Case Law Details

M. Abdul Mannan Vs ITO (ITAT Hyderabad)

ITAT Upholds Revision u/s 263 in Cancelled Sale Deed Case – AO Faulted for Accepting “No Capital Gains” Claim Without Proper Enquiry

The Hyderabad ITAT upheld the Principal CIT’s revisionary order u/s 263, holding that the Assessing Officer had accepted the assessee’s claim of “no capital gains” arising from a registered property sale without conducting proper enquiry and verification. The Tribunal observed that the registered sale deed itself recorded receipt of consideration of ₹1.09 crore and handing over of possession on the date of registration, yet the AO merely relied on a later cancellation deed and accepted the explanation without deeper verification.

The Tribunal noted that the PCIT had specifically pointed out failures on the part of the AO to verify revenue records, banking transactions and the actual flow of consideration. The purchaser’s statement recorded u/s 131 also stated that the cancellation deed was executed to overcome capital gains liability and avoid appellate proceedings.

Rejecting the assessee’s argument that the AO had adopted a “possible view”, the ITAT held that Explanation 2(a) to section 263 squarely applied where assessment orders are passed without making enquiries or verifications which ought to have been made. The Tribunal clarified that the PCIT had not conclusively decided taxability but had only directed fresh examination of the capital gains issue after proper enquiry.

The order is also notable for condoning delay in filing appeal by applying the Supreme Court’s Covid limitation extension orders, holding that the assessee’s appeal filed on 30.05.2022 fell within the extended limitation period granted by the Apex Court.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

This appeal is filed by Shri M. Abdul Mannan, (“the assessee”), feeling aggrieved by the order passed by the Learned Principal Commissioner of Income Tax, Tirupati (“Ld. PCIT”) dated 11.03.2021 for the A.Y. 2011-12.

2. At the outset, it is noticed that there is a delay of 376 days in filing the present appeal before this Tribunal against the order passed by the Ld. PCIT under section 263 of the Income Tax Act, 1961 (“the Act”) dated 11.03.2021. In support of the condonation petition, the assessee has filed an affidavit explaining the reasons for delay in filing the appeal before this Tribunal. The Learned Authorized Representative (“Ld. AR”) submitted that the delay is covered by the extension of limitation granted by the Hon’ble Supreme Court in Suo Motu Writ Petition (Civil) no.3 of 2020 read with Miscellaneous Application No.665 of 2021 in Miscellaneous Application No.21 of 2022 dated 10.01.2022, passed in view of the Covid-19 pandemic. Inviting our attention to para no.5(I) of the said order, the Ld. AR submitted that where the period of limitation fell within the period from 15.03.2020 to 28.02.2022, the same stood extended till 28.02.2022. Further, by referring to para no.5 (III) of the said order, the Ld. AR submitted that the Hon’ble Supreme Court had further directed that in cases where the limitation expired during the aforesaid period, all persons shall have a limitation period of 90 days from 01.03.2022. Accordingly, it was submitted that since the limitation period of filing the appeal before the Tribunal against the order passed by the Ld. PCIT under section 263 of the Act dated 11.03.2021 falls within the aforesaid period, the limitation for filing the appeal before this Tribunal stood extended till 30.05.2022. As the assessee has filed the appeal before this Tribunal on 30.05.2022, therefore the delay deserves to be condoned.

3. Per contra, the Ld. DR did not raise any serious objection to the condonation of delay.

4. We have heard the rival submission and considered the material available on record. We have also gone through para nos.5(I) to 5(III) of the order of the Hon’ble Supreme Court in Suo Motu Writ Petition (Civil) No.3 of 2020 (Supra), which is to the following effect:

“5. Taking into consideration the arguments advanced by learned counsel and the impact of the surge of the virus on public health and adversities faced by litigants in the prevailing conditions, we deem it appropriate to dispose of the M.A. No. 21 of 2022 with the following directions:

I. The order dated 23.03.2020 is restored and in continuation of the subsequent orders dated 08.03.2021, 27.04.2021 and 23.09.2021, it is directed that the period from 15.03.2020 till 28.02.2022 shall stand excluded for the purposes of limitation as may be prescribed under any general or special laws in respect of all judicial or quasi-judicial proceedings.

