Department Audit under GST as per Section 65 : Common issues arised during Audit

1. Introductory paragraph on common issues arised during Audit :-

This article provides a detailed exploration of Section 65, including its text, key provisions, and practical implications for taxpayers.

Recently, there have been a spate of audit intimations being issued for conducting audit u/s 65 by GST Department covering period of upto past 5 years. In the course of audit done by department under section 65 of the CGST Act, certain issues/objections could be raised. The assesses have to carefully examine the matter, give their explanation.

Under Goods & Services Tax (GST), audit is defined under Section 2(13). Today, we will analyze one of the actions under GST Law; Section 65-where audits are carried out by tax authorities as mentioned in Section 61.

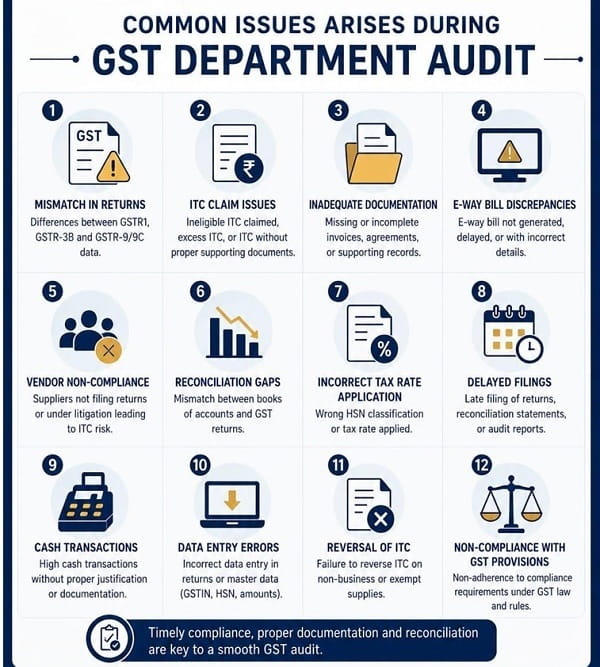

2. Common issues and its implications arised during Audit by Department :-

I. Differences in GST Returns i.e Turnover in 3B vs GSTR 1, unreconciled turnover in GSTR 9C, GSTR 3B vs sales register, Differences between GSTR-3B, GSTR-1, and Audited Financial Statements (P&L).

Common causes include “Income from Other Sources” being mis-classified or exempt income not being reported in returns. The department also cross-references TDS/TCS data from the Income Tax portal with GST returns. In all cases, reasons for difference to be provided along with reconciliation statement to establish correctness of taxes has been duly discharged.

Differences in ITC i.e Excess ITC availed in GSTR-3B as comparison with GSTR-2B:

The ITC cannot be denied merely due to the non-reflection of invoices in GSTR-2A/2B when all the conditions specified under Section 16 of CGST Act, 2017 have been satisfied.

- Reflecting of ITC in GSTR-2A/2B is not prescribed under GST law till 31.12.2021. It was inserted only wef 1.1.2022[ vide section 16(2)(aa)wherein sets out that the invoice details are furnished by supplier in GSTR 1 and be communicated to recipient in 2B].

- Diya Agencies Vs. State Tax Officer (Kerala High Court) – WP(C) No. 29769 of 2023, the Hon’ble Kerala High Court highlights that, denying input tax credit based solely on discrepancies in GSTR-2A is unjust.

- The input tax credit is an indefeasible and vested Right. Reliance can be placed in the case of Shabnam Petrofils Private Limited vs. Union of India (2019) 29 G.S.T.L. 225 (Guj.), Eicher Motors Ltd. Vs UOI – 1999 (106) ELT 3 (SC),

- The facility of GSTR-2A is ONLY for assesses facilitation and credit cannot be denied merely because it is not reflected in GSTR 2A. Refer press release 18th October 2018.

- Goparaj Gopalakrishnan Pillai v. State Tax Officer-1 [WP(C) NO. 29855 OF 2023], the Hon’ble Kerala High Court ruled in favour of the petitioner, by stating that the excess Input Tax Credit (ITC) claimed in Form GST-3B, which was not reflected in GSTR-2A, should not be a reason for denying the right to claim Input Tax Credit (ITC). Credit on the IGST paid at the time of import of goods shall be availed even if the same does not appear in GSTR 2A/2B To avoid disputes, suggest to maintain reconciliation of ITC availed in GSTR 3B, with 2A/2B, ITC in 9/9C and books of account.

