The document explains the provisions relating to interest payable by taxpayers under Sections 234A, 234B, and 234C of the Income-tax Act, along with the computation rules prescribed under Rule 119A. Section 234A provides for levy of simple interest at 1% per month or part thereof for delay in filing the return of income, filing an updated return, or filing a return in response to a notice under Section 142(1). Section 234B deals with interest for failure to pay advance tax or where advance tax paid is less than 90% of the assessed tax, with interest charged at 1% per month or part thereof on the unpaid amount from the first day of the assessment year until the specified date. Section 234C governs interest for deferment of advance tax instalments when prescribed percentages are not paid by due dates. The document also outlines exceptions, computation methods, illustrative examples, and explanatory multiple-choice questions for better understanding.

INTEREST PAYABLE BY THE TAXPAYER UNDER THE INCOME-TAX ACT

Introduction

Under the Income-tax Act, different types of interests are levied for various kinds of delays/defaults. In this part, you can gain knowledge about the provisions of section 234A, 234B and 234C dealing with interest levied for (i) delay in filing the return of income; (ii) non-payment or short payment of advance tax; and (iii) non-payment or short payment of individual instalment or instalments of advance tax (i.e., deferment of advance tax).

Manner of computation of interest under the Income -tax Act

Before understanding the provisions of section 234A, 234B and 234C it is important to understand the provisions of Rule 119A which gives the manner of computation of interest under the Income-tax Act.

As per Rule 119A, while calculating the interest payable by the taxpayer or the interest payable by the Central Government to the taxpayer under any provision of the Act, the following rule shall be followed :

a) where interest is to be calculated on annual basis, the period for which such interest is to be calculated shall be rounded off to a whole month or months. For this purpose any fraction of a month shall be ignored and the period so rounded off shall be deemed to be the period in respect of which the interest is to be calculated;

b) where the interest is to be calculated for every month or part of a month comprised in a period, any fraction of a month shall be deemed to be a full month and the interest shall be so calculated;

c) the amount of tax, penalty or other sum in respect of which such interest is to be calculated shall be rounded off to the nearest multiple of one hundred rupees. For this purpose, any fraction of one hundred rupees shall be ignored and the amount so rounded off shall be deemed to be the amount in respect of which the interest is to be calculated.

E.g. If we want to compute interest under section 234A on Rs. 8,489 for 3 months and 10 days, then as per Rule 119A discussed above, while computing the amount liable to interest, any fraction of Rs. 100 is to be ignored and, hence, we will ignore Rs. 89 and the balance amount will come to Rs. 8,400. Interest will be computed on Rs. 8,400. Further, the period of 10 days will be considered as full month and, hence, interest will be computed for 4 months.

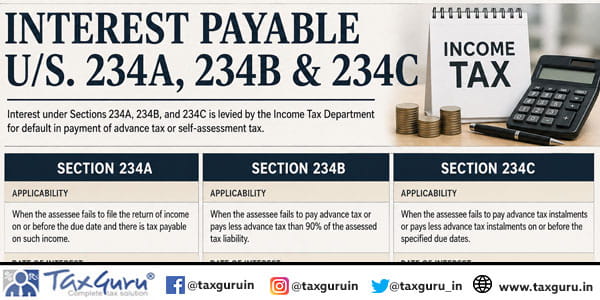

Interest for delay in filing the return of income [Section 234A]

Under section 234A, interest is levied for delay in filing the return of income, filing of an updated return or filing of a return in response to notice issued under section 142(1).

Basic provisions

➢ Interest under section 234A is levied for delay in filing the return of income. In other words, if the taxpayer files the return of income after the due date specified in this regard or files an updated return, interest under section 234A will be levied.

Illustration

Mr. Kapoor is a doctor. His tax liability for the financial year 2025-26 amounted to Rs. 8,400. The due date of filing the return of income in his case is 31st July, 2026. On 5th August, 2026 he paid tax of Rs. 8,400 and filed his return of income. Will he be liable to pay interest under section 234A?

