Reassessment of income escaping assessment has always remained one of most litigatd areas in direct tax practice. Under Income tax Act, 1961 reassessment mechanism was primarily contained in Sections 147 to 153 which was substantially changed by the Finance Act, 2021 & further refined by the Finance Act 2024.

Income tax Act 2025 continues with this refined reassessment structure, but place it in new statutory framework under Sections 279 to 286. We hereby discussing the new scheme, the procedure for issuing reassessment notice, the time limits, and most importantly, the transitional position for tax years prior to 1 April 2026.

For tax professionals, this chapter is extremely important because reassessment notices after 1 April 2026 may still relate to old assessment years.

Hence, first and practical question will not merely be “whether reassessment is valid”, but “which Act governs the reassessment?”

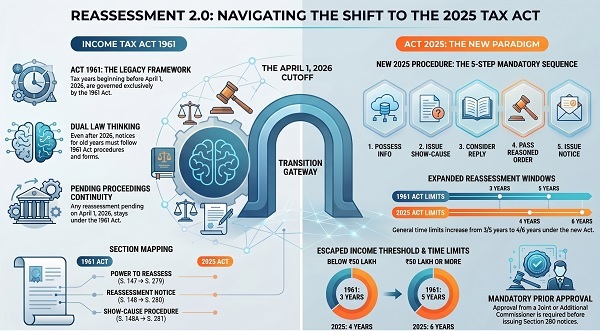

1. The Reassessment Section Mapping

The 2025 Act restructures reassessment provisions by replacing old sections numbers with new ones. The substance of the framework is carried forward with structural improvements.

| Description | Income tax Act 1961 | Income tax Act 2025 |

| Power to assess/reassess escaped income | Section 147 | Section 279 |

| Issue of notice for reassessment | Section 148 | Section 280 |

| Procedure before issue of notice / show-cause | Section 148A | Section 281 |

| Saving where notice deemed valid | Section 148B | Folded into Section 281 |

| Time limits for notices | Section 149 | Section 282 |

| Assessment pursuant to appellate/court orders | Section 150 | Section 283 |

| Sanction for issue of notice | Section 151 | Section 284 |

| Rate of tax / dropping of proceedings | Section 152 | Section 285 |

| Time limit for completion of reassessment | Section 153 | Section 286 |

Above mentioned mapping is very much needed because once new Act comes into force, professionals will need to identify whether the case falls under the 1961 Act or the 2025 Act before drafting any response, objection, writ petition, appeal, or advisory note.

2. The New Reassessment Procedure Under the 2025 Act

Section 280 read with Section 281 of the Income tax Act, 2025 prescribes a structured procedure for issuing a reassessment notice.

This process is broadly divided into five below mentioned stages : –

Step 1: AO Must have information suggesting escapement

Assessing Officer must first possess “information suggesting that income chargeable to tax has escaped assessment” for the relevant tax year. This is the foundation of the reassessment proceeding.

Without such information, the reassessment process cannot be validly triggered.

Step 2: Show-Cause Notice Under Section 281(1)

Before issuing notice under Section 280, AO must issue showcause notice u/s. 281(1). Notice must share & contain information with assessee and provide reasonable opportunity to respond within the prescribed time.

This is a crucial safeguard because it gives assessee a opportunity to explain why reassessment should not be initiated.

Step 3: AO must consider Assessee’s reply

After receiving reply, AO is required to consider response of assessee which means reply cannot be ignored mechanically.

The consideration of reply is very much important procedural step because it connects natural justice with reassessment jurisdiction.

Step 4: Reasoned order u/s. 281(3)

AO must pass reasoned order u/s. 281(3) with prior approval of Hon. Additional Commissioner or Hon. Joint Commissioner, deciding whether the case is fit for reassessment or no.

This order becomes very important in litigation because it shows whether the AO has applied his mind to the information and the assessee’s explanation.

Step 5: Formal Notice u/s. 280

If order is in favour of reopening, AO may issue formal reassessment notice u/s. 280.

Even where show-cause procedure u/s. 281 is not required prior approval of Hon. Additional Commissioner or Hon. Joint Commissioner remains mandatory before issuing notice u/s. 280.

3. What Qualifies as “Information Suggesting Escaped Assessment”?

Section 280(6) of the 2025 Act provides exhaustive list of categories of information that may trigger for reassessment which is very important part of new framework because reopening cannot be based on vague suspicion.

The following categories are recognised:

1. Information identified under the Board’s risk management strategy for the relevant year

2. Audit objections indicating that assessment was not done as per the Act.

3. Information received under agreement with a foreign country or specified territory under Section 159.

4. Information made available to the AO under any scheme notified under Section 260 for collection of information.

5. Information requiring action pursuant to Tribunal or Court order

6. Information arising from survys conducted u/s. 253 except sub-section (4).

7. Directions from the Approving Panel under Section 274(6) in GAAR cases.

8. Findings or directions contained in an order passed by any authority, Tribunal or Court.

Above mentioned is statutory list and important for professionals because the first level of examination in any reassessment case should be whether information relied upon by the AO falls within the permitted categories.

