With the Covid 19 situation changing the dynamics of business huge reliance is placed by the taxpayers on the refunds available under the various laws. GST being no exception is also flooded with applications for refunds specially as for many MSMEs working capital tied up in refund is a huge challenge. However as the entire mechanism of refund is made online wef 26th September, 2019 the visits to the GST offices for following up on refunds have been significantly reduced. Though we have recently started leaving our houses and going to offices, most of the movements are restricted and visits to different offices are on need basis only. So I am sharing the preferred mode of communication with the GST department in relation to the refund applications filed which has been introduced on the common portal. Hopefully this will help the tax payers to know the status of the refunds, post which may be needful action can be taken.

Issues related to processing of refund

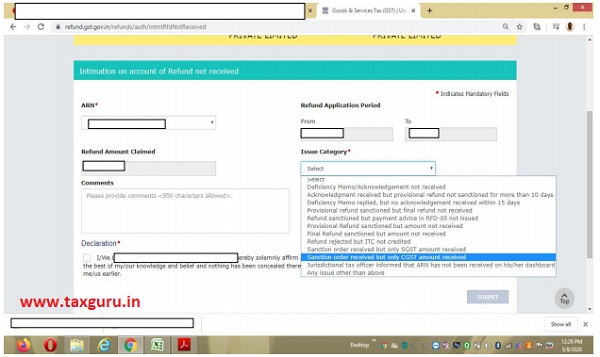

Some of the common reasons for which such intimation can be filed are :

1. Deficiency memo/ Acknowledgement not received.

2. Deficiency memo replied, but no acknowledgement received within 15 days.

3. Refund sanctioned by Payment advice in RFD 05 not issued.

4. Final refund sanctioned but amount not received.

5. Refund rejected but ITC not credited.

6. Sanction order received but only CGST/IGST/SGST received

7. Jurisdictional tax officer has informed that ARN has not been received in his/her dashboard

8. Acknowledgement received but provisional refund not sanctioned for more than 10 days.

9. Provisional refund sanctioned but amount/final refund not received.

10. Any other issue

In the any other issue we could mention the other issues faced by us if any. For instance refund is rejected and ITC is also re credited, but taxpayer is unable to file refund for the same period.

Precaution is better than cure

As we all are aware about the above common saying, it very much applies to our refund applications under the various heads. Prior to filing of the refunds we would need to prepare ourselves by diligently following the requirements as per the Master Circular on refund CGST 125/2019 issued on 18/11/2019 and also subsequent CGST Circular 135/2020 dated 31/03/2020. Apart from these other notifications and circulars as applicable to the refund applications need to be followed .

So we should first of all check as to the eligibility for the refund and then finalize the appropriate category as the requirements may vary from case to case. Once the eligibility, category of refund and documents required are finalised, we would need to fill the online forms get the documents signed and duly scanned so that they are within the size restrictions as mentioned on the common portal and then file the refund.

Now lets discuss the process as to how we can move towards filing of the intimation.

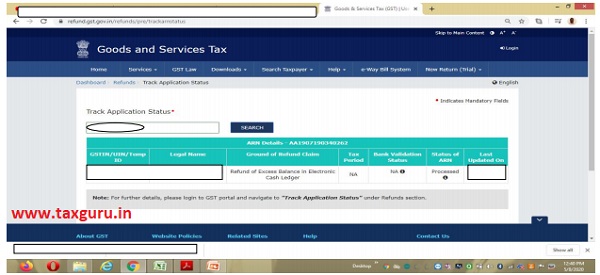

Step 1 : Checking the status of Refund

For this we need to go to the common portal www.gst.gov.in and then we need to visit the services tab. From the services tab we need to go to the refunds tab and click on track application status.

Step 2 : Key the ARN and check the status.

Once the ARN is keyed in the status of the refund will be reflected. So in case of a refund for excess balance in cash ledger, may be our refund is processed and we have received the sanction order, but we have not received the refund from the department. So we can file an intimation for the same to know whether there is any other technical issue because of which the refund is getting delayed.

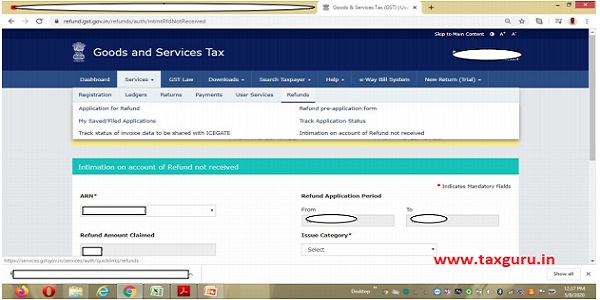

Step 3 : Filing an intimatation

We can also know the status of the refund by using the log in feature and going to refund tab as mentioned above.

So once we are aware about the correct status of the refund from the status as shown on the portal we would need to collate the supporting facts if any which we would like to upload along with the intimation in the comments portion. For example the date of receipt of sanction order or filing of reply, or any other information that would help the nodal officer or the jurisdictional tax officer to evaluate the actions taken by the taxpayer and enable him/her to process the refund application.

For filing the intimation we would need to log in the common portal using our user id and password.

Then we would need to put the ARN and other details and then choose the issue category properly by assessing as to what is the issue in relation to the refund that we would like to highlight and get feedback on.

We would need to understand that if the issue chosen by us is inappropriate, maybe we will not be able to get the desired results we want. Hence we need to see in which stage of refund processing our present application is lying and then choose category accordingly. For instance, may be we have replied to the Deficiency memo but have not received the acknowledgement, so here if we choose any other category and state that our refund is not sanctioned, we would not be able to get a proper status update.

Step 4 : Providing necessary details

Once we choose the issue category properly based on the information available to us, in the comments section we would need to put in as much details possible and then submit the form. Once we submit the same, we would get an acknowledgment number which we need to keep for our records.

As the GST laws are still evolving and refund process has lately transitioned from partly manual and partly online to fully online process, some teething issues are being experienced which we are hopeful of being resolved as we move forward as huge number of refunds have been processed during the last three months. While on this it would be inappropriate if I don’t mention that various refund provisions and circulars are being debated and deliberated upon in various forums. However until they are changed either through further amendments in law or changes in position of law because of Judicial review, we would need to abide by the same and file refund applications accordingly.

Appeal relating to refunds : If you have already received a rejection order already you have the option to either re file the application or file an appeal with the Jurisdictional Appellate Authority if you deem necessary. For that raising an intimation as discussed above would not be the right approach.

Disclaimer : The article is purely for educational purpose and has not legal validity. Hence no liability shall arise to the author whatsoever for relying on the above. In case there is any difference of opinion or any suggestions relating to subjects for future articles, it would be great if you could mail me at dgarup@gmail.com or put it in the comments section.

Author Bio