**

Interest under section 234A is levied for delay in filing the return of income. The due date for filing the return of income in the case of Mr. Kapoor is 31st July, 2026 and he has paid the tax and filed the return on 5th August 2026. Hence, he will be liable to pay interest under section 234A on the outstanding tax liability (provisions relating to rate of interest, period of levy of interest and amount liable to interest are discussed later).

Rate of interest

Interest under section 234A is levied for delay in filing the return of income. Interest is levied at 1% per month or part of a month. The nature of interest is simple interest. In other words, the taxpayer is liable to pay simple interest at 1% per month or part of a month for delay in filing the return of income.

Period of levy of interest under section 234A

Interest under section 234A is levied from the period commencing on the date immediately following the due date of filing the return of income and ending on the date of furnishing the return of income, or in case where no return has been furnished, on the date of completion of the assessment under section 144.

It should be noted that while computing the period of levy of interest, part i.e. fraction of a month is considered as full month.

Illustration

Mr. Sunil is an engineer. The due date of filing the return of income in his case is 31st July, 2026. He filed his return of income on 9th December, 2026. His tax liability for the financial year 2025-26 is Rs. 8,400 (which is paid on 9th December, 2026). Will he be liable to pay interest under section 234A, if yes then what will be the period of levy of interest?

**

The due date of filing the return of income is 31st July, 2026, and return of income is filed on 9th December, 2026 i.e. after the due date and hence, Mr. Sunil will be liable to pay interest under section 234A.

While computing interest, part of the month will be taken as full month. In this case, there is a delay of 4 months and 9 days. Part of the month i.e. 9 days will be considered as full month and hence, interest will be levied for 5 months.

Amount liable to interest under section 234A

Interest under section 234A is levied on the amount of tax as determined under section 143(1) and where regular assessment is made, the tax on total income as determined under such regular assessment as reduced by advance tax, tax deducted/collected at source, relief claimed under various sections like sections 89/90/90A/91 and tax credit claimed under section 115JAA/115JD.

Note:

1. Tax on total income determined under section 143(1) shall not include the additional income-tax, if any, payable under section 140B or section 143.

2. Tax on total income determined under regular assessment shall not include the additional income-tax payable under section 140B.

Illustration

Mr. Kumar is running a medical store. The due date for filing the return of income in his case is 31st August. He filed his return of income on 3rd December. Tax liability of Mr. Kumar for the year is Rs. 28,400 (which is paid on 3rd December). Advance tax paid by him is Rs. 15,000 and he has TDS credit of Rs. 5,000. Will he be liable to pay interest under section 234A, if yes then how much?

**

**

Mr. Kumar has filed his return of income after the due date i.e. after 31st August and hence, he will be liable to pay interest under section 234A. Interest will be levied at 1% per month or part of the month.

The due date of filing the return of income is 31st August and the return of income is filed on 3rd December and hence, there is a delay of 3 months and 3 days. Part of the month i.e. 3 days will be considered as full month and hence, interest will be charged for a period of 4 months. Interest will be levied at 1% per month on Rs. 8,400 (*) for 4 months. Thus, interest under section 234A will come to Rs. 420.

(*) Advance tax of Rs. 15,000 and TDS of Rs. 5,000 are to be deducted from the tax liability of Rs. 28,400, hence, net liability after deducting advance tax and TDS will come to Rs. 8,400. Thus, interest will be levied on Rs. 8,400.

Interest for default in payment of advance tax [Section 234B]

Section 234B provides for levy of interest for default in payment of advance tax.

Basic provisions

Interest under section 234B is levied in following two cases:

a) When the taxpayer has failed to pay advance tax though he is liable to pay advance tax; or

b) Where the advance tax paid by the taxpayer is less than 90% of the assessed tax (meaning of assessed tax is discussed later).

As per Section 208 of the Act, advance tax shall be payable by the taxpayer during the financial year if estimated tax liability of assessee during that year is ten thousand rupees or more.

Illustration

Mr. Khushal is running a provision shop. Tax liability of Mr. Khushal for the year is Rs. 38,400. He has not paid any advance tax till 31st March. Entire tax was paid by him at the time of filing the return of income. Will he be liable to pay interest under section 234B?

**

Interest under section 234B is levied in following two cases:

a) When the taxpayer has failed to pay advance tax; or

b) Where the advance tax paid by the taxpayer is less than 90% of the assessed tax.

As per section 208 every person whose estimated tax liability for the year is Rs. 10,000 or more, shall pay his tax in advance in the form of “advance tax”.

The tax liability of Mr. Khushal is Rs. 38,400 (i.e., not less than Rs. 10,000), thus, he is liable to pay advance tax. However, he has not paid any advance tax and, hence, he will be liable to pay interest under section 234B (provisions relating to period of interest, rate of interest and amount on which interest is levied are discussed in later part).

Illustration

Mr. Mangal is running a provision shop. Tax liability of Mr. Mangal for the year is Rs. 48,400. He has paid advance tax of Rs. 46,000 till 31st March. Balance tax of Rs. 2,400 is paid by him at the time of filing the return of income. Will he be liable to pay interest under section 234B?

**

Interest under section 234B is levied in following cases:

(a) When the taxpayer has failed to pay advance tax; or

(b) Where the advance tax paid by the taxpayer is less than 90% of the assessed tax.

In this case, Mr. Mangal has paid 95% of the advance tax (*) i.e. more than 90% and thus, no interest will be levied under section 234B.

(*) The tax liability of Mr. Mangal is Rs. 48,400 and he has paid advance tax of Rs. 46,000. The quantum of advance tax paid by him will come to 95% (i.e., Rs. 46,000/Rs. 48,400) of the total tax liability.

Illustration

Mr. Raja is engaged in furniture business. Tax liability of Mr. Raja for the year is Rs. 58,400. He has paid advance tax of Rs. 35,000 till 31st March. Balance tax of Rs. 23,400 is paid by him at the time of filing the return of income. Will he be liable to pay interest under section 234B?

**

Interest under section 234B is levied in following cases:

(a) When the taxpayer has failed to pay advance tax; or

(b) Where the advance tax paid by the taxpayer is less than 90% of the assessed tax.

In this case, Mr. Raja has paid advance tax of Rs. 35,000. The quantum of advance tax paid by him is 60% of the total tax liability (*) i.e. less than 90% and hence, he will be liable to pay interest under section 234B.

(*) The tax liability of Mr. Raja is Rs. 58,400 and he has paid advance tax of Rs. 35,000. The quantum of advance tax paid by him will come to 60% (i.e., Rs. 35,000/Rs. 58,400) of the total tax liability.

Rate of interest

Under section 234B, interest for default in payment of advance tax is levied at 1% per month or part of a month. The nature of interest is simple interest. In other words, the taxpayer is liable to pay simple interest at 1% per month or part of a month for default in payment of advance tax.

Amount liable for interest

Interest under section 234B is levied on the amount of unpaid advance tax. If there is a shortfall in payment of advance tax, then interest is levied on the amount by which advance tax is short paid. The amount of unpaid/short paid advance tax is computed as follows :

| Particulars | Amount |

| Assessed tax (*) | XXXXX |

| Less : Advance tax paid (if any) | (XXXXX) |

| Amount of unpaid/short paid advance tax | XXXXX |

(*) Assessed tax means the amount of tax as determined under section 143(1) and where regular assessment is made, the tax on total income as determined under such regular assessment as reduced by tax deducted/collected at source, relief/deduction of tax claimed under various sections like sections 89/90/90A/91 and tax credit claimed under section 115JAA/115JD.

Tax on total income determined under section 143(1) shall not include the additional income-tax, if any, payable under section 140B or section 143 and tax on total income determined under regular assessment shall not include the additional income-tax payable under section 140B.

Period of levy of interest

Interest under section 234B is levied from the first day of the assessment year, i.e., from 1st April till the date of determination of income under section 143(1) or when a regular assessment is made, then till the date of such a regular assessment.

In a case where the income is increased on account of assessment/re-computation, interest under section 234B will be levied on the differential amount from the first day of the assessment year till the date of assessment/re-computation. In a case where an application is made to Settlement Commission, interest under section 234B will be levied on the differential amount from the first day of the assessment year till the date of making the application. Further, if the income as declared in the application is increased by the Settlement Commission, interest under section 234B will be levied on the differential amount from the first day of the assessment year till the date of such order. If as a result of rectification order of the Settlement Commission, income is increased/decreased, interest will also be increased/decreased accordingly.

If the taxpayer has paid any tax before completion of assessment, then interest will be levied as follows:

(a) Upto the date of payment of self assessment tax, interest will be computed on the amount of unpaid advance tax.

(b) From the date of payment of self assessment tax, interest will be levied on the unpaid amount of advance tax after deducting the self assessment tax paid by the taxpayer.

Illustration

Mr. Suraj is a businessman. His tax liability as determined under section 143(1) is Rs. 28,400. He has not paid any advance tax but there is a TDS credit of Rs. 10,000 in his account. He has paid the balance tax on 31st August i.e. at the time of filing the return of income. Will he be liable to pay interest under section 234B, if yes, then how much?

**

In this case, the tax liability (after allowing credit of TDS) of Mr. Suraj comes to Rs. 18,400 (i.e. Rs. 28,400 – Rs. 10,000) which exceeds Rs. 10,000 and hence, he will be liable to pay advance tax.

He has not paid any advance tax and hence, he will be liable to pay interest under section 234B. Interest under section 234B will be levied at 1% per month or part of the month. In this case, Mr. Suraj has paid the outstanding tax on 31st August and hence, interest under section 234B will be levied for the period from 1st April to 31st August i.e. for 5 months.

Interest will be levied on unpaid tax liability of Rs. 18,400. Interest at 1% per month on Rs. 18,400 for 5 months will come to Rs. 920.

Interest for default in payment of instalment(s) of advance tax [Section 234C]

Section 234C provides for levy of interest for default in payment of instalment(s) of advance tax. Before getting into the detailed provisions of section 234C, lets recall the provisions relating to payment of advance tax by a taxpayer.

As per section 208, every person whose estimated tax liability for the year exceeds Rs. 10,000, shall pay his tax in advance in the form of “advance tax” by following dates :

| Status | By 15th June | By 15th September | By 15th December | By 15th March |

| Taxpayers (other than those who opted for presumptive taxation scheme of section 44AD or section 44ADA) | Upto 15% of advance tax | Upto 45% of advance tax | Upto 75% of advance tax | Upto 100% of advance tax |

| Taxpayers who opted for presumptive taxation scheme of section 44AD or section 44ADA | Nil | Nil | Nil | Upto 100% of advance tax |

Any tax paid till 31st March will be treated as advance tax.

Basic provisions

Interest under section 234C is levied, if advance tax paid in any instalment(s) is less than the required amount. In other words, interest under section 234C in case of deferment of different instalments of advance tax is levied in following cases:

(A) In case of taxpayers (other than those who opted for presumptive taxation scheme under section 44AD or section 44ADA), interest shall be levied-

-

- If advance tax paid on or before 15thJune is less than 12% of advance tax payable

- If advance tax paid on or before 15th September is less than 36% of advance tax payable

- If advance tax paid on or before 15th December is less than 75% of advance tax payable

- If advance tax paid on or before 15th March is less than 100% of advance tax payable

(B) In case of taxpayers who opted for presumptive taxation scheme of section 44AD or section 44ADA interest shall be levied if advance tax paid on or before 15th March is less than 100% of advance tax payable.

No levy of interest if shortfall in payment of advance tax is due to capital gains or winning from lottery, etc.

Interest under section 234C is not levied, if, the shortfall in payment of advance tax is due to failure to estimate the amount of capital gains or income referred to in section 2(24)(ix) (i.e. winning from lotteries, crossword puzzle, etc.) or income from a new business or income referred to in section 115BBDA (i.e., dividend received from a domestic company exceeds Rs. 10,00,000) and the taxpayer pays the required advance tax on such income as a part of immediate following instalments or till 31st March, if no instalment is pending.

Rate of interest

Interest under section 234C for default in payment of instalment(s) of advance tax is charged at 1% per month or part of a month. The nature of interest is simple interest. In other words, the taxpayer is liable to pay simple interest @ 1% per month or part of a month for short payment/ non-payment of individual instalment(s) of advance tax.

Period of levy of interest

Interest under section 234C is levied for a period of 3 months, in case of short fall in payment of 1st, 2nd and 3rd instalment and for 1 month, in case of short fall in payment of last instalment.

Amount liable for interest

Interest under section 234C is levied on the short paid amount of instalment(s) of advance tax.

Illustration

Mr. Khushal is running a garments shop. Tax Liability of Mr. Khushal is Rs 45,500. He has paid advance tax as given below:

➢ Rs. 8,000 on 15th June,

➢ Rs. 11,000 on 15th September,

➢ Rs. 12,000 on 15th December,

➢ Rs. 14,500 on 15th March.

Mr. Khushal has not opted for presumptive taxation scheme of section 44AD. Will he be liable to pay interest under section 234C, if yes, then how much?

**

Every person whose estimated tax liability for the year exceeds Rs. 10,000, shall pay his tax in advance in the form of “advance tax” by the following dates:

| Status | By 15th June | By 15th September | By 15th December | By 15th March |

| Taxpayers (other than those who opted for presumptive taxation scheme of section 44AD or section 44ADA) | Upto 15% of advance tax | Upto 45% of advance tax | Upto 75% of advance tax | Upto 100% of advance tax |

| Taxpayers who opted for presumptive taxation scheme of section 44AD or section 44ADA | Nil | Nil | Nil | Upto 100% of advance tax |

Any tax paid till 31st March will be treated as advance tax.

Considering the above dates, the advance tax liability of Mr. Khushal at different installments will be as follows:

1) In first installment: Not less than 15% of tax payable should be paid by 15th June. The tax liability is Rs. 45,500 and 15% of 45,500 amounts to Rs. 6,825. Hence, he should pay Rs. 6,825 by 15thJune. He has paid Rs. 8,000, hence, there is no short payment in case of first installment.

2) In second installment: Not less than 45% of tax payable should be paid by 15th September. Tax liability is Rs. 45,500 and 45% of 45,500 amounts to Rs. 20,475. Hence, he should pay Rs. 20,475 by 15th September. He has paid Rs. 8,000 on 15th June and Rs. 11,000 on 15th September (i.e. total of Rs. 19,000 is paid till 15th September). There is short payment of Rs. 1,475 (i.e. Rs. 20,475 – Rs 19,000).

Though there is short payment of Rs. 1,475 but Mr. Khushal will not be liable to pay interest under section 234C because he has paid minimum of 36% of advance tax payable by 15th September. He has paid Rs. 19,000 till 15th September and 36% of 45,500 amounts to Rs. 16,380. Hence, no interest shall be levied in case of deferment of second installment.

3) In third installment: Not less than 75% of tax payable should be paid by 15th December. Tax liability is Rs. 45,500 and 75% of 45,500 amounts to Rs. 34,125. Hence, he should pay Rs. 34,125 by 15th December. He has paid Rs. 8,000 on 15th June, Rs. 11,000 on 15th September and Rs. 12,000 on 15th December (i.e. total of Rs. 31,000 is paid till 15th December). There is a short payment of Rs. 3,125 (i.e. Rs. 34,125 – Rs 31,000). Hence, he will be liable to pay interest under section 234C on account of short fall of Rs. 3,125 (*).

4) In last installment: 100% of tax payable should be paid by 15th March. The total tax liability of Rs. 45,500 is paid by Mr. Khushal by 15th March (i.e. 8,000 on 15th June, Rs. 11,000 on 15th September, Rs. 12,000 on 15th December and Rs 14,500 on 15th March). Hence, there is no short payment in case of last installment. Thus, Mr. Khushal will not be liable to pay interest under section 234C in case of last instalment.

(*) There is a short fall of Rs. 3,125 in case of third installment (computation already discussed). Due to short fall in case of third installment, interest under section 234C will be levied. Interest will be levied at 1% per month or part of the month on the short paid amount of Rs. 3,100 (i.e. Rs. 3,125 rounded off to Rs. 3,100 as per Rule 119A). Interest will be levied for a period of 3 months. In other words, interest will be levied on Rs. 3,100 at 1% per month for 3 months. Interest under section 234C will come to Rs. 93.

MCQ ON INTEREST PAYABLE BY THE TAXPAYER UNDER THE INCOME- TAX ACT

Q1. Under section 234A, interest is levied for ______.

(a) Delay in filing the return of income (b) Non-payment of tax

(c) For non-payment of advance tax (d) For short payment of advance tax

Correct answer : (a)

Justification of correct answer :

Interest under section 234A is levied for delay in filing the return of income. In other words, if the taxpayer files the return of income after the due date specified in this regard, interest under section 234A will be levied.

Thus, option (a) is the correct option.

Q2. Interest under section 234A for delay in filing the return of income is levied at _____ % per month or part of a month.

(a) 1.5 (b) 2

(c) 0.5 (d) 1

Correct answer : (d)

Justification of correct answer :

Interest under section 234A is levied for delay in filing the return of income. Interest is levied at 1% per month or part of a month. The nature of interest is simple interest. In other words, the taxpayer is liable to pay simple interest @ 1% per month or part of a month for delay in filing the return of income.

Thus, option (d) is the correct option.

Q3. Section 234B provides for levy of interest for default in complying with the notice for payment of tax

(a) True (b) False

Correct answer : (b)

Justification of correct answer :

Section 234B provides for levy of interest for default in payment of advance tax.

Thus, the statement given in the question is false and hence, option (b) is the correct option.

Q4. Interest under section 234B is levied in following two cases:

(i) When the taxpayer has failed to pay advance tax though he is liable to pay advance tax; or

(ii) Where the advance tax paid by the taxpayer is less than 75% of the assessed tax

(a) True (b) False

Correct answer : (b)

Justification of correct answer :

Interest under section 234B is levied in following two cases:

(i) When the taxpayer has failed to pay advance tax though he is liable to pay advance tax; or

(ii) Where the advance tax paid by the taxpayer is less than 90% of the assessed tax.

Thus, the statement given in the question is false and hence, option (b) is the correct option.

Q5. Interest under section 234B for default in payment of advance tax is levied @____% per month or part of a month.

(a) 1.5 (b) 2

(c) 0.5 (d) 1

Correct answer : (d)

Justification of correct answer :

Under section 234B, interest for default in payment of advance tax is levied at 1% per month or part of a month. The nature of interest is simple interest. In other words, the taxpayer is liable to pay simple interest at 1% per month or part of a month for default in payment of advance tax.

Thus, option (d) is the correct option.

Q6. Interest under section 234B is levied on the amount of unpaid advance tax. If there is a shortfall in payment of advance tax, then also interest is levied on the entire amount of advance tax.

(a) True (b) False

Correct answer : (b)

Justification of correct answer :

Interest under section 234B is levied on the amount of unpaid advance tax. If there is a shortfall in payment of advance tax, then interest is levied on the amount by which advance tax is short paid. The amount of unpaid/short paid advance tax is computed as follows :

| Particulars | Amount |

| Assessed tax (*) | XXXXX |

| Less : Advance tax paid (if any) | (XXXXX) |

| Amount of unpaid/short paid advance tax | XXXXX |

Assessed tax means the amount of tax as determined under section 143(1) and where regular assessment is made the tax on total income as determined under such regular assessment as reduced by tax deducted/collected at source, relief of tax claimed under various sections like sections 89/90/90A/91 and tax credit claimed under section 115JAA/115JD.

Thus, the statement given in the question is false and hence, option (b) is the correct option.

Q7. Interest under section _____ is levied from the first day of the assessment year, i.e., from 1st April till the date of determination of income under section 143(1) or when a regular assessment is made, then till the date of such a regular assessment.

(a) 234A (b) 234B

(c) 234C (d) 234D>

Correct answer : (b)

Justification of correct answer :

Interest under section 234B is levied from the first day of the assessment year, i.e., from 1st April till the date of determination of income under section 143(1) or when a regular assessment is made than till the date of such a regular assessment.

Thus, option (b) is the correct option.

Q8. Section provides for levy of interest for default in payment of instalment(s) of advance tax.

(a) 234A (b) 234B

(c) 234C (d) 234D

Correct answer : (c)

Justification of correct answer :

Section 234C provides for levy of interest for default in payment of instalment(s) of advance tax.

Thus, option (c) is the correct option.

Q9. Interest under section 234C is not levied, if, the shortfall in payment of advance tax is due to failure to estimate the amount of capital gains or income referred to in section 2(24)(ix) (i.e. winning from lotteries, crossword puzzle, etc.).

(a) True (b) False

Correct answer : (a)

Justification of correct answer :

Interest under section 234C is not levied, if, the shortfall in payment of advance tax is due to failure to estimate the amount of capital gains or income referred to in section 2 (24)(ix) (i.e. winning from lotteries, crossword puzzle, etc.) or income from a new business or income referred to in section 115BBDA (i.e., dividend received from a domestic company exceeds Rs. 10,00,000) and the taxpayer pays the required advance tax on such income as a part of immediate following instalments or till 31st March if no instalment is pending.

Thus, the statement given in the question is true, and hence, option (a) is the correct option.

Above document contains the provisions of the Income-tax Act, 1961, as amended by the Finance Act, 2026.

*****

Disclaimer: The contents of this document are for information purposes only. This aims to enable public to have a quick and an easy access to information and do not purport to be legal documents. Viewers are advised to verify the content from Government Acts/Rules/Notifications etc.

(Republished with amendments)

I am a senior citizen (75). In December 2023, I sold a property with an LTCG. When Am I supposed to pay the tax on LTCG? IS the section 234 B and C will be applicable for my case also even though I am normally exempt from paying any Advance tax?

I am a Senior Citizen yet to file IT Return for AY 21-22. Balance Tax payable is 194000. Whether I have to pay any interest.

Yes it is exempt in case of senior citizen.

Also if this amount is only upto 10% of total tax payable then also it is exempt.

Am I liable to pay interest u/s 234B & 234C on Interest earned in bank account and Dividends on stocks where the Bank and the Divident paying companies have not deducted the prescribed percentage of tax ?

If yes, is it not unfair to penalize the individuals for things beyond their control, where the Bank or dividend paying companies have not fullfilled their obigations quoting whatever reasons ?

I am a senior citizen. While filling up my return for 2020-21 before due date, it has been auto filled in my return an amount of Rs1640/- towards interest us/234A. Please let me know why this interest amount I have to pay since I am submitting the return much before the due date, i.e. 30th Sept. 20121.

I BEING A SENIOR CITIZEN HAS BEEN IMPOSED INTEREST U/S 234 A . PLEASE CLARIFY

my tax liability is Rs 4,27,787 for the FY 19-20 and my TDS Credit is more than 90% i.e Rs 4,10,106, but while i am filing my returns 234B is coming. can any one explain it why 234B is coming?

Hello. I am a senior citizen aged 62. My self-assessment tax works out to more than Rs 1 lakh as of now(1 Jul). Itr2 does not work out any interest. Do we have to calculate the interest and pay? Thanks in advance for your guidance.

If there is delay in filing return and there is short payment of advance tax, is interest payable u/s 234A in addition to interest u/s 234B?

in vivad se viswas scheme int. 234b and 234c is also

weived

Whether 234a interest need to be calculated on tax payable including late filing fee also?????

In the case of re-assessment of ROI for AY 12-13 u/s 147 completed after 15.06.2015, interest u/s 234B(3) will be computed as per the amended provisions of 234B(3) – (i.e) interest period will start from 1st April of the AY (or from the date of completion of regular assessment u/s 143(3) ?

FOR AY 2016-17,MY TAX LIABILITY WAS RS.745922 AND OUT OF THAT RS.717546 WAS DEDUCTED AS TDS SHOWN IN 26AS. THE BALANCE. AMOUNT RS.28376 AND RS.1132 U/S 234B AND RS.1048 U/S 234C AGGREGATING RS.30560 (AFTER R/OFF) WAS PAID AS SELF ASSESSED TAX. IS THIS CALCULATION OK OR WRONG ?

