Case Law Details

In re Gangwal Healthcare Private Limited (CAAR Mumbai)

The Customs Authority for Advance Ruling (CAAR), Mumbai, has ruled that Corn Silk Extract Powder, proposed for import by Gangwal Healthcare Private Limited, should be classified under Customs Tariff Heading (CTH) 1302 19 19. This classification supports the applicant’s claim for a partial exemption from customs duty, as specified under Sl. No. 54 of notification No. 50/2017-Customs,

Applicant’s Position and Supporting Evidence

Gangwal Healthcare Private Limited sought an advance ruling to clarify the customs classification of “Corn Silk Extract Powder” and its eligibility for a partial customs duty exemption. The company plans to import this product, manufactured in China, which is derived from the “Style and Stigma” parts of the corn plant (Zea Mays L). The applicant submitted that the extract is obtained through a simple hot water extraction process, followed by evaporation and spray drying, resulting in a 100% pure corn silk extract powder. This powder is intended for use as a raw material in the manufacture of nutritional supplements. The applicant relied on the Harmonized System of Nomenclature (HSN) Explanatory Notes for Heading 13.02, which covers “Vegetable saps and extracts,” and cited a US Customs Ruling (N241904) supporting this classification. They argued that the extract, being from a plant part and obtained via solvent extraction without additives that alter its character, squarely fits within Heading 1302.

Jurisdictional Commissionerates’ Divergent Views

The jurisdictional Commissionerates presented differing opinions. The Nhava Sheva Commissionerate argued that corn silk extract, being used in therapeutic applications like nutritional supplements, might be excluded from Heading 13.02 as per HSN notes related to therapeutic or prophylactic purposes. They suggested Heading 2106 (Food preparations) as a potential alternative. Conversely, the Sahar Air Cargo Commissionerate contended that corn silk, derived from a cereal (maize), is not botanically classified as a vegetable and thus might not fall under “Vegetable Extracts” of CTH 1302 19 19. They proposed CTH 1302 39 90 (Other Plant Extracts) as a more accurate classification if it remained a pure extract, or CTH 2106 90 99 if it was a formulated nutritional supplement. However, neither of these alternative headings would qualify for the exemption under notification No. 50/2017-Customs,

CAAR’s Ruling and Rationale

The CAAR, after careful examination of submissions and legal precedents, ruled in favour of the applicant. The Authority noted that Heading 13.02 specifically covers “Vegetable saps and extracts.” While Chapter 13 Notes do exclude certain products like medicaments put up for retail sale for therapeutic purposes, the CAAR found that the “Corn Silk Extract Powder” in this case is imported in bulk and is not a finished medicament. Furthermore, the HSN Explanatory Notes broaden the definition of “vegetable” for Heading 13.02 to include extracts from various plant materials, including cereals like rye, as exemplified. The CAAR determined that the extraction process described by the applicant, using hot water and resulting in a pure extract without added substances that change its fundamental character, aligns with the requirements for classification under Heading 13.02. The Authority dismissed the applicability of Heading 2106, as the product is not a “food preparation” in itself but a raw material, and also rejected CTH 1302 39 90, as the Corn Silk Extract does not fit the description of mucilages or thickeners derived from specific seeds.

Conclusion on Classification and Exemption

The CAAR concluded that the “Corn Silk Extract Powder” is indeed a vegetable extract and is appropriately classifiable under HS Code 1302 19 19. Consequently, the Authority ruled that the goods are eligible for the partial exemption from customs duty as provided under Sl. No. 54 of notification No. 50/2017-Customs, dated the 30th June, 2017 which grants an exemption from so much of the customs duty as is in excess of 15%.

FULL TEXT OF THE ORDER OF CUSTOMS AUTHORITY OF ADVANCE RULING, MUMBAI

1. Gangwal Healthcare Private Limited (JEC No. AAJCG0105E) (hereinafter referred as “The Applicant”) filed an application for advance ruling in the Office of Secretary, Customs Authority for Advance Ruling, Mumbai. The said application was received in the secretariat of the CAAR, Mumbai on 28.04.2025, along with its enclosures in terms of Section 28H (1) of the Customs Act, 1962 (hereinafter referred to as the ‘Act’). The applicant is seeking advance ruling regarding classification of the goods “Corn Silk Extract Powder” and applicability of exemptions available under Sr. No. 54 of notification No. 50/2017-Customs, dated the 30th June, 2017

2. Submission by the Applicant:

2.1 The Applicant is a private limited company and is engaged in the activity of import and trading of various goods. The Applicant is proposing to import “Corn Silk Extract Powder” manufactured by Herbalife Nat Source (Hunan) Natural Products Co. Ltd., China and sold under the name “Corn Silk Extract Powder, India”.

2.2 The Applicant submitted that the said Corn Silk Extract Powder is a vegetable extract in powder form, consisting of 100% corn silk extract. It is imported in bulk and used as raw material/ ingredient in manufacture of Nutritional Supplements. The applicant further submitted that the said Corn Silk Extract Powder is obtained by extraction from the “Style and Stigma” parts of the Plant having the botanical name “Zea Mays L”, commonly known as “Corn”. The process of extraction is by Water extraction, using hot water as the Solvent for extraction. The water is thereafter evaporated to obtain the solid, which is spray dried to obtain the powder, which is 100% Corn Silk Extract in powder form. The said Corn Silk Extract Powder is used as an ingredient/ raw material in the manufacture of Nutritional Supplement.

3. Applicants Interpretation of Law/Facts:

3.1 The applicant submitted that the “Corn Silk Extract powder” being an extract from the “Style and Stigma” parts of the Plant having the botanical name “Zea Mays L”, commonly known as “Corn”, the same is Vegetable Extract which is covered by Customs Tariff Heading 13.02, which covers “Vegetable Saps and Extracts”. Under Heading 13.02, “Corn Silk Extract Powder” is correctly classifiable as “Other” Vegetable Extract under the four dash (—) Sub-heading 13021919, which falls under the triple dash (—) description of “Extracts”, which falls under double dash (–) sub- heading “Other”, which falls under single dash (-) description of Vegetable saps and extracts.

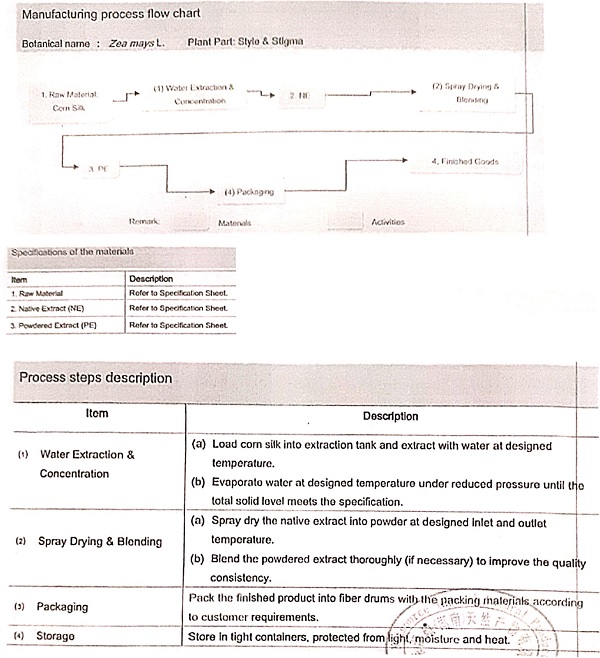

3.2 The applicant further submitted that Corn silk are the fine thread-like “Styles” on the ear of Corn. The Corn Silk Extract is obtained by extraction from the “Style and Stigma” parts of the Plant having the botanical name “Zea Mays L”, commonly known as “Corn”. The process of extraction is by Water extraction, using hot water as the Solvent for extraction. The water is thereafter evaporated to obtain the solid, which is spray dried to obtain the powder, which is 100% Corn Silk Extract in powder form. The product Corn Silk Extract powder is 100% Corn Silk extract in powder form and no additives are added to the said corn silk extract powder. This is evident from the Material Safety Data Sheet, Manufacturing Process Flow Chart and Composition of the said product.

Manufacturing Process Flow Chart:

3.5 The applicant further submitted that as per the HSN notes under Heading 13.02, the vegetable extract of heading 13.02 arc generally used as raw materials for various manufactured products. As submitted herein above, the “Corn Silk Extract Powder” is used as an ingredient/ raw material in the manufacture of Nutritional Supplement.

3.6 The applicant submitted that in view of the above analysis, the said product to be imported as “Corn Silk Extract Powder” is correctly classifiable under Heading 13.02 and Sub-heading 13 02 1919. Further, in support of the classification of “Corn Silk Extract Powder” under Heading 13.02, the applicant placed its reliance on US Customs Ruling N241904 dated 4th June 2013.

3.7 The applicant further submitted that all goods of Heading 1302 19 (other than vegetable seeds and extracts of pyrethrum or of the roots of plants containing rotenone) are covered by Sr. No. 54 of notification No. 50/2017-Customs, dated the 30th June, 2017 and entitled to partial exemption from Customs duty in excess of 15%. Accordingly, the said goods, “Corn Silk Extract Powder” are covered by the said sr. No.54 and liable to Customs duty at 15%.

4. Port of Import and reply from Jurisdictional Commissionerate

4.1 The applicant in their CAAR-1 indicated that they intend to import the subject goods i.e. Corn Silk Extract Powder at the jurisdiction of office of the Pr. Commissioner of Customs, NS-I, JNCH, Nhava Sheva, Tal: Uran Distt: Raigad, Maharashtra-400707 and at the jurisdiction of office of the Principal Commissioner/Commissioner of Customs (Imports), Air Cargo Complex, Sahar, Andheri (East), Mumbai 400099. In terms of Provisions of the Section 28-1(1) of the Customs Act, 1962 read with the Sub-regulation No. (7) of the Regulation No. 8 of the Customs Authority for Advance Rulings Regulations, 2021, the application was forwarded to the office of the Principal Commissioner of Customs, NS-I, JNCH, Nhava Sheva, Tal: Uran Distt: Raigad, Maharashtra-400707 and to the of office of the Principal Commissioner/Commissioner of Customs (Imports), Air Cargo Complex, Sahar, Andheri (East), Mumbai 400099 on 01.05.2025 as indicated by the applicant at Sr. No. 13 of their CAAR-1 Forms calling upon them to furnish the relevant records with comments, if any, in respect of the said application.

4.2 The Nhava Sheva Commissionerate vide its letter dated 28.05.2025 stated that the goods are extracts of Corn and are going to be used in nutritional supplements i.e. in therapeutic applications. The reference can be taken from Chapter Notes of Heading 1302 — “the heading also excludes vegetable extracts which have been mixed or compounded (without the addition of other substances) for therapeutic or prophylactic purposes ….” Therefore, 1302 is not the right heading for classification of goods. The Commissionerate further stated that the goods are intended to be imported from China and as found in open source, process of manufacturing Corn Silk involves inclusion of ethanol along with processing with boiling water. The importer also submitted that the process of extraction is by Water extraction, using hot water as the Solvent for extraction. In addition to above, the said product Corn Silk Powder is going to be added in nutritional supplements for human consumption after processing and therefore, for reference to decide right classification, Chapter Notes of Heading 2106 are produced below:

| “2106 | – | Food preparations not elsewhere specified or included |

| 2106.10 | – | Protein Concentrates and textured protein substances |

| 2106.90 | – | Other |

Provided that they are not covered by any other heading of the Nomenclature, this heading cover:

(A) Preparations for use, either directly or after processing (such lying or boiling in water, milk, etc.) for human consumption.”

The Commissionerate concluded that in view of the above, it appears that the right classification for import of Corn Silk is under Heading 2106 as goods are preparations (extract) which will be used in nutritional supplements for human consumption.

4.3 The Sahar Air Cargo (Import) Commissionerate vide its letter dated 20.06.2025 (received in this office vide email dated 12.08.2025) stated that after a detailed analysis of the submissions made by the importer, relevant tariff headings, Harmonised System of Nomenclature (HSN) Explanatory Notes, and scientific classification of the product, the Department submits the following comments:

A. On the Nature and Botanical Identity of the Product: Corn silk is the stigma and style of the maize (Zea mays), a cereal plant. Botanically, corn (maize) is classified under Poaceae (Gramineae) family and is considered a cereal, not a vegetable. Therefore, its extracts cannot be treated as “vegetable extracts” in the context of CTH 13021919 which applies to extracts derived from vegetables.

B. Proposed Classification under CTH 13021919: Heading 1302 19 19 refers to: “Vegetable saps and extracts: Other: Of other origin: Other” This heading is meant for extracts derived from vegetables, which corn is not. The product corn silk is not obtained from what is considered a vegetable in trade parlance or botanical classification. Hence, the product does not merit classification under CTH 13021919, and the benefit of notification No. 50/2017-Customs. (S1. No. 54) would not be admissible.

C. Appropriate Classification — CTH 13023990 (Other Plant Extracts): Heading 1302 39 90 refers to: “Vegetable saps and extracts: Other: Other: Other” This heading is broader and includes extracts of plant origin other than those specifically covered under vegetable saps/extracts. Since corn silk is of plant origin but not of vegetable origin, it may appropriately fall under this heading. Therefore, CTH 13023990 is a more accurate classification, as corn silk is a plant extract not classifiable under vegetable extracts. However, notification No. 50/2017-Customs (S1. No. 54) is not applicable to Heading 130239, and hence, exemption cannot be granted.

D. Alternate Classification — CTH 21069099 (Preparations for Nutrition/Supplementation): In the event the Corn Silk Extract Powder is a preparation containing added protein, flavour, or other constituents, and is marketed or intended for use as a nutritional supplement, it may be classifiable under Heading 2106, which covers: “Food preparations not elsewhere specified or included” Specifically, CTH 21069099 covers: “Other: Other: Other” — commonly used for nutritional supplements, health mixes, and protein-rich preparations. In such case, where the extract is not a pure extract but a formulated product, classification under 21069099 may be appropriate.

The Commissionerate concluded that in view of the above and based on the foregoing examination, they are of the considered view that:

i. The product Corn Silk Extract Powder is not derived from a vegetable in the context of Chapter Heading 13021919, and hence, the classification and exemption sought under CTH 13021919 read with notification No. 50/2017-Customs (S1. No. 54) is not admissible.

ii. If the product is imported in pure extract form (without additives), it is correctly classifiable under CTH 13023990 — plant extracts not elsewhere specified. However, this heading does not attract any exemption under the said Notification.

iii. If the product contains added proteins or is a formulated preparation intended for nutritional use, then it may merit classification under CTH 21069099. This heading also does not qualify for exemption under notification No. 50/2017-Customs

5. Rebuttal by the Applicant

5.1 The applicant vide email dated reiterