Summary: Recent amendments to GSTR-1 modify several reporting tables, aiming to refine the declaration of outward supplies. Table 5 now requires inter-State supplies to unregistered persons with an invoice value exceeding Rs 1.5 lakh to be reported, with the threshold having been adjusted from Rs 2.5 lakh to Rs 1 lakh effective August 1, 2024. This table is further bifurcated for outward supplies not through e-commerce operators and those attracting TCS via e-commerce. Reporting for zero-rated supplies and deemed exports in Table 6 includes separate sections for exports, SEZ supplies, and deemed exports. Table 7, covering taxable supplies to unregistered persons, now distinguishes between intra-State and inter-State supplies, with specific provisions for e-commerce operator transactions and a Rs 1 lakh invoice value limit for inter-State supplies. Table 8 details nil-rated, exempted, and non-GST outward supplies across different recipient types. Amendments to previously furnished details are handled in Table 9 for registered persons and Table 10 for unregistered persons, with specific rules for correcting invoice details, debit/credit notes, and place of supply. Table 11 addresses advances received and adjusted, particularly for services, with state and rate-wise reporting. A significant change is in Table 12 for HSN-wise summaries, which now mandates selecting HSN codes from a dropdown, splits reporting into B2B and B2C tabs, introduces auto-validation with other GSTR-1 tables, and specifies 4-digit or 6-digit HSN codes based on aggregate annual turnover. Table 13 makes detailing documents issued during the tax period obligatory, requiring series-wise reporting for various document types including invoices, debit/credit notes, and delivery challans.

Recent Amendments in GSTR-1

let’s view summary of tables to be reported in GSTR-1.

1.Taxable No. 4 outward supplies made to registered persons (including UIN-holders) other than supplies covered by Table 6

2. Taxable No. 5 outward inter-State supplies to un-registered persons where the invoice value is more than Rs 1.5 lakh

amount changed from 2.5 lakh to 1 lakh

Substituted (w.e.f. 01.08.2024) vide Notification No. 12/2024 – CT dated 10.07.2024.

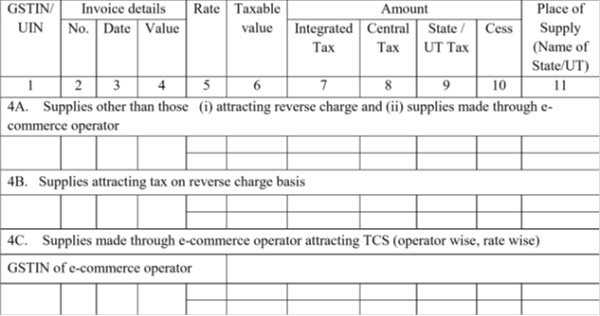

5A: Outward supplies (other than supplies made through e-commerce operator, rate wise)

5B. Supplies made through e-commerce operator attracting TCS (operator wise, rate wise)

3. Table No. 6 Zero rated supplies and Deemed Exports

6A. Exports

6B. Supplies made to SEZ unit or SEZ Developer.

6C. Deemed exports.

4. Table No. 7 Taxable supplies (Net of debit notes and credit notes) to unregistered persons other than the supplies covered in Table 5

7A. Intra-State supplies

7A (1). Consolidated rate wise outward supplies [including supplies made through e-commerce operator attracting TCS]

7A (2). Out of supplies mentioned at 7A(1), value of supplies made through e-Commerce Operators attracting TCS(operator wise, rate wise) mention E-Commerce GSTIN

7B. Inter-State Supplies where invoice value is uptoRs 1 Lakh [Rate wise]

7B (1). Place of Supply (Name of State)

7B (2). Out of the supplies mentioned in 7B (1), the supplies made through e-Commerce Operators (operator wise, rate wise)

5. Table No.8 : Nil rated, exempted and non GST outward supplies

8A. Inter-State supplies to registered persons

8B. Intra- State supplies to registered persons.

8C. Inter-State supplies to unregistered persons .

8D. Intra-State supplies to unregistered persons.

6. Table No. 9 Amendments to taxable outward supply details furnished in returns for earlier tax periods in Table 4, 5 and 6 [including debit notes, credit notes, refund vouchers issued during current period and amendments thereof]

9A. If the invoice/Shipping bill details furnished earlier were incorrect

9B. Debit Notes/Credit Notes/Refund voucher [original]

9C. Debit Notes/Credit Notes/Refund voucher

[amendments thereof]

7. Table 10: Amendments to taxable outward supplies to unregistered persons furnished in returns for earlier tax periods in Table 7

Amendments to supply reported under Table 7.

Amendment under tax rate, amount, POS allowed.

Note: Not allowed to add new place of supply. You can only amend and change earlier reported POS with same amount of supply.

Example: Earlier reported supplies under B2Cs as follows:

Original- POS > 24-GUJARAT – Taxable Value> 10,00,000/-

You can change POS with same amount of supply as:-

Amended–

POS > 29-KARNATAKA – Taxable Value> 10,00,000/-

8. Table No. 11 Consolidated Statement of Advances Received/Advance adjusted in the current tax period/ Amendments of information furnished in earlier tax period

- Declare here the tax liability arising on account of receipt of consideration for which invoices have not been issued in the same tax period.

- Reporting State wise and Rate Wise only.

- Applicable only for the services.

- Not applicable to composition dealers.

> What if tax is paid on advances and after that the Rate of Tax is changed while issuing tax invoice.?

√ If tax rate is changed after advance is received and tax is already paid on advance then balance amount of tax payable shall be adjusted against excess paid or

√ Refund can be claimed after filing returns.

> What if further supply is cancelled after payment of tax on advance?

√ Refund voucher shall be issued to the receipent.

√ Refund shall be claimed on account of excess payment of tax.

9. Table 11B. Advance amount received in earlier tax period and adjusted against the supplies being shown in this tax period in Table Nos. 4, 5, 6 and 7

Report adjustment of advances reported earlier tax period and invoice is issued in current tax period.

State wise and Rate wise reporting.

10. Table 12 HSN-wise summary of outward supplies

√ Reporting HSN and Tax Rate wise summery up to the tax period April-2025.

11. Table No. 13. Documents issued during the tax period

√ Detailing documents issued, is now obligatory.

√ Reporting series of various documents issued during the period.

√ Number of documents cancelled.

√ List of documents to be reported under this table:-

- Invoices for outward supply

√ All outward supply invoices including bill of supply for tax free or exempt supply.

√ Series wise reporting for different series.

2. Invoices for inward supply from unregistered person

√ Invoice to be generated by recipient for URD purchase.

3. Revised Invoice

4. Debit Note

5. Credit Note

6. Receipt voucher

7. Payment Voucher

8. Refund voucher

9. Delivery Challan for job work

10. Delivery Challan for supply on approval

11. Delivery Challan in case of liquid gas

12. Delivery Challan in cases other than by way of supply (excluding at S no. 9 to 11)

Changes in HSN Summery

√ From april-2025 amended as

Implemented as part of Notification No. 78/2020 – Central Tax dated 15.10.2020. Enforced through Rule 59(6) of the CGST Rules.

Phase-III – Implementation of Table 12 in GSTR-1/1A (HSN Code Reporting)

Changes:

1.Mandatory Dropdown Selection for HSN Codes:

Taxpayers must now select HSN codes from a predefined dropdown list. Manual entry is no longer allowed.

2. Table 12 Split:

Table 12 is bifurcated into two tabs: “B2B Supplies” and “B2C Supplies” for separate HSN summary reporting.

3. Auto-Validation Feature:

A new system check ensures consistency of HSN totals in Table 12 with other GSTR-1 tables.

4. HSN Code Digits:

AATO up to ₹5 crore must report 4-digit HSN codes,

AATO above ₹5 crore must report 6-digit HSN codes.

(As per Notification No. 78/2020 – Central Tax dated 15.10.2020)

Before 01/04/2021

| AATO Previous Year | Digits of HSN |

| Up to rupees 1.5 Cr | Nil |

| 1.5 to 5 Cr | 2 |

| More than 5Cr | 4 |

After 01/04/2021

| AATO Previous Year | Digits of HSN |

| Up to 5 Cr | 2 |

| More Than 5 Cr | 4 |

√ Exemption to report Number of Digit of HSN numbers in case supply to B2CS whose AATO is up to 5 Cr.

√ But Description is mandatory for B2CS Supply (as per form GSTR-1 tables)

In Table-12 validation with regards to value of the supplies have also been introduced.

i. These validations will validate the value of B2B supplies shown in different Tables viz: 4A, 4B, 6B, 6C, 8 (recipient registered), 9A, 9B (registered), 9C (registered), 15 (recipient registered), 15A (recipient registered) with the value of B2B supplies shown in table-12.

ii. Similarly, validations will validate the value of B2C supplies shown in different tables viz: 5A, 6A, 7A, 7B, 8 (recipient unregistered), 9A (export), 9A (B2CL), 9B (unregistered), 9C (unregistered), 10, 15 (recipient unregistered), 15A (recipient unregistered) with the value of B2C supplies shown in Table-12.

iii. In case of amendments, only the differential value will be taken for the purpose of validation.

iv. However, initially these validations have been kept in warning mode only, that means warning or alert message shall be shown in case of mismatch in values, whereas taxpayers will be able to file GSTR-1 in such cases. Further, in case B2B supplies are reported in other tables of GSTR-1, in that case B2B tab of Table-12 cannot be left empty.

Effective From:

Phase III – 01/05/2025

Phase II – 01/11/2022

Phase I – 01/04/2022

Stay in touch..

Thanking You …!

Author Bio