Like Sec 115BAA of Income-tax Act 1961, the New Act (Income-tax Act 2025) is also having the option to choose pay the Income-tax under Regular method or under New Tax Regime (Sec 200) by the Domestic Companies.

FAQs on New Tax Regime for Domestic Companies under Income Tax Act, 2025

(1) Who is eligible to choose an option to pay Tax under section 200 of the Income Tax Act, 2025?

A person, being a Domestic Company is eligible to choose an option to pay Tax under section 200 of the Income Tax Act, 2025 (popularly known as ‘New Tax Regime’ for Companies).

Sec 2(42) defines ‘Domestic Company’ means—

(i) an Indian company; or

(ii) any other company which has made the prescribed arrangements within India for the declaration and payment of the dividends (including dividends on preference shares) payable out of its income liable to tax under this Act.

(2) What is the Income Tax Rate under the New Tax Regime for Domestic Companies?

The income-tax payable for a tax year shall be @ 22% in respect of the total income computed in the manner prescribed under Sec 200.;

In addition to the above Tax Rate of 22%, applicable surcharge and Cess shall also be payable, which will be prescribed in Finance Act of the respective Tax Year.

For the Tax year 2026-27, the Finance Act, 2026 prescribes a Surcharge of 10% and a Cess of 4%. The effective Tax Rate will be 25.168% as detailed below:

| Particulars | Rate | Effective Rate |

Remarks |

| Income Tax

Rate |

22% | 22.000% | (A) |

| Surcharge | 10% | 2.200% | (A) = 10% of A |

| Cess | 4% | 0.968% | (B) = 4% on (A+B) |

| Total Effective Rate | 25.168% | ||

(3) How to compute the Total Income under Sec 200?

The Total Income under section 200 shall be computed without any deduction under the following sections:

| Section / Chapter |

Remarks |

| Sec 45 (2) | Expenditure on scientific research by a company in the business of bio- technology or production of any article or thing, which is not specified in Schedule XIII will not be allowed as deduction. |

| Chapter VIII (Except Sec 146 or 148) | See Note – 1 |

| Sections Specified in 205(1)(a) to (g) | |

| Sec 33 (8) | Additional depreciation cannot be claimed on purchase of New Machinery or Plant. |

| Sec 45 (3) | Amount paid to a research association, University, Indian Institute of Technology for scientific research cannot be claimed. |

| Sec 46 | Whole of the capital expenditure cannot be claimed for specified businesses |

| Sec 47 (1)(a) | Expenditure on agricultural extension project |

| Sec 49

|

Site Restoration Fund for extracting, or producing petroleum or natural gas |

| Sec 144

|

Newly established units in SEZs (exemptions computed as per Sec 10AA of the Old IT Act, 1961) |

| Adjustment of

brought forward Losses |

Set-off of brought forward loss or unabsorbed depreciation, if it is due to deduction of specified amounts as listed above is not allowed.

– Unabsorbed depreciation on account of additional 20% depreciation claimed under sec 33(8) in earlier tax year is not allowed for set-off. Other than this, any other unabsorbed depreciation is allowed to be set-off. – This is applicable for unabsorbed depreciation of the amalgamating company eligible for set-off U/s. 116 in the hands of the amalgamated company for the tax year, in which the amalgamation was effected. i.e. – Unabsorbed depreciation on account of additional 20% depreciation claimed by amalgamating company the under sec 33(8) in earlier tax year is not allowed for set-off, if the amalgamated company opts to pay tax U/s. 200. |

Sec 200(3) states that the loss and depreciation referred above shall be deemed to have been given full effect to and no further deduction for such loss or depreciation shall be allowed for any subsequent year.

