The Income-tax Act, 2025 introduces a structured New Tax Regime under Section 202 for individuals, Hindu Undivided Families (HUFs), associations of persons, bodies of individuals, and artificial juridical persons. Similar to the earlier system under the Income-tax Act, 1961, taxpayers can choose between the normal tax method and the new regime. Under the new regime, concessional tax rates apply along with a rebate under Section 156, which allows a rebate of up to ₹60,000 where total income does not exceed ₹12 lakh, effectively reducing tax liability to zero in many cases. If income exceeds ₹12 lakh, rebate may still apply in limited situations based on excess income calculations. While several exemptions and deductions continue to be allowed—such as standard deduction, NPS contribution, gratuity, and certain allowances—many traditional benefits like HRA, LTA, and most Chapter VIII deductions are disallowed. The regime is the default tax system, but taxpayers may opt out when filing returns, with specific rules for those having business income.

PROVISIONS RELATED TO “NEW TAX REGIME” FOR INDIVIDUAL, HUF ETC., UNDER INCOME TAX ACT, 2025

Like Income-tax Act 1961, the New Act (Income-tax Act 2025) is also having the option to choose pay the Income-tax under Regular method or under New Tax Regime (Sec 202) by the following assessees:

a. an individual; or

b. a Hindu undivided family; or

c. an association of persons (other than a co-operative society); or

d. a body of individuals, whether incorporated or not; or

e. an artificial juridical person referred to in section 2(77)(g).

The details of provisions of new tax regime under section 202 is given below:

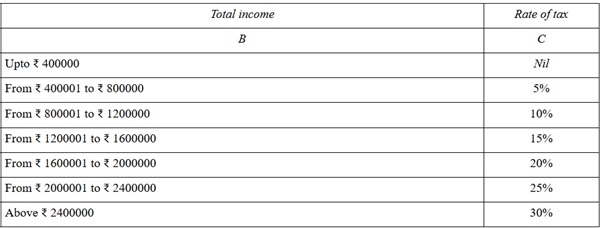

A. TAX RATES APPLICABLE FOR NEW TAX REGIME

B. REBATE UNDER SEC 156

If an Assessee chooses to pay the Income-tax under the New Tax Regime, then Tax Rebate will be available under Sec 156 (2). The Assessee shall deduct the following from income-tax:

| Scenario | Amount of Tax Rebate |

| 1. If the Income does not exceed Rs.12 Lakhs. | 100% of tax payable or Rs.60,000/-, whichever is less. |

| 2. If the Income exceeds Rs.12 Lakhs. (Tax Rebate is available to Assessees, in select cases, where the following dual conditions are met).

a. Excess Income (E) = Total Income−12,00,000 b. Income Tax Payable>Excess Income |

Tax Rebate=Income Tax Payable−(Total Income−12,00,000) |

Examples:

Scenario – 1: (If the Income does not exceed Rs.12 Lakhs.)

| Total Income | Income-tax (before rebate) | Rebate U/s.156 | Final Tax |

| 10,00,000 | 50,000 | 50,000 | 0 |

| 11,50,000 | 58,000 | 58,000 | 0 |

| 12,00,000 | 60,000 | 60,000 | 0 |

Scenario – 2: Example – 1

If the Total Income is Rs.12,50,000, then the rebate u/s.156 is computed as under:

Step-1 – Computation of Tax Payable (before Rebate):

| Income Slab | Rate | Tax |

| 0 – 4,00,000 | 0% | 0 |

| 4,00,000 – 8,00,000 | 5% | 20,000 |

| 8,00,000 – 12,00,000 | 10% | 40,000 |

| 12,00,000 – 12,50,000 | 15% | 7,500 |

| TOTAL Tax before Rebate | 67,500 |

Step-2 – Computation of Excess Income =

Total Income – 1200000 = 12,50,000-12,00,000 = 50,000

Step -3 : Is Tax payable is more than Excess Income.

Yes (67,500 > 50,000)

Step -4 : Computation of Tax Rebate.

Tax Rebate=Income Tax Payable−(Total Income−12,00,000)

= 67,500 (-) [12,50,000 (-) 12,00,000]

= 67,500 (-) 50,000

= 17,500

Final Tax Payable:

| Tax Payable as per Step – 1 (before Rebate) | 67,500 |

| Rebate computed in Step 4 | 17,500 |

| Tax Payable | 50,000 |

Scenario – 2: Example – 2

If the Total Income is Rs.13,00,000, then the rebate u/s.156 is computed as under:

Step-1 – Computation of Tax Payable (before Rebate):

| Income Slab | Rate | Tax |

| 0 – 4,00,000 | 0% | 0 |

| 4,00,000 – 8,00,000 | 5% | 20,000 |

| 8,00,000 – 12,00,000 | 10% | 40,000 |

| 12,00,000 – 13,00,000 | 15% | 15,000 |

| TOTAL Tax before Rebate | 75,000 |

Step-2 – Computation of Excess Income =

Total Income – 1200000 = 13,00,000-12,00,000 = 1,00,000

Step -3 : Is Tax payable is more than Excess Income.