- To avoid disputes, suggest to maintain reconciliation of ITC availed in GSTR 3B, with 2A/2B, ITC in 9/9C and books of account.

II. Differences of GST paid under reverse charge and credit availed:

- Reasons for difference to be provided along with reconciliation statement of RCM taxes paid and credit of such taxes being availed.

III. Denial of credit due to nonpayment of taxes by vendors as per Rule 37:

- It is near impossible to keep a track of the payment of tax by the supplier/vendor to the government under the existing scheme of returns as the tax is paid in GSTR-3B as the vendor pays the taxes by declaring it in a consolidated manner the principle of Lex Non-Cogit Ad Impossibiliae., The law does not compel a man to do that which he cannot possibly perform, as was held in the case of:

- Indian Seamless Steel & Alloys Ltd Vs UOI, 2003 (156) ELT 945 (Bom.)

- Hico Enterprises Vs CC, 2005 (189) ELT 135 (T-LB). Affirmed by SC in 2008 (228) ELT 161 (SC).

- Commr of CE vs Tata Motors Ltd (2012(294) ELT 394 (Jhar);

- Since the law cannot compel the taxpayers to comply with impossible conditions, whereby auditee does not have access to the portal to check whether supplier has actually paid or not.

- Even assuming that the taxes were not paid by vendors on the invoices, the substantial benefit of credit should not be denied due to the default [if any] by vendors. Further, the benefit of the input tax credit cannot be denied to a bona fide purchaser, because of the default of the selling dealer.

IV. Denial of credit due to cancelled registration of vendors:

ITC Cannot Be Denied Solely Due to Retrospective Cancellation as long as the purchaser complies with Section 16(2), their ITC claim remains valid.

To defend ITC claims, taxpayers should maintain detailed records, including:

- Tax invoices/Debit Note

- E-way bills

- Bank statements/Payment proof via Bank

- Proper Reconciliation of GSTR-2B with Books

- Proof of goods movement (kata slips, transporter records)

V. Denial of credit alleging blocked credit u/s 17(5):

√ ITC on Passenger Transport

ITC is blocked on motor vehicles used for transportation of persons having seating capacity ≤13 (including driver), except when used for:

(A) further supply of such vehicles,

(B) training on driving such vehicles,

(B) transportation of passengers.

√ ITC on Vessel and Aircraft

ITC is not available on vessels and aircraft except when used for:

(A) Transportation of Goods,

(B) Taxable supply of the same (further supply), passenger transport, or training on navigation/flying.

√ ITC on Insurance

ITC is blocked unless:

- The vehicle/vessel/aircraft is used for eligible purposes under clauses (a) or (aa), or

- The recipient is a manufacturer or insurer of such motor vehicles, vessels or

√ ITC allowed on food, beverages, outdoor catering, and similar personal services

ITC is not available on services like:

(A) Food and beverages, Outdoor catering,

(B) Beauty treatment, Health services, Cosmetic or plastic surgery,

(C) Leasing/renting of vehicles (as per clause a/aa),

(D) Life and health insurance, except when: The same category of supply is outwardly provided, or

(E) It forms part of a taxable composite or mixed supply.

√ ITC on air ticket service charges

(A) Eligible when air travel performed for purpose of company business.

√ ITC on Hotel Accommodation

(A) Eligible when performed for purpose of company business.

√ ITC on works contract services used for construction of immovable property

(A) ITC is not available on works contract services for construction of immovable property (other than plant and machinery), except when it is an input for further supply of works contract service.

3. Non payment of Reverse charge liability under section 9(3) r/w notification 13/2017-CT (R): Section 9(4) :-

Only specific categories of expenses notified under Section 9(3) are liable for RCM, such as legal services, goods transport agency (GTA), etc. Accordingly, identify such applicable transactions from the “Expenses” on which duly discharged GST under RCM on the same.

4. Concluding Remarks :-

In order to avoid any surprises during audit, it is also suggested to get pre-audit done internally / externally by competent professional CA’s. During pre-audit if any valid tax liability omitted/ unpaid found out [such as RCM on import of services/GTA services], discharge voluntarily with interest [to avoid penalty- if found in course of dept audit]. In this article the paper writer has given practical issues and the replies which if properly drafted could certainly help to avoid/reduce frivolous objections and relief by way of dropping of demands at the stage of audit itself [prior to SCN].

*******

The author can be contacted at calokeshaggarwal52@gmail.com His mobile number is +91-8368353016.

DISCLAIMER : This publication serves as a general guide for informational purposes only. The references and content provided are for educational purposes and should not be considered as legal advice.

Author Bio