The content provides a comprehensive overview of the legal framework governing Permanent Account Number (PAN) and Aadhaar under the Income-tax Act, 1961, along with corresponding rules and compliance requirements. PAN is a ten-digit alphanumeric identifier issued by the Income-tax Department for uniquely identifying taxpayers. It is mandatory for filing income tax returns, undertaking specified financial transactions, and for correspondence with tax authorities. Aadhaar, a 12-digit unique identification number, can be used in lieu of PAN in specified situations.

PAN must be obtained by individuals whose income exceeds the basic exemption limit, businesses or professionals with turnover exceeding ₹5 lakh, persons involved in financial transactions of ₹2.5 lakh or more, and persons receiving income subject to TDS/TCS. It is also mandatory for individuals in key roles such as directors, partners, trustees, and authorized representatives of entities engaged in financial transactions. PAN application is made through prescribed forms such as Form 49A (for residents) and Form 49AA (for non-residents), and can also be obtained through incorporation forms for companies and LLPs.

Quoting PAN is mandatory in various situations, including income-tax returns, tax payments, and specified high-value transactions such as purchase of vehicles, opening bank accounts, making deposits, applying for credit cards, and opening demat accounts. Rule 114B further lists specific transactions requiring PAN, including immovable property transactions exceeding ₹10 lakh, purchase of securities, insurance premiums, and cash payments above prescribed limits.

The law provides for interchangeability between PAN and Aadhaar. If a person does not have PAN but possesses Aadhaar, quoting Aadhaar is treated as an application for PAN. Similarly, where PAN is linked with Aadhaar, Aadhaar can be quoted in place of PAN for specified transactions. Section 139A(5E) enables such substitution.

Mandatory linking of PAN with Aadhaar is required under Section 139AA for persons eligible to obtain Aadhaar. Failure to link results in PAN becoming inoperative. An inoperative PAN leads to consequences such as higher TDS/TCS rates, denial of tax refunds, and no interest on refunds during the inoperative period. However, PAN can be reactivated upon linking Aadhaar by paying a prescribed fee. Persons allotted PAN using Aadhaar enrolment ID before 01.10.2024 must update Aadhaar details by 31.12.2025.

Certain exemptions from PAN and Aadhaar requirements are provided. Minors may use the PAN of their parents or guardians. Individuals without PAN can furnish Form 60 for specified transactions. Non-residents and foreign companies may be exempt from obtaining PAN under specific conditions, such as transactions in IFSC units or where income is not chargeable to tax in India. Rule 114AAB provides exemptions for eligible foreign investors and specified fund investors subject to conditions.

Rule 114 prescribes the procedure for applying for PAN, including documentation requirements for identity, address, and date of birth. Different categories of applicants, including individuals, companies, firms, trusts, and foreign entities, must submit prescribed documents. Aadhaar-based PAN allotment allows simplified application without additional documentation.

Rule 114AAA governs the consequences of non-linking of Aadhaar, including inoperative PAN status and associated restrictions. Rule 114C and Rule 114D impose obligations on specified persons to verify PAN in transactions and report Form 60 declarations. Rule 114BA and Rule 114BB mandate quoting of PAN or Aadhaar for specific transactions such as large cash deposits, withdrawals, and opening of bank accounts.

Penalties for non-compliance include ₹10,000 under Section 272B for failure to obtain or quote PAN, quoting incorrect PAN, or holding multiple PANs. Additionally, higher tax rates apply where PAN is not furnished.

Overall, the framework establishes PAN and Aadhaar as central tools for tax administration, ensuring identification, transparency, and compliance in financial transactions, while also prescribing detailed procedures, exceptions, and consequences for non-compliance.

Permanent Account Number (PAN)

Introduction

PAN is a ten-digit alphanumeric identifier issued by the Income-tax Department to identify taxpayers uniquely. It is mandatory for income-tax filings, high-value financial transactions, and correspondence with the tax authorities. Aadhaar can be used in lieu of PAN.

How to obtain PAN

- A resident applies for PAN in Form 49A, while a foreign citizen applies in Form 49AA.

- For company incorporation, PAN is allotted through Part B of the SPICe+ form

- For LLP incorporation, PAN can be applied through Form FiLLiP.

Who Should Obtain PAN?

- Individuals with taxable income exceeding the exemption limit.

- Businesses or professionals with gross receipts exceeding Rs. 5 lakh.

- Every person receiving income from property held under trust or legal obligation, wholly or partly for charitable or religious purposes, and liable to be assessed as a representative assesse in respect of such income.

- Entities conducting financial transactions of Rs. 2.5 lakh or more annually.

- Any person acting as MD, director, partner, trustee, author, founder, Karta, CEO, principal officer, office bearer

- Authorised representative of an entity with financial transactions of Rs. 2.5 lakhs or more in a year.

- Persons entitled to receive any sum subject to TDS/TCS.

- Persons depositing or withdrawing cash of Rs. 20 lakh or more annually.

- Persons opening current or cash credit accounts (exceptions for non-residents under specific conditions).

- Any other persons notified by the Central Govt..

Mandatory Quoting of PAN

- Quoting of PAN is mandatory in the following circumstances:

- If receipts/payments are subject to TDS/TCS;

- In all returns, challan or income-tax correspondence

- In certain financial transactions such as:

- Sale or purchase of a motor vehicle (other than two-wheelers)

- Opening an account [other than a basic savings bank deposit account] with a bank or a co-op. bank

- Time deposits with banks, co-op banks, post offices, Nidhis, or NBFCs exceeding Rs. 50,000 per transaction or Rs. 5 lakh in a year.

- Making an application for issue of a credit or debit card;

- Opening of a Demat account and more…

Interchangeability with Aadhaar

- If a person has Aadhaar but no PAN, quoting Aadhaar in specified transactions is treated as an application for PAN, with no separate documents required.

- If a person has PAN linked with Aadhaar (Sec. 139AA), Aadhaar can be quoted in place of PAN for all transactions where PAN is mandatory.

Exemptions from Quoting PAN

- Minor may quote PAN of parent/guardian if he has no taxable income.

- Form 60Declarations: The form allowed for individuals (not companies/firms) who do not have PAN. Form 60 is furnished for specified financial transactions.

- A foreign company may submit Form instead of PAN if:

a) It has no income chargeable to tax in India;

b) It does not have PAN;

c) The transaction is in an IFSC banking unit; and

d) The transaction relates to opening an account or time deposit

- As per Rule 114AB, a non-resident, not being a company or a foreign company, shall not be required to obtain and quote PAN if the specified conditions are satisfied.

Consequences of Non-Compliance of PAN

- Penalty under Section 272Bfor failure to obtain or quote PAN.

- Having Multiple PANs: Attracts penalty under section 272B

- Rs. 10,000 penalty for quoting false PAN or failure to quote PAN or failure to authenticate it.

- Higher TDS/TCS rates apply if PAN is not quoted (Sections 206AAand 206CC).

Quoting and Linking of Aadhaar Number

Introduction

Aadhaar, a 12-digit unique identification number, is mandatory for quoting in Income Tax Returns (ITRs) and PAN applications. Aadhaar can replace PAN for specific purposes. PANs allotted before 01-10-2024 using Aadhaar Enrolment ID must be updated with Aadhaar by 31-12-2025.

Eligibility for Aadhaar

- Any resident who has stayed in India for 182 or more days in the preceding 12 months.

- Non-Resident Indians (NRIs) with valid Indian passports can apply immediately upon arrival in India.

PAN-Aadhaar Linking Requirements

- All PAN holders as of July 1, 2017, who are eligible for Aadhaar, must link the two till 31-03-2022.

- Failure to link renders PAN inoperative, but linking is allowed thereafter with a fee under Section 234H.

- An inoperative PAN linked with Aadhaar after 31-03-2022 becomes operative within 30 days of intimation.

