The document explains the tax treatment of unexplained cash credits and related unexplained amounts under Sections 68 to 69D of the Income-tax Act, 1961, as amended by the Finance Act, 2026. Under Section 68, any sum credited in the books of a taxpayer for which no satisfactory explanation regarding its nature and source is provided may be treated as income of that year. Special provisions apply to closely held companies receiving share application money, share capital, or share premium, requiring satisfactory explanations from the contributors. Similar deeming provisions cover unexplained investments, unexplained money, bullion or jewellery, underreported investments, unexplained expenditure, and hundi transactions under Sections 69, 69A, 69B, 69C, and 69D. The document also outlines the conditions necessary for invoking these provisions and highlights the stringent tax regime under Section 115BBE. Such income is taxable at 60%, subject to surcharge and applicable additions, and taxpayers are generally denied deductions, loss set-offs, and related tax benefits against such income.

TAX TREATMENT OF CASH CREDITS

Any sum found credited in the books of the taxpayer, for which he offers no explanation about the nature and source thereof or the tax authorities are not satisfied by the explanation offered by the taxpayer, is termed as cash credit. In this part you can gain knowledge about various provisions relating to tax treatment of cash credit.

Basic provisions

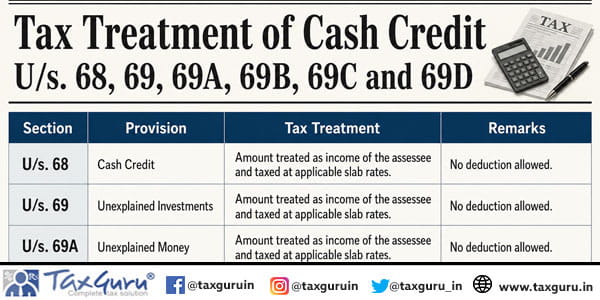

The provisions relating to tax treatment of cash credit are given in section 68. As per section 68, any sum found credited in the books of a taxpayer, for which he offers no explanation about the nature and source thereof or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, may be charged to income-tax as the income of the taxpayer of that year.

In case of a taxpayer being a closely held company (i.e., not being a company in which the public are substantially interested), if the sum so credited consists of share application money, share capital, share premium or any such amount by whatever name called, any explanation offered by such company shall be deemed to be not satisfactory, unless:

(a) the person, being a resident in whose name such credit is recorded in the books of such company, also offers an explanation about the nature and source of such sum so credited; and

(b) such explanation in the opinion of the Assessing Officer has been found to be satisfactory.

Further, where any amount is found credited in the books of an assessee by way of loan or borrowing or any such amount, the explanation of the assessee cannot be deemed to be satisfactory unless:

(a) the person in whose name such credit is recorded in the books of such assessee also offers an explanation about the nature and source of such sum so credited; and

(b) such explanation in the opinion of the Assessing Officer aforesaid has been found to be satisfactory. [Applicable w.e.f. Assessment Year 2023-24]

The above discussed provisions shall not apply if the person, in whose name such sum is recorded, is a venture capital fund or a venture capital company as referred to in section 10(23FB).

Conditions to be satisfied for applicability of section 68

From the reading of section 68, following conditions can be stated to attract the applicability of section 68 :

- Assessee has maintained ‘books’

- There has to be credit of amounts in the books maintained by the taxpayer of a sum during the year.

- The taxpayer offers no explanation about the nature and source of such credit found in the books or the explanation offered by the taxpayer in the opinion of the Assessing Officer is not satisfactory.

If all the above conditions exist, sum so credited may be charged to tax as income of the taxpayer of that year.

Other provisions to be kept in mind

Apart from the provisions relating to taxing of cash credit given under section 68, similar provisions are designed under section 69, 69A , 69B , 69C and 69D in respect of certain other items. The provisions in this regard are as follows:

| Section | Brief overview |

| 69 | Unexplained investments

Where in a year the taxpayer has made investments which are not recorded in the books of account, if any, maintained by him for any source of income, and he offers no explanation about the nature and source of the investments or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, than the value of the investments may be deemed to be the income of the taxpayer of such year. |

| 69A | Unexplained money, etc.

