Startup: Startup India is a flagship initiative of the Government of India, intended to build a strong ecosystem that is conducive for the growth of startup businesses, to drive sustainable economic growth and generate large scale employment opportunities.

Who can be registered as Startup?

- Private Limited Company

- Registered Partnership Firm

- limited liability partnership (LLP)

Note: – 1. An entity is eligible to be recognized as start upto a period 10 years from the date of incorporation.

2. Startup Certificate issued by the DIPP is valid for 10 years from the date of its incorporation.

Turnover Limit for consideration of an entity as a Startup?

Turnover of the entity for any of the financial years since incorporation/ registration should not exceed Rs.100Crore.

Activity covered under Startups?

The Entity which is working towards innovation, development or improvement of products or processes or services, or if it is a scalable business model with a high potential of employment generation or wealth creation..

Benefits/Relaxations provided to recognized Startups:

| S.NO. | BENEFITS/RELAXATIONS | PARTICULARS |

| 1 | Simple process | Government of India has launched a mobile app and a website for easy registration for startups. Anyone interested in setting up a startup can fill up a simple form on the website and upload certain documents. |

| 2 | Easy access to Funds | The Government is also giving guarantee to the lenders to encourage banks and other financial institutions for providing venture capital. |

| 3 | Tax holiday for 3 Years | Startups will be exempted from income tax for 3 years provided they get a certification from Inter-Ministerial Board (IMB) as per Section 80-IAC of Income Tax Act. |

| 4 | R&D facilities | Seven new Research Parks will be set up to provide facilities to startups in the R&D sector. |

| 5 | Easy Winding of Company | Within 90 days under Insolvency & Bankruptcy Code, 2016. |

| 6 | Startup Patent Application & IPR Protection | Fast track patent application with up to 80% rebate in filling patents. |

| 7 | Easier Public Procurement Norms | Exemption from requirement of earnest money deposit, prior turnover and experience requirements in government tenders. |

| 8 | SIDBI Fund of Funds | Funds for investment into startups through Alternate Investment Funds. |

Taxation: Section 80-IAC: Special provision in respect of specified business.

Eligible Startup:Where the gross total income of an eligible start-up, includes any profits and gains derived from eligible business, be allowed, in computing the total income of the assessee, a deduction of an amount equal to 100 % of the profits and gains derived from such business for 3 consecutive assessment years.The deduction as specified above may, at the option of the assessee, be claimed by him for any three consecutive assessment years out of ten years beginning from the year in which the eligible start-up is incorporated.

Eligible start-up: means a company or a limited liability partnership engaged in eligible business which fulfils the following conditions, namely: —

(a) It is incorporated on or after the 01/04/2016 but before the 01/04/2021;

(b) The total turnover of its business does not exceed 25 crore rupees in the previous year relevant to the assessment year for which deduction under sub-section (1) is claimed; and

(c) It holds a certificate of eligible business from the Inter-Ministerial Board (IMB)of Certification.

CAN STARTUP COMPANIES ISSUE SWEAT EQUITY SHARES?

Yes, Startup companies can issue sweat equity shares to its directors or employees.

Let’s have a brief studyabout the issuing criteria read with latest Notification of MCA dated 5th June 2020:

Section 2(88) “sweat equity shares”: means such equity shares as are issued by a company to its directors or employees at a discount or for consideration, other than cash, for providing their know-how or making available rights in the nature of intellectual property rights (IPR) or value additions.

Applicable Rules?

Section 54 of the Companies Act 2013 read with the companies (Share Capital and Debentures) Rule, 2014.

Who can issue sweat equity shares?

Who are covered under the sweat equity scheme?

Sweat equity shares can be issued by a company at discount or for consideration other than cash to:

What is meant by Value addition?

Value Addition

Means actual or anticipated economic benefits derived from an expert or a professional for providing know-how or making available rights in the nature of intellectual property rights, by such person to whom sweat equity is being issued for which the consideration is not paid or included in the normal remuneration payable under the contract of employment, in the case of an employee.

