 to 11-12. In AY 06 -07, interest claimed was Rs.12.29 lakhs, in AY 07-08 Rs.13.76 lakhs, and in AY 08-09 Rs.7.68 lakhs, and in 09-10 at Rs.6.05 lakhs. All these assessments has been completed U/s.143(3) of the Act. In AY 10 -11, interest claimed is Rs.10.50 lakhs and in AY 11 -12 Rs.10.95 lakhs. These Returns are accepted u/s.143(1). It is stated that interest paid to Smt. Shobha Desai of Rs.6 lakhs and Rs.5.95 lakhs to Suresh Patel, HUF is on the borrowings made in the earlier years and utilized for acquisition of house property. In AY 12 -13, fresh borrowings has been made of Rs.2 cr. approx. from M/s.ECL Finance Ltd, on which interest of Rs.3,- 11,9200/ is being claimed. Funds were borrowed at the faq -end of the year and has been spent for carrying out improvement and finishing of house property acquired by the appellant under Development Agreement, to make it fit for earning house property income in subsequent years. It is submitted that no part of the interest is disallowable.

18.1 Ld. CIT(A), out of the interest payment of ₹15,06,920/-disallowed the amount of ₹3,11,920/-.

19. Before us, the assessee is not able to substantiate as how the interest paid to ECL finance Ltd is deductible under the income from house property. The assessee has failed to establish that said borrowing from ECL finance Ltd is incurred for acquisition or construction of house property, income from which was offered under the head ‘income from house property’. In absence of any such evidence, we do not find any error in the order of Ld. CIT(A) on the issue in dispute and accordingly uphold the same.

20. The ground 3 of the appeal relates to addition of ₹1,30,000/-. The Ld. Assessing Officer made addition on the basis of loose papers impounded during the course of survey action under section 133 A of the Act in the case of the assessee, which was carried on 21/11/2012. The Ld. CIT(A) has summarized the factual background of the addition made by the AO as under:

“9. Ground No.10 is related to the addition made of Rs.1,30,000/- u/s.69C of the Act. There was a survey action on the appellant u/s.133A on 21.11.12 at the office premises. During the course of survey, a diary marked Al was impounded and based on pg.no.149 of the diary, an addition of Rs 1,30,000/- is being made by AO. The AO has dealt with the issue in para -6 cf the order. AO relied upon pg. 149 of the said diary which provided details of following payments:

(i) Plumber :₹30,000/-

(ii) RS :₹50,000/-

(iii) Daughter-in- :₹50,000/ – law

9.1 A.O. made addition relying on the provisions of Sec.69C of the Act. During the course of appellate proceedings, Ld.AR has relied upon the statement as recorded of Shri Suresh Patel U/s.133A dtd. 21.11.12. Shri Suresh Patel has described that various notings in the diary are scribbling, not connected to the business. During the course of assessment proceedings, appellant explained the above referred expense of Rs.1.30 lakhs as personal expenditure, household expenses of Sures7 Patel were claimed to be reflected in the personal books of account of Shri Suresh Patel. A copy of impounded paper pg.149 is filed in compilation at pg. 114. It is stated that RSP stand for the wife of Shri Suresh Patel and all these expenses of Rs. 1.30 lakhs are not claimed as business expenses in the books of account of appellant and are the personal expenses of Shri Suresh Patel, which are duly explainable as aimed to be recorded in the books of account of Shri Suresh Patel.”

21. The Ld. CIT(A) rejected the contention of the assessee observing as under:

“9.2 I have duly considered the submissions made by the appellant and the facts found by AO in the assessment order. Shri Suresh Patel claimed these expenses to be personal and also claimed that these expenses are reçorded in is personal books of account and has no connection with the appellant. /However, Shri Suresh Patel, who is also a partner of the firm, failed to produce any evidence to substantiate the claim that such expenditure is incurred by him out of explained sources. In view of lack of any such proof being produced even in appellate proceeding, no fault can be found on this ground in the assessment order. Ground no.10 stands rejected.”

22. We have heard rival submission of the parties on the issue in dispute and perused relevant material on record. The assessee has clearly admitted that the expenditure of ₹ 1.3 lakh was incurred, therefore, the assessee was required to explain source of the said expenditure. The Ld. CIT(A) has noted that assessee failed to substantiate the actual expenditure incurred out of the explained sources. Before us, the assessee has not filed any capital account or withdrawal by the assessee and his family members to substantiate the source of expenditure. In the circumstances, we do not find any error in the order of the Ld. CIT(A) on the issue in dispute and accordingly we uphold the same.

23. In the result, the a ppeal of the Revenue for AY 2012 -13 is dismissed and the appeal of the assessee for AY 2012 -13 is partly allowed. The cross- objection of the assessee is dismissed as withdrawn.

24. As far as appeal of the concerned, the ground raise is reproduced as under :

“1. On the facts and circumstances of the case and in law, the Ld. Commissioner of Income-tax(Appeals) has erred in not considering the fact that transfer has been effected in AY 2009-10 as per the provision of Sec.2 (47) (v) of Income-tax Act, 1961 rws 53A of the Transfer of property Act, 1882 which clearly states that once ingress lo the property is handed over to the transferee ie Vidhi Enterprises, the provisions of Sec 53A of ToPA are attracted. In this case, clause 9B, 22(b) and 26 of the DA clearly establish that the Developer had complete access to the property and that he was liable for the actions thereon.”

25. The sole ground raised in the appeal of the Revenue for assessment year 2009 -10, i.e. the year of taxability, has already been adjudicated in the appeal for AY 2012-13, therefore said appeal of Revenue is also dismissed. The cross objection of the assessee for assessment year 2009 -10 is dismissed as withdrawn.

26. In the result, both the appeals of the Revenue for AY 2012 -13 & AY 2009-10 and cross -objections of the assessee for AY 20 12-13 and 2009-10 are dismissed, whereas appeal of the assessee for assessment year 2012 -13 is partly allowed.

Order pronounced in the Court on 06/07/2022.