FROM 01-01-2021 , GST RETURN FILING SYSTEM will see complete change. (We call it version 3.0) . Intention to Overhaul GST return filing system, But is it the correct solution in reality??? We will find out that in future . FYI, NOTIFICATION 82 TO 85 to notify/amend rule 60/61/62/61A. Also Circular No. 143/13/2020 is issued on 11-11-2020 . I have tried to make it very easy in understanding. also covered everything about GSTR 1, 3B, 2B, IFF, QRMP, 36(4) in one article to a complete 360 degree analysis on New return filling system. Let’s dive in.

Intention to Overhaul GST return filing system, But is it correct solution in reality???

(NOTIFICATION 82 TO 85 to notify/amend rule 60/61/62/61A. Also Circular No. 143/13/2020 is issued)

This article is presented in manner it is dedicated to every professional who are involved in compliance work.

LET US BEGIN FROM BEGINNING – KAL, AAJ, AUR KAL

Author’s Comments

It’s all same. We are almost back to 2017 July scenario.Except Accept /reject /edit. Problem appears more here which is “You can take ITC ONLY what appears in GSTR 2B till 14th date”.

Very Tight restrictions than even earlier original system. (What about natural right to take ITC? What about promises of Seamless ITC? What about section 16 which says if you have invoices, claim ITC??? )

Please note that for your reference – From Oct-2020, with rule 36(4) restriction I.E ITC as per 2B or 10% more as per rule 36(4). (Claiming ITC more than 110% is subject to reversal or Interest). I have explained this in this article. https://taxguru.in/goods-and-service-tax/itc-interest-section-364-dangerous-provision-gst-professional-aware.html

NOW LET US UNDERSTAND IN DETAIL

NEW GST RETURN FILLING SYSTEM FROM 01-01-2021

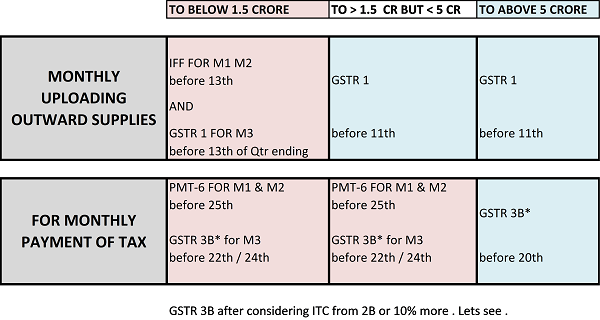

CATEGORY 1 – RETURN FILLING SYSTEM FOR TURNOVER BELOW 5 CRORE

Part A – For uploading Sales invoices –

| If turnover below 1.5 crore | If turnover above 1.5 crore but less than 5 crore |

| Ø M1 ( 1st month of Qtr) – may upload in IFF ( Only B2B) before 13th

Ø M2 ( 2nd month of Qtr) – may upload in IFF ( Only B2B) before 13th Ø M3 ( 3RD month of Qtr ) – FILE GSTR-1 before 13th ( as usual) B2B, B2C, Other B2B invoices, B2CL, Other Dr. & Cr. Notes |

FILE MONTHLY GSTR 1 before 11th

( as usual) B2B, B2C, Other B2B invoices, B2CL, Other Dr. & Cr. Notes |

What is Invoice Furnishing Utility (IFF)?

Upload B2B invoices, using INVOICE FURNISHING FACILITY.

Of course, No need to report invoices again in GSTR-1 if already reported in IFF. The invoices in IFF to be furnished from 1st day of next month till 13th day of next month.(1-13th) ( So it’s almost like GSTR 1). IFF is An Improvised Solution to upload monthly b2b invoice in case of Quarterly dealers, so that Counter party can claim ITC Monthly.

READ NOTIFICATION EXTRACT –

Quarterly dealer may furnish the details of outward supply for the first and second months of a quarter, up to a cumulative value of fifty lakh rupees in each of the months,- using invoice furnishing facility (hereafter in this notification referred to as the ―IFF’) electronically on the common portal, duly authenticated in the manner prescribed under rule 26, from the 1st day of the month succeeding such month till the 13th day of the said month.

For example-

For JANUARY- Upload invoices in IFF (B2B) till 13th February

For FEBRUARY – Upload invoices in IFF (B2B) Till 13th March

For MARCH – Upload invoices (B2B + B2CS + B2CL) in GSTR1 till 13th April.

PART B – For payment of Tax –

QRMP scheme from 01-01-2020 (We call it alternative method of 3B for 5 cr below. Mind well you can still file GSTR 3B. This seems optional)

QRMP ( full form) – Quarterly Return monthly payment (for so called Ease )

1. How it works? For any Quarter

M1 ( first month) – pay challan – GST PMT-06 by 25th day of succeeding month

M2 (second month) – pay challan – GST PMT-06 by 25th day of succeeding month

M3 ( third month) – File GSTR 3B ( as usual) – 22nd or 24th day

2. How to ascertain? – 2 methods to ascertain tax liability in QRMP FOR M1 & M2 month.

Method 1 – Self assessment

it is Like self assessed 3B, but don’t file 3B. Just Pay challan (in PMT 6) after considering Outward liability and inward ITC from 2B..(Yes you have to calculate manually your self assessment tax monthly)

That’s means, जैसा चल रहा था ऐसा ही चलने दो.

Method 2 – Fixed sum method

Pre filled challan in PMT 6. It’s for lazy people, pay amount as equal to 35% of total Amt paid in last Quarter…( Read again… “35% of Last quarter Net tax”) in M1 & M2.

3. How PMT-6 will work ?

The amount deposited through PMT-06 for 1st and 2nd month will remain in the cash ledger and will be adjusted on filing GSTR 3B at the end of Quarter.

Any claim of refund of such amount lying in balance in the electronic cash ledger, if any, out of the amount so deposited shall be permitted only after the return in FORM GSTR-3B for the said quarter has been filed.

Lets see how actually this system will work after 01-01-2021. People might continue with GSTR 3B.

Author’s Comments

You will file GSTR 1 if TO above 1.5 cr / IFF monthly ( i.e b2b invoice upload facility for 1.5 cr below TO ) . And a simplified (read messed up) challan system replacing GSTR 3B. So both these works are monthly compliance only. There is nothing that Compliance reduced or anything eased up. These CHALLAN ( instead of 3B) and UPLOAIDNG OUTWARD supplies are compliance for M1 AND M2. For 3rd Month, You have to file GSTR 3B as usual and also upload GSTR 1 AS USUAL. (Of course those invoice which are already upload in IFF, not require uploading). It’s like from outer pack, you are under quarterly, but from inside you have to do everything monthly. (Not commenting on Interest and late fees and how it will work).

GSTR 3B was much stable and proper. It was easy and fast system of return filling..Better they should just stop simplification…We don’t more simplified GST.. In the name of simplification, everything is messed up for MSME.

So for 5 cr below, Check the scenario after 1-1-2021.

On one side – GSTR 3B Quarterly. But with monthly payment of Approximate tax ( Almost like 3B). For first 2 months, you may check 2B for ITC determination. In 3rd month, ITC will be restricted to the extent of available in GSTR 2B or as per 36(4). And a GSTR 3B after quarter end.

On other side – Monthly GSTR 1 OR IFF To upload monthly invoice. Also quarterly GSTR 1.

It will take some time to digest even. Situation is funnier than ever.

CATEGORY 2 – RETURN FILLING SYSTEM FOR TURNOVER ABOVE 5 CRORE

Part A – For uploading Sales invoices –

Every month GSTR 1 before 11th ( as usual)

PART B – For payment of Tax –

GSTR 3B – AUTOMATIC (Almost) – FILE BEFORE 20TH / 22 TH / 24TH

HOW almost AUTO GSTR 3B will be for 5 crore above taxpayers ?

| FOR OUTWARD LIABILITY | It will be Auto populated from GSTR 1 (You may / may not be allowed to edit) |

| For RCM | This detail need to filled up after asking taxpayer. |

| For Inward ITC details (including Import ITC)

Read below |

It will be Auto-populated from GSTR 2B from 12th day 00.00 hrs

As per rule 36(4), Taxpayer can claim 10% more ITC than what appears in GSTR 2B |

HOW TO ASCERTAIN DETAILS OF INWARD SUPPLIES

INWARD SUPPLIES From monthly filer

Since Your monthly supplier will file GSTR 1 ideally before 11th, ITC details will be auto-populated.

INWARD SUPPLIES from Quarterly filer –

M1 (1st month of Qtr) – may upload in IFF (Only B2B) before 13th

M2 (2nd month of Qtr) – may upload in IFF (Only B2B) before 13th

M3 (3RD month of Qtr) – FILE GSTR-1 before 13th (as usual)

So ITC will be auto-populated monthly from the purchases only if he uploads regularly in IFF before 13th.

| Please note that as per rule 36(4), ITC amount will be restricted only to the extent of 10%* of the eligible ITC value already reflected in the GSTR-2A for that period.

BRIEF HISTORY ON RULE 36(4) – Before 9 October 2019, all taxpayers claimed ITC on a self-declaration basis in Table 4(a) of GSTR-3B. This means that they declared the summary figure of eligible tax credits under IGST, CGST, and SGST. There was no compulsion to reconcile the ITC figure with the GSTR-2A until now, although it was always advised. Even if the GSTR-2A reflected an ITC amount lower than the books of accounts, taxpayers could still make their ITC claim in full in the GSTR-3B, and the unreflected amount was treated as provisional credit. After the implementation of this rule, the provisional ITC amount will be restricted only to the extent of 10% (With effect from 1 Jan 2020; Was earlier restricted to 20% for the period from 9 Oct 2019 to 31 Dec 2019) of the eligible ITC value already reflected in the GSTR-2A for that period. Apart from the 10% of eligible ITC which a taxpayer can claim as provisional credit, the balance tax liability will need to be paid in cash. This new rule could affect the working capital of a taxpayer, as he will be required to make GST payments in cash, despite having paid his supplier for the tax invoice raised to him and having eligible ITC in his books. Said rule was made optional for Covid period in 2020. the said Rule shall apply cumulatively for the period February, March, April, May, June, July and August, 2020 and the return in FORM GSTR-3B for the tax period September, 2020 shall be furnished with the cumulative adjustment of input tax credit for the said months. So from October-2020, Finally Rule 36(4) is applicable in full force & restriction. |

Authors’ comments

Now, Government wants to restrict ITC anyhow. “Claim only to the extent available in 2B. That’s it. Earlier GSTR 1/1A/2/2A/3 was conceptualised on this principle only.

In present return filling system, ITC is subject to GSTR 2B. But Problem for taxpayer is that “ITC from Quarterly dealers do not appear in GSTR 2B in M1 and M2. So taxpayer may not be able to claim ITC as equal to books. This problem is huge if Taxpayer has Purchases from Quarterly dealers in particular month. “On other hand, claiming ITC more than 110% is subject to reversal or Interest. I have explained this in this article. https://taxguru.in/goods-and-service-tax/itc-interest-section-364-dangerous-provision-gst-professional-aware.html

To remove this problem, Government has come up with highly ambitious project. To do these, NOTIFICATION 82 TO 85 issued to notify/amend rule 60/61/62/61A. Also Circular No. 143/13/2020- GST is issued. Applicable from 01-01-2021. And for this, IFF is introduced and this might be a improvised solution that quarterly dealer may able to upload his SALES invoices before 13th (of course B2B only) every month, And recipients will be able to claim ITC on monthly basis. Cool. Let see how this added workload on part of professionals will be dealt by them.

GSTR 3B will be almost auto drafted. You may/may not change ITC amount by claiming 10% more. Or let’s see how things turn out after January -2021 on portal. Cant say right now.

Strategy to make it successful

1. Instruct every Client to send GSTR 1 in 1ST WEEK OF MONTH

2. Now even Quarterly dealers will be able to upload their B2B invoices in IFF monthly. So every professional should educate Clients. And Clients should inform their all Suppliers to upload invoice on time

3. For Getting FULL ITC, Instruct every client to employ Full time Employee who will 24*7 call each suppliers ( including each quarterly supplier) from whom Purchases are made and get screenshot from them ensuring that counter party has uploaded invoice in GSTR 1/ IFF before due date. Everyone must be on-time.

4. Send your clients GSTR 2B on 14th (atleast to all clients having TO 5 crore above). So that he can analyse that which counter party has uploaded and which has not yet uploaded.

IN SUMMARY, THIS MIGHT BE THE FINAL PICTURE FOR RETURN FILLING AFTER 1-1-2021

As a professional, how your Monthly timeline will be

This will be Monthly timeline For Compliance work of Jan, Feb, April, May, July, Aug, Oct, Nov

- 1-11th = Upload GSTR 1 Of Monthly Clients (1.5cr Above)

- 12-13th = Upload IFF of Quarterly Clients ( 1.5 Cr Below)

- 14th = Send 2B To All 5 Crore Above Clients

- 15th – 20th = File 3B Of Those Having 5 crore above

- 25TH = File challan PMT -6 for Those Having 5 crore above (instead 3B) in M1 +M2. After self assessment.

