Introduction

Imagine earning ₹10–15 lakhs a year from your farmland and legally paying zero income tax on it. Sounds incredible, right? But there’s a twist, this same agricultural income can influence the tax rate on your other earnings. Welcome to the world of agricultural income taxation in India, where constitutional provisions, statutory definitions, judicial interpretations, and practical tax rules all come into play. In this blog, we will break down agricultural income in India , from legal definitions and exemptions to real-life examples and landmark court cases in a way that’s both insightful and easy to understand.

1. Constitutional and Legal Basis

In India, the power to levy taxes is divided between the Central Government and the State Governments through the Constitution. Specifically, agricultural income falls under the jurisdiction of State Governments as per Entry 46 of the State List (7th Schedule). This means that states have the authority to tax income derived from agriculture.

However, in practice, the Central Government provides a tax exemption for agricultural income under Section 10(1) of the Income Tax Act, 1961. This means that if you earn income from agriculture in India, it is not directly taxed by the Central Government.

At the same time, agricultural income is not completely ignored for tax purposes. While it is exempt from direct taxation, it is taken into account when determining the tax rate on your other income, such as salary, business profits, or interest. This is known as the “partial integration” mechanism, which ensures that higher agricultural earnings can affect the rate of tax applied to non-agricultural income, even though the agricultural income itself remains tax-free.

In short, agricultural income in India has a special status:

- States can tax it if they choose.

- Central tax laws exempt it.

- It can still influence your overall tax rate through integration with other taxable income.

2. What is “Agricultural Income”? — Section 2(1A)

Agricultural income is specifically defined under Section 2(1A) of the Income Tax Act, 1961. It refers to income that is earned directly from agricultural activities or from land used for agriculture in India. Not all income from land qualifies — the key is that the income must arise from genuine agricultural operations.

According to Section 2(1A), agricultural income includes:

1. Rent or revenue from agricultural land in India

- This is the money earned by letting out farmland or from the produce grown on it.

- Example: If a farmer leases 10 acres of farmland to another person and receives ₹2 lakhs as rent for cultivation, this is considered agricultural income.

2. Income from agricultural operations, including processing produce to make it marketable

- Income from growing crops, horticulture, or other agricultural produce qualifies. It also includes activities essential to make the produce ready for sale, such as cleaning, grading, or simple processing.

- Example: Cleaning and packaging vegetables grown on your land for sale in the market.

3. Income from a farmhouse, subject to conditions

- If a farmhouse is used for agricultural purposes, income derived from it may be treated as agricultural income.

- Example: Renting out a farmhouse for storage of crops or agricultural activities may qualify.

4. Income from saplings, seedlings, or horticultural plants grown in a nursery

- This includes income from selling plants, seedlings, or trees raised for agricultural purposes.

- Example: A nursery growing saplings for sale to farmers qualifies under agricultural income.

3. Examples: What Is and Is Not Agricultural Income

| Agricultural Income (Exempt) | Non‑Agricultural (Taxable) |

| Sale of crops grown on land | Sale of processed food products |

| Rent from agricultural land | Rent from farmland used for non‑agri business |

| Income from saplings/seedlings | Dairy product manufacturing beyond basic farming |

| Income from horticulture | Poultry farming |

| Share of profit from a farm firm (proportionate) | Salary from Agri‑based firm unrelated to agri operations |

| (Based on definitions under Sections 2(1A) & 10(1)) |

4. Exemption Under the Law — Section 10(1)

- Agricultural income, as defined under Section 2(1A) of the Income Tax Act, 1961, is fully exempt from income tax under Section 10(1). This means that any income earned from genuine agricultural activities in India, such as rent from farmland, cultivation of crops, horticulture, or income from a farmhouse used for agricultural purposes, is not directly taxable.

- However, this exemption applies only to income generated within India, and agricultural income earned abroad may be subject to regular taxation. While the income itself is exempt, it is not entirely ignored for tax purposes ,it is considered when determining the applicable tax rate on other sources of income, such as salary or business profits, through the partial integration mechanism.

