Case Law Details

Baba Metalics Private Limited Vs ITO (ITAT Kolkata)

In a combined ruling involving reassessment proceedings and addition under Section 68 of the Income-tax Act, the Kolkata Bench of the Income Tax Appellate Tribunal (ITAT) allowed both appeals filed by the assessee for Assessment Year 2012-13. The Tribunal held that reassessment proceedings initiated on the basis of incorrect and mechanically recorded reasons were invalid, and further ruled that additions towards share capital and share premium could not be sustained where the assessee had furnished documentary evidence establishing the identity, creditworthiness, and genuineness of investors.

In ITA No. 455/KOL/2025, the dispute concerned the reopening of assessment under Sections 147 and 148 of the Income-tax Act. The assessee had originally filed its return declaring nil income, and an assessment under Section 143(3) was completed assessing total income at ₹7.84 crore. Subsequently, reassessment proceedings were initiated and an addition of ₹10 lakh was made as unexplained money.

During appellate proceedings, the assessee argued that the reasons supplied for reopening did not relate to it but instead pertained to another company, M/s Balaji Polytex Industries Pvt. Ltd. The assessee informed the Assessing Officer that the reopening had been initiated on the basis of incorrect reasons. Thereafter, fresh reasons were supplied. The Tribunal observed that the reasons had been recorded by one officer, while the notice under Section 148 was issued nearly a year later by another officer. The Tribunal held that the notice issued after such delay, following recording of reasons and approval, was bad in law and unsustainable.

The Tribunal further noted that the Assessing Officer had merely reproduced information received from the Directorate of Investigation and stated satisfaction in a single line without independently applying his mind to the material. According to the Tribunal, the reopening was based on “borrowed satisfaction” and the reasons were recorded mechanically. Relying on judicial precedents including PCIT vs. Meenakshi Overseas Pvt. Ltd., CIT vs. SFIL Stock Broking Ltd., GRD Commodities Ltd. vs. PCIT, PCIT vs. Shodiman Investment Pvt. Ltd., and Sarthak Securities Co. Pvt. Ltd. vs. ITO, the Tribunal quashed the reassessment proceedings and allowed the assessee’s appeal.

In ITA No. 419/KOL/2025, the issue related to addition of ₹7.87 crore under Section 68 in respect of share capital and share premium received by the assessee. The assessee had issued 39,385 equity shares at a face value of ₹10 with a premium of ₹1,990 per share. During assessment proceedings, the assessee furnished names, addresses, PAN details, bank statements, audited financial statements, confirmations, and source-of-funds documents relating to the share subscribers. Notices under Sections 131 and 133(6) were also issued by the Assessing Officer to certain subscribers, and replies along with supporting documents were furnished by them.

Despite receipt of replies and supporting evidence, the Assessing Officer treated the share capital and share premium as unexplained cash credit on the ground that there was no personal appearance by some subscribers. The Commissioner (Appeals) affirmed the addition.

The Tribunal observed that the Assessing Officer had not discussed the replies received under Section 133(6) or the compliance made pursuant to summons under Section 131. It held that once the assessee had furnished all relevant evidence regarding the investors, the addition could not be sustained merely because there was no personal appearance by directors or subscribers. The Tribunal stated that the assessee had complied with notices and summons by filing documentary evidence supporting the transactions, including audited accounts, confirmations, and bank statements.

The Tribunal relied extensively on recent Calcutta High Court rulings, including PCIT vs. Bright Commodeal Pvt. Ltd. and Principal Commissioner of Income Tax vs. Shipra Enclave Pvt. Ltd. In those decisions, the High Court held that where investors were identifiable taxpayers who responded to notices under Section 133(6) and transactions were supported through banking channels and documentary records, additions under Section 68 could not be justified merely due to non-appearance of directors. The High Court also emphasized that suspicion could not replace evidence and distinguished such cases from PCIT vs. NRA Iron & Steel (P) Ltd., which dealt with non-existent or phantom entities.