II. Consequently, the balance period of limitation remaining as on 03.10.2021, if any, shall become available with effect from 01.03.2022.

III. In cases where the limitation would have expired during the period between 15.03.2020 till 28.02.2022, notwithstanding the actual balance period of limitation remaining, all persons shall have a limitation period of 90 days from 01.03.2022. In the event the actual balance period of limitation remaining, with effect from 01.03.2022 is greater than 90 days, that longer period shall apply.”

5. On perusal of the above paragraph No.5(I), we find that the Hon’ble Supreme Court has extended the period of limitation falling within the period from 15.03.2020 to 28.02.2022 till 28.02.2022. Further on perusal of para no.5(III), we find that the Hon’ble Supreme Court has granted a period of 90 days from 01.03.2022. Since the limitation period of filing the appeal against the impugned order under section 263 of the Act dated 11.03.2021 falls within the aforesaid period, the limitation for filing the present appeal before this Tribunal stood extended till 30.05.2022 in terms of the directions of the Hon’ble Supreme Court. The assessee has filed the present appeal on 30.05.2022. Accordingly, considering the facts and circumstances of the case and respectfully following the directions of the Hon’ble Supreme Court, we condone the delay in filing the present appeal and admit the appeal for adjudication on merits.

6. The assessee has raised the following grounds of appeal:

“1. The Learned Principal Commissioner of Income Tax-Central/Tirupati erred on facts of the case and the law involved in so far as it is prejudicial to the interest of the Appellant.

2. The Learned Principal Commissioner of Income Tax-Central/Tirupati has erred in passing orders under section 263 directing the A.O to invoke provisions of Section 45 without considering submissions made by the assessee.

3. On the facts and in the circumstances of the case, the Learned Principal Commissioner of Income Tax-Central/Tirupati erred in assuming jurisdiction under section 263 of the Act in order to impost his own views on the Ld. A.O when the A.O had taken a possible view.

4. The impugned order passed by the A.O originally being neither erroneous nor prejudicial to the interest of the revenue, the Ld. Pr. CIT wrongly invoked jurisdiction by making allegation which is not supported by any contra evidence or by law.

5. The Ld. Pr. CIT erred on facts as also in law in having exercised revisionary power under section 263 on the issues which were beyond the jurisdiction of A.O while framing original assessment under section 143(3), as interpreted by various Courts and hence the order passed under section 263 is totally unjustified on facts as also in law and liable to be quashed.

6. The Learned Principal Commissioner of Income Tax-Central/Tirupati ought to have considered the Cancellation Deed produced by the assessee and observed that no capital gains were liable to be taxed in the hands of the appellant.

7. To modify the grounds raised or to raise any other ground(s) not raised with the permission of the Hon’ble Members of the Income Tax Appellate Tribunal Hyderabad”.

7. The assessee has raised the following Additional ground of appeal:

“1. The Ld. PCIT has erred in passing order under section 263 without proper DIN, which is mandatory procedure prescribed by the CBDT vide Circular No.19/2019 and hence the order passed is invalid and is to be treated to have never been issued”

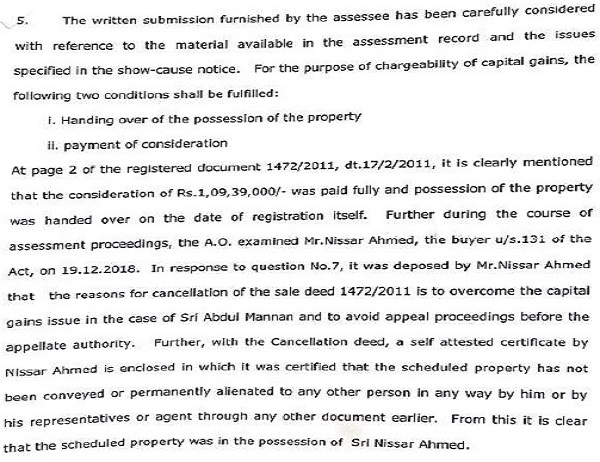

8. The brief facts of the case are that the assessee is an individual deriving income from retail trade of weights and measurement items under the name and style of M/s Al-Madeena Agencies. The assessee filed his return of income for Assessment Year 2011-12 on 31.03.2012 declaring total income of Rs.1,95,960/-. Subsequently, the case of the assessee was reopened under section 147 of the Act and assessment under section 143(3) of the Act was completed on 21.12.2018 determining total income of the assessee at Rs.3,95,960/-. Thereafter, on examination of assessment records of the assessee, the Ld. PCIT observed that during the course of assessment proceedings, the assessee had furnished one cancellation deed No.15359/2018 dated 17.12.2018 in respect of sale deed No.1472/2011 dated 17.02.2011 and the Learned Assessing Officer (“Ld. AO”) accepted the same without making any addition towards capital gains. According to the Ld. PCIT, the assessment order was passed without conducting proper enquiry and verification with respect to chargeability of capital gains arising from sale of immovable property. Accordingly, the Ld. PCIT issued show cause notice under section 263 of the Act dated 14.02.2020. In response thereto, the assessee filed detailed written submissions contending that the sale transaction dated 17.02.2011 was subsequently cancelled by mutual consent and therefore no capital gains arose in the hands of the assessee. The assessee further submitted before the Ld. PCIT that no consideration was actually received and the property continued to remain in his possession. However, the Ld. PCIT, after considering the submissions of the assessee and material available on record, observed that as per the registered sale deed dated 17.02.2011, consideration of Rs.1,09,39,000/- was stated to have been received and possession was also handed over on the date of registration itself. The Ld. PCIT further observed that the statement recorded from the purchaser under section 131 of the Act revealed that the cancellation deed was executed only to overcome capital gains liability and avoid appellate proceedings. The Ld. PCIT also noted that the Ld. AO had failed to conduct independent enquiry from revenue authorities and failed to verify banking transactions relating to receipt of sale consideration. The Ld. PCIT further relied upon the decision of the Hon’ble Kerala High Court in the case of CIT Vs. Harbour View (ITA No.33 of 2010, dated 24.09.2018) and observed that subsequent rescission of contract would not absolve tax liability arising under section 45 of the Act. The Ld. PCIT also referred to the judgment of the Hon’ble Andhra Pradesh High Court in the case of Smt. P. Veda Kumari and Others Vs. SRO in W.P. No. 4174/2008 and held that registration authorities are not empowered to cancel a registered sale deed in absence of orders from a competent court. Accordingly, the Ld. PCIT held that the assessment order passed by the Ld. AO under section 143(3) of the Act, dated 21.12.2018 was erroneous insofar as it was prejudicial to the interests of Revenue within the meaning of section 263 of the Act and set aside the assessment order with direction to the Ld. AO to redo the assessment de novo after proper enquiry and verification regarding chargeability of capital gains.

9. Aggrieved by the order passed by the Ld. PCIT under section 263 of the Act, the assessee is in appeal before this Tribunal. At the outset, the Ld. AR submitted that the assessee is not pressing the additional ground filed before this Tribunal. Accordingly, additional ground raised by the assessee is dismissed, being not pressed.

10. The Ld. AR further submitted that the Ld. AO had conducted adequate enquiry during the course of assessment proceedings and after examining the cancellation deed as well as statement recorded under section 131 of the Act, accepted the explanation of the assessee that no capital gains were chargeable to tax. The Ld. AR submitted that prior to execution of the sale deed dated 17.02.2011 in favour of Shri S. Nisar Ahmed, (english translated copy of sale deed is placed at page nos.7 and 8 of the paper book), the assessee had already executed a sale deed for the same property in favour of Shri M.V. Lokeshwar Reddy vide sale deed dated 05.11.2007 (english translated copy of which is placed at page nos.1 and 2 of the paper book). The Ld. AR submitted that the assessee had executed the sale deed dated 05.11.2007 in favour of Shri M.V. Lokeshwar Reddy on the basis of his promise that after execution of the sale deed, he would pay the sale consideration to the assessee. However, subsequently Shri M.V. Lokeshwar Reddy denied payment of the sale consideration and accordingly the assessee did not receive any sale consideration in respect of the said transaction. The Ld. AR further submitted that consequently the assessee filed suit for cancellation of the said sale deed before the competent court. Inviting our attention to the order of the court placed at page nos.38 and 39 of the paper book, the Ld. AR submitted that the assessee succeeded in the said suit and the Hon’ble Court vide ex party order dated 30.12.2010 set aside the sale deed dated 05.11.2007 executed in favour of Shri M.V. Lokeshwar Reddy and accordingly restored the property in favour of the assessee. The Ld. AR submitted that thereafter the assessee executed second sale deed in favour of Shri S. Nisar Ahmed duly informing him about the pending litigation and Shri S. Nisar Ahmed promised to pay the sale consideration amount after resolution of litigation. However, in the sale deed executed in favour of Shri S. Nisar Ahmed, it was recorded that sale consideration was paid to the assessee. The Ld. AR submitted that subsequently Shri M.V. Lokeshwar Reddy filed petition before the court seeking setting aside of the order dated 30.12.2010 and the dispute is still pending before the Hon’ble Court. The Ld. AR further submitted that the assessee had not received any consideration against the subsequent sale deed executed in favour of Shri S. Nisar Ahmed. Relying upon the decision of the Hon’ble Patna High Court in the case of Smt. Raj Rani Devi Ramna Vs. CIT reported in 201 ITR 1032, the Ld. AR submitted that in absence of receipt of consideration, the sale cannot be considered to have been effectively executed and therefore no capital gains can arise in the hands of the assessee. The Ld. AR further invited our attention to page no.6 of the assessment order and submitted that after considering all aspects of the matter, the Ld. AO had accepted the explanation of the assessee and therefore it cannot be said that the Ld. AO failed to verify the issue. Relying upon the decision of the Hon’ble Supreme Court in the case of Malabar Industrial Co. Ltd. Vs. CIT (243 ITR 83), the Ld. AR submitted that where the Ld. AO has adopted one of the possible views, the Ld. PCIT cannot invoke jurisdiction under section 263 of the Act merely because he holds another view. Accordingly, it was submitted that invocation of powers under section 263 of the Act by the Ld. PCIT is not in accordance with law.

11. Per contra, the Ld. DR strongly supported the order passed by the Ld. PCIT under section 263 of the Act. The Ld. DR submitted that the assessment order was passed without conducting proper enquiry and verification regarding genuineness and validity of cancellation of sale deed. The Ld. DR submitted that the registered sale deed dated 17.02.2011 itself clearly mentioned receipt of consideration amounting to Rs.1,09,39,000/- and handing over of possession on the date of registration. However, despite such specific recital in the registered document, the Ld. AO accepted the claim of the assessee without making any independent verification from revenue authorities or bank accounts. The Ld. DR further submitted that even the statement recorded under section 131 of the Act from the purchaser clearly revealed that the cancellation deed was executed only to overcome capital gains liability and therefore the Ld. AO ought to have examined the issue in greater detail before accepting the explanation of the assessee. The Ld. DR further relied upon Explanation 2(a) to section 263(1) of the Act and submitted that an order passed without making enquiries or verification which should have been made is deemed to be erroneous insofar as prejudicial to the interests of Revenue. Accordingly, it was submitted that the Ld. PCIT had rightly exercised revisional jurisdiction under section 263 of the Act.

12. We have heard the rival submissions and perused the material available on record including the case laws relied upon. We have also gone through the order passed by the Ld. PCIT under section 263 of the Act and the assessment order passed by the Ld. AO under section 143(3) of the Act. On perusal of the assessment records as discussed in the order passed by the Ld. PCIT, we find that the assessee had executed registered sale deed No.1472/2011 dated 17.02.2011 in respect of immovable property for consideration of Rs.1,09,39,000/-. The registered document itself specifically records that the sale consideration was received and possession of the property was handed over to the purchaser on the date of execution of sale deed itself. We further find that during the assessment proceedings, the assessee furnished cancellation deed dated 17.12.2018 and on the basis of the same, the Ld. AO accepted the claim of the assessee that no capital gains were chargeable to tax. In this regard, we have gone through para no. 6 of the order of the Ld. AO which is to the following effect:

“6. The following points have been keenly verified and considered for deciding the capital gains issue:

i. The said land is in dispute and the case is pending before First Class Magistrate, Kurnool. The assessee furnished the copy of p3etition filed by one Mr. Lokeswar Reddy before first class magistrate, Kurnool. Under this circumstance on the advice of lawyer the sale deed No.1472/2011 was executed by the assessee in favor of Sri Shaik Nisar Ahmed to mitigate litigation.

ii. Though it is mentioned in the sale deed mentioned above that the entire sale consideration received by the seller, as confirmed by Sri Shaik Nisar Ahmed in the statement recorded u/s 131 that no cash transaction was took place as the purpose of executing sale deed is to mitigate the litigations existing on the said land.

iii. In the cancellation deed no. 15359 /2018 dated 17.12.2018, it is clearly mentioned that the cancellation deed is executed with the mutual consent of both the parties as sale consideration was not received. In the statement Sri Shaik Nisar Ahmed confirmed that the consent was given by him for cancellation of sale deed.

iv. As verified from the Encumbrance certificate downloaded from the IGRS site, on the said land no further sale activities have been taken place after 2011 in the year in which the sale deed was executed.

In view of the above and considering the circumstances of the case, as the said land is still in the possession of the assessee as the sale deed doc no 1472/2011 dated 17.02.2011 is cancelled, no capital gain attracts.”

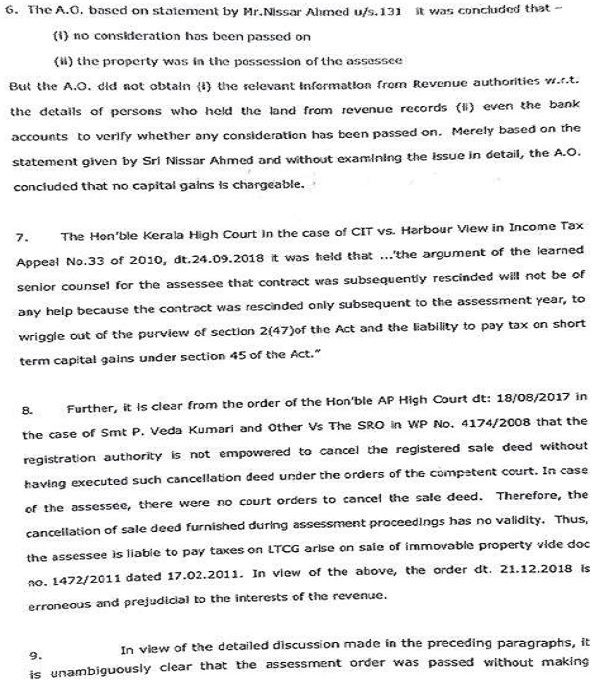

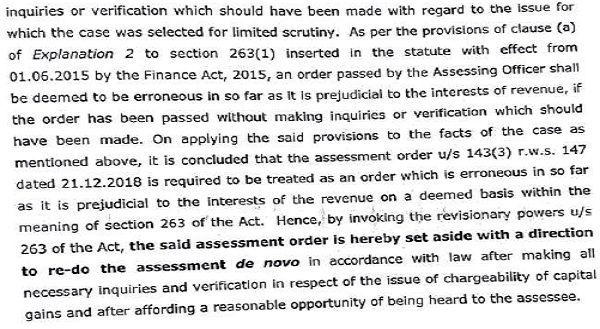

13. On a perusal of the above, we do not find any proper enquiry or verification conducted by the Ld. AO regarding genuineness and legal validity of the cancellation deed and actual taxability arising from the registered transaction. We have also gone through the para nos. 5 to 9 of the order of the Ld. PCIT, which is to the following effect:

–

–

14. On perusal of the above, we find that the Ld. PCIT has categorically observed that the Ld. AO failed to verify revenue records, failed to verify bank accounts and failed to conduct independent enquiry regarding actual payment of consideration and possession of the property. We have also gone through para no.7 of the statement of Mr. S. Nisar Ahmed, recorded under section 131 of the Act, which is to the following effect:

“7. The sale was executed in the year 2011, whereas, the cancellation deed is executed in the ve2 2018. There is a time gap of nearly eight year. Please explain why so much of long time was taken for cancellation.

Ans: Actually, the problem was started in the year 2007 when Sri Abdul Mannan sold the saic property to one Mr. Lokeshwar Reddy who has not paid sale consideration. Hence, Sri Abdul mannan approached first class magistrate, Kurnool. The judgment was pronounced ex-parte in favour of Sri Abdul manna. Later, Mr. Loakeswar Reddy filed case before the first-class magistrate, Kurnool claiming that the judgment was given without his appearance and the land belongs to him. Since then, the litigation is still alive. The reason for cancellation of sale deed now is the assessment proceedings before income tax department is pending for completion by 31.12.2018. To overcome capital gains issue in the case of Sri Abdul mannan and to avoid -appeal before first appellate authority the sale deed is cancelled. Thus, I can overcome facing appeal proceedings before respective authority from income tax department as I have already facing legal proceedings before the first-class magistrate in respect of the land”.

15. On a perusal of the above, we find that the purchaser has admitted that the cancellation deed was executed to overcome capital gains liability and avoid appellate proceedings. The Ld. AR has elaborately explained the background relating to earlier sale deed executed in favour of Shri M.V. Lokeshwar Reddy and the subsequent litigation pending before the Court and further submitted that no consideration was actually received by the assessee from Shri S. Nisar Ahmed. The Ld. AR has also relied upon the decision of the Hon’ble Patna High Court in the case of Smt. Raj Rani Devi Ramna vs. CIT (Supra) for the proposition that in absence of receipt of consideration, no transfer can be said to have taken place giving rise to capital gains. However, we find that the Ld. PCIT in the impugned proceedings under section 263 of the Act has not given any conclusive finding regarding ultimate taxability of the transaction in the hands of the assessee. The Ld. PCIT has only observed that the assessment order was passed without proper enquiry and verification in respect of the issue relating to chargeability of capital gains. Therefore, at this stage, the submissions advanced by the assessee regarding ultimate taxability of the transaction and reliance placed on the decision of the Hon’ble Patna High Court are not directly relevant for adjudicating validity of assumption of jurisdiction under section 263 of the Act. We further find that despite existence of registered sale deed evidencing transfer of property along with recital regarding receipt of consideration and handing over of possession, the Ld. AO accepted the explanation of the assessee without conducting proper enquiry and verification. The Ld. A.O has summarily accepted the cancellation deed, inspite of the specific mention therein that the cancellation deed was executed to overcome capital gains liability and avoid appellate proceedings. Therefore, in our considered opinion, the assessment order was passed without making enquiries and verifications which ought to have been made in the facts and circumstances of the case. We have also gone through the provisions of Explanation 2(a) to section 263(1) of the Act, which is to the following effect:

“263 (1)……

Explanation 1

Explanation 2.—For the purposes of this section, it is hereby declared that an order passed by the Assessing Officer shall be deemed to be erroneous in so far as it is prejudicial to the interests of the revenue, if, in the opinion of the Principal [Chief Commissioner or Chief Commissioner or Principal] Commissioner or Commissioner,—

(a) the order is passed without making inquiries or verification which should have been made”.

16. On perusal of the above, it is evident that Explanation 2(a) to section 263(1) of the Act specifically provides that an order passed without making enquiries or verification which should have been made shall be deemed to be erroneous insofar as it is prejudicial to the interests of Revenue. The reliance of the assessee on the decision of the Hon’ble Supreme Court in the case of Malabar Industrial Co. Ltd. Vs. CIT (Supra) is misplaced, since the present issue is covered under Explanation 2(a) to section 263 of the Act. Therefore, in the facts of the present case, we do not find any infirmity in the action of the Ld. PCIT in invoking revisional jurisdiction under section 263 of the Act. We further find that the Ld. PCIT has only set aside the assessment order with direction to the Ld. AO to conduct proper enquiry and frame assessment afresh after affording reasonable opportunity of being heard to the assessee. Therefore, no prejudice is caused to the assessee by the impugned order passed under section 263 of the Act. Accordingly, considering the totality of facts and circumstances of the case, we uphold the order passed by the Ld. PCIT under section 263 of the Act and dismiss the appeal filed by the assessee.

17. In the result, appeal of the assessee is dismissed.

Order pronounced in the Open Court on 15th May, 2026.

Author Bio