No, Tax payable of Rs.75,000 is less than Excess Income of Rs.1,00,000

Step -4 : Computation of Tax Rebate.

Nil (Condition of Income Tax Payable>Excess Income failed)

Final Tax Payable:

| Tax Payable as per Step – 1 (before Rebate) | 75,000 |

| Rebate computed in Step 4 | Nil |

| Tax Payable | 75,000 |

C. EXEMPTIONS & DEDUCTIONS ALLOWED

The Act stipulates the exemptions / deductions, which are not available under New Tax Regime (Negative List) and the same is furnished in Para C below. Other than this, all other deductions / exemptions are available to the Assessee both under Normal method and New Tax Regime.

Few examples of deductions / exemptions available under New Tax Regime is given below: (Not an exhaustive list)

| Sl No | Type of Exemptions / deductions allowed | Reference |

| 1 | any allowance granted to meet the cost of travel on tour or on transfer | Sl. No. 12 of Schedule III read with Rule 280(1)(a) |

| 2 | any sum paid in connection with transfer, packing and transportation of personal

effects on such transfer |

Sl. No. 12 of Schedule III read with Rule 280(1)(b) |

| 3 | any allowance, whether granted on tour or for the period of journey in connection with transfer, to meet the ordinary daily charges incurred by an employee on account of absence from his normal place of duty. | Sl. No. 12 of Schedule III read with Rule 280(1)(c) |

| 4 | any allowance granted to meet the expenditure incurred on conveyance in

performance of duties of an office or employment of profit where no free conveyance is provided by the employer. |

Sl. No. 12 of Schedule III read with Rule 280(1)(d) |

| 5 | Standard Deduction of Rs.75,000/- or the salary whichever is lower | Sec 19(1) – Table Sl. No.2 |

| 6 | Gratuity | Sec 19(1) – Table Sl. No.3,4,5 or 6 |

| 7 | Payment in commutation of pension | Sec 19(1) – Table Sl. No.7,8, or 9 |

| 8 | Retrenchment compensation | Sec 19(1) – Table Sl. No.10 or 11 |

| 9 | VRS payments | Sec 19(1) – Table Sl. No.12 |

| 10 | Leave Salary | Sec 19(1) – Table Sl. No.13 or 14 |

| 11 | Contribution to NPS fund by the Employer to the extent of 14% of the Salary | Sec 124(1) & (2) |

| 12 | Amount of contribution to Agniveer Corpus Fund made in respect of the Assessee by Central Government | Sec 125 |

| 13 | Deduction in respect of additional employee cost (30% for 3 years) | Sec 146 |

In addition to the above exemptions / deductions, other deductions / exemptions (other than those given in C below) are automatically available under New Tax Regime. The above list is given only for easy reference.

D. EXEMPTIONS & DEDUCTIONS NOT ALLOWED:

| Sl No | Type of Exemptions / deductions not allowed | Reference |

| 1 | Any Allowance received by MPs or MLAs | Sl. No. 5, 6, 7 of Schedule III |

| 2 | Leave Travel Allowance (LTA) | Sl. No. 8 of Schedule III |

| 3 | House Rent Allowance (HRA) | Sl. No. 11 of Schedule III |

| 4 | Exemption of Rs.1,500/- for each of minor child, in case of clubbing provision u/s. 99(1)(c) | Sl. No. 17 of Schedule III |

| 5 | any allowance granted to meet the expenditure incurred on a helper. | Sl. No. 12 of Schedule III read with Rule 280(1)(e) |

| 6 | any allowance granted for encouraging the academic, research and training in educational and research institutions. | Sl. No. 12 of Schedule III read with Rule 280(1)(f) |

| 7 | Uniform Allowance | Sl. No. 12 of Schedule III read with Rule 280(1)(g) |

| 8 | Remote Locality Allowance / Tough Location Allowance-I, II & III in the places of J&K, Himachal etc., | Sl. No. 13 of Schedule III read with Rule 280(2) Table – Sl. No.1, 2 & 3 |

| 9 | Compensatory Field Area Allowance / Compensatory Modified Field Area Allowance. | Table – Sl. No.4 & 5 |

| 10 | Allowances granted to employees working in transport system | Table – Sl. No.6 |

| 11 | Children Education Allowance / Hostel Expenditure | Table – Sl. No.7 & 8 |

| 12 | Counter-insurgency allowance / highly active field area allowance / Island (duty) allowance / Siachen Allowance paid to Armed forces | Table – Sl. No.9, 13, 14 & 15 |

| 13 | Transport allowance granted to an employee, being differently abled (blind , deaf, dump etc.,) | Table – Sl. No.10 |