Consequences of Inoperative PAN

- Higher TDS/TCS rates apply (Sections 206AA, 206CC).

- No refund of any tax or part thereof shall be made.

- No interest on refund is payable for the period from 01-07-2023 until the date the PAN becomes operative.

Exemptions from Aadhaar Linking

Applicable only if Aadhaar is not possessed:

- Residents of Assam, Jammu & Kashmir, and Meghalaya.

- Non-residents under the Income-tax Act.

- Individuals aged 80 or above during the financial year.

- Non-citizens of India.

Interchangeability of Aadhaar and PAN

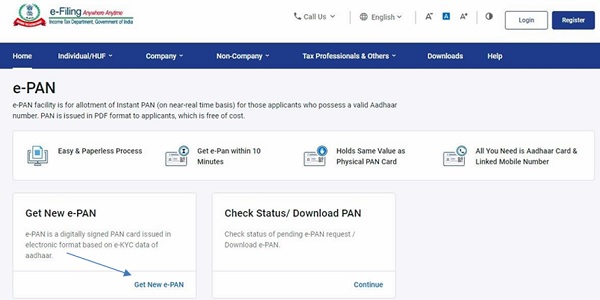

Aadhaar can substitute PAN for specified transactions under Section 139A(5E). Aadhaar can be used to instantly obtain PAN via the e-filing portal without submitting additional documents.

Mandatory quoting of Aadhaar in ITR and PAN application

Quoting Aadhaar in ITR and PAN application is compulsory. If Aadhaar is not available, Enrolment ID can be used—but only till 30.09.2024. From 01.10.2024, only Aadhaar number will be accepted. Anyone allotted a PAN before 01.10.2024 using an Aadhaar Enrolment ID must link his Aadhaar by 31.12.2025. [Notification No. 26/2025, dated 03-04-2025]

Extract of Relevant Sections under Income-tax Act, 1961

Section – 139A – Permanent account number.

139A. (1) Every person,—

i. if his total income or the total income of any other person in respect of which he is assessable under this Act during any previous year exceeded the maximum amount which is not chargeable to income-tax; or

ii. carrying on any business or profession whose total sales, turnover or gross receipts are or is likely to exceed five lakh rupees in any previous year;

Or

iii. who is required to furnish a return of income under sub-section (4A) of section 139; or

iv. being an employer, who is required to furnish a return of fringe benefits under section 115WD; or

v. being a resident, other than an individual, which enters into a financial transaction of an amount aggregating to two lakh fifty thousand rupees or more in a financial year; or

vi. who is the managing director, director, partner, trustee, author, founder, karta, chief executive officer, principal officer or office bearer of the person referred to in clause (v) or any person competent to act on behalf of the person referred to in clause (v); or

vii. who intends to enter into such transaction as may be prescribed by the Board in the interest of revenue, and who has not been allotted a permanent account number shall, within such time, as may be prescribed, apply to the Assessing Officer for the allotment of a permanent account number.

(1A) Notwithstanding anything contained in sub-section (1), the Central Government may, by notification in the Official Gazette, specify, any class or classes of persons by whom tax is payable under this Act or any tax or duty is payable under any other law for the time being in force including importers and exporters whether any tax is payable by them or not and such persons shall, within such time as mentioned in that notification, apply to the Assessing Officer for the allotment of a permanent account number.

(1B) Notwithstanding anything contained in sub-section (1), the Central Government may, for the purpose of collecting any information which may be useful for or relevant to the purposes of this Act, by notification in the Official Gazette, specify, any class or classes of persons who shall apply to the Assessing Officer for the allotment of the permanent account number and such persons shall, within such time as mentioned in that notification, apply to the Assessing Officer for the allotment of a permanent account number.

(2) The Assessing Officer, having regard to the nature of the transactions as may be prescribed, may also allot a permanent account number, to any other person (whether any tax is payable by him or not), in the manner and in accordance with the procedure as may be prescribed.

(3) Any person, not falling under sub-section (1) or sub-section (2), may apply to the Assessing Officer for the allotment of a permanent account number and, thereupon, the Assessing Officer shall allot a permanent account number to such person forthwith.

(4) For the purpose of allotment of permanent account numbers under the new series, the Board may, by notification in the Official Gazette, specify the date from which the persons referred to in sub-sections (1) and (2) and other persons who have been allotted permanent account numbers and residing in a place to be specified in such notification, shall, within such time as may be specified, apply to the Assessing Officer for the allotment of a permanent account number under the new series and upon allotment of such permanent account number to a person, the permanent account number, if any, allotted to him earlier shall cease to have effect :

Provided that the persons to whom permanent account number under the new series has already been allotted shall not apply for such number again.

(5) Every person shall—

a. quote such number in all his returns to, or correspondence with, any income-tax authority;

b. quote such number in all challans for the payment of any sum due under this Act;

c. quote such number in all documents pertaining to such transactions as may be prescribed by the Board in the interests of the revenue, and entered into by him:

Provided that the Board may prescribe different dates for different transactions or class of transactions or for different class of persons:

Provided further that a person shall quote General Index Register Number till such time Permanent Account Number is allotted to such person;

d. intimate the Assessing Officer any change in his address or in the name and nature of his business on the basis of which the permanent account number was allotted to him.

(5A) Every person receiving any sum or income or amount from which tax has been deducted under the provisions of Chapter XVIIB, shall intimate his permanent account number to the person responsible for deducting such tax under that Chapter :

Provided further that a person referred to in this sub-section shall intimate the General Index Register Number till such time permanent account number is allotted to such person.

(5B) Where any sum or income or amount has been paid after deducting tax under Chapter XVIIB, every person deducting tax under that Chapter shall quote the permanent account number of the person to whom such sum or income or amount has been paid by him—

i. in the statement furnished in accordance with the provisions of sub-section (2C) of section 192;

ii. in all certificates furnished in accordance with the provisions of section 203;

iii. in all returns prepared and delivered or caused to be delivered in accordance with the provisions of section 206 to any income-tax authority;

iv. in all statements prepared and delivered or caused to be delivered in accordance with the provisions of sub-section (3) of section 200:

Provided that the Central Government may, by notification in the Official Gazette, specify different dates from which the provisions of this sub-section shall apply in respect of any class or classes of persons:

Provided further that nothing contained in sub-sections (5A) and (5B) shall apply in case of a person whose total income is not chargeable to income-tax or who is not required to obtain permanent account number under any provision of this Act if such person furnishes to the person responsible for deducting tax, a declaration referred to in section 197A in the form and manner prescribed thereunder to the effect that the tax on his estimated total income of the previous year in which such income is to be included in computing his total income will be nil.

(5C) Every buyer or licensee or lessee referred to in section 206C shall intimate his permanent account number to the person responsible for collecting tax referred to in that section.

(5D) Every person collecting tax in accordance with the provisions of section 206C shall quote the permanent account number of every buyer or licensee or lessee referred to in that section—

i. in all certificates furnished in accordance with the provisions of sub-section (5) of section 206C;

ii. in all returns prepared and delivered or caused to be delivered in accordance with the provisions of sub-section (5A) or sub-section (5B) of section 206C to an income-tax authority;

iii. in all statements prepared and delivered or caused to be delivered in accordance with the provisions of sub-section (3) of section 206C.

(5E) Notwithstanding anything contained in this Act, every person who is required to furnish or intimate or quote his permanent account number under this Act, and who,—

a. has not been allotted a permanent account number but possesses the Aadhaar number, may furnish or intimate or quote his Aadhaar number in lieu of the permanent account number, and such person shall be allotted a permanent account number in such manner as may be prescribed;

b. has been allotted a permanent account number, and who has intimated his Aadhaar number in accordance with provisions of sub-section (2) of section 139AA, may furnish or intimate or quote his Aadhaar number in lieu of the permanent account number.

(6) Every person receiving any document relating to a transaction prescribed under clause (c) of sub-section (5) shall ensure that the Permanent Account Number or the General Index Register Number or the Aadhaar number, as the case may be, has been duly quoted in the document.