Referring to these precedents, the Tribunal concluded that the assessee had discharged the burden of proving identity, creditworthiness, and genuineness of the investors. It held that documentary traceability through PAN details, income tax returns, audited financial statements, and banking records carried greater evidentiary value than mere suspicion regarding the transactions. Accordingly, the Tribunal set aside the order of the Commissioner (Appeals) and directed deletion of the addition under Section 68. Both appeals of the assessee were allowed.

FULL TEXT OF THE ORDER OF ITAT KOLKATA

These are appeals preferred by the assessee against the order of the National Faceless Appeal Centre, Delhi (hereinafter referred to as the “Ld. CIT(A)”] dated 08.01.2025 for the AY 2012-13.

ITA No. 455/KOL/2025

2. At the time of hearing, the counsel of the assessee pressed ground no.3, which is extracted below:-

“3. Considering the facts and circumstances of the case and the applicable provisions of law, it is submitted that the Learned CIT(A) erred in concluding that the appellant failed to establish the identity, creditworthiness, and genuineness of the sums credited in the books of accounts. In contrast, all relevant and material documents, including responses from shareholders to notices issued u/s 133(6) of the Act, were duly furnished to the Ld. CIT (A) during appeal proceeding. Despite this, the Ld. CIT(A), grossly erred on confirming additions to the total income and displaying a predetermined bias, disregarded each submission, record, document, and response provided-contravening principles of natural justice and fairness. Consequently, the order of the Learned CIT(A) is void and unsustainable in law.”

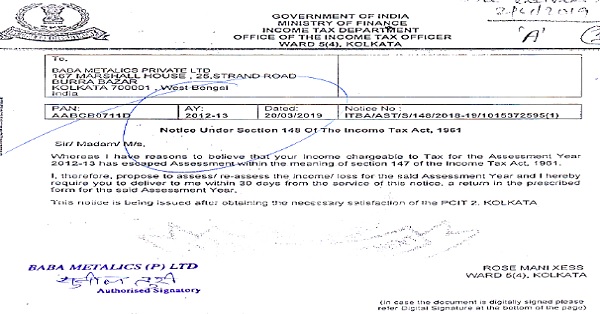

3. The facts in brief are that the assessee filed the return of income on 27.08.2012, declaring total income at ₹ nil. The case of the assessee was selected for scrutiny and assessment u/s 143(3) of the Act was framed vide order dated 31.03.2015 assessing the total income at ₹7,84,95,800/-. Thereafter, the case of the assessee was reopened u/s 147 of the Act by issuing notice u/s 148 of the Act on 20.03.2019 after obtaining approval u/s 151 of the Act from the competent authority. The reasons recorded are extracted by the ld. AO on page no.1 of the assessment order. Thereafter, when there was no compliance from the assessee’s side, the assessment was framed by the order dated 26.11.2019, u/s 144/ 147 of the Act assessing the total income at ₹7,94,96,800/- after making an addition of ₹10,00,000/- on account of unexplained money.

