An assessee whose estimated tax liability justifies no tax deduction or deduction at a lower rate can apply to the Assessing Officer for a certificate permitting nil or lower TDS. The facility is available to all categories of taxpayers, including residents, non-residents, individuals, firms, and companies. The application must be filed online in Form 13 using a PAN and authenticated through a Digital Signature Certificate or Electronic Verification Code. The certificate can be sought only for specified categories of income covered under designated TDS provisions, including salaries, interest, dividends, rent, professional fees, contractor payments, certain payments to non-residents, e-commerce transactions, and specified purchases of goods. Once issued, the certificate is generally sent to the deductor and remains valid for the period specified by the Assessing Officer unless cancelled earlier. The process involves furnishing estimated income, tax liability, supporting documents, and relevant declarations through the TRACES portal.

Certificate of lower/no deduction of tax at source

An assessee can apply to the Assessing Officer to issue a nil or lower TDS certificate. Such certificate is issued if the estimated tax liability of the assessee justifies no deduction of tax or deduction of tax at a lower rate.

Introduction

An assessee can apply to the Assessing Officer to issue a nil or lower TDS certificate. Such certificate is issued if the estimated tax liability of the assessee justifies no deduction of tax or deduction of tax at a lower rate.

Who can apply for certificate?

The application to obtain the Nil or Lower TDS certificate can be filed by any person, i.e., resident, non-resident, individual, firm, domestic company, foreign company, etc.

Which incomes are eligible for no deduction /lower deduction certificate?

The assessee can apply to obtain this certificate in respect of the following incomes only:

• TDS from Salaries (Section 192)

• TDS from Interest on Securities (Section 193)

• TDS from Dividend (Section 194)

• TDS from Interest other than Interest on Securities (Section 194A)

• TDS from Payment to Contractors (Section 194C)

• TDS from Insurance Commission (Section 194D)

• TDS from commission on sale of lottery tickets (Section 194G)

• TDS from Commission or brokerage (Section 194H)

• TDS from Rent (Section 194-I)

• TDS from Fees for professionals or technical services (Section 194J)

• TDS from income in respect of units (Resident) (Section 194K)

• TDS from payment of compensation on compulsory acquisition of an immovable property (Section 194LA)

• TDS from Income Distributed by Business Trust1 (Section 194LBA)

• TDS from Income in respect of units of Investment Fund (Section 194LBB)

• TDS from Income in respect of investment in Securitization Trust (Section 194LBC)

• TDS from the payment made to a contractor or a professional by certain individuals or Hindu undivided family (Section 194M)

• TDS from the payment made to e-commerce participants (194-O)

• TDS from payment of certain sum for purchase of goods (Section 194Q) [applicable w.e.f 01-10-2024]

• TDS from payment of any other income to a Non-Resident (Section 195)

How to apply for this certificate?

The application for the issue of a Nil or Lower TDS certificate can be filed in Form No. 13. Such form can be filed online under Digital Signature or through Electronic Verification Code. PAN is mandatory to apply for this certificate. If the assessee doesn’t have PAN, he cannot apply to the Assessing Officer to issue such certificate.

Issue of certificate

The certificate for lower or nil deduction of tax shall be issued directly to the person responsible for deducting the tax, with advice to the person who made the application for issue of such certificate.

However, if the number of persons responsible for deducting the tax is likely to exceed 100 and the details of such persons are not available with the person making such application, the certificate may be issued to the applicant authorizing him to receive income after deduction of tax at a lower rate.

The certificate shall remain valid for such period as may be mentioned in that unless it is cancelled by the Assessing Officer before the expiry of that period.

Steps to file Form 13

Step 1: Visit the traces portal https://contents.tdscpc.gov.in/ and ‘Login’

Step 2: Login as a ‘Taxpayer’

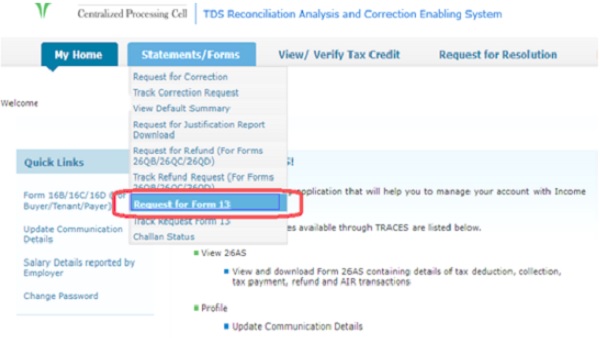

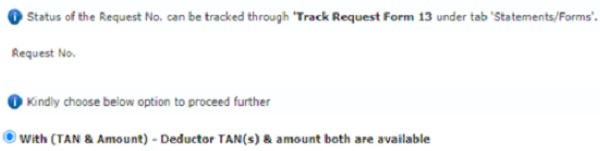

Step 3: On the next page, go to ‘Statement/Forms>Request for Form 13 ‘ from the dropdown menu.

