CBIC has issued various notifications yesterday i.e on 10th Nov, 2020 amending various rules in respect of return filing. A summary of the same is as below:

♦ Notification No. 82/2020 – Central Tax

Central Goods and Services Tax (Thirteenth Amendment) Rules, 2020 have been notified. Highlights of the same are:

- e.f. 01.01.2021, an option for quarterly filing of FORM GSTR-1 would be made available to the taxpayers.

- The registered persons required to furnish GSTR 3B return quarterly under proviso to sub-section (1) of section 39 may furnish the details of such outward supplies for the first and second months of a quarter, up to a cumulative value of fifty lakh rupees in each of the months,- using invoice furnishing facility (IFF) from the 1st day of the month succeeding such month till the 13th day of the said month.

- The details furnished using the IFF, shall not be furnished again in FORM GSTR-1 for that quarter.

- The details furnished through IFF shall include only B2B supplies along with relevant DNs and CNs.

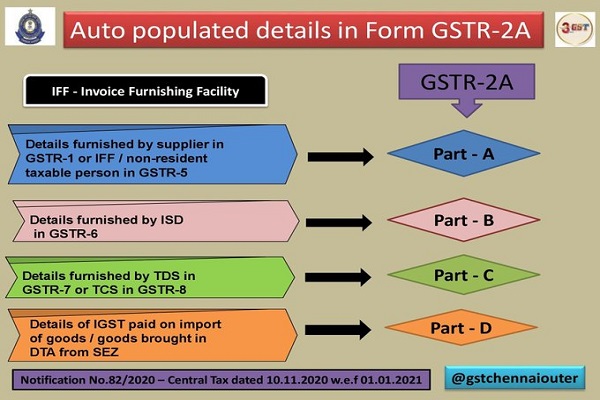

- W.e.f. 01.01.2021, FORM GSTR-2A shall also include details furnished through IFF and also details of the integrated tax paid on the import of goods or goods brought in domestic Tariff Area from SEZ unit or a SEZ developer on a bill of entry.

- FORM GSTR-2B has been given legal backing.

- Rule 61 has been amended and FORM GSTR-3B has been notified as the monthly and quarterly return and FORM GSTR-3 has been done away with.

- The due dates for monthly GSTR-3B is the 20th of the succeeding month while that of the quarterly GSTR-3B is the 22nd or 24th of the month succeeding such quarter based on the principal place of business of the Registered Persons.

- Quarterly return filers shall pay tax for the first two months of the quarter by using PMT-06 by 25th day of the succeeding month.

- The amount paid as above shall be credited in the electronic cash ledger and has to be debited while filing GSTR-3B quarterly.

- Rule 61A has been inserted to provide for the manner of opting quarterly GSTR-3B. Such option has to be exercised from the 1st day of the second month of the preceding quarter till the last day of the first month of the quarter for which the option is being exercised. In simple words, quarterly option for Apr-Jun 2021 can be exercised from 01.02.2021 till 30.04.2021.

- A Registered person shall not be eligible to opt for furnishing quarterly return in case the last return due on the date of exercising such option has not been furnished.

- A registered person, whose aggregate turnover exceeds 5 crore rupees during the current financial year, shall opt for furnishing of return on a monthly basis, from the first month of the quarter, succeeding the quarter during which his aggregate turnover exceeds 5 crore rupees.

- HSN Codes have to be mandatorily specified in FORM GSTR-1 as per proviso to Rule 46.

♦ Notification No. 83/2020 – Central Tax

W.e.f 01.01.2021, the due date for monthly GSTR-1 shall be 11th of the succeeding month, whereas, the due date for quarterly filers shall be the 13th of the month succeeding such quarter.

♦ Notification No. 84/2020 – Central Tax

Registered Persons having an aggregate turnover of up to Rs 5 crores in the preceding financial year and who have opted for quarterly return filing under Rule 61A as mentioned above can furnish quarterly GSTR-3B provided:

1. the return for the preceding month, as due on the date of exercising such option, has been furnished;

2. once exercised, such option shall continue unless revised by the registered person.

Default migration has been prescribed for registered persons who have furnished the return for the tax period October, 2020 on or before 30th November, 2020. Such default option can be changed from 05th December, 2020 to 31st January, 2021.

♦ Notification No. 85/2020 – Central Tax

Two options are prescribed for monthly payment of taxes in case of quarterly return filers.

Fixed Sum Method: A facility is being made available on the portal for generating a pre-filled challan in FORM GST PMT-06 for an amount equal to 35% of the tax paid in cash in the preceding quarter where the return was furnished quarterly; or equal to the tax paid in cash in the last month of the immediately preceding quarter where the return was furnished monthly.

Self-Assessment Method: The said persons, in any case, can pay the tax due by considering the tax liability on inward and outward supplies and the input tax credit available, in FORM GST PMT-06.

In case the balance in the electronic cash ledger and/or electronic credit ledger is adequate for the tax due for the first month of the quarter or where there is nil tax liability, the registered person may not deposit any amount for the said month. Similarly, for the second month of the quarter, in case the balance in the electronic cash ledger and/or electronic credit ledger is adequate for the cumulative tax due for the first and the second month of the quarter or where there is nil tax liability, the registered person may not deposit any amount.

♦ Notification No. 86/2020 – Central Tax

N.N 76/2020-CT dated 15th Oct, 2020 notifying due dates for FORM GSTR-3B for the months from Oct, 2020 till March, 2021 has been rescinded.

♦ Notification No. 87/2020 – Central Tax

The time limit for furnishing the declaration in FORM GST ITC-04, in respect of goods dispatched to a job worker or received from a job worker, during the period from July, 2020 to September, 2020 has been extended till the 30th day of November, 2020.

♦ Notification No. 88/2020 – Central Tax

W.e.f 01.01.2021, the provisions of e-invoicing shall be applicable to registered persons having turnover exceeding 100 crore rupees instead of current limit of 500 crore rupees

Circular No. 143/13/2020- GST has been issued on these matters which concur with our views as mentioned above.

Author Bio

You are awesome sir. Explained in a simple language. How this FM can frequently changes the GST Laws, is there any intention to kill the business community and tax professionals? Business community is just coming to the way and forgetting the COVID 19 impact and Govt. is sucking all the way.

If a dealer submits monthly Returns and the purchaser of that party submits quarterly Returns ,how input tax can be checked?

But i had not received any reply, and i would like to clear this quary.

If a dealer submits monthly Returns and the purchaser of that party submits quarterly Returns ,how input tax can be checked?