(6A) Every person entering into such transaction, as may be prescribed, shall quote his permanent account number or Aadhaar number, as the case may be, in the documents pertaining to such transactions and also authenticate such permanent account number or Aadhaar number, in such manner as may be prescribed.

(6B) Every person receiving any document relating to the transactions referred to in sub-section (6A), shall ensure that permanent account number or Aadhaar number, as the case may be, has been duly quoted in such document and also ensure that such permanent account number or Aadhaar number is so authenticated.

(7) No person who has already been allotted a permanent account number under the new series shall apply, obtain or possess another permanent account number.

Explanation.—For the removal of doubts, it is hereby declared that any person, who has been allotted a permanent account number under any clause other than clause (iv) of sub-section (1), shall not be required to obtain another permanent account number and the permanent account number already allotted to him shall be deemed to be the permanent account number in relation to fringe benefit tax.

(8) The Board may make rules providing for—

a. the form and the manner in which an application may be made for the allotment of a permanent account number and the particulars which such application shall contain;

b. the categories of transactions in relation to which Permanent Account Numbers or the General Index Register Number or the Aadhaar number, as the case may be, shall be quoted by every person in the documents pertaining to such transactions;

c. the categories of documents pertaining to business or profession in which such numbers shall be quoted by every person;

d. class or classes of persons to whom the provisions of this section shall not apply;

e. the form and the manner in which the person who has not been allotted a Permanent Account Number or who does not have General Index Register Number shall make his declaration;

f. the manner in which the Permanent Account Number or the General Index Register Number or the Aadhaar number, as the case may be, shall be quoted in respect of the categories of transactions referred to in clause (c);

g. the time and the manner in which the transactions referred to in clause (c) shall be intimated to the prescribed authority.

Explanation—For the purposes of this section,—

(a) “Aadhaar number” shall have the meaning assigned to it in clause (a) of section 2 of the Aadhaar (Targeted Delivery of Financial and Other Subsidies, Benefits and Services) Act, 2016 (18 of 2016);

(aa) “Assessing Officer” includes an income-tax authority who is assigned the duty of allotting permanent account numbers;

(ab) “authentication” means the process by which the permanent account number or Aadhaar number alongwith demographic information or biometric information of an individual is submitted to the income-tax authority or such other authority or agency as may be prescribed for its verification and such authority or agency verifies the correctness, or the lack thereof, on the basis of information available with it;

(b) “permanent account number” means a number which the Assessing Officer may allot to any person for the purpose of identification and includes a permanent account number allotted under the new series;

(c) “permanent account number under the new series” means a permanent account number having ten alphanumeric characters

(d) “General Index Register Number” means a number given by an Assessing Officer to an assessee in the General Index Register maintained by him and containing the designation and particulars of the ward or circle or range of the Assessing Officer.

Section – 139AA – Quoting of Aadhaar number.

139AA. (1) Every person who is eligible to obtain Aadhaar number shall, on or after the 1st day of July, 2017, quote Aadhaar number—

(i) in the application form for allotment of permanent account number;

(ii) in the return of income:

Provided that where the person does not possess the Aadhaar Number, the Enrolment ID of Aadhaar application form issued to him at the time of enrolment shall be quoted in the application for permanent account number or, as the case may be, in the return of income furnished by him:

88-89[Provided further that nothing in the first proviso shall apply in respect of any application form for allotment of permanent account number or return of income furnished on or after the 1st day of October, 2024.]

(2) Every person who has been allotted permanent account number as on the 1st day of July, 2017, and who is eligible to obtain Aadhaar number, shall intimate his Aadhaar number to such authority in such form and manner as may be prescribed, on or before a date to be notified by the Central Government in the Official Gazette:

Provided that in case of failure to intimate the Aadhaar number, the permanent account number allotted to the person shall be made inoperative after the date so notified in such manner as may be prescribed.

88-89[(2A) Every person who has been allotted permanent account number on the basis of Enrolment ID of Aadhaar application form filed prior to the 1st day of October, 2024, shall intimate his Aadhaar number to such authority in such form and manner, as may be prescribed, on or before a date to be notified by the Central Government in the Official Gazette.]

(3) The provisions of this section shall not apply to such person or class or classes of persons or any State or part of any State, as may be notified by the Central Government in this behalf, in the Official Gazette.

Explanation.—For the purposes of this section, the expressions-

(i) “Aadhaar number”, “Enrolment” and “resident” shall have the same meanings respectively assigned to them in clauses (a), (m) and (v) of section 2 of the Aadhaar (Targeted Delivery of Financial and other Subsidies, Benefits and Services) Act, 2016 (18 of 2016);

(ii) “Enrolment ID” means a 28 digit Enrolment Identification Number issued to a resident at the time of enrolment.

Note:

88-89 Ins. by Act No. 15 of 2024, w.e.f. 1-10-2024.

Extract of Relevant Income-tax Rules

Rule – 114 – Application for allotment of a permanent account number.

114. (1) An application under sub-section (1) or sub-section (1A) or sub-section (2) or sub-section (3) of section 139A for allotment of a permanent account number shall be made in Form No. 49A or 49AA, as the case may be :

91[Provided that an applicant may apply for allotment of permanent account number through a common application form notified by the Central Government in the Official Gazette, and the Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) shall specify the classes of persons, forms and formats along with procedure for safe and secure transmission of such forms and formats in relation to furnishing of permanent account number.]

92[(1A) Any person, who has not been allotted a permanent account number but possesses the Aadhaar number and has furnished or intimated or quoted his Aadhaar number in lieu of the permanent account number in accordance with sub-section (5E) of section 139A, shall be deemed to have applied for allotment of permanent account number and he shall not be required to apply or submit any documents under this rule.

(1B) Any person, who has not been allotted a permanent account number but possesses the Aadhaar number may apply for allotment of the permanent account number under sub-section (1) or sub-section (1A) or sub-section (3) of section 139A to the authorities mentioned in sub-rule (2) by intimating his Aadhaar number and he shall not be required to apply or submit any documents under this rule.

(1C) The Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) shall on receipt of information under sub-rule (1A) or sub-rule (1B), as the case may be, authenticate the Aadhaar number for that purpose.]

(2) An application referred to in sub-rule (1) shall be made,—

(i) in cases where the function of allotment of permanent account number under section 139A has been assigned by the Chief Commissioner or Commissioner to any particular Assessing Officer, to that Assessing Officer;

(ii) in any other case, to the Assessing Officer having jurisdiction to assess the applicant.

(3) The application referred to in sub-rule (1) shall be made,—

(i) in a case where the total income of the person or the total income of any other person in respect of which he is assessable under the Act during any financial year exceeds the maximum amount which is not chargeable to income-tax and he has not been allotted any permanent account number, on or before the 31st day of May of the assessment year for which such income is assessable;

(ii) in the case of a person not falling under clause (i), but carrying on any business or profession, the total sales, turnover or gross receipts of which are or is likely to exceed five lakh rupees in any financial year and who has not been allotted any permanent account number, before the end of that financial year;

(iii) in the case of a person who is required to furnish a return of income under sub-section (4A) of section 139 and who has not been allotted any permanent account number, before the end of the financial year;

(iv) in the case of a person who is entitled to receive any sum or income or amount, on which tax is deductible under Chapter XVII-B in any financial year, before the end of such financial year;

93[(v) in the case of a person, being a resident, other than an individual, which enters into a financial transaction of an amount aggregating to two lakh fifty thousand rupees or more in a financial year and which has not been allotted any permanent account number, on or before the 31st day of May immediately following such financial year;

(vi) in the case of a person, who is the managing director, director, partner, trustee, author, founder, karta, chief executive officer, principal officer or office bearer of the person referred to in clause (v) or any person competent to act on behalf of the person referred to in clause (v) and who has not been allotted any permanent account number, on or before the 31st day of May immediately following the financial year in which the person referred to in clause (v) enters into financial transaction specified therein;]

94[(vii) in the case of a person who intends to enter into the transaction prescribed under clause (vii) of sub-section (1) of section 139A, at least seven days before the date on which he intends to enter into the said transaction.]

(4) The application, referred to in sub-rule (1) 95[other than that referred to in the proviso to sub-rule (1)] in respect of an applicant mentioned in column (2) of the Table below, shall be filled in the Form mentioned in column (3) of the said table, and shall be accompanied by the documents mentioned in column (4) thereof, as proof of identity, address and date of birth of such applicant:

Table

| Sl. No. | Applicant | Form | Documents as proof of identity, address and date of birth |

| (1) | (2) | (3) | (4) |

| 1. | Individual who is a citizen of India | 49A | (A) Proof of identity—

(i) Copy of,— (a) elector’s photo identity card; or (b) ration card having photograph of the applicant; or (c) passport; or (d) driving licence; or (e) arm’s license; or (f) AADHAAR Card issued by the Unique Identification Authority of India; or (g) photo identity card issued by the Central Government or a State Government or a Public Sector Undertaking; or (h) Pensioner Card having photograph of the applicant; or (i) Central Government Health Scheme Card or Ex-servicemen Contributory Health Scheme photo card; or (ii) certificate of identity in original signed by a Member of Parliament or Member of Legislative Assembly or Municipal Councillor or a Gazetted Officer, as the case may be; or (iii) bank certificate in original on letter head from the branch (along with name and stamp of the issuing officer) containing duly attested photograph and bank account number of the applicant. Note : In case of a person being a minor, any of the above documents of any of the parents or guardian of such minor shall be deemed to be the proof of identity. (B) Proof of address— (i) copy of the following documents of not more than three months old— (a) electricity bill; or (b) landline telephone or broadband connection bill; or (c) water bill; or (d) consumer gas connection card or book or piped gas bill; or (e) bank account statement or as per Note 1; or (f) depository account statement; or (g) credit card statement; or (ii) copy of,— (a) post office pass book having address of the applicant; or (b) passport; or (c) passport of the spouse; or (d) elector’s photo identity card; or (e) latest property tax assessment order; or (f) driving licence; or (g) domicile certificate issued by the Government; or (h) AADHAAR Card issued by the Unique Identification Authority of India; or (i) allotment letter of accommodation issued by the Central Government or State Government of not more than three years old; or (j) property registration document; or (iii) certificate of address signed by a Member of Parliament or Member of Legislative Assembly or Municipal Council or or a Gazetted Officer, as the case may be; or (iv) employer certificate in original. Note 1 : In case of an Indian citizen residing outside India, copy of Bank Account Statement in country of residence or copy of Non-resident External bank account statements shall be the proof of address. Note 2 : In case of a minor, any of the above documents of any of the parents or guardian of such minor shall be deemed to be the proof of address. (a) birth certificate issued by the municipal authority or any office authorised to issue birth and death certificate by the Registrar of Birth and Deaths or the Indian Consulate as defined in clause (d) of sub-section (1) of section 2 of the Citizenship Act, 1955 (57 of 1955); or (b) pension payment order; or (c) marriage certificate issued by the Registrar of Marriages; or (d) matriculation certificate or mark sheet of recognised board; or (e) passport; or (f) driving licence; or (g) domicile certificate issued by the Government; or] (h) aadhaar card issued by the Unique Identification Authority of India; or (i) elector’s photo identity card; or (j) photo identity card issued by the Central Government or State Government or Central Public Sector Undertaking or State Public Sector Undertaking; or (k) Central Government Health Service Scheme photo card or Ex-servicemen Contributory Health Scheme photo card; or (l) affidavit sworn before a magistrate stating the date of birth.] |

| 2. | Hindu undivided family | 49A | (a) An affidavit by the karta of the Hindu Undivided Family stating the name, father’s name and address of all the coparceners on the date of application; and

(b) Copy of any document applicable in the case of an individual specified in serial number 1, in respect of karta of the Hindu undivided family, as proof of identity, address and date of birth. |

| 3. | Company registered | 49A | 97[(a) Copy of Certificate of Registration issued by in India the Registrar of Companies; or

(b) corporate identity number allotted by the Registrar under section 7 of the Companies Act, 2013 (18 of 2013)] |

| 4. | Firm (including Limited Liability Partnership) formed or registered in India | 49A | (a) Copy of Certificate of Registration issued by the Registrar of Firms/Limited Liability Partnerships; or

(b) Copy of Partnership Deed. |

| 5. | Association of persons(Trusts) formed or registered in India | 49A | (a) Copy of trust deed; or

(b) Copy of Certificate of Registration Number issued by Charity Commissioner. |

| 6. | Association of persons(other than Trusts) or body of individuals or local authority or artificial juridical person formed or registered in India | 49A | (a) Copy of Agreement; or

(b) Copy of Certificate of Registration Number issued by Charity Commissioner or Registrar of Co-operative Society or any other Competent Authority; or (c) Any other document originating from any Central Government or State Government Department establishing Identity and address of such person. |

| 7. | Individuals not being a citizen of India | 49AA | (i) Proof of identity :—

(a) Copy of Passport; or (b) copy of person of Indian Origin card issued by the Government of India; or (c) copy of Overseas Citizenship of India Card issued by Government of India; or (d) copy of other national or citizenship Identification Number or Taxpayer Identification Number duly attested by “Apostille” (in respect of countries which are signatories to the Hague Apostille Convention of 1961) or by Indian embassy or High Commission or Consulate in the country where the applicant is located or authorised officials of overseas branches of Scheduled Banks registered in India. (ii) Proof of address:— (a) copy of Passport; or (b) copy of person of Indian Origin card issued by the Government of India; or (c) copy of Overseas Citizenship of India Card issued by Government of India; or (d) copy of other national or citizenship Identification Number or Taxpayer Identification Number duly attested by “Apostille” (in respect of countries which are signatories to the Hague Apostille Convention of 1961) or by Indian embassy or High Commission or Consulate in the country where the applicant is located or authorised officials of over- seas branches of Scheduled Banks registered in India; or (e) copy of bank account statement in the country of residence; or (f) copy of Non-resident External bank account statement in India; or (g) copy of certificate of residence in India or Residential permit issued by the State Police Authority; or (h) copy of the registration certificate issued by the Foreigner’s Registration Office showing Indian address; or (i) copy of Visa granted and copy of appointment letter or contract from Indian Company and Certificate (in original) of Indian Address issued by the employer. |

| 8. | LLP registered outside India | 49AA | (a) Copy of Certificate of Registration issued in the country where the applicant is located, duly attested by “Apostille” (in respect of countries which are signatories to the Hague Apostille Convention of 1961) or by Indian embassy or High Commission or Consulate in the country where the applicant is located or authorised officials of overseas branches of Scheduled Banks registered in India; or

(b) Copy of registration certificate issued in India or of approval granted to set up office in India by Indian Authorities. |

| 9. | Company registered outside India | 49AA | (a) Copy of Certificate of Registration issued in the country where the applicant is located, duly attested by “Apostille” (in respect of countries which are signatories to the Hague Apostille Convention of 1961) or by Indian embassy or High Commission or Consulate in the country where the applicant is located or authorised officials of overseas branches of Scheduled Banks registered in India; or

(b) Copy of registration certificate issued in India or of approval granted to set up office in India by Indian Authorities. |

| 10. | Firm formed or regist red outside India | 49AA | (a) Copy of Certificate of Registration issued in the country where the applicant is located, duly attested by “Apostille” (in respect of countries which are signatories to the Hague Apostille Convention of 1961) or by Indian embassy or High Commission or Consulate in the country where the applicant is located or authorised officials of overseas branches of Scheduled Banks registered in India; or