Step 4: On the next screen, select your residential status to proceed.

Step 6: Select the relevant option from the dropdown of ‘Request Type‘ and ‘Financial Year‘ and click ‘Proceed’

Step 7: The request number will be generated

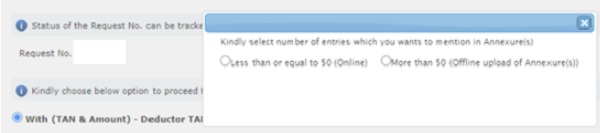

Step 8: Select the number of entries for which nil or lower TDS certificate is required.

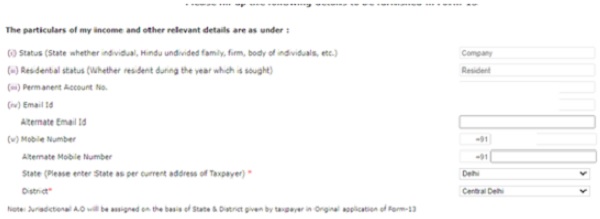

Step 9: Furnish the following details:

Point (i) to (v): Status, Residential Status, PAN, Email ID, and Mobile number shall be auto-filled. You need to select the state and district from the dropdown menu. Jurisdictional AO will be automatically assigned based on the State and District selected by the applicant.

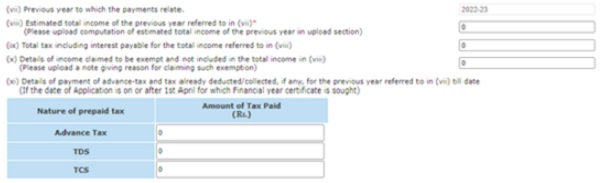

Point (vi): Details of existing liability under the Income-tax Act has to be provided:

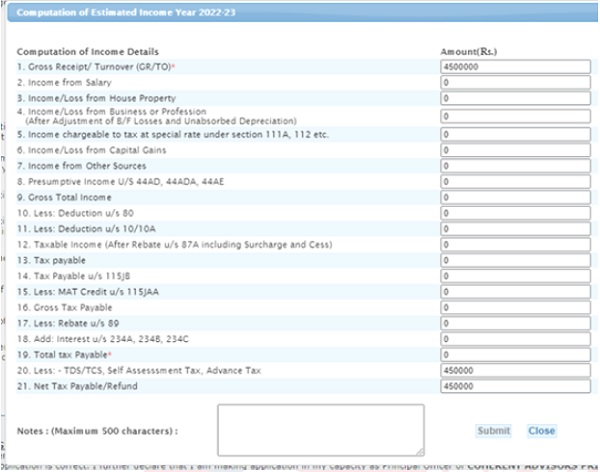

Point (vii) to Point (xi): Enter the estimated total income, total tax, details of income claimed to be exempt, and details of payment of advance tax and tax already deducted/collected.

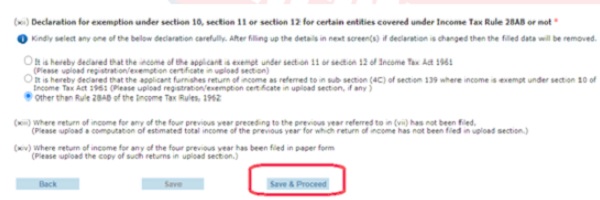

Point (xii):Select the declaration for exemption under Section 10, Section 11 or Section 12 for certain entities covered under Rule 28AB or not.

Step 10: Click ‘Save and Proceed‘

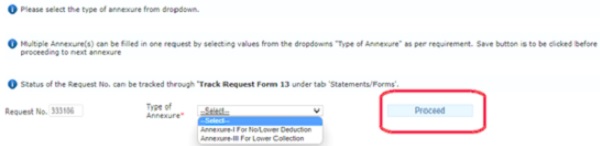

Step 11: Select the type of ‘Annexure‘ from the dropdown and click ‘Proceed’

Step 12: Fill the details in the ‘Annexure-I (No/Lower Deduction)‘ and click on ‘Save & Proceed’

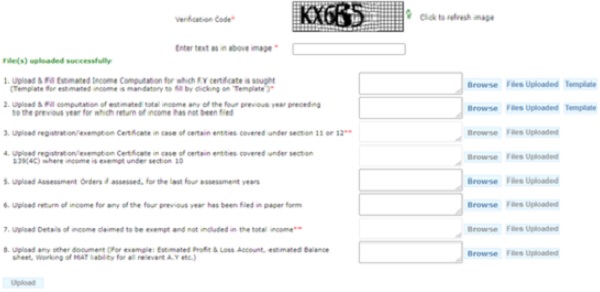

Step 13: Upload the required document by clicking ‘Browse‘. It is also mandatory to fill the template of estimated income.

–

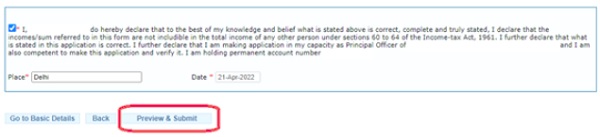

Step 14: Fill the declaration and click ‘preview and submit’

Step 15: Filled ‘ Form 13 ‘ will be displayed. If you want to edit the details, click on the ‘back button’ of the browser to go back to the previous screen. Else, proceed to ‘Submit’ the form.

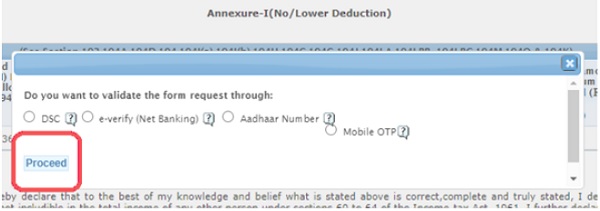

Step 16: Validate the form using the suitable option and proceed to submit the form.

MCQs on Certificate of lower/no deduction of tax at source

Q1. An assessee can apply to the Assessing Officer to issue a nil or lower TDS certificate if the estimated tax liability of the assessee justifies ___________.

(a) no deduction of tax

(b) deduction of tax at a lower rate

(c) Either (a) or (b)

(d) None of the above

Correct answer: (c)

Justification of the correct answer: An assessee can apply to the Assessing Officer to issue a nil or lower TDS certificate. Such certificate is issued if the estimated tax liability of the assessee justifies no deduction of tax or deduction of tax at a lower rate.

Q2. The application to obtain the Nil or Lower TDS certificate can be filed only by a resident person.

(a) True

(b) False

Correct answer: (b)

Justification of the correct answer: The application to obtain the Nil or Lower TDS certificate can be filed by any person, i.e., resident, non-resident, individual, firm, domestic company, foreign company, etc.

Q3. The assessee can apply to obtain this certificate for which of the following incomes?

(a) Rental income where tax is deductible under 194-I

(b) Rental income where tax is deductible under Section 194-IB

(c) Lottery income where tax is deductible under section 194B

(d) Withdrawal from Employee’s Provident Fund where tax is deductible under

(d) Withdrawal from Employee’s Provident Fund where tax is deductible under section 192A

Correct answer: (a)

Justification of the correct answer: The assessee can apply to obtain this certificate in respect of the rental income where tax is deductible under Section 194-I and not for rental income where tax is deductible under 194-IB, lottery income where tax is deductible under section 194B or withdrawal from employee’s provident fund where tax is deductible under

(d) Withdrawal from Employee’s Provident Fund where tax is deductible under section 192A

Q4. The application for the issue of a Nil or Lower TDS certificate can be filed in _______.

(a) Form 64

(b) Form 13

(c) Form 61A

(d) Form 10-IA

Correct answer: (b)

Justification of the correct answer: The application for the issue of a Nil or Lower TDS certificate can be filed in Form No. 13

Q5. The certificate shall remain valid for __________.

(a) 1 year

(b) 5 years

(c) As mentioned by the Assessing Officer in the certificate

(d) None of the above

Correct answer: (c)

Justification of the correct answer: The certificate shall remain valid for such period as may be mentioned in that unless it is cancelled by the Assessing Officer before the expiry of that period.

Notes:

1. Inserted by the Finance Act, 2023 with effect from 01.04.2023

Above document contains the provisions of the Income-tax Act, 1961, as amended by the Finance Act, 2026.

******

Disclaimer: The contents of this document are for information purposes only. This aims to enable public to have a quick and an easy access to information and do not purport to be legal documents. Viewers are advised to verify the content from Government Acts/Rules/Notifications etc.

(Republished with amendments)

At what time form 13 can be filed? Can one Non resident file it after execution and registration of sale deed for lower TDS ?