4. In the appellate proceedings, dismissed the appeal of the assessee.

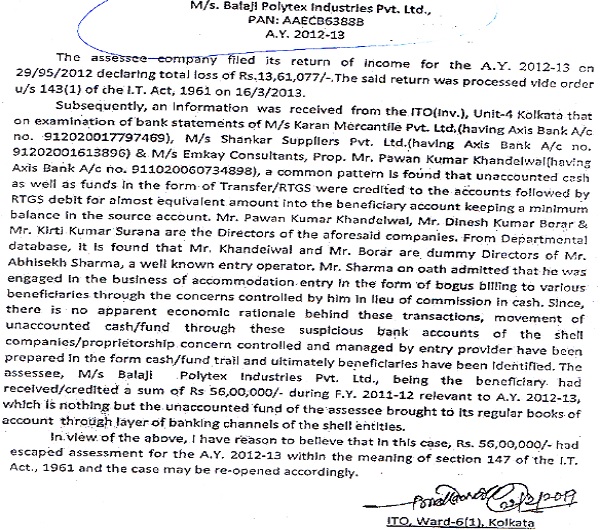

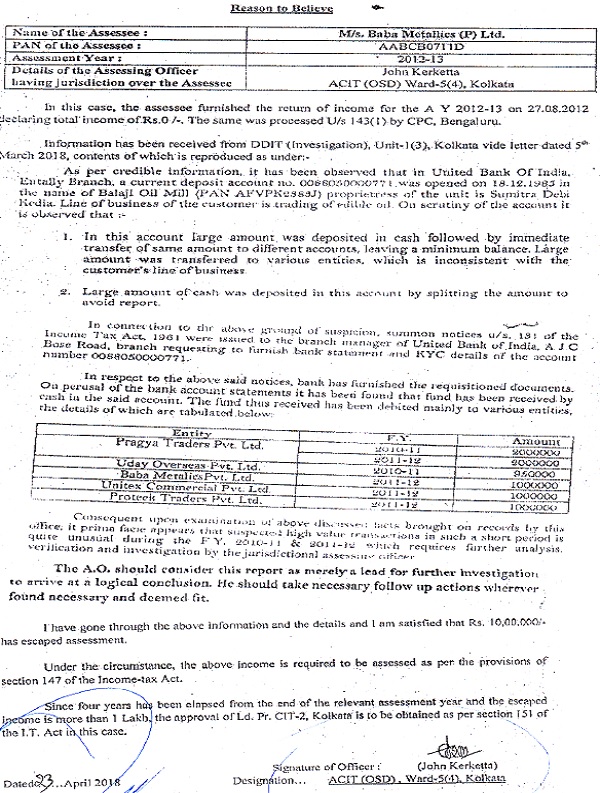

5. After hearing the rival contentions and perusing the materials available on record, we find that the notice u/s 148 of the Act was issued on 28.03.2019. The reasons were supplied to the assessee vide letter dated 15.10.2019, which is available at page no.3 of the paper book, which read as under:-

5.1. We note that the said reasons were relating to the different assessee i.e. M/s Balaji Polytex Industries Pvt. Ltd. Accordingly, the assessee pointed out to the ld. AO vide letter dated 02.11.2019, that copy of reasons recorded was not belonging to the assessee and the same belonged to M/s Balaji Polytex Industries Pvt. Ltd. and therefore, reopening has been made on the basis of wrong reasons recorded. Thereafter, the ld. AO again supplied the reasons on 19.11.2019, which are available at page no.6 and 7 of the Paper Book, which read as under:-

5.2. We find from the perusal of the said reasons that the ld. AO who recorded the reasons on 23.04.2018, is Mr. John Kerketta, ACIT (OSD), Ward 5(4), Kolkata, whereas the notice u/s 148 of the Act was issued originally on 20.03.2019, by ITO Ward 5(4) Kolkata, Mr. Rose Mani Xess, which read as under:-

5.3. Therefore, the said notice is issued u/s 148 of the Act was issued almost a year after recording rthe reasons and obtaining the approval which is bad in law and cannot be sustained.

