#NAA

Log in to FollowEvery article filed under the “NAA” tag — analysis, news and updates.

454 articlesGoods and Services Tax

Goods and Services Tax

No profiteering as no Tax reduction in GST Era on Courier Services

Goods and Services Tax

Goods and Services Tax

No profiteering if no increase in per unit base price post tax reduction

Goods and Services Tax

Goods and Services Tax

Competition from exempt /compounding manufacturers not valid ground to indulge in Profiteering

Goods and Services Tax

Goods and Services Tax

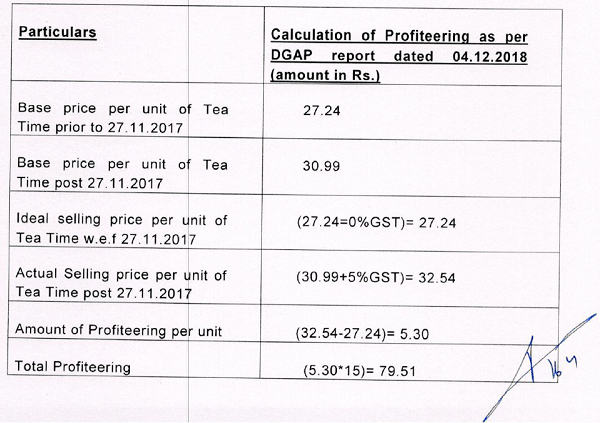

Profiteering Complaints Adjudicated by NAA In 2018

Goods and Services Tax

Goods and Services Tax

No profiteering as tax rate in GST era increased to 28% from earlier 14.75%

Goods and Services Tax

Goods and Services Tax

No Anti-Profiteering if base price remained same even after tax reduction

Goods and Services Tax

Goods and Services Tax

Builder Guilty of not passing benefit of ITC to purchasers of flats: NAA

Goods and Services Tax

Goods and Services Tax

No Profiteering as there was commensurate reduction in base price

Goods and Services Tax

Goods and Services Tax

Anti –Profiteering- Dealer cannot escape Responsibility on the ground that he does not have control over pricing

Goods and Services Tax

Goods and Services Tax