The Annual Information Statement (AIS), introduced under Section 285BB of the Income-tax Act, provides taxpayers with a comprehensive view of their financial information for a particular financial year. Accessible through the income-tax e-filing portal, AIS contains details relating to TDS and TCS, specified financial transactions, tax payments, demands and refunds, pending and completed proceedings, GST-related information, foreign remittances, interest on income-tax refunds, off-market transactions, dividends, mutual fund investments, and other information received from domestic or international authorities. The statement is intended to facilitate accurate return filing by enabling taxpayers to verify pre-filled information and compute their tax liability correctly. It also assists the tax authorities in cross-checking disclosures made in income-tax returns. Taxpayers can review AIS online or through an offline utility and submit feedback if the reported information is incorrect, duplicated, or pertains to another person.

Annual Information Statement (AIS)

Annual Information Statement (AIS) is a statement that provides complete information about the prepaid taxes and prescribed financial transactions entered into by taxpayer for a particular financial year. A taxpayer can access AIS information by logging into his income-tax e-filing account.

Annual Information Statement (AIS) is a statement that provides complete information about the prepaid taxes and prescribed financial transactions entered into by taxpayer for a particular financial year. A taxpayer can access AIS information by logging into his income-tax e-filing account.

What is Annual Information Statement (AIS)?

Section 285BB of the Income-tax Act provides that the Income-tax authority or any other person authorized on this behalf shall make available an Annual Information Statement to the assessee containing information on various financial transactions made by him during the year.

AIS has been introduced in the Income-tax Act to enlarge the scope of information to be made available to the assessee for filing of return of income. This information, on one hand, will be useful for the Assessing Officers to cross-check the details furnished in return for income by taxpayers. On the other hand, taxpayers would be able to easily compute their tax liability and file returns as all information would be pre-filled on basis of AIS.

Which types of information are covered in AIS?

Section 285BB read with rule 114-I of the Income-tax Rules, 1962 provides that the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) or any person authorised by him shall, upload such annual information statement in Form No. 26AS in the registered account of the assessee within 3 months from the end of the month in which the information is received. Such form shall consist of the following information:

a) Information relating to TDS and TCS;

b) Information relating to Specified Financial Transactions (SFT);

c) Information relating to the payment of taxes;

d) Information relating to demand and refund;

e) Information relating to pending proceedings;

f) Information relating to completed proceedings;

g) Information received from any officer, authority, or body performing any functions under any law or information received under an agreement referred under section 90or 90A;

h) Information relating to GST return;

i) Foreign remittance information reported in Form 15CC ;

j) Information in Annexure-II of the Form 24QTDS Statement of the last quarter;

k) Information in the ITR of other taxpayers;

l) Interest on Income Tax Refund;

m) Information in Form 61/61Awhere PAN could be populated;

n) Off Market Transactions Reported by Depository/Registrar and Transfer Agent (RTA);

o) Information about dividends reported by Registrar and Transfer Agent (RTA);

p) Information about the purchase of mutual funds reported by Registrar and Transfer Agent (RTA); and

q) Information received from any other person to the extent it may be deemed fit in the interest of the revenue.

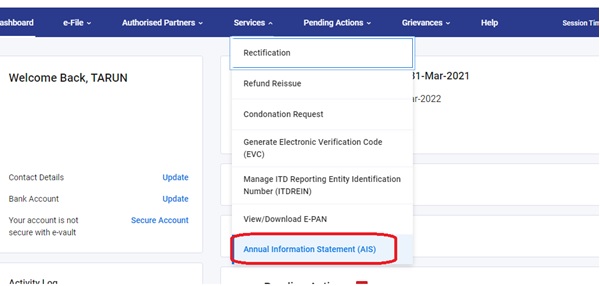

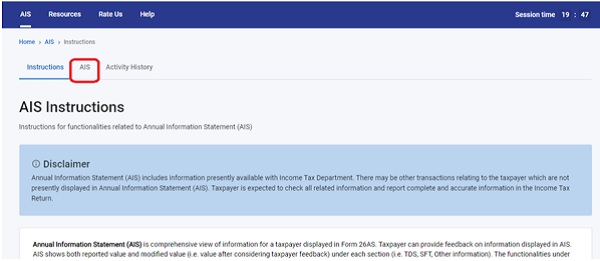

How to access AIS?