5.4. Moreover, from the reasons recorded above it is clear that the AO has extracted the report received from the DDIT (Investigation) Unit1(3) Kolkata and thereafter merely by recording one line that “I have gone through the above information and details and I am satisfied that income of the assessee of ₹ 10,00,000/- has escaped assessment.” In our opinion the AO has not recorded his own satisfaction as to how the income has escaped assessment but relied on the DDIT report as it is. In our opinion the reasons have been recorded in a mechanical manner without application of mind by the AO which at best can be considered as borrowed satisfaction of the Assessing Officer. I our considered opinion the re-opening of assessment can not mbe made on the basis of borrowed satisfaction. The case of the assessee finds support from the decision in the case PCIT Vs Meenakshi Overseas Pvt Ltd (2017) 82 taxmann.com 300 (Del). In the said decision, Hon’ble Delhi High Court has held that where the reasons to believe contain not the reasons but the conclusions of the AO one after the other and there was no independent application of mind by the AO to the tangible material which forms the basis of the reasons to believe that income has escaped assessment. The Hon’ble High Court has held that the conclusions of the AO are at best a reproduction of the conclusion in the investigation report. Indeed it is a borrowed satisfaction. Besides the case of the assessee is squarely covered by the decisions of CIT vs. SFIL Stock Broking Ltd. in [2010] 325 ITR 285 (Del) ,GRD Commodities Ltd Vs PCIT (2023) 149 taxmann.com 223(Cal), PCIT Vs Shodiman Investment Pvt Ltd (2018) 93 taxmann.com 153 (Bom) and Sarthak Securities Co Pvt Ltd. Vs ITO (2010) 329ITR 110(Del).Consequently, we quash the reopening of assessment. The ground no. 3 is allowed.

6. The other ground raised are not being adjudicated at this stage and are being left open to be decided at later stage if need arises for the same.

7. The appeal of the assessee in ITA No. 455/KOL/2025 is allowed.

ITA No. 419/KOL/2025

8. The only issue raised in the various grounds of appeal is against the confirmation of addition of ₹7,87,70,000/- by the ld. CIT (A) as made by the AO u/s 68 of the Income-tax Act, 1961 in respect of share capital / share premium.

9. The facts in brief are that the assessee filed the return of income on 27.08.2012, declaring total loss of ₹3,34,482/-, which was processed u/s 143(1) of the Act. Later, the case of the assessee was selected for scrutiny under Computer Assisted Scrutiny Selection (CASS) and notice u/s 143(2) and 142(1) of the Act along with questionnaire were duly served upon the assessee. The assessee furnished before the ld. AO the details/ documents along with books of accounts which were test checked and verified by the ld. AO as stated in Para no.3. The ld. AO observed from the balance sheet that the assessee has issued 39,385 equity shares at a face value of ₹10 each at a premium of ₹1990/- thereby collecting total amount of ₹7,87,70,000/- as share capital/ share premium. The ld. AO also issued summon u/s 131 of the Act to two subscribers namely; Prateek Niketan Pvt. ltd. and Mojjika Steels Pvt. ltd. which were duly replied by the said parties. The ld. AO also issued notice u/s 133(6) of the Act to the share subscribers, which were also replied by the subscribers by furnishing all the necessary evidences and details as called for thereby confirming the transactions of investment in the assessee company. Thereafter, the ld. AO issued show cause notice which according to the ld. AO was not replied and finally, he treated the share capital/ share premium of ₹7,87,70,000/- as unexplained cash credit and added to the income of the assessee in the assessment framed u/s 143(3) of the Act dated 31.03.2015.