- For instance, if a farmer earns ₹6 lakhs from crops and ₹2 lakhs from freelance work, the agricultural income does not get taxed directly but may slightly increase the tax rate on the ₹2 lakhs of freelance income. The rationale behind this exemption is to recognise the importance of agriculture in India and to ensure that individuals who rely on farming are not overburdened by taxes, while maintaining fairness in the taxation of other income sources.

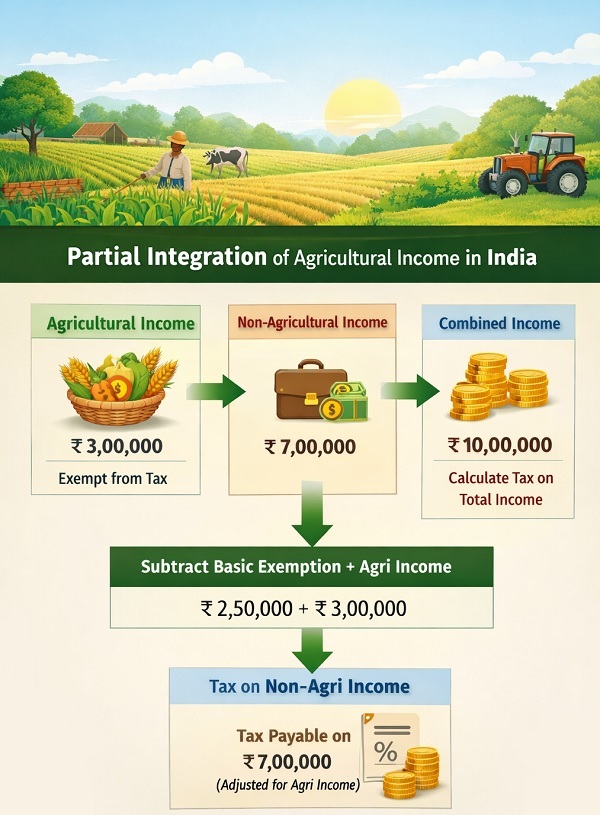

5. Partial Integration — When Agricultural Income Affects Your Tax

Although agricultural income is fully exempt from direct taxation under Section 10(1), it can still influence the tax liability on other sources of income through a mechanism called partial integration. This rule is designed to ensure that individuals with significant agricultural income are taxed fairly on their non-agricultural earnings. Partial integration applies only when certain conditions are met: the agricultural income exceeds ₹5,000 in a financial year, the total non-agricultural income exceeds the basic exemption limit (₹2.5 lakhs under the old regime or ₹4 lakhs under the new regime), and it applies only to individuals, Hindu Undivided Families (HUFs), Associations of Persons (AOPs), or Bodies of Individuals (BOIs), but not to firms or companies.

The computation under partial integration involves a few steps. First, the total of agricultural income and non-agricultural income is calculated to determine the tax liability on the aggregate. Then, the agricultural income is added to the basic exemption limit, and tax is computed again. The difference between these two calculations represents the tax payable on the non-agricultural income, adjusted for the agricultural component. Finally, applicable cess, such as Health and Education Cess at 4%, is added to arrive at the total tax liability.

Example: Suppose a person earns ₹3,00,000 from agriculture and ₹7,00,000 from salary in the same financial year. The total income of ₹10,00,000 is first considered for tax calculation. Next, the agricultural income of ₹3,00,000 is added to the basic exemption limit, and tax is computed again. The difference between these two computations represents the additional tax payable on the salary, reflecting the impact of agricultural income on the overall tax rate, even though the agricultural income itself remains exempt.

Partial integration is an important concept because it balances exemption for farmers with equitable taxation of other income, ensuring fairness in the income tax system while acknowledging the unique nature of agricultural earnings.

6. Special Rules for Mixed Agri & Business Activities

Under Income‑tax Rules (e.g., Rule 7, Rule 7A, Rule 8), some activities are partly agricultural and partly non-agricultural, like:

| Activity | Agricultural Portion | Business Portion |

| Coffee grown & cured | 75 % | 25 % |

| Coffee roasted & ground | 60 % | 40 % |

| Tea grown & manufactured | 60 % | 40 % |

| Rubber latex processed | 65 % | 35 % |

| (As per tax rules and judicial interpretations) |

This affects how much of the income is exempt and how much is taxable.