| 14 | High Altitude Allowance | Table – Sl. No.11 |

| 15 | Underground Allowance | Table – Sl. No.12 |

| 16 | Newly established units in SEZs (exemptions computed as per Sec 10AA of the Old IT Act, 1961) | Sec 144 |

| 17 | Tax on Employment | Sec 19(1) – Table Sl.No.1 |

| 18 | Interest on borrowed capital for self-occupied properties | Sec 22 (1)(b) read with Sec 21 (6) |

| 19 | Additional Depreciation for new Machinery | Sec 33(8) |

| 20 | Tea / Coffee / Rubber development account | Sec 48 |

| 21 | Site Restoration Fund for extracting, or producing petroleum or natural gas | Sec 49 |

| 22 | Expenditure on scientific research | Sec 45(3)(a), (b) or (c) |

| 23 | Capital expenditure of specified business | Sec 46 |

| 24 | Expenditure on agricultural extension project | Sec 47 (1)(a) |

| 25 | All deductions under Chapter VIII (equivalent to Chapter VIA of Old IT Act, 1961), except the provisions of sections 124(1) and 124(2), or 125(2) or 146 | Chapter VIII |

| 26 | Set-off of brought forward loss or unabsorbed depreciation, if it is due to deduction of specified amounts as listed above | |

| 27 | Set-off of House property loss with any other heads of income | |

| 28 | Any exemption or deduction for allowances or perquisite, called by any name, provided under any other law in force |

E. HOW TO EXERCISE THE OPTION TO PAY TAX UNDER NEW TAX REGIME

If the Assessee does not have Business Income:

a. The Assessee, by default, will be paying the tax under New Tax Regime under Sec 202, unless he exercises an option to Pay the Tax under the Normal Method.

b. The option to pay tax under Normal method can be exercised while filing the Return of Income U/s. 263.

c. This option can be modified, every Tax Year, if the Assessee wishes to change the Tax methods.

For Example: For the Tax year 2026-27, he can choose to pay tax under Normal method, in the next year 2027-28, he may choose to pay tax under New Tax Regime u/s. 202 and in the tax year 2028-29, he can choose to pay tax under Normal method and so on.

The Assessee has to choose his option in the Return of Income as given below:

| Tax Year | Type of Tax payment | Particulars in the Return of Income | Answer |

| 2026-27 | Normal method | Do you wish to exercise the option u/s 202(4) of Opting out of new tax regime? (default is “No”) | Yes |

| 2027-28 | New Tax Regime | Do you wish to exercise the option u/s 202(4) of Opting out of new tax regime? (default is “No”) | No |

| 2028-29 | Normal method | Do you wish to exercise the option u/s 202(4) of Opting out of new tax regime? (default is “No”) | Yes |

We have to carefully select the option, as the question is opt-out of New Tax Regime. Hence if you wish to pay the tax under New Tax Regime, you have to choose “No” i.e. not opting-out of New Tax Regime.

If the Assessee has Business Income:

For Assessee having business income,

a. he can opt to pay tax under New Tax Regime in any tax year, and the option once chosen will be applicable to all subsequent tax years.

b. He can withdraw the option only once in a life time and once the option is withdrawn, he cannot opt to pay the tax under New Tax Regime thereafter.

c. The option under (a) or withdrawal under (b) above can be exercised while filing the Return under Sec 263.

F. DUE DATE TO EXERCISE THE OPTION TO PAY TAX UNDER NEW TAX REGIME

The option should be exercised on or before the due date for furnishing the Return u/s. 263(1)*, which is reproduced below:

| Assessee Type | Due Date * |

| 1. All types of Assessees,

2. Partners of the firm or the spouse of such partner (if section 10 applies to such spouse), who is required to be furnished a report referred to in section 172 (Transfer pricing). |

30th November |

| 1. Company,

2. Assessee (other than a company) whose accounts are required to be audited under this Act or under any other law in force; 3. Partner of a firm whose accounts are required to be audited under this Act or under any other law in force; or the spouse of such partner (if section 10 applies to such spouse). |

31st October |

| 1. Assessee having income from profits and gains of business or profession whose accounts are not required to be audited under this Act or under any other law in force.

2. Partner of a firm whose accounts are not required to be audited under this Act or under any other law in force or the spouse of such partner (if section 10 applies to such spouse). |

31st August |

| 1. Any other assessee | 31st July |

* As amended by the Finance Bill, 2026.

** All the Rules referred in this article are based on Draft Income Tax Rules, 2026. Final Rules yet to be notified as on 15-03-2026.

Disclaimer: Readers are advised to refer to the Income-tax Act, 1961 and the Income-tax Act, 2025 before taking any decision. The author is not responsible for consequences arising from reliance on this article.

***

(Republished with amendments)

Author Bio

Please send the article in PDF format regarding New Tax Regime Provisions under Income-tax Act 2025 for Individual & HUF