10. In the appellate proceedings, the ld. CIT (A) simply affirmed the order of the ld. AO and confirmed the addition.

11. After hearing the rival contentions and perusing the materials available on record, we find that undisputedly during the year the assessee has issued 39,385 equity shares face value of ₹10 each at a premium of ₹1990/- thereby collecting ₹7,87,70,000/- during the year. We note that assessee has furnished all the evidences qua the subscribers. We note that the assessee filed before the ld. AO the names, addresses, PANs of share subscribers including the equity shares allotted , premium received, total amount received, copies of bank statements, statement of sour of funds, copy of audited balance sheets along with confirmations. We also note that the notices were issued u/s 131 of the Act to two subscribers namely; Prateek Niketan Pvt. ltd. and Mojjika Steels Pvt. ltd., which were replied by the said subscribers. The copies of the summons along with reply were available at page no. 62 to 81. However, there was no personal appearance by the subscribers. The ld. AO also issued letters u/s 133(6) of the Act to nine subscribers which were replied by the subscribers by furnishing all the details and evidences such as copy of audited accounts, bank statements and confirmations etc. However, the ld. AO has not discussed about the issuance of notice u/s 133(6) of the Act, receiving of replies from the subscribers. Similarly, the ld. AO did not discuss anything about compliance made to summons u/s 131 of the Act by two subscribers who submitted their replies before the ld. AO along with evidences. Under these circumstances, we are of the view that the addition made by the ld. AO and as sustained by the ld. CIT (A) is not sustainable in the eyes of law. In our opinion, once the assessee furnished all the details/ evidences qua the share subscribers, the addition cannot be made on the ground that there was no compliance to the summons u/s 131 of the Act or non-compliance to notice issued u/s 133(6) of the Act. The case of the assessee stands on better foot as the assessee complied with the summons as well as the notice issued u/s 133(6) of the Act by filing all the details/ evidences qua the investment made in the assessee company. Therefore, the order of the ld. CIT (A) upholding the order of the ld. AO cannot be sustained.

11.1. The case of the assessee is also supported by the decision of the Hon’ble Calcutta High Court in the case of PCIT vs. Bright Commodeal Pvt Ltd (ITAT No. 162 of 2025) dated 28.08.2025, wherein, it was held as under:

“We have perused the reasons assigned by the learned Tribunal for allowing the assessee’s appeal. It is seen that the assessing officer issued notice under Section 133 (6) of the Act to the investing companies and both the parties have complied with the said notice and furnished the requisite details.

Summons under Section 131 of the Act was issued to the Director of the assessee company to be personally present and also to produce the Directors of the investing company for examination of genuineness of the transaction, identity and creditworthiness of the lenders. The Tribunal noted that the Directors appeared pursuant to the summons but the assessing officer wrongly recorded that the Directors of the assessee company failed to appear in response to the summons issued under 131 of the Act.

Furthermore, the Tribunal examined the factual position and noted that the assessee has filed evidences as called for by the assessing officer in respect of the assessee as well as the investing companies. The evidences filed comprised of income tax retums, audited balance sheet, profit and loss account, audited report, bank statement and master data in respect of each of the subscribers. Furthermore, both the parties have submitted their reply pursuant to the notice issued under Section 133(6) of the Act. After noting these facts, the Learned Tribunal held that the assessing officer as well as the CIT(A) did not cause any verification or conduct any enquiry into the evidences which were filed by the assessee and merely harped on noncompliance of the summons issued under Section 131 of the Act, which is factually incorrect.

Learned Tribunal placed reliance on the decision of the Hon’ble Supreme Court in CIT-Vs- Orissa Corporation Ltd. (1986) 159 ITR 78 (SC) as well as the decision of this Court in Crystal Networks Pvt. Ltd. -Vs- CIT, (353) ITR 171 (Cal). The Tribunal also noted the decision of the Co-ordinate Bench in the case of ITO -VS- M/S Cygnus Developers India Pvt. Ltd. (ITA/282/Kol/2012) wherein the factual position was also similar to that of the case of the assessee.

Thus, we find that the facts have been examined by the Tribunal and the conclusion has been arrived at and therefore, no question of law, much less substantial questions of law, arises for consideration in this appeal.”