An assessee can access AIS information by logging into his income-tax e-filing account. If he feels that the information furnished in AIS is incorrect, duplicated, or relates to any other person, etc., he can submit his feedback thereon.

–

An assessee can access and respond to AIS information either directly from the income-tax e-filing portal or he can also use an offline utility.

MCQ on Annual Information System

Q1: Annual Information Statement (AIS) provides complete information about a taxpayer for ___________.

(a) a quarter

(b) a financial year

(c) a calendar year

(d) six months

Correct Answer: (b)

Justification of correct answer:

Annual Information Statement (AIS) is a statement that provides complete information about a taxpayer for a particular financial year. It contains information about taxpayers’ incomes, financial transactions, tax details, income-tax proceedings, etc.

Q2: Who is the prescribed authority for uploading the information in AIS?

(a) Principal Director General of Income-tax (Systems)

(b) Director General of Income-tax (Systems)

(c) Any person authorised by (a) and (b)

(d) All of the above

Correct Answer: (d)

Justification of correct answer:

Section 285BB read with rule 114-I of the Income-tax Rules, 1962 provides that the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) or any person authorised by him shall upload certain specified information as available with them in the annual information statement.

Q3: AIS contains information relating to ___________.

(a) TDS and TCS

(b) Dividends reported by Registrar and Transfer Agent (RTA)

(c) Specified Financial Transactions (SFT)

(d) All of the above

Correct Answer: (d)

Justification of correct answer:

Annual Information statement contains the following information in respect of an assessee about all the above-mentioned options i.e., TDS and TCS, Dividends reported by Registrar and Transfer Agent (RTA), and Specified Financial Transactions (SFT) for a particular financial year.

Q4: Which of the following information is required to be uploaded in AIS by DGIT (System) within 3 months from the end of the month in which the information is received?

(a) Information relating to TDS and TCS

(b) Information relating to foreign remittance details reported in Form 15CC

(c) Both (a) and (b)

(d) None of the above

Correct Answer: (b)

Justification of correct answer:

The CBDT has authorised the Director General of Income-tax (Systems) to upload information relating to points (h) to (p) given above in the AIS within 3 months from the end of the month in which the information is received by him. Such points include information relating to foreign remittance information reported in Form 15CC .

Q5: In case of any deficiency in AIS, a taxpayer can submit feedback through which portal?

(a) Income Tax Department (https://www.incometaxindia.gov.in.)

(b) e-Filing website (https://www.incometax.gov.in/iec/foportal/)

(c) TRACES Website (https://contents.tdscpc.gov.in/ )

(d) Reporting Portal (https://report.insight.gov.in/reportingwebapp/portal/homePage)

Correct Answer: (b)

Justification of correct answer:

An assessee can access AIS information by logging into his income-tax e-filing account. If he feels that the information furnished in AIS is incorrect, duplicated, or relates to any other person, etc., he can submit his feedback thereon.

Q6: An assessee can access and respond to AIS information _________.

(a) Online through income-tax e-filing portal

(b) Through offline utility

(c) Both (a) and (b)

(d) None of the above

Correct Answer: (c)

Justification of correct answer:

An assessee can access and respond to AIS information either directly from the income-tax e-filing portal or he can also use an offline utility.

Above document contains the provisions of the Income-tax Act, 1961, as amended by the Finance Act, 2026.

*******

Disclaimer: The contents of this document are for information purposes only. This aims to enable public to have a quick and an easy access to information and do not purport to be legal documents. Viewers are advised to verify the content from Government Acts/Rules/Notifications etc.

(Republished with amendments)

While AIS is supposed to HELP Tax payer , to whom do I complain / report about a FALSE

INFORMATION in SFT-17 ? The info indicates

Rs 49. 93 Lacs , for purchase of securities in the quarter July -Sept. of FY 2023, which DOES NOT PERTAIN to me. My Demat agency also declares NO SUCH TRANSACTION has

happened in my account .