#NAA

Log in to FollowEvery article filed under the “NAA” tag — analysis, news and updates.

454 articlesGoods and Services Tax

Goods and Services Tax

Builder entitled to opt for paying GST @8%: NAA

Goods and Services Tax

Goods and Services Tax

Increase in base price of product, post-GST rate reduction is profiteering: NAA

Goods and Services Tax

Goods and Services Tax

Dealer not passed GST Rate reduction benefit on Sanitary napkin: NAA

Goods and Services Tax

Goods and Services Tax

NAA found Liberty Shoe dealer Guilty of Profiteering

Goods and Services Tax

Goods and Services Tax

‘Unicharm’ not passed tax reduction benefit on Sanitary Napkins: NAA

Income Tax

Income Tax

Benefit of reduction in rate of GST not passed; Anti Profiteering provisions contravened

Goods and Services Tax

Goods and Services Tax

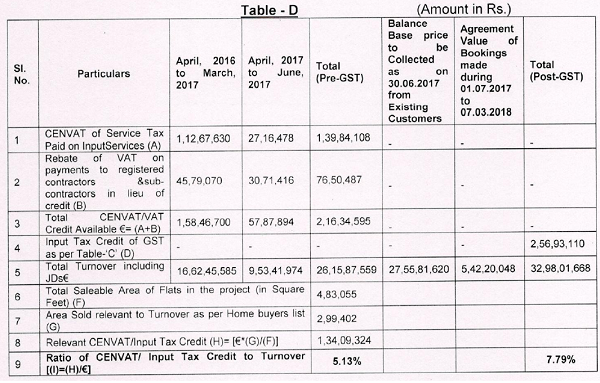

Builder realised more price by issuing incorrect tax invoices- Guilty of Anti-Profiteering

Goods and Services Tax

Goods and Services Tax

NAA tenure extended for 2 Years; Phased electronic invoicing system introduction; Decision on GSTAT

Goods and Services Tax

Goods and Services Tax

NAA found builder guilty of Additional GST realisation by issuing incorrect invoices

Goods and Services Tax

Goods and Services Tax