What is the maximum limitation on difference in Tax paid and Tax Payable amounts IT department can allow without asking for rectification or payment of tax. For INR 2 shortfall are you bound to pay large amount of interest under U/S 234B&C?

For salaried employee whose tds is deducted by his employer in this case can provisions of 234B & 234C are applicable ? Please guide.

i m Sr citizen.pls confirm whether interst under sr citizen saving scheme is tax free up to rs 50000 per year or not

under section 80 d,can i claim deduction on medical expenses done in treatment from private doctors or not

No illustration in the case of Senior Citizen is given.

As senior citizen need not pay advance tax, is he liable to interest on late payment

It’s help a lot. Thank you so much.

Very Informative topic with crystal clear illustrations

Thanks for giving a detailedly the manner in which interest is to be calculated under sections 234 A, B, and C.

You have dealt in detail the provisions of sec 234 and it’s sub sections

Regards

CA T S Nagarajan

When A company Sale Investment and arrised taxable Capital Gain in the month of March for the FY,

But company need to pay MAT as applicable .

should the company need to pay 234C on the MAT payable?

An assessee received arrears of salary for 5 years. Tax payable before relief u/s 89(1) works out to Rs.11,700 and relief u/s 89(1) works out to Rs. 8,900. thus, effective tax liability for AY 2017-18 comes to Rs.2,800. Whether there will be any liability towards interest u/s 234A, 234B and 234C for AY 2017-18. Kindly enlighten. Thanks

Whether interest U/S 234A is applicable

in case return is filed in response to notice U/S 148 with in 30 days for A.Y. 2011-12 on receipt of notice ??

f advance tax paid on or before 15th June is less than 12% of advance tax payable

If advance tax paid on or before 15thSeptember is less than 36% of advance tax payable

Please clarify the 12% or 36%. I could not understand

GOOD ARTICLE

Very Good Article.

Very Good Article and Helpful for Many Peoples.

Keep it up Dear.

Thanks a lot

One of my clients have only interest income from bank.Notice u/s148 has been issued for AY1314.

His residential status is non-resident. Whether the residential status of an assesse has any relevance in calculating interest u/s 234b &234 C.No TDS has been deducted by bank on interest amount.

Please advise.

Interest u/s 234B and 234 C to be paid on MAT?

Res. Sir,

I have filled a IT return of salary employee & he got his arrear amount on march-17 & whole year TDS is deducted at a time in 4th Qtr, i.e. TDS of approx Rs. 60000/- deposit in April-2017,

i have also return file on july-2017, but my question is, after processing of IT return u/s 143(1), it is charges 234b & 234C interest approx Rs. 8500/-

please suggest me.

Very Informative & clear. Good Illustrations as well. Many thanks & wishing God’s grace

If I file income tax return after 31st December 2017 for financial year 2016-17 Assessment Year 2017-18, Then I have will applicable Late return filing levy????

how we can calculate the 234A,234B,234C in lac of income tax calculator(closed from site)

Given a situation, the total tax liability of the assessee is Rs.18000 and has a TDS of Rs.10000 thereby resulting the net tax payable Rs.8000. Does interest provisions apply as per Sec 208.

What about relief U/s 89? Whether it will also be deducted for calculating interest?

Interest will be payable if total tax liability is greater than tds deducted

Sigh & Associates

Tax Law Firm

moradabad U.P.

Mob-9760633999

Please advice:-

1. Assessee – Individual

2.Only Income from Salary and Inters from SB a/c

3.I.T Return for the F.Y-2016-17 (A.Y-2017-18)

4.TDS on Salary already deducted with in April 2017 which was payable for F.Y 2016-17

5.ITR1 to be filed during Nov.2017

6.Interest u/s 234A payable or not.

Regards,

Srimonta Ghosh

Whether Int. u/s 234C is levied if business of non corporate assessee is started in the month of November of that year.