GST Came in 1st July 2017. After the GST arrival, many person took the GST number without knowing the applicability of GST. Many taxpayers did not even know that the returns of Nil GST had to be filed. As a result of this, taxpayers started getting to know GST registration cancellation.

In this article, we will discuss the cases when GST registration can be cancel. We also discuss the procedure of revocation of cancellation of registration.

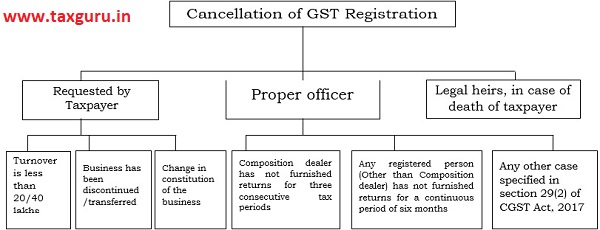

Section 29 (1) of CGST Act

Cases when registration may be cancelled

The proper office may cancel the registration in the following cases:

- On his motion: or

- On an application filed (In Form GST REG 16) by the registered person or his legal heirs, in case of death of such person.

Cancellation of registration shall be carried out keeping in view the circumstances where:

1. The business has been discontinued, transferred fully for any reason including-

- Death of the proprietor; or

- Amalgamated with other legal entity; or

- Demerged or otherwise disposed of; or

2. There is any change in the constitution of any business- e.g.: Partnership firm is converted into LLP leading to change in PAN; or

3. The taxable person, other than the person who is registered voluntarily is no longer liable to be registered under section 22 or section 24.

Proviso of section 29(1) of CGST Act (w.e.f. 01.02.2019)

During pendency of the proceedings relating to cancellation of registration filed by the registered person, the registration may be suspended for such period and in such manner as may be prescribed.

Application for cancellation of registration to be filled in FORM GST REG-16 including therein the following details:

- Details of inputs held in stock or inputs contained in semi-finished or finished goods held in stock and details of capital goods held in stock on the date from which the cancellation of registration is sought;

Tax liability thereon;

The details of the payment, If any, made against such liability; and

Other relevant documents in support thereon.

Application for cancellation of registration shall be made at the common portal within a period of 30 days of the occurrence of the event warranting the cancellation.

Cancellation by the Proper Officer (Section 29(2) of CGST Act)

The proper officer may cancel the registration of a person from such date, including any retrospective date, as he may deem fit, where-

(a) A registered taxable person has contravened the provisions of Act or Rules; or

(b) a person paying tax under Section 10 (composition dealer) has not furnished returns for three consecutive periods; or

(c) any registered person other than composition supplier has not furnished the returns for a consecutive period of six months; or

(d) a person who has taken voluntary registration has not commenced the business within six months from date of registration; or

(e) registration taken by means of fraud, willful misstatement or suppression of facts.

Rule 21: Registration to be cancelled in specified cases

- the registered person does not conduct any business from the declared place of business; or

- issues invoice or bill without supply of goods or services in violation of the provisions of the Act, or the rules made thereunder; or

- violates the provisions of Section 171 of the Act (Anti -Profiteering) or the rules made thereunder; or

- A registered person who does not furnish the details of the bank account within 45 days from the date of grant of registration or the date on which the return required under Section 39 is due to be furnished, whichever is earlier.

Rule 22: Procedure for Cancellation of Registration by the Proper Officer

- Where the proper officer has reasons to believe that the registration of a person is liable to be cancelled, then he shall issue a notice in FORM GST REG-17 requiring the person to show cause as to why the registration shall not be cancelled.

- A reply to this notice has to be given within 7 working days from the date of service of notice in FORM GST REG- 18.

- If the reply to the notice is found to be satisfactory, then the proper officer shall drop the proceedings and pass an order in FORM GST REG -20.

- If the registered person instead of filing a reply to the show cause notice, furnishes all the returns and makes full payment of the tax dues along with applicable interest and late fee, the proper officer can drop the proceedings and pass an order in FORM GST REG-20.

- Where the registration is liable to be cancelled, then the proper officer shall issue an order in FORM GST REG- 19 within 30 days from the date of reply to Show Cause Notice, cancelling the registration.

Section 29(3) of CGST Act

Person shall still remain to pay tax and other dues

The cancellation of registration under this section shall not affect the liability of the person to pay tax and other dues under this act or to discharge any obligation under this Act or the rules made thereunder for any period prior to the date of cancellation whether or not such tax and other dues are determined before or after the date of cancellation.

Revocation of cancellation of registration

Revocation of cancellation of registration means that the decision to cancel the registration has been reversed and the registration is still valid.