Where in any year the taxpayer is found to be the owner of any money, bullion, jewellery or other valuable article and such money, bullion, jewellery or valuable article is not recorded in the books of account, if any, maintained by him for any source of income, and the taxpayer offers no explanation about the nature and source of acquisition of the money, bullion, jewellery or other valuable article, or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, than the money and the value of the bullion, jewellery or other valuable article may be deemed to be the income of the taxpayer for such year. |

| 69B | Amount of investments, etc., not fully disclosed in books of account

Where in any year the taxpayer has made investments or is found to be the owner of any bullion, jewellery or other valuable article, and the Assessing Officer finds that the amount expended on making such investments or in acquiring such bullion, jewellery or other valuable article exceeds the amount recorded in this behalf in the books of account maintained by the taxpayer for any source of income, and the taxpayer offers no explanation about such excess amount or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, than the excess amount may be deemed to be the income of the taxpayer for such year. |

| 69C | Unexplained expenditure, etc.

Where in any year the taxpayer has incurred any expenditure and he offers no explanation about the source of such expenditure or part thereof, or the explanation, if any, offered by him is not, in the opinion of the Assessing Officer, satisfactory, then the amount covered by such expenditure or part thereof, as the case may be, may be deemed to be the income of the taxpayer for such year. Aforesaid unexplained expenditure which is deemed to be the income of the taxpayer by virtue of section 69C shall not be allowed as a deduction under any head of income. |

| 69D | Amount borrowed or repaid on hundi

Where any amount is borrowed on a hundi from, or any amount due thereon is repaid to, any person otherwise than through an account- payee cheque drawn on a bank, the amount so borrowed or repaid shall be deemed to be the income of the person borrowing or repaying the such amount. It will be treated as income for the year in which it was borrowed or repaid, as the case may be. However it should be noted that if any amount borrowed on a hundi has been treated as income of any person by virtue of section 69D, than such person shall not be liable to be assessed again in respect of the same amount on repayment thereof. Amount repaid shall include the amount of interest paid on the amount borrowed. |

Tax rates applicable to amount charged to tax by virtue of sections 68, 69 , 69A , 69B , 69C and 69D

As per Section 115BBE, income tax shall be calculated at 60% where the total income of assessee includes following income:

a) Income referred to in Section 68, Section 69, Section 69A, Section 69B, Section 69Cor Section 69Dand reflected in the return of income furnished under Section 139; or

b) Which is determined by the Assessing Officer and includes any income referred to in Section 68, Section 69, Section 69A, Section 69B, Section 69Cor Section 69D, if such income is not covered under clause (a).

Such tax rate of 60% will be further increased by 25% surcharge, 6% penalty (under section 271AAC), i.e., the final tax rate comes out to be 84% (including cess). Provided that such 6% penalty shall not be levied when the income under Section 68, 69 , etc., has been included in return of income and tax has been paid on or before the end of relevant previous year.

No deduction in respect of any expenditure or allowance [or set off of any loss] shall be allowed to the assessee in computing his income referred to in clause (a) of sub-section (1) of Section 115BBE.

MCQ ON TAX TREATMENT OF CASH CREDITS

Q1. Any sum found credited in the books of the taxpayer, for which he offers no explanation about the nature and source thereof or the tax authorities are not satisfied by the explanation offered by the taxpayer, is generally termed as cash credit.

(a) True (b) False

Correct answer : (a)

Justification of correct answer :

Any sum found credited in the books of the taxpayer, for which he offers no explanation about the nature and source thereof or the tax authorities are not satisfied by the explanation offered by the taxpayer, is termed as cash credit.

Thus, the statement given in the question is true and hence, option (a) is the correct option.

Q2. The provisions relating to tax treatment of cash credit are given in section________________.

(a) 69B (b) 69A

(c) 69 (d) 68

Correct answer : (d)

Justification of correct answer :

The provisions relating to tax treatment of cash credit are given in section 68.

Thus, option (d) is the correct option.

Q3. In case of a taxpayer being a closely held company if the sum so credited consists of share application money, share capital, share premium or any such amount by whatever name called, any explanation offered by such company shall be deemed to be not satisfactory, unless:

- the person, being a resident in whose name such credit is recorded in the books of such company, also offers an explanation about the nature and source of such sum so credited; and

- such explanation in the opinion of the Assessing Officer has been found to be satisfactory.

(a) True (b) False

Correct answer : (a)

Justification of correct answer :

In case of a taxpayer being a closely held company if the sum so credited consists of share application money, share capital, share premium or any such amount by whatever name called, any explanation offered by such company shall be deemed to be not satisfactory, unless:

- the person, being a resident in whose name such credit is recorded in the books of such company, also offers an explanation about the nature and source of such sum so credited; and

- such explanation in the opinion of the Assessing Officer has been found to be satisfactory.