4. When can officer skip the Section 281 Showcause procedure?

Showcause procedure u/s. 281 is normally mandatory. However Section 281(4) carves out limited exceptions where AO may directly proceed to issue notice Under Section 280 without issuing showcause notice u/s, 281(1).

There are some exceptions as under : –

1. Where information is received under faceless collection of information scheme notified u/s. 260.

2. Where directions are received from the GAAR Approving Panel u/s. 274(6), declaring an arrangement to be an impermissible avoidance arrangement.

3. Where there is finding or direction in order passed by any authority, Tribunal or Court in proceedings under the Act by way of appeal, reference or revision, or by a Court in proceedings under any other law.

In all other cases, the show-cause procedure Under Section 281 is mandatory. AO cannot make assessment, reassessment, or recomputation u/s. 279 without issuing notice under Section 280.

5. Time Limits Under the Old Act and New Act

This gives us clear comparison of reassessment notice time limits under 1961 Act and the 2025 Act.

a. Time limit under Income tax Act 1961 : –

| Notice / Threshold | Time Limit from End of Assessment Year |

| Section 148A showcause where escaped income is below ₹50 lakh | 3 years |

| Section 148A showcause where escaped income is ₹50 lakh or more | 5 years |

| Section 148 reassessment notice where escaped income is below ₹50 lakh | 3 years and 3 months |

| Section 148 reassessment notice where escaped income is ₹50 lakh or more | 5 years and 3 months |

b. Time Limits Under the Income tax Act, 2025

| Notice / Threshold | Time Limit from End of Tax Year |

| Section 281 showcause where escaped income is below ₹50 lakh | 4 years |

| Section 281 showcause where escaped income is ₹50 lakh or more | 6 years |

| Section 280 reassessment notice where escaped income is below ₹50 lakh | 4 years and 3 months |

| Section 280 reassessment notice where escaped income is ₹50 lakh or more | 6 years and 3 months |

Section 282(3) also provides that no notice under Section 280 or 281 shall be issued within one year from end of any tax year.

Further also, Section 286(1) provides that reassessment order u/s. 279 must be passed within one year from end of financial year in which notice under Section 280 was served, subject to extensions & exclusions for matters such as transfer pricing references and ITAT/court stay orders.

6. Big Shift : Expanded Reassessment Window Under the 2025 Act

One of the major practical takeaways is that reassessment time limits have expanded under the 2025 Act.

For cases involving escaped income below ₹50 lakh, the general showcause time limit has increased from 3 years under Section 149 of the 1961 Act to 4 years under Section 282 of the 2025 Act.

For cases involvement for escapment of income of grater than ₹50 lakh for that extended time limit increased from 5 years to 6 years.

However expansion is relevant for tax year beginning from 1 April 2026. For year before 2026 old time limit under 1961 Act continue to apply by the virtue of Section 536(2)(c).

Above distinction is extremely important. For income for Financial year 2025-26 old 3 year / 5 year framework remain relevant. For income for Financial Year 2026-27 new 4 years and 6 year framework apply.

7. Transitional Rule: The Real Game-Changer

Very Most important part of is the transition rule. Section 536(2)(c) provides the master rule.

Pre 2026 Tax Years Continue Under the 1961 Act

Reassessment of any tax year which is beginning before 1st April 2026 is governed exclusively by Income tax Act 1961.

This means that for earlier assessment years, the Department cannot automatically apply Sections 279 to 286 of the 2025 Act merely because the new Act has come into force.

The CBDT has also restated this position in its FAQs also.

8. Pending Reassessment as on 1 April 2026

Where a notice u/s. 148 of the 1961 Act was issued before 1 April 2026 & proceedings remain pending on commencement date entire reassessment continues under the 1961 Act.

Even if reassessment order is passed in 2027 or later, it will still be passed under the 1961 Act.

All consequential proceedings will also be governed by the 1961 Act, including :

- Penalty under Section 271(1)(c) or Section 270A;

- Appeal under Section 246A or Section 253;

- Rectification under Section 154.

This principle avoids confusion and ensures procedural continuity for old tax years.

9. Fresh Reassessment Notices After 1 April 2026 for Old Years

Department may initiate fresh reassessment proceedings which may be after 1st April 2026 for assessment year 2026-27 or it can be for earlier assessment year which should be subject to limitation u/s. 149 of 1961 Act.

In such cases :-

1. Entire procedure will be u/s. 148A of the 1961 Act;

2. Notice will be u/s. 148 of the 1961 Act;

3. Approval will be as per Section 151 of the 1961 Act;

4. Consequential proceedings will also remain under the 1961 Act.

Mere enforcement of the 2025 Act does not bring Sections 279 to 286 into play for pre-2026 years.