This will be Monthly timeline For Compliance work of over above work For Mar, June, Sept, Dec

- 13th = Upload GSTR 1 Of Monthly Clients (1.5 crore below ) only in M3

- 21st – 22th/24th = File 3B for Those Having 5 crore below only in M3

LAST SHOCK – NOW GST DATA IS VISIBLE IN INCOME TAX 26AS… SO KEEP RECONCILIATION OF

3B with 2A, 3B with 2B, 2A with 2B, 3B with 1, 3B + 1 with 9, 9 /9C with Books,

All above with 26AS

All above with GST/IT Audits

Last comment- Let’s us accept firstly that, just because of some 2% people claiming fake ITC or claiming Excess ITC, Government is imposing strictest rule 36(4). Their idea is seem clearer that they want taxpayer to claim ITC only what appears in 2B. OK. For making its successful, Its better they should have just removed Quarterly category if they really want to make 36(4) and Auto drafted 3B successful (with help of 2B ). Instead of doing above KHICHDI solution. Everything is difficult to make clients understand. Difficult to make staff understand. For professionals, In totally uncertain regulatory environment, it’s difficult to operate. They must give time to stabilize a system of 1.25 Cr tax payers. Instead of that since Jul 17, this is NTH time they have changed the rules of the game. And adding restrictions on ITC. Every time they try to remove an organ instead of treating the body.. What you think on this? Do give us feedback. Any error/mistake, please correct me –-CA HARSHIL SHETH.

is gst invoice in fincal year 19-20 is not submitted in current year.please suggested

The govt always misguide that they are actually favoring small dealers by making their return quarterly but reality is far from that…QRMP is nothing but a tool to make taxpayer fool that their return is quarterly and this will also result in headache for professionals to tell clients reality of QRMP

The earlier system ie before 31/12/2020 was easier and it became comfortable for professional gradually. But the new system again creates more confusion and complex and gives work load for professionals. This system should be restored to earlier one.

what the hell gst deptt is doing…the are much loopholes in system..deptt can nail the tax evaders by other terms..loyal taxpayers are suffering ..to stop tax evasion deptt.must not implement confusing rules regulations.it must be simple as it should be..

SIR THANKS FOR VERY VERY EASY WAY OF EXPLAINING ONE OF THE COMPLEX ISSUES AND COVER ALL THE DOUBTS. ONE MORE THING IF YOU CAN EXPLAIN – AS PER NEW GUIDE LINES ANY CORRECTION IN GSTR 1 (M1 AND M2) IS ALLOWED OR NOT AND IF IT IS ALLOWED HOW IT WORKS AND IF NOT POSSIBLE IT MEANS ANY TYPO OR HUMAN ERROR IS CRIME AND EVERY CRIME HAS TO BE PUNISH WITH HARSH PENLATY AND LOSS OF ITC WITHOUT ANY REMEDIES SIR WHAT TO DO

Who is implementing the new system . He should understand the pain , effort and work load of professionals. If he can’t understand , resign and go away. GSt dept should look at Gulf Countries/. How did they implemented VAT. All items having same (5%) percentage of tax. You (gst dept) claims as intelligent and blames Arab as stupid. But actually Arabs implemented VAT succesfully and GST becoming complicated day by day and the amendments going on since last 3.5 years. What non sense the GST dept doing. GST really becomes a very complex task. Quarterly filing system must be stopped and make monthly filing for all irrespective of turnover. ITC must be auto populated and must be given time to claim ITC upto next financial year sept .

I also expect GST team to add auto sms facility to clients whenever GSTR1 filed by supplier. So that clients will know their supply invoice is included instead of verifying in the website.

GST System should be universal for all the catagories either below or above any limits like 1.5 crore etc. GSTR1 AND GSTR3B Should be filed in monthly mode only for all the registered dealers. It will ease to get reflections of ITC claimed in 2A. New pre filled GSTR forms 2A or other can ease the complications arising due to multiple durations of filing returns.

Super Dhulai!

The problems of Gst system Only understand the person who is doing ground level Gst working neither Government nor Management nor common public.

Using a word simplifucation, they r making complexities. Nobody in the ministries and bureaucracy knows the dictionary meaning of this words. May be they never have used it. Its high time that organisational bodies like CIi makes them to understand those words and take them to courts for better understanding

Govt should go away from current gst structure. Instead of they should levy maximum tax 10 to 12 % without allowing cenvar credit. In some cases cost will be higher but solve all other procedural problems

It is better if GST Dept. keep only Monthly GSTR1 & Monthly GSTR3B for all Categories i.e. below 1.5, 5 & above 5 Carores & keep Due Date 15th & 25th of the succeeding Month for GSTR1 & 3B respectively.

Sir, was there any facility to file all parties below 1.5 crores, as usual. I mean old monthly returns like gstr 1 and gstr3b. Of course we want to take input tax only as visible on gstr 2or gstr2a