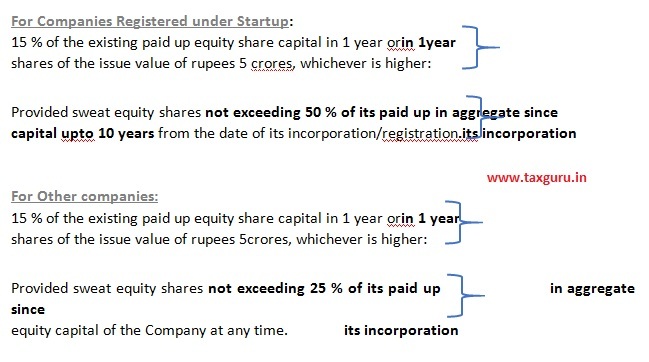

The company shall not issue sweat equity shares for more than:

What is lock-in periodfor Sweat Equity?

The sweat equity shares issued to directors or employees shall be locked in/non- transferable for a period of 3 years from the date of allotment and period of expiry of lock in shall be stamped in bold on the share certificate.

Valuation of Sweat Equity shares?

The procedure for valuation of sweat equity shares are as follows:

1. Valued at a price determined by a registered valuer as the fair price giving justification for such valuation

2. After Valuation, registered valuer required to provide a proper report addressed to the Board of directors with justification for such valuation.

3. Copy of gist along with critical elements of the valuation report shall be sent to the shareholders with the notice of the general meeting

The report must be in accordance with the Accounting Standards in both the cases i.e. Cash or consideration other than cash.

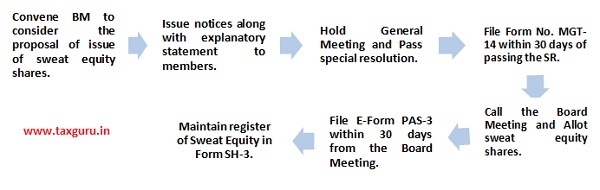

What is the procedure for issuance of sweat equity shares?

- Notice of EGM must contain the following particulars:

(a) Date of the BM at which the proposal for issue of sweat equity shares was approved;

(b) Reasons or justification for the issue;

(c) Class of shares under which sweat equity shares are intended to be issued;

(d) the total number of shares to be issued as sweat equity;

(e) the class or classes of directors or employees to whom such equity shares are to be issued;

(f) the principal terms and conditions on which sweat equity shares are to be issued, including basis of valuation;

(g) the names of the directors or employees to whom the sweat equity shares will be issued and their relationship with the promoter or/and Key Managerial Personnel;

(h) the price at which the sweat equity shares are proposed to be issued;

(i) the consideration including consideration other than cash, if any to be received for the sweat equity;

(j) the ceiling on managerial remuneration, if any, be breached by issuance of such sweat equity and how it is proposed to be dealt with;

(k) a statement to the effect that the company shall conform to the applicable accounting standards; and

(l) diluted Earning Per Share pursuant to the issue of sweat equity shares, calculated in accordance with the applicable accounting standards.

Forms required to be filed with the authority?

As mentioned above in process only 2 forms are required i.e.

- MGT-14 filed within 30 days from the passing of SR and

- PAS-3filed within 30 days from the allotment of shares in Board Meeting.

Register for recording of Sweat Equity Issue?

Maintain a Register of Sweat Equity Shares in Form No. SH-3 andshall be authenticated by the Company Secretary of the company or by any other person authorized by the Board for the purpose.

Issue of Sweat Equity Shares under as Foreign Investment in India.

“Sweat equity shares” may be issued to employees/ directors or employees/ directors of its holding company or joint venture or wholly owned overseas subsidiary/ subsidiaries who are resident outside India, subject to the following conditions:

- Issue of Sweat equity shares are in compliance with the sectoral cap applicable to the said company;

- Issue of Sweat equity shares in a company where investment by a person resident outside India is under the approval route requires prior Government approval;

- Issue ofSweat equity shares to a citizen of Bangladesh/ Pakistan requires prior Government approval.

Startup Sectors Likely to Grow Post COVID-19 Pandemic

Corona virus impact is not just physical, it’s temperamental, psychological, ergonomic and it is here to stay for some time!

- ED-Tech

- Health &Wellness

- Financial Services & NBFCs

- E-Commerce &Delivery Based Services

- Over the Top Platforms & Online Gaming

- Pharma, Life Sciences & Labs/Pathology

About the Author

Author is Divya Goel, ACS working as Assistant Manager- Company Secretary with Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India. Author can be reached at info@neerajbhagat.com.