Section 30(1) of CGST Act with Rule 23 (1)

Application for revocation of cancellation of registration

Any registered person, whose registration is cancelled by the proper officer on his own motion, may apply to such officer for revocation of cancellation of the registration in the FORM GST REG-21 within thirty days from the date of service of the cancellation order at the common portal.

As per proviso to Rule 23(1), in case the registration has been cancelled due to non filing of returns the application of registration can be filed only after furnishing of returns and payment of tax, interest, penalty and late fee.

Further, second proviso to Rule 23(1), the returns for the period from date of order of cancellation of registration till the date of order of revocation of cancellation of registration shall be furnished within 30 days from date of such order.

Example:

| Date of order of cancellation of Mr. A | 01.07.2019 |

| Date of order of revocation of cancellation | 31.08.2019 |

Mr. A shall be required to furnish all the returns for the period from 01.07.2019 to 31.08.2019 by 30.09.2019 i.e. within a period of 30 days from 31.08.2019.

Further, third proviso to Rule 23(1), where the registration has been cancelled with retrospective effect, all returns relating to period from the effective date of cancellation of registration till the date of order of revocation of cancellation of registration shall be furnished by a registered person whose registration is cancelled. Such returns shall be furnished within 30 days from the date of order of revocation of cancellation of registration.

Example:

| Date of order of cancellation of Mr. A retrospectively with effect from 01.11.2018 | 01.07.2019 |

| Effective date of cancellation of registration | 01.11.2018 |

| Date of order of revocation of cancellation | 31.08.2019 |

Mr. A shall be required to furnish all the returns for the period from 01.11.2018 to 31.08.2019 by 30.09.2019 i.e. within a period of 30 days from 31.08.2019.

Acceptance or Rejection of Application

Section 30(2) of CGST Act, 2017

The proper officer may by order either revoke cancellation of the registration or reject the application of revocation of registration. However, the application for revocation of cancellation of registration shall be rejected unless the applicant has been given an opportunity of being heard.

As per Rule 23(2) (a), where the proper officer is satisfied, for reasons to be recorded in writing, that there are sufficient grounds for revocation of cancellation of registration, he shall revoke the cancellation of registration by an order in FORM GST REG-22 within a period of thirty days from the date of the receipt of the application and communicate the same to the applicant.

Further Rule 23(2) (b), provides that the proper officer may reject the application for revocation of cancellation of registration by an order in FORM GST REG-05 and communicate the same to the applicant.

As per Rule 23 (3), before passing the order for rejecting the application for revocation of cancellation of registration, the proper officer shall issue a notice in FORM GST REG-23 requiring the applicant to show cause as to why the application submitted for revocation should not be rejected and the applicant shall furnish the reply within a period of seven working days from the date of the service of the notice in FORM GST REG-24.

Further in terms of Rule 23 (4), Upon receipt of the information or clarification in FORM GST REG-24, the proper officer shall proceed to dispose of the application by either revoking the cancellation of registration or rejecting the application, within 30 days from the date of receipt of such information or clarification from the applicant.

Relief in regard to revocation of cancellation of registration

As per notification no. 35/2020- Central Tax Dated 03.04.2020,was issued under section 168A of CGST Act, 2017, time limit of any compliance which falls during the period from 20.03.2020 to 29.06.2020 shall be extended upto the 30.06.2020.

As per this notification, if the registration has been cancelled, the application for revocation of cancellation of registration is to be filed within 30 days from the date of service of order of cancellation of registration. Now if such period of 30 days is expiring between 20.03.2020 to 29.06.2020, the application can be filed till 30.06.2020.

One Time extension in period for seeking revocation of cancellation of registration

one of the decision made by GST Council in its 40th Meeting held on 12.06.2020 is providing a one time extension in period for seeking revocation of cancellation of registration.

To facilitate taxpayers who could not get their cancelled GST registrations restored in time, an opportunity is being provided for filing of application for revocation of cancellation of registration up to 30.09.2020, in all cases where registration have been cancelled till 12.06.2020.

Disclaimer: This is meant purely for general education purpose.While the information is believed to be accurate to the best of my knowledge, I do not make any representations or warranties, express or implied, as to the accuracy or completeness of this information. Reader should conduct and rely upon their own examination and analysis and are advised to seek their own professional advice. This note is not an offer, invitation, advice or solicitation of any kind. I accept no responsibility for any errors it may contain, whether caused by negligence or otherwise or for any loss, howsoever caused or sustained, by the person who relies upon it.

Author Bio

When did my revocation of cancellation letter is issued