[Please read Q.No.4]

(4) X Limited, a Domestic Company was having unabsorbed depreciation of Rs.200 Lakhs, at the end of the FY 2025-26 (AY 2026-27). Out of this depreciation claimed under normal rate is Rs.150 Lakhs and additional depreciation claimed for new machineries under sec 33(8) was Rs.50 Lakhs. For the Tax year 2026-27, the Company wants to pay tax under section 200. Whether the additional depreciation of Rs.50 Lakhs, (which was included in the unabsorbed depreciation of Rs.200 Lakhs) should not be claimed while computing the Total Income under Sec 200 for the tax year 2026-27? Any alternate remedy is available or it should be treated as permanent disallowance.

As per Sub-section (1)(b) and (3) of Sec 200, the additional depreciation of Rs.50 Lakhs, (which was included in the unabsorbed depreciation of Rs.200 Lakhs) should not be claimed while computing the Total Income under Sec 200 while computing the Total Income under Sec 200 for the tax year 2026-27. Only an amount of Rs.150 Lakhs will be allowed for adjustment against the Income for the tax year 2026-27.

However, in some judicial decisions, the Courts have held that there is difference between depreciation ‘actually’ allowed and depreciation ‘deemed’ to have been allowed, which helped the Assessees to recompute the ‘Written-Down Value’ of the Assets, on which depreciation under section 38 is allowed.

The phrase ‘Written-Down Value’ is defined under Sec 41 of the Act –

For the purposes of computation of income under the head “Profits and gains of business or profession”, written down value means—

(a) in case the asset is acquired in the tax year, the actual cost to the assessee;

(b) in case the asset is acquired before the tax year, actual cost to the assessee less depreciation actually allowed under this Act or under the Income-tax Act, 1961 (43 of 1961);

(c) in case of block of assets, the written down value computed in the following manner:

[(A – D) + B – C] – E, where

A = the written down value of the block of assets in the immediately preceding tax year;

B = actual cost of any asset falling within that block, acquired during the tax year;

C = moneys payable together with scrap value, if any, in respect of any asset falling within the block, which is sold, transferred, demolished, destroyed or discarded during the tax year, where “C” shall not exceed (A – D) + B;

D = depreciation actually allowed in respect of block of assets in relation to the said immediately preceding tax year;

E = in the case of a slump sale, ….

In the case of X Limited, while computing the WDV of the Block of Machineries, the unabsorbed depreciation of Rs.50 Lakhs (which was the additional depreciation claimed in the last year, but not actually deducted and carried forward to next year) can be added to the ‘WDV’ while opting to pay the Tax under the New Tax Regime, since this amount was not ‘actually’ allowed to the Assessee.

Case Laws:

(i) Decision of High Court of Madras in the case of EID Parry (India) Ltd. v. Dy. Commissioner of Income-tax, Special Range-I, Chennai [2012] 23 com348 (Mad.)

(ii) Decision of High Court of Bombay in the case of Technova Imaging Systems Ltd. v. Deputy Commissioner of Income-tax [2025] 173 com405 (Bombay).

The Income Tax Act is having similar provisions in many sections (depreciation deemed to be allowed). We will now compare Sec 200 (New Tax Regime) with Sec 58 (Presumptive taxation):

| Sec 58 | Sec 200 |

| (4) Any loss, allowance ordeduction deduction allowable under the provisions of this Act, shall not be allowed against the income computed in the manner specified in sub- section (2).

(6) The written down value of any asset used for the purposes of specified business or profession shall be computed as if the assessee mentioned in column C of the Table in sub-section (2) had claimed and was actually allowed deduction in respect of depreciation thereon for each of the relevant tax years. |

(3) Any The loss and depreciation referred to in sub-section (1)(b) and (c) shall be deemed to have been given full effect to and no further deduction for such loss or depreciation shall be allowed for any subsequent year.

(No provision about computation of written down value) |

Summary:

(A) As Sec 200 restricted to assessee not to adjust the brought forward unabsorbed depreciation and does not have provisions related to computation of ‘WDV’, we have no other option but to compute ‘WDV’ in accordance with Sec 41.

(B) Sec 41 says WDV to be computed after deducting the depreciation ‘actually’ allowed.

(C) High Courts of Madras and Bombay categorically held that ‘deemed’ to be allowed is not ‘actually’ allowed.

(D) Hence X Limited can add back the amount of unabsorbed additional depreciation of Rs.50 Lakhs in computing the WDV of machinery block of assets while opting to pay the tax under New Tax Regime.

This is my personal view. I request readers to exercise cautions, while taking any decision for their companies, as the provisions / legal case laws will be different for different situation. I have explained a hypothetical question and tried to answer that theoretically. Please get a legal opinion from eminent Lawyers / Chartered Accountants for practical issues, before taking a decision.

(5) Assume that G Limited, a Domestic Company will file its Return of Income for the AY 2026-27 (FY 2025-26) with a Loss of Rs.180 Crores (unabsorbed depreciation) as per details given below:

| Particulars | Amount – Rs. In Crores | |

| Total Income before allowing depreciation U/s.32 | 100 | |

| Normal Depreciation U/s. 32(1)(ii) | 200 | |

| Normal Depreciation U/s. 32(1)(ii) | 80 | |

| Total Depreciation | 280 | |

| Total Income / (-) Loss i.e.Unabsorbed Depreciation | (-) 180 | |

Now G Limited would like to opt to pay tax under Section 200 for the Tax Year 2026-27. Whether the entire amount of unabsorbed depreciation of Rs.180 Crores will be available for set-off against the Income for the Tax Year 2026-27?

First we will analyse the Transitional Provision:

As per Sec 536(2)(r), the unabsorbed depreciation available under old Act will be allowed to be carried forward and shall be added to the amount of corresponding allowances of the New Act.

Hence the brought forward unabsorbed depreciation u/s. 32(2) of the Old Act of Rs.180 Crores will be added to the Depreciation amount for the Tax Year 2026-27 to be computed under Sec 33 of the New Act.

Second, let us analyse, whether the entire amount of Rs.180 Crores will be available for set-off, if New Tax Regime is opted:

As per Sec 200(1)(b)(iii), set-off of unabsorbed depreciation from any earlier tax year is not allowed, if such unabsorbed depreciation is attributable to additional depreciation computed as per Sec 33(8).

The unabsorbed depreciation brought forward under old Act will be added to the current year depreciation as per the provisions of Sec 536(2)(r). Hence it is not depreciation attributable to additional depreciation computed as per Sec 33(8). The Section should have clearly mentioned that-

set-off of unabsorbed depreciation from any earlier tax year is not allowed, if such unabsorbed depreciation is attributable to additional depreciation computed as per Sec 33(8) of the Act or Sec 32(1)(ii) of the Income-tax Act, 1961.

Even assuming (assumptions are not allowed in Tax Laws), that the amount specified U/s. 200(1)(b)(iii) includes unabsorbed depreciation attributable to additional depreciation computed Sec 32(1)(ii) of the Income-tax Act, 1961, G Limited still argue that unabsorbed depreciation of Rs.180 Crores is attributable to Normal Depreciation computed under Sec 32(1)(i) and not attributable to additional deprecation computed under Sec 32(1)(ii) of the Old Act, and hence entire unabsorbed depreciation of Rs.180 crores will be available for set-off, if the option to pay tax is exercised under Sec 200.

The Old Act or the New Act does not prescribe the order of adjustment of normal depreciation and additional depreciation. Unless there is an express provision to specify the order of such adjustment, G Limited can argue that it has adjusted the additional depreciation of Rs.80 Crores fully in the profits and gains of business of Rs.100 Crores and the normal depreciation of Rs.200 Crores is adjusted in the remaining profits of Rs.20 Crores and balance amount of Normal Unabsorbed depreciation of Rs.180 Crores is carried forward.

(6) Z Limited, a Domestic Company, opted to pay the tax under New Tax Regime and filed its Return of Income accordingly. The Assessing officer found that the Company has failed to satisfy the requirements of Sec 200(1). What are the consequences?

As per Sec 200(2), where the person fails to satisfy the requirements contained in sub-section (1) in any tax year, the option shall become invalid in respect of the said tax year and subsequent years and other provisions of the Act shall apply, as if the option had not been exercised for such tax year and for subsequent years.

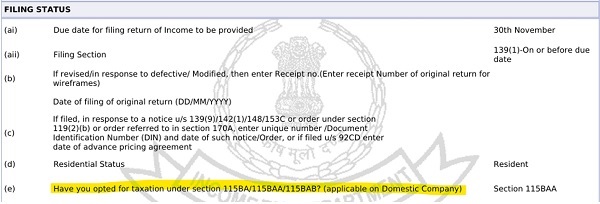

(7) X Limited, decides to pay tax under Sec 200 for the Tax Year 2026-27. What is the procedure to choose this option and how to communicate such option to Income Tax Department?

The option to pay the Tax under Sec 200 should be exercised by X Limited on or before the due date specified under section 263(1) for furnishing the return of income.

As per Rule 136 of the Income Tax Rules, 2026 such option shall be exercised in the Return of Income.

The Return of Income is having a specific column to select this option. For example, the Return of Income for the AY 2025-26 was having the following provision:

(8) X Limited, which decides to pay tax under Sec 200 for the Tax Year 2026-27. What is the procedure to change such option for the same tax year? Is it possible to change the option for subsequent tax years?

No, it is not possible to change such option. The option once exercised, shall apply to subsequent tax years also.

Once the option under this section has been exercised for any tax year, it shall not be subsequently withdrawn for the same or any other tax year.

(9) Y Limited is having a MAT credit of Rs.150 Crores under Section 115JAA of the Income Tax Act, 1961 as at the end of the FY 2025-26. Such credits are allowed to be carried forward under the New Act also as per the provisions of Sec 536(2)(l). Whether the MAT credit can be adjusted against the tax liability of Y Limited, if it opts to pay the tax under Sec 200 for the tax year 2026-27? If the tax liability for the Tax Year 2026-27 will be Rs.100 Crores, how much credit can be adjusted?

Yes, the Finance Act, 2026 has amended Sec 206 (3) of New Act, by which, it has given some relief for the Companies, opting to pay the Tax under New Tax Regime.

The MAT credit as on 31st March 2026 which is allowed to be carried forward to the assessee under the provisions of section 115JAA of the Income-tax Act 1961 –

(a) shall be allowed to be set off in any tax year to the extent of 25% of the tax payable on the total income computed as per the other provisions of this Act for that tax year.

(b) the remaining credit shall be carried forward to the subsequent tax year; and

(c) such carry forward or set off of tax credit shall not be allowed beyond the fifteenth tax year immediately succeeding the tax year in which the tax credit first became allowable under section 115JAA of the Income-tax Act, 1961.

Hence, it the case of Y Limited, it can adjust Rs.25 Crores (25% of Tax payable of Rs.100 Crores) for the Tax Year 2026-27 and the remaining amount will be carried forward to the next tax year (maximum upto 15 years from the tax year in which the tax credit first became allowable under section 115JAA)

Note:

Companies which had opted (until AY 2025-26) / will opt (AY 2026-27) to pay tax under New Tax regime under Sec 115BAA of the Old Act, will be in a disadvantageous position, as the MAT credits were denied / will be denied to them as per Sec 115JAA(8).

I am of the opinion that this a fit case for filing a Writ petition before the High Court / Supreme Court for differential treatment, wherein a Company which had decided to pay the tax under New Tax Regime is being penalised and for those who have opted it much later years are enjoying the benefits. Let us wait and watch.

*****

Disclaimer: Views expressed are purely personal and for academic purpose only. Readers are advised to refer to the Income-tax Act, 1961 and the Income-tax Act, 2025 before taking any decision. The author is not responsible for consequences arising from reliance on this article.

Author Bio