(b) Copy of registration certificate issued in India or of approval granted to set up office in India by Indian Authorities. |

| 11. | Association of persons (Trusts) formed outside | 49AA | (a) Copy of Certificate of Registration issued in the country where the applicant is located, duly India attested by “Apostille” (in respect of countries which are signatories to the Hague Apostille Convention of 1961) or by Indian embassy or High Commission or Consulate in the country where the applicant is located or authorised officials of overseas branches of Scheduled Banks registered in India; or

(b) Copy of registration certificate issued in India or of approval granted to set up office in India by Indian Authorities. |

| 12. | Association of persons (other than Trusts) or body of individuals or local authority or person formed or any other entity (by whatever name called) registered outside India | 49AA | (a) Copy of Certificate of Registration issued in the country where the applicant is located, duly at tested by “Apostille” (in respect of countries which are signatories to the Hague Apostille Convention of 1961) or by Indian embassy or High Commission or Consulate in the country where the applicant is located or authorised officials of overseas branches of Scheduled Banks registered in India; or

(b) Copy of registration certificate issued in India or of approval granted to set up office in India by Indian Authorities. |

98[(5) Every person who has been allotted permanent account number as on the 1st day of July, 2017 and who in accordance with the provisions of sub-section (2) of section 139AA is required to intimate his Aadhaar number, shall intimate his Aadhaar number to the Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) or the person authorised by the said authorities.

99[(5A) Every person who, in accordance with the provisions of sub-section (2) of section 139AA, is required to intimate his Aadhaar number to the prescribed authority in the prescribed form and manner, fails to do so by the date referred to in the said sub-section, shall, at the time of subsequent intimation of his Aadhaar number to the prescribed authority, be liable to pay, by way of fee, an amount equal to,—

(a) five hundred rupees, in a case where such intimation is made within three months from the date referred to in sub-section (2) of section 139AA; and

(b) one thousand rupees, in all other cases.]

1[(5AA) Every person who has been allotted permanent account number on the basis of Enrolment ID of Aadhaar application form filed prior to the 1st day of October, 2024, shall intimate his Aadhaar number to the Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) or the person authorised by the said authorities.]

(6) The Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) shall specify the formats and standards along with procedure, for the verification of documents filed with the application 1a[under sub-rule (4), 1b[intimation of Aadhaar number in sub-rules (5) and (5AA)] and issue of permanent account number], for ensuring secure capture and transmission of data in such format and standards and shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to furnishing of the application forms for allotment of permanent account 2[number, intimation of Aadhaar number and issue of permanent account number].]

3[(7) The Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) shall lay down the formats and standards along with procedure for,—

(a) furnishing or intimation or quoting of Aadhaar number under sub-rule (1A); or

(b) intimation of Aadhaar number under sub-rule (1B); or

(c) authentication of Aadhaar number under sub-rule (1C); or

(d) obtaining demographic information of an individual from the Unique Identification Authority of India,

for ensuring secure capture and transmission of data and shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to furnishing or intimation or quoting or authentication of Aadhaar number or obtaining of demographic information of an individual from the Unique Identification Authority of India, for allotment of permanent account number and issue thereof.]

Notes:

91 Substituted by the IT (Second Amdt.) Rules, 2017, w.e.f. 9-2-2017.

92 Sub-rules (1A), (1B) and (1C) inserted by the IT (Fifth Amdt.) Rules, 2019, w.e.f. 1-9-2019.

93 Inserted by the IT (Twelfth Amdt.) Rules, 2018, w.e.f. 5-12-2018.

94 Inserted by the IT (Fifteenth Amdt.) Rules, 2022. The amendment shall come into force after the expiry of fifteen days from 10-5-2022.

95 Inserted by the IT (Fifth Amdt.) Rules, 2015, w.e.f. 10-4-2015.

96 Substituted by the IT (Fifth Amdt.) Rules, 2015, w.e.f. 10-4-2015.

97 Substituted for “Copy of Certificate of Registration issued by the Registrar of Companies” by the IT (Fifth Amdt.) Rules, 2015, w.e.f. 10-4-2015.

98 Sub-rules (5) and (6) substituted for sub-rule (5) by the IT (Seventeenth Amdt.) Rules, 2017, w.e.f. 1-7-2017.

99 Inserted by the IT (Third Amdt.) Rules, 2022, w.e.f. 1-4-2022.

1 Inserted by the IT (Ninth Amdt.) Rules, 2025., e.f. 3-4-2025.

1a Substituted for “under sub-rule (4) or intimation of Aadhaar number in sub-rule (5)” by the IT (Twelfth Amdt.) Rules, 2018, w.e.f. 5-12-2018. lb. Substituted for “intimation of Aadhaar number in sub-rule (5)” by the IT (Ninth Amdt.) Rules, 2025., w.e.f. 3-4-2025.

2 Substituted for “number and intimation of Aadhaar number” by the IT (Twelfth Amdt.) Rules, 2018, w.e.f. 5-12-2018.

3 Inserted by the IT (Fifth Amdt.) Rules, 2019, w.e.f. 1-9-2019.

Rule – 114AAA

5[Manner of making permanent account number inoperative.

114AAA. (1) Where a person, who has been allotted the permanent account number as on the 1st day of July, 2017 and is required to intimate his Aadhaar number under sub-section (2) of section 139AA, has failed to intimate the same on or before the 31st day of March, 2022, the permanent account number of such person shall become inoperative, and he shall be liable for payment of fee in accordance with sub-rule (5A) of rule 114.

(2) Where the person referred to in sub-rule (1) has intimated his Aadhaar number under sub-section (2) of section 139AA after the 31st day of March, 2022, after payment of fee in accordance with sub-rule (5A) of rule 114, his permanent account number shall become operative within thirty days from the date of intimation of Aadhaar number.

(3) A person, whose permanent account number has become inoperative, shall be liable for further consequences for the period commencing from the date as specified under sub-rule (4) till the date it becomes operative, namely:—

(i) refund of any amount of tax or part thereof, due under the provisions of the Act shall not be made;

(ii) interest shall not be payable on such refund for the period, beginning with the date specified under sub-rule (4) and ending with the date on which it becomes operative;

(iii) where tax is deductible under Chapter XVIIB in case of such person, such tax shall be deducted at higher rate, in accordance with provisions of section 206AA;

(iv) where tax is collectible at source under Chapter XVIIBB in case of such person, such tax shall be collected at higher rate, in accordance with provisions of section 206CC.

(4) The provisions of sub-rule (3) shall have effect from the date specified by the Board.

(5) The Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) shall specify the formats and standards along with the procedure for verifying the operational status of permanent account number under sub-rule (1) and sub-rule (2).]

Note:

5 Substituted by the IT (Fourth Amdt.) Rules, 2023, w.e.f. 1-4-2023

Rule – 114AAB

6 [Class or classes of person to whom provisions of section 139A shall not apply.

114AAB. (1) The provisions of section 139A shall not apply to a non-resident, not being a company, or a foreign company, (hereinafter referred to as the non- resident) who has, during a previous year, made investment in a specified fund if the following conditions are fulfilled, namely:—

i. the non-resident does not earn any income in India, other than the income from investment in the specified fund during the previous year;

ii. any income-tax due on income of non-resident has been deducted at source and remitted to the Central Government by the specified fund at the rates specified in section 194LBB of the Act; and

iii. the non-resident furnishes the following details and documents to the specified fund, namely:—

a. name, e-mail id, contact number;

b. address in the country or specified territory outside India of which he is a resident;

c. a declaration that he is a resident of a country or specified territory outside India; and

d. Tax Identification Number in the country or specified territory of his residence and in case no such number is available, then a unique number on the basis of which the non-resident is identified by the Government of that country or the specified territory of which he claims to be a resident.

(2) The specified fund shall furnish a quarterly statement for the quarter of the financial year, in which the details and documents referred to in clause (iii) of sub-rule (1) are received by it, in Form No. 49BA to the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) or the person authorised by him, electronically and upload the declaration referred to in sub-clause (c) of clause (iii) of sub-rule (1) within fifteen days from the end of the quarter of the financial year to which such statement relates in accordance with the procedures, formats and standards specified by the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) under sub-rule (3).

7[(2A) The provisions of section 139A shall not apply to a non-resident, being an eligible foreign investor, who has made transaction only in a capital asset referred to in clause (viiab) of section 47 which are listed on a recognised stock exchange located in any International Financial Services Centre and the consideration on transfer of such capital asset is paid or payable in foreign currency, if the following conditions are fulfilled, namely:—

i. the eligible foreign investor does not earn any income in India, other than the income from transfer of a capital asset referred to in clause (viiab) of section 47;

ii. the eligible foreign investor furnishes the following details and documents to the stock broker through which the transaction is made namely:—

a. name, e-mail id, contact number;

b. address in the country or specified territory outside India of which he is a resident;

c. a declaration that he is a resident of a country or specified territory outside India; and

d. Tax Identification Number in the country or specified territory of his residence and in case no such number is available, then a unique number on the basis of which the non-resident is identified by the Government of that country or the specified territory of which he claims to be a resident.

(2B) The stock broker shall furnish a quarterly statement for the quarter of the financial year, in which the details and documents referred to in sub-rule (2A) are received by it, in Form No. 49BA to the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) or the person authorised by him, electronically and upload the declaration referred to in sub-clause (c) of clause (ii) of sub-rule (2A) within fifteen days from the end of the quarter of the financial year to which such statement relates in accordance with the procedures, formats and standards specified by the Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) under sub-rule (3).]

(3) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) shall specify the procedures, formats and standards for the purposes of furnishing and verification of Form 49BA and shall be responsible for the day-to-day administration in relation to the furnishing and verification of quarterly statement 8[in accordance with the provisions of sub-rule (2) or sub-rule (2B)].

Explanation.—For the purposes of this rule—

9 [(a)”specified fund” means any fund established or incorporated in India in the form of a trust or a company or a limited liability partnership or a body corporate which has been granted a certificate of registration as a Category I or Category II Alternative Investment Fund and is regulated under the Securities and Exchange Board of India (Alternative Investment Funds) Regulations, 2012 made under the Securities and Exchange Board of India Act, 1992 (15 of 1992) or regulated under the International Financial Services Centres Authority (Fund Management) Regulations, 2022 made under the International Financial Services Centres Authority Act, 2019 (50 of 2019) and which is located in any International Financial Services Centre or a specified fund referred to in sub-clause (i) of clause (c) of Explanation to clause (4D) of section 10;]

(b) “International Financial Services Centre” shall have the same meaning as assigned to it in clause (q) of section 2 of the Special Economic Zones Act, 2005 (28 of 2005);]

10 [(c) “eligible foreign investor” means a non-resident who operates in accordance with the Securities and Exchange Board of India, Circular IMD/HO/FPIC/CIR/P/2017/003, dated 4th January, 2017;

(d) “stock broker” means a person having trading rights in a recognised stock exchange located in any International Financial Services Centre and the member of such exchange.]

Notes:

6 Inserted by the IT (Nineteenth Amdt.) Rules, 2020, w.e.f. 10-8-2020.

7 Sub-rules (2A) and (2B) inserted by the IT (Fourteenth Amdt.) Rules, 2021, w.e.f. 4-5-2021.

8 Substituted for “in accordance with the provisions of sub-rule (2)” by the IT (Fourteenth Amdt.) Rules, 2021, w.e.f. 4-5-2021.

9 Substituted by the IT (Twelfth Amdt.) Rules, 2023, w.e.f. 17-7-2023

10 Inserted by the IT (Fourteenth Amdt.) Rules, 2021, w.e.f. 4-5-2021.

Rule – 114B

11[Transactions in relation to which permanent account number is to be quoted in all documents for the purpose of clause (c) of sub-section (5) of section 139A.

114B. Every person shall quote his permanent account number in all documents pertaining to the transactions specified in the Table below, namely:—

TABLE

| Sl. No. | Nature of transaction | Value of transaction | ||||||||||||

| (1) | (2) | (3) | ||||||||||||

| 1. | Sale or purchase of a motor vehicle or vehicle, as defined in clause (28) of section 2 of the Motor Vehicles Act, 1988 (59 of 1988) which requires registration by a registering authority under Chapter IV of that Act, other than two wheeled vehicles. | All such transactions. | ||||||||||||

| 2. | Opening an account [other than a time-deposit referred to at Sl. No. 12 and a Basic Savings Bank Deposit Account] with a banking company or a co-operative bank to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act). | All such transactions. | ||||||||||||

| 3. | Making an application to any banking company or a co-operative bank to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act) or to any other company or institution, for issue of a credit or debit card. | All such transactions. | ||||||||||||

| 4. | Opening of a demat account with a depository, participant, custodian of securities or any other person registered under sub-section (1A) of section 12 of the Securities and Exchange Board of India Act, 1992 (15 of 1992). | All such transactions. | ||||||||||||

| 5. | Payment to a hotel or restaurant against a bill or bills at any one time. | Payment in cash of an amount exceeding fifty thousand rupees. | ||||||||||||

| 6. | Payment in connection with travel to any foreign country or payment for purchase of any foreign currency at any one time. | Payment in cash of an amount exceeding fifty thousand rupees. | ||||||||||||

| 7. | Payment to a Mutual Fund for purchase of its units. | Amount exceeding fifty thousand rupees. | ||||||||||||

| 8. | Payment to a company or an institution for acquiring debentures or bonds issued by it. | Amount exceeding fifty thousand rupees. | ||||||||||||

| 9. | Payment to the Reserve Bank of India, constituted under section 3 of the Reserve Bank of India Act, 1934 (2 of 1934) for acquiring bonds issued by it. | Amount exceeding fifty thousand rupees. | ||||||||||||

| 10. | Deposit with,—

|

Cash deposits,—

|

||||||||||||

| 11. | Purchase of bank drafts or pay orders or banker’s cheques from a banking company or a co-operative bank to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act). | Payment in cash for an amount exceeding fifty thousand rupees during any one day. | ||||||||||||

| 12. | A time deposit with,—

|

Amount exceeding fifty thousand rupees or aggregating to more than five lakh rupees during a financial year. | ||||||||||||

| 13. | Payment for one or more pre-paid payment instruments, as defined in the policy guidelines for issuance and operation of pre-paid payment instruments issued by Reserve Bank of India under section 18 of the Payment and Settlement Systems Act, 2007 (51 of 2007), to a banking company or a co- operative bank to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act) or to any other company or institution. | Payment in cash or by way of a bank draft or pay order or banker’s cheque of an amount aggregating to more than fifty thousand rupees in a financial year. | ||||||||||||

| 14. | Payment as life insurance premium to an insurer as defined in clause (9) of section 2 of the Insurance Act, 1938 (4 of 1938). | Amount aggregating to more than fifty thousand rupees in a financial year. | ||||||||||||

| 15. | A contract for sale or purchase of securities (other than shares) as defined in clause (h) of section 2 of the Securities Contracts (Regulation) Act, 1956 (42 of 1956). | Amount exceeding one lakh rupees per transaction. | ||||||||||||

| 16. | Sale or purchase, by any person, of shares of a company not listed in a recognised stock exchange. | Amount exceeding one lakh rupees per transaction. | ||||||||||||

| 17. | Sale or purchase of any immovable property. | Amount exceeding ten lakh rupees or valued by stamp valuation authority referred to in section 50C of the Act at an amount exceeding ten lakh rupees. | ||||||||||||

| 18. | Sale or purchase, by any person, of goods or services of any nature other than those specified at Sl. Nos. 1 to 17 of this Table, if any. | Amount exceeding two lakh rupees per transaction: |

Provided that where a person, entering into any transaction referred to in this rule, is a minor and who does not have any income chargeable to income-tax, he shall quote the permanent account number of his father or mother or guardian, as the case may be, in the document pertaining to the said transaction:

12[Provided further that any person, not being a company or a firm,] who does not have a permanent account number and who enters into any transaction specified in this rule, he shall make a declaration in Form No. 60 giving therein the particulars of such transaction 13[either in paper form or electronically under the electronic verification code in accordance with the procedures, data structures, and standards specified by the Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems)]:

14[Provided also that a foreign company who,—

(i) does not have any income chargeable to tax in India; and

(ii) does not have a permanent account number,

and enters into any transaction referred to at Sl. No. 2 or 12 of the Table, in an IFSC banking unit, shall make a declaration in Form No. 60:]

Provided also that the provisions of this rule shall not apply to the following class or classes of persons, namely :—

(i) does not have any income chargeable to tax in India; and

(ii) does not have a permanent account number,

15[Provided also that a person who has an account (other than a time deposit referred to at S. No.12 of the Table and a Basic Saving Bank Deposit Account) maintained with a banking company or a co-operative bank to which the Banking Regulation Act, 1949 (10 of 1949), applies (including any bank or banking institution referred to in section 51 of that Act) and has not quoted his permanent account number or furnished Form No. 60, as the case may be, at the time of opening of such account or subsequently, he shall furnish his permanent account number or Form No. 60, as the case may be, to the person specified in clause (c) of sub-rule (1) of rule 114C on or before the 16[30th day of June], 2017.]

Explanation.—For the purposes of this rule,—

14[(1)”IFSC banking unit” means a financial institution defined under clause (c) of sub-section (1) of section 3 of the International Financial Services Centres Authority Act, 2019 (50 of 2019), that is licensed or permitted by the International Financial Services Centres Authority to undertake permissible activities under the International Financial Services Centres Authority (Banking) Regulations, 2020;]

17[(1A)] “payment in connection with travel” includes payment towards fare, or to a travel agent or a tour operator, or to an authorised person as defined in clause (c) of section 2 of the Foreign Exchange Management Act, 1999 (42 of 1999);

(2) “travel agent or tour operator” includes a person who makes arrangements for air, surface or maritime travel or provides services relating to accommodation, tours, entertainment, passport, visa, foreign exchange, travel related insurance or other travel related services either severally or in package;

(3) “time deposit” means any deposit which is repayable on the expiry of a fixed period.

Notes:

11 Rules 114B to 114D substituted by the IT (Twenty-second Amdt.) Rules, 2015, w.e.f. 1-1-2016.

12 Substituted for “Provided further that any person” by the IT (Twenty-fourth Amdt.) Rules, 2023, w.e.f. 10-10-2023.

13 Inserted by the IT (Fourteenth Amdt.) Rules, 2017, w.e.f. 9-6-2017.

14 Inserted by the IT (Twenty-fourth Amdt.) Rules, 2023, w.e.f. 10-10-2023.

15 Inserted by the IT (First Amdt.) Rules, 2017, w.e.f. 6-1-2017.

16 Substituted for “28th day of February” by the IT (Seventh Amdt.) Rules, 2017, w.r.e.f. 1-3-2017.

17 Clause (1) renumbered as clause (1A) by the IT (Twenty-fourth Amdt.) Rules, 2023, w.e.f. 10-10-2023.

Rule – 114BA

18[Transactions for the purposes of clause (vii) of sub-section (1) of section 139A.

114BA. The following shall be the transactions for the purposes of clause (vii) of sub-section (1) of section 139A, namely:—

a. cash deposit or deposits aggregating to twenty lakh rupees or more in a financial year, in one or more account of a person with a banking company or a co-operative bank to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act) or a Post Office;

b. cash withdrawal or withdrawals aggregating to twenty lakh rupees or more in a financial year, in one or more account of a person with a banking company or a co-operative bank to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act) or a Post Office;

c. opening of a current account or cash credit account by a person with a banking company or a co-operative bank to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act) or a Post Office:]

19[Provided that the provisions of this rule shall not apply in a case,—

(a) where the person, making the deposit or withdrawal of an amount otherwise than by way of cash as per clause (a) or (b), or opening a current account not being a cash credit account as per clause (c) of this rule, is a non-resident (not being a company) or a foreign company;

(b) the transaction is entered into with an IFSC banking unit; and

(c) such non-resident (not being a company) or the foreign company does not have any income chargeable to tax in

Explanation.—For the purposes of this rule, “IFSC banking unit” shall have the same meaning as assigned to it in clause (1) of the Explanation to rule 114B.]

Notes:

18 Inserted by the IT (Fifteenth Amdt.) Rules, 2022. The amendment shall come into force after the expiry of fifteen days from 10-5-2022.

19 Inserted by the IT (Twenty-fourth Amdt.) Rules, 2023, w.e.f. 10-10-2023.

Rule – 114BB

20[Transactions for the purposes of sub-section (6A) of section 139A and prescribed person for the purposes of clause (ab) of Explanation to section 139A.

114BB. (1) Every person shall, at the time of entering into a transaction specified in column (2) of the Table below, quote his permanent account number or Aadhaar number, as the case may be, in documents pertaining to such transaction, and every person specified in column (3) of the said Table, who receives such document, shall ensure that the said number has been duly quoted and authenticated—

TABLE

| Sl. No. | Nature of transaction | Person |

| (1) | (2) | (3) |

| 1. | Cash deposit or deposits aggregating to twenty lakh rupees or more in a financial year, in one or more account of a person with,—

(i) A banking company or a co-operative bank to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act); (ii) Post Office |

(i) A banking company or a cooperative bank to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act);

(ii) Post Master General as referred to in clause (j) of section 2 of the Indian Post Office Act, 1898 (6 of 1898). |

| 2. | Cash withdrawal or withdrawals aggregating to twenty lakh rupees or more in a financial year, in one or more account of a person with,—

(i) A banking company or a co-operative bank to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act); (ii) Post Office |

(i) A banking company or a cooperative bank to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act);

(ii) Post Master General as referred to in clause (j) of section 2 of the Indian Post Office Act, 1898 (6 of 1898). |

| 3. | Opening of a current account or cash credit account by a person with,—

(i) A banking company or a co-operative bank to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act); (ii) Post Office |

(i) A banking company or a cooperative bank to which the Banking Regulation Act, 1949 (10 of 1949) applies (including any bank or banking institution referred to in section 51 of that Act);

(ii) Post Master General as referred to in clause (j) of section 2 of the Indian Post Office Act, 1898 (6 of 1898). |

21[Provided that the provisions of this sub-rule shall not apply in a case where the person, depositing the money as per Sl. No. 1 of column (2) or withdrawing money as per Sl. No. 2 of column (2) or opening a current account or cash credit account as per Sl. No. 3 of column (2) of the Table above, is the Central Government, the State Government or the Consular Office:]

22[Provided further that the provisions of this sub-rule shall not apply in a case,—

(a) where the person, making the deposit or withdrawal of an amount otherwise than by way of cash as per Sl. No. 1 or Sl. No. 2 of column (2), or opening a current account not being an cash credit account as per Sl. No. 3 of column (2) of the Table, is a non-resident (not being a company) or a foreign company;

(b) the transaction is entered into with an IFSC banking unit; and

(c) such non-resident (not being a company) or the foreign company does not have any income chargeable to tax in India.

Explanation.—For the purposes of this sub-rule, “IFSC banking unit” shall have the same meaning as assigned to it in clause (1) of the Explanation to rule 114B.]

(2) The permanent account number or Aadhaar number alongwith demographic information or biometric information of an individual shall be submitted to the Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) or the person authorised by the Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) with the approval of the Board, for the purposes of authentication referred to in section 139A.

(3) Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) shall lay down the formats and standards along with procedure for authentication of permanent account number or Aadhaar number.]

Notes:

20 Inserted by the IT (Fifteenth Amdt.) Rules, 2022. The amendment shall come into force after the expiry of sixty days from 10-5-2022.

21 Inserted by the IT (Twenty-ninth Amdt.) Rules, 2022, w.r.e.f. 9-7-2022.

22 Inserted by the IT (Twenty-fourth Amdt.) Rules, 2023, w.e.f. 10-10-2023

Rule – 114C

Verification of Permanent Account Number in transactions specified in rule 114B.

114C. (1) Any person being,—

a. a registering officer or an Inspector-General appointed under the Registration Act, 1908 (16 of 1908);

b. a person who sells the immovable property or motor vehicle;

c. a manager or officer of a banking company or co-operative bank, as the case may be, referred to at No. 2 or 3 or 10 or 11 or 12 or 13 of rule 114B;

d. post master;

e. stock broker, sub-broker, share transfer agent, banker to an issue, trustee of a trust deed, registrar to issue, merchant banker, underwriter, portfolio manager, investment adviser and such other intermediaries registered under sub-section (1) of section 12 of the Securities and Exchange Board of India Act, 1992 (15 of 1992);

f. a depository, participant, custodian of securities or any other person registered under sub-section (1A) of section 12 of the Securities and Exchange Board of India Act, 1992 (15 of 1992) referred to at Sl. No. 4 of rule 114B;

g. the principal officer of a company referred to at No. 3 or 4 or 8 or 12 or 13 or 15 or 16 of rule 114B;

h. the principal officer of an institution referred to at No. 2 or 3 or 8 or 10 or 11 or 12 or 13 of rule 114B;

i. any trustee or any other person duly authorised by the trustee of a Mutual Fund referred to at No. 7 of rule 114B;

j. an officer of the Reserve Bank of India, constituted under section 3 of the Reserve Bank of India Act, 1934 (2 of 1934), or of any agency bank authorised by the Reserve Bank of India;

k. a manager or officer of an insurer referred to at No. 14 of rule 114B,

who, in relation to a transaction specified in rule 114B, has received any document shall ensure after verification that permanent account number has been duly and correctly mentioned therein or as the case may be, a declaration in Form 60 has been duly furnished with complete particulars.

(2) Any person, being a person raising bills referred to at Sl. No. 5 or 6 or 18 of rule 114B, who, in relation to a transaction specified in the said Sl. No., has issued any document shall ensure after verification that permanent account number has been correctly furnished and the same shall be mentioned in such document, or as the case may be, a declaration in Form 60 has been duly furnished with complete particulars.

23 [(3) The person referred to in sub-rule (1) or sub-rule (2) who has received any document in which permanent account number is mentioned or as the case may be, a declaration in Form No. 60 has been furnished, shall ensure that the valid permanent account number or the fact of furnishing of Form No. 60, is duly mentioned in the records maintained for the transactions referred to in rule 114B and the permanent account number or the details of Form No. 60 are linked and mentioned in any information furnished to the income-tax authority or any other authority or agency under any provision of the Act or any rule prescribed therein.]

Note:

23 Inserted by the IT (First Amdt.) Rules, 2017, w.e.f. 6-1-2017.

Rule – 114D

Time and manner in which persons referred to in rule 114C shall furnish a statement containing particulars of Form No. 60.

114D. (1) Every person referred to in,—

I. 24[clauses (a)] to (k) of sub-rule (1) of rule 114C; and

II. sub-rule (2) of rule 114C and who is required to get his accounts audited under section 44AB of the Act,

who has received any declaration in Form No. 60, on or after the 1st day of January, 2016, in relation to a transaction specified in rule 114B, shall—

i. furnish a statement in Form No. 61 containing particulars of such declaration to the Director of Income-tax (Intelligence and Criminal Investigation) or the Joint Director of Income-tax (Intelligence and Criminal Investigation) through online transmission of electronic data to a server designated for this purpose and obtain an acknowledgement number; and

ii. retain Form No. 60 for a period of six years from the end of the financial year in which the transaction was undertaken.

(2) The statement referred to in clause (i) of sub-rule (1) shall,—

i. where the declarations are received by the 30th September, be furnished by the 31st October of that year; and

ii. where the declarations are received by the 31st March, be furnished by the 30th April of the financial year immediately following the financial year in which the form is received :

25[Provided that the statement in respect of the transactions listed in clause (ii) of column (3) of serial number (10) of the Table under rule 114B shall be furnished on or before the 15th day of January, 2017.]

(3) The statement referred to in clause (i) of sub-rule (1) shall be verified—

a. in a case where the person furnishing the statement is an assessee as defined in clause (7) of section 2 of the Act, by a person specified in section 140 of the Act;

b. in any other case, by the person referred to in rule 114C.]

26[(4) The Principal Director General of Income-tax (Systems) or Director General of Income-tax (Systems) shall specify the procedures, data structures, and standards for ensuring secure capture and transmission of data, evolving and implementing appropriate security, archival and retrieval policies in relation to the statement referred to in sub-clause (i) of sub-rule (1).]

Notes:

24 Substituted for “clauses (b)” by the IT (Twenty-sixth Amdt.) Rules, 2016, w.e.f. 6-10-2016.

25 Inserted by the IT (First Amdt.) Rules, 2017, w.e.f. 6-1-2017.

26 Inserted by the IT (Twenty-sixth Amdt.) Rules, 2016, w.e.f. 6-10-2016.

Income-tax Forms

Form No. : 1

1[Appendix IV

FORM NO. 1

[See rule 11UE (1)]

Undertaking under sub-rule (1) of rule 11UE of the Income-tax Rules, 1962

To,

Principal Commissioner/Commissione

………………….. ………………………. ……………………

Sir/Madam,

I …………………………………….. (name in block letters) son/daughter of …………………………………………. designation ………………………………….. and nationality …………………………………. and related passport number………………………………….. (hereinafter referred to as “signatory”) having Permanent Account Number/Aadhaar Number (see Note 1) …………………………………………………………………. on behalf of ………………………………………… (name of the declarant) having Permanent Account Number/Aadhaar number/Tax Deduction Account Number (see Note 2) ……………………………………….. and being duly authorised and competent to represent the declarant in this regard pursuant to Board Resolution and legal authorisation (see Note 3), as the case may be ,hereby declare as follows:

a. That specified orders have been passed or made in respect of income accruing or arising through or from the transfer of an asset or a capital asset situate in India in consequence of the transfer of a share or interest in a company or entity registered or incorporated outside India made before the 28th day of May, 2012 and particulars of such specified orders are provided in Part A of the Annexure.

b. The declarant has (strike off the options that are not applicable),

i. not filed any appeal or application or petition or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings constituted under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant orders, and hereby undertakes that it shall not file any appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such relevant order or orders are provided in Part B of the Annexure;

ii. filed one or more appeals or applications or petitions or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant orders and has irrevocably withdrawn, on a with prejudice basis, all such appeals or applications or petitions or proceeding and evidence thereof is furnished herewith and hereby undertakes that it shall not file any appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such appeals or applications or petitions or proceeding filed and irrevocably withdrawn with prejudice by the declarant, are provided in Part C of the Annexure;

iii. filed one or more appeals or applications or petitions or proceeding before any Income-tax authority or Authority for Advance Rulings constituted under section 245-O of the Act or the Board for Advance Rulings under section 245-OB or Income-tax Settlement Commission constituted under section 245B or the Interim Board for Settlement constituted under section 245AA or any tribunal or court against the relevant order or orders and all the appeals or applications or petitions or proceeding filed by the declarant have been disposed of and no further appeal or application or petition or proceeding has been filed by the declarant and evidence thereof is furnished herewith and hereby undertake that it shall not file any appeal, application, petition or proceeding in future against the relevant order or orders. Particulars of such appeals or applications or petitions or proceeding filed and disposed of, are provided in Part C of the Annexure;