Here is very important drafting point for professionals that If a notice for an old assessment year is issued after 1 April 2026, the assessee’s reply should still be framed under the 1961 Act, not under the 2025 Act.

10. Notices Straddling the Transition Date

A practical situation may arise where showcause notice u/s. 148A(1) of the 1961 Act is issued before 1 April 2026, but the order under Section 148A(3) and the formal notice u/s. 148 are issued after 1 April 2026

Entire sequence continues under the 1961 Act, subject to limitation under Section 149 of the 1961 Act.

The assessee must respond under the 1961 Act framework and file the return in response to Section 148 notice in the form prescribed under the 1961 Rules.

11. Parallel Proceedings Under Both Acts

Lets take example the same assessee may have :

- There can be reassessment proceedings for AY 24-25 under old Act along with assessment proceedings for Tax Year 2026-27 under New Act.

Both can run simultaneously because they are definitely related to different income periods as well as governed by different statutory framework also

For tax professionals, this means one client may require two separate compliance tracks at same time — one under the 1961 Act and another under the 2025 Act.

12. Penalty Proceedings for the year before year 2026.

Section 536 (2) (d) provide that the penalty proceedings for tax year beginning before 1st April 2026 can be initiated & penalty may be imposed under 1961 Act as on the assumption that the new Act had not been enacted.

Therefore penalties arising from reassessment of years before 2026 will follow Sections 270A, 271(1)(c) etc. of Income tax Act 1961.

This remains true even if penalty notice is issued and penalty order is passed after 1st April 2026.

13. Let’s discuss certain CBDT FAQ which are completely based on practical issues : –

a. For which tax year will new reassessment provisions apply?

As per section 279 to 286 of Income tax act 2025 it applies to Tax Year 26-27 only and for subsequent years which clearly means that for any tax year beginning before 1st April 2026 Income tax Act 1961 apply.

b. Can Department take action of reassessment for assessment year 22-23 or 24-25 after 1st April 2026?

Yes definitely but provided limitation period u/s. 149 of the 1961 Act has not expired and also new Act does not extend or revive limitation which has already expired

c. If notice u/s. 148A(1) is issued before 1 April 2026 but notice u/s. 148 is issued after 1 April 2026 in that case is the proceeding valid?

Yes surely this sequence is governed by 961 Act however limitation period under Section 149 must be taken care off.

d. Who can approve notice for reassessment for AY 26-27 or earlier after 1 April 2026?

Approval remains under hierarchy u/s. 151 of the 1961 Act which is specified authority Additional Commissioner / Additional Director / Joint Commissioner / Joint Director.

e. Is there any form in which assessee should respond to notice u/s. 148 issued after 1 April 2026 for AY 22-23?

Assessee must respond in Income tax return form prescribed under 1961 Rules for that assessment year because entire reassessment is governed by 1961 Act framework.

14. Professional Checklist for Tax Practitioners from article

Everyone before replying to any reassessment notice after 1 April 2026 should check below mentioned simple checklist :-

1. Which tax year is involved?

If the tax year begin before 1 April 2026 the 1961 Act governs.

2. What is the nature of notice?

For old years verify whether it is u/s. 148A / 148 of Act. For new years check the sections 281 / 280 of 2025 Act.

3. Whether show cause procedure was mandatory or not. ?

Under 2025 Act, Section 281 specifically talks about mandatory nature of show cause except in limited cases under Section 281(4).

4. Whether information falls within permitted category or not ?

U/s. 280(6) whatever information possessed by AO must fall within listed categories.

5. Whether approval requirement was fulfilled or not.?

Under 2025 Act approval of Additional Commissioner or Joint Commissioner is required at the relevant stage.

6. Whether limitation is satisfied or not ?

For old years check section 149 of 1961 Act. For new year check Section 282 of 2025 Act.

7. Whether Department is wrongly applying the new Act to old years?

Section 536(2)(c) which specifically protects old years from being shifted into 2025 Act framework.

8. Whether penalty proceedings follow the correct Act?

For tax year prior to 2026 penalty proceedings continue under 1961 Act.

9. New Reassessment Era Requires Dual Law Thinking right ????

For tax professionals most important learning is this after 1st April 2026 every reassessment case must be examined through two lenses first >>> tax year involved & second >>> Applicable Act

For tax years beginning before 1st April 2026 Income tax Act 1961 continues to govern reassessment, limitation, approval, penalty, appeal, and rectification.

However, for Tax-Year 26-27 & onwards new reassessment code u/s. 279 to 286 is applicable.

In practical terms reassessment litigation after 2026 will not become simpler merely because new Act exists. Professionals must need sharper classification better limitation analysis along with strong procedural scrutiny.

Future ready tax professional will not just ask >>> “What is the addition?” but also will first ask >>> “Which Act controls the notice?”

Author Bio