11.2. The decision of the jurisdictional Hon’ble Calcutta High Court in the case of Principal Commissioner Of Income Tax 1 vs M/S Shipra Enclave Pvt Ltd ITAT 94 OF 2025 also squarely applies to the assessee. In this case the facts were that the assessee had raised share capital and premium from fifteen corporate entities. During scrutiny assessment, the assessee produced comprehensive documentary evidence including PAN details, Income-tax return acknowledgements, bank records, and audited financial statements of all subscriber companies. Despite the availability of such material, the Assessing Officer issued summons under Section 131 to the directors of the subscriber companies and, upon their non-appearance, treated the entities as “shell companies” and added 26.22 crore as unexplained cash credit under Section 68, which was affirmed by the CIT(A). The Tribunal reversed the addition after noting that all subscriber companies were active taxpayers who had responded to notices issued under Section 133(6) and confirmed the transactions conducted through banking channels. Before the High Court, the Revenue argued that the low income declared by the investors compared to the high share premium suggested accommodation entries, relying on the Supreme Court judgment in PCIT v. NRA Iron & Steel (P) Ltd.However, the Court held that the assessee had discharged its burden under Section 68 by establishing the identity, creditworthiness, and genuineness of the investors through strong documentary evidence. The Court further held that the non-appearance of directors could not invalidate documented transactions, especially when the AO had powers under Section 131 to enforce attendance. Distinguishing NRA Iron & Steel, the Court observed that the said judgment applies to phantom or non-existent entities, whereas the present investors were identifiable taxpayers who confirmed the transactions. Emphasizing that suspicion cannot replace evidence, the Court upheld the Tribunal’s findings and dismissed the Revenue’s appeal, holding that no substantial question of law arose. It was held:

3. The factual matrix, as can be gleaned from the records, reveals that the respondent-assessee is a Non-Banking Financial Company (NBFC) duly registered with the Reserve Bank of India. For the relevant Assessment Year, its retum was selected for scrutiny specifically to examine the receipt of a large share premium. During the assessment proceedings, the Assessing Officer (AO) noted that the assessee had raised share capital and premium from fifteen corporate entities.

4. It is seen from the record that the assessee had placed before the AO a voluminous “Paper Book” containing all requisite documents, including PAN details, Income Tax Retum acknowledgments, and audited financial statements of all fifteen subscriber companies. Notwithstanding the availability of this documentary evidence, the AO issued summons under Section 131 of the Act to the directors of these companies. When they failed to appear personally, the AO proceeded to brand these companies as “shell entities” and added the entire amount of Rs 6,22,00,000/- as unexplained cash credit. This view was subsequently affirmed by the CIT (Appeals).

5. The leamed Tribunal, however, reversed this finding, noting that the subscribers were active taxpayers who had confirmed the transactions in response to notices issued under Section 133(6) of the Act.

6. We have heard Mr. Soumen Bhattacharjee, learned Advocate for the Revenue, and Mr. S.M Surana, learned Advocate for the respondent-assessee.

7. Bhattacharjee strenuously argued that the meagre income declared by the subscriber companies, when contrasted with the high premium paid to acquire the shares of the assessee, leads to an irresistible conclusion that the transactions were mere accommodation entries. He relied heavily on the decision of the Hon’ble Supreme Court in PCIT vs. NRA Iron & Steel (P) Ltd. and contended that the AO was justified in looking behind the “paper trail” to ascertain the true creditworthiness of the investors and genuineness of the transaction.

8. Per contra, Mr. Surana, learned Advocate for the assessee, submitted that as a regulated NBFC, the assessee’s financial transactions are subject to stringent oversight by the RBI and the MCA. He pointed out that all fifteen subscribers were active assessees on the records of the Income Tax Department and had duly responded to the notices issued by the AO under Section 133(6) of the Act.

9. We have carefully considered the rival submissions and perused the materials on record. It is a settled legal position that to discharge the initial onus under Section 68, the assessee must establish the identity of the creditor, their creditworthiness, and the genuineness of the transaction. In the instant case, the leamed Tribunal conducted a meticulous factual inquiry and recorded a specific finding that the assessee provided a “Cast Iron” documentary foundation. The audited balance sheets of the subscribers demonstrated a substantial net worth, which was far in excess of the amounts invested.

10. Furthermore, we find that the AO’s reliance on the non-appearance of the directors is misplaced and is not supported by the statutory scheme where robust documentary evidence isavailable. As held by this Court in PCIT vs. Sreeleathers [2022] 448 ITR 332 (Cal), the AO is vested with co-terminus powers under Section 131 of the Act to compel attendance. If the AO fails to exercise these powers, he cannot subsequently visit the consequences of such failure upon the assessee. Personal appearance of a director is not a statutory substitute for documented traceability in a corporate assessment, especially when the entities are active taxpayers.

11. Insofar as the reliance on NRA Iron & Steel is concerned, we find the facts of that case to be clearly distinguishable. In that case, the investors were found to be non-existent or “phantom” entities upon field inquiry. In the case before us, the investors are identifiable taxpayers who directly responded to notices u/s 133(6) and confirmed the transactions through banking channels. Equating “traceable investors” with “phantom entities” is a leap in logic that cannot be countenanced. Furthermore, the valuation of shares is a matter of commercial wisdom. Unless the Revenue proves a “live link” showing that the funds originated from the assessee’s own coffers, the AO cannot substitute his judgment for that of the marketplace.

12. In view of the aforesaid discussion, we arrive at a definite conclusion that in a corporate assessment, documented traceability (comprising ITR acknowledgments, PAN details, and Bank Statements) through legitimate banking channels carries greater evidentiary weight than the subjective suspicion of an Assessing Officer. The “Test of Human Probability” cannot be invoked as a tool to disregard a verified and audited paper trail. We also conclude that the ratio in NRA Iron & Steel is applicable only to “phantom” or “non-existent” entities found to be non-traceable upon field inquiry. It cannot be extended to active, traceable taxpayers simply because their investment decisions appear commercially improbable to the Revenue. Equating “traceable investors”with “phantom entities” is a leap in logic that cannot be countenanced. Furthermore, the valuation of shares is a matter of commercial wisdom. Unless the Revenue proves a “live link” showing that the funds originated from the assessee’s own coffers, the AO cannot substitute his judgment for that of the marketplace.

13. Upon considering the submissions made on either side and perusing the materials on record, we find that the learned Tribunal has conducted a meticulous factual inquiry. The Tribunal has recorded a specific finding that the assessee had provided “Cast Iron” documentary evidence to establish the identity and creditworthiness of the subscribers. The audited balance sheets of these companies reflected a substantial net worth, which was far in excess of the amounts invested in the assessee company.

14. We are convinced that the findings of the learned Tribunal are based on a meticulous factual inquiry. The Revenue has failed to produce any contrary material to disprove the documents filed. It is a settled position that suspicion, however strong, cannot take the place of evidence. We find no perversity in the findings of the learned Tribunal.

15. For the reasons aforementioned, we are of the view that no substantial question of law arises for consideration in this appeal. The findings of the learned Tribunal are based on a sound appreciation of facts and settled legal principles.

11.3. The case of the assessee is squarely covered by the decisions of Hon’ble Jurisdictional High Court in the cases of PCIT Vs. M/s Bright Commodeal Private Limited in ITAT/162/2025, IA No: GA/1/2025, GA/2/2025, vide order dated 28.08.2025, PCIT Vs. Devbhumi Vinimay Pvt. Ltd. in ITAT/16/2025, IA No.GA/2/2025, vide order dated 22.07.2025, PCIT Vs. Balaka Vinimay Private Limited in ITAT/131/2025, IA no. GA/1/2025, GA/2/2025 vide order dated 21.07.2025, PCIT Vs. Rajshree Integrated Cold Chain Pvt. Ltd., ITAT/286/2024, IA No.GA/2/2024, vide order dated 17.07.2025, PCIT Vs. One Point Commercial Pvt. Ltd., ITAT/27/2025, IA no.GA/1/2025, vide order dated 3.07.2025. Therefore, considering the facts before us, we set aside the order of ld. CIT (A).

11.4. We therefore, respectfully following the above decisions, set aside the order of ld. CIT (A) and direct the AO to delete the addition. The appeal of the assessee is allowed.

12. In the result, the both the appeals of the assessee are allowed.

Order pronounced on 20.05.2026.

Author Bio