Thus, the statement given in the question is true and hence, option (a) is the correct option.

Q4. The condition of satisfactory explanation about the nature and source of credit by the person in whose name credit of share application money, share capital, etc. is recorded in the books of a closely held company, shall not apply if such person is________________.

(a) A partnership firm

(b) A venture capital fund or venture capital company as referred to in section 10(23FB)

(c) A HUF

(d) An individual

Correct answer : (b)

Justification of correct answer :

The condition of satisfactory explanation about the nature and source of credit by the person in whose name credit of share application money, share capital, etc. is recorded in the books of a closely held company, shall not apply if such person is a venture capital fund or a venture capital company as referred to in section 10(23FB).

Thus, option (b) is the correct option.

Q5. As per section 115BBE, any cash credit found in the books of the taxpayer which is charged to tax by virtue of section 68 is taxable at a flat rate of (plus surcharge and cess as applicable).

(a) 30% (b) 15%

(c) 20% (d) 60%

Correct answer : (d)

Justification of correct answer :

As per Section 115BBE, income tax shall be calculated at 60% where the total income of assessee includes following income:

- a) Income referred to in Section 68, Section 69, Section 69A, Section 69B, Section 69Cor Section 69Dand reflected in the return of income furnished under Section 139; or

- b) Which is determined by the Assessing Officer and includes any income referred to in Section 68, Section 69, Section 69A, Section 69B, Section 69Cor Section 69D, if such income is not covered under clause (a).

Such tax rate of 60% will be further increased by 25% surcharge, 6% penalty, i.e., the final tax rate comes out to be 84% (including cess). Provided that such 6% penalty shall not be levied when the income under Section 68, 69 , etc., has been included in return of income and tax has been paid on or before the end of relevant previous year.

No deduction in respect of any expenditure or allowance [or set off of any loss] shall be allowed to the assessee in computing his income referred to in clause (a) of sub-section (1) of Section 115BBE.

Thus, option (d) is the correct option.

Q6. As per section 115BBE, the taxpayer is not entitled to claim any deduction, set-off any loss as well as the benefit of adjustment of the basic exemption limit against the cash credits charged to tax by virtue of section 68.

(a) True (b) False

Correct answer : (a)

Justification of correct answer :

As per section 115BBE, the taxpayer is not entitled to claim any deduction, set-off any loss or to adjust the basic exemption limit against the income referred to in clause (a) of section 115BBE(1).

Thus, the statement given in the question is true and hence, option (a) is the correct option.

Q7. As per section_______________, where in a year the taxpayer has made investments which are not recorded in the books of account, if any, maintained by him for any source of income, and he offers no explanation about the nature and source of the investments or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, then the value of the investments may be deemed to be the income of the taxpayer of such year.

(a) 68 (b) 69

(c) 69B (d) 69D

Correct answer : (b)

Justification of correct answer :

As per section 69, where in a year the taxpayer has made investments which are not recorded in the books of account, if any, maintained by him for any source of income, and he offers no explanation about the nature and source of the investments or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, then the value of the investments may be deemed to be the income of the taxpayer of such year.

Thus, option (b) is the correct option.

Q8. Section 69C contains the provisions relating to________________.

(a) Unexplained money

(b) Amount borrowed or repaid on Hundi

(c) Unexplained expenditure

(d) Amount of investments, etc., not fully disclosed in books of account

Correct answer : (c)

Justification of correct answer :

Section 69C contains the provisions relating to unexplained expenditure.

Thus, option (c) is the correct option.

Q9. The taxpayer is entitled to claim any deduction, set-off any loss as well as the benefit of adjustment of the basic exemption limit against the amount charged to tax by virtue of provisions of sections 69 to 69D .

(a) True (b) False

Correct answer : (b)

Justification of correct answer :

As per section 115BBE, the taxpayer is not entitled to claim any deduction, set-off any loss as well as the benefit of adjustment of the basic exemption limit against the amount charged to tax under clause (9) of sub-section (1) of section 115BBE.

Thus, the statement given in the question is false and hence, option (b) is the correct option.

Above document contains the provisions of the Income-tax Act, 1961, as amended by the Finance Act, 2026.

*****

Disclaimer: The contents of this document are for information purposes only. This aims to enable public to have a quick and an easy access to information and do not purport to be legal documents. Viewers are advised to verify the content from Government Acts/Rules/Notifications etc.

(Republished with amendments)

SIR CAN A HUF CLIAM A RELIF U/S 89

Thanks for sharing information