7. Judicial Interpretations and Landmark Cases on Agricultural Income

In Raja Benoy Kumar Sahas Roy vs. CIT AIR 1957 SC 873 The Supreme Court clarified the fundamental meaning of agriculture under the Income Tax Act. It held that agricultural income must arise from actual cultivation or operations on land, involving human effort and management. Merely owning land or earning rent from it does not automatically qualify unless genuine agricultural operations are carried out. This case laid the foundation for determining what constitutes agricultural income for tax exemption purposes.

In Namdhari Seeds vs. CIT (2018) 10 SCC 7, the Supreme Court held that income from the sale of seeds, fruits, and vegetables grown on agricultural land is considered agricultural income. The court emphasised that produce directly derived from cultivation qualifies for exemption under Section 2(1A). It reinforced that even if agricultural produce is sold commercially, the income retains its agricultural character as long as it is a result of genuine cultivation.

In Shiv Shankar Lal vs. CIT 1977 109 ITR 191 (SC), The court ruled that rent or lease income from agricultural land is considered agricultural income, even if the owner is not personally engaged in cultivation. The judgment highlighted that the agricultural nature of land determines the tax treatment of income. This case established that the mere leasing of agricultural land for cultivation retains the agricultural income exemption under Section 10(1).

Similiarly in Raza Buland Sugar Co vs. CIT 1980 122 ITR 354 (SC), The Supreme Court clarified that income derived from the sale of sugarcane grown on agricultural land qualifies as agricultural income. The judgment stressed that income from crops directly tied to cultivation activities, including commercial crops, is exempt. This decision reinforced that the exemption applies to farmers and entities involved in genuine agricultural operations, maintaining the principle of partial integration where applicable.

8. Do’s and Don’ts for Taxpayers

Do:

- Declare agricultural income if it exceeds ₹5,000 in your ITR.

- Maintain evidence: land documents, receipts, invoices.

- Understand the partial integration impact if you have other income.

Don’t:

- Assume all land sale proceeds are exempt ,capital gains may apply, especially for urban or non-agricultural land.

- Ignore computing tax on non-agricultural income with respect to slabs.

- Claim dairy/poultry income as agricultural if it involves significant processing.

9. Conclusion

Agricultural income in India enjoys a special status; it is fully exempt under Section 10(1) of the Income Tax Act, yet it can influence the tax liability on other earnings through the partial integration mechanism. Understanding what qualifies as agricultural income, keeping proper records, and being aware of mixed agricultural-business activities are essential for accurate tax compliance. This system not only supports farmers and encourages agricultural activity but also ensures fairness in taxation for individuals with multiple income sources. By following the legal provisions and guidelines, taxpayers can benefit from exemptions while remaining fully compliant with the law.

References

- The Constitution of India, 1950, Seventh Schedule, Entry 46, State List.

- The Income-tax Act, 1961, No. 43 of 1961, Sections 2(1A), 2(2), 10(1), Government of India, Ministry of Finance.

- Income-tax Rules, 1962, Rule 7, Rule 7A, Rule 8, Government of India, Ministry of Finance.

- Raja Benoy Kumar Sahas Roy v. Commissioner of Income-tax, AIR 1957 SC 873.

- Namdhari Seeds v. Commissioner of Income-tax, (2018) 10 SCC 7.

- Shiv Shankar Lal v. Commissioner of Income-tax, (1977) 109 ITR 191 (SC).

- Raza Buland Sugar Co v. Commissioner of Income-tax, (1980) 122 ITR 354 (SC).

- Lakshmanan & Co v. Commissioner of Income-tax, (1996) 220 ITR 172 (SC).

- N. Manoharan & R. Natarajan (Eds.), Income Tax Law & Practice, Latest Edition, Snow White Publications, 2023.

- S. Datey, Indirect Taxes and Direct Taxes: Law and Practice, 24th Edition, Taxmann Publications, 2022.

- TaxGuru, “Partial Integration of Agricultural Income Explained,” Available at: https://www.taxguru.in, Accessed on: 17 Feb. 2026