Introduction: The Goods and Services Tax (GST) landscape has witnessed two significant and potentially hazardous amendments in the form of Rule 88C and Rule 88D. These alterations specifically target discrepancies in GSTR-1 vs 3B and GSTR-2B ITC vs 3B ITC, respectively. In this article, we delve into the intricacies of these changes, understanding their implications and guiding taxpayers on the necessary actions to ensure compliance.

Rule 88C- for difference in GSTR-1 vs GSTR -3B (Form DRC-01B)

1. Taxpayer shall be intimated of such difference in Part A of FORM GST DRC-01B

2. Taxpayer should do following action in 7 days from the date of issue of GST DRC-01B

Option-a) pay the amount of the differential tax, as specified in Part A of FORM GST DRC-01B, fully or partially, along with interest under section 50, through FORM GST DRC-03 and furnish the details thereof in Part B of FORM GST DRC-01B

or

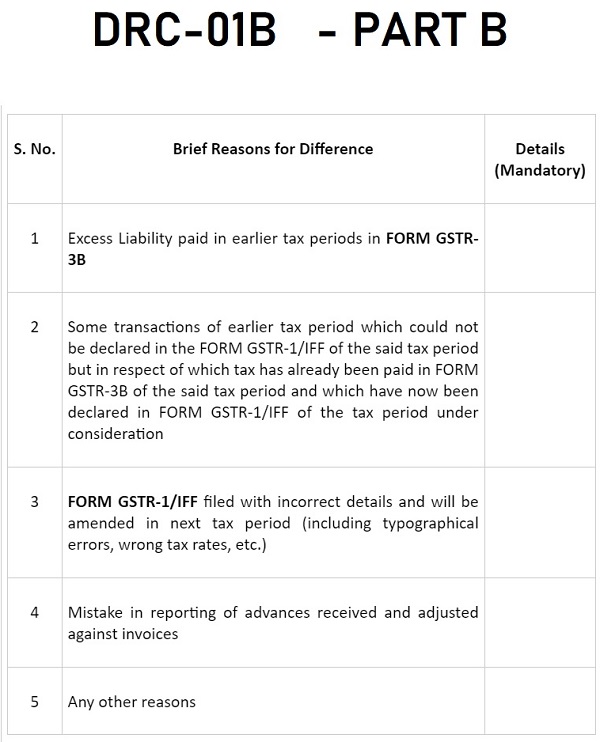

Option -b) furnish a reply, incorporating reasons in respect of that part of the differential tax liability that has remained unpaid, if any, in Part B of FORM GST DRC-01B

3. If he fails to pay and No reply furnished or when his reply is not satisfactory then recovery u/s 79 and he will not be able to file GSTR -1 of next period as per clause (d) of Rule 59(6).

Rule 88D- for difference in GSTR-2B ITC vs 3B ITC ( DRC-01C )

1. Taxpayer shall be intimated of such difference in Part A of FORM GST DRC-01C

2. Taxpayer should do following action in 7 days from the date of issue of GST DRC-01C

Option-a) pay the amount of the differential tax, as specified in Part A of FORM GST DRC-01C, fully or partially, along with interest under section 50, through FORM GST DRC-03 and furnish the details thereof in Part B of FORM GST DRC-01C

or

Option -b) furnish a reply, incorporating reasons in respect of the amount of excess input tax credit that has remained unpaid, if any, in Part B of FORM GST DRC-01C

3. If he fails to pay and No reply furnished or when his reply is not satisfactory then recovery u/s 73/74 and he will not be able to file GSTR -1 of next period as per clause (e) of Rule 59(6)

Conclusion: These recent changes in GST rules, specifically Rule 88C and Rule 88D, necessitate a heightened awareness among taxpayers. Non-compliance can lead to severe consequences, including recovery proceedings and restrictions on filing future GSTR-1. It is imperative for businesses to stay informed, act promptly, and ensure adherence to these amended regulations to avoid financial penalties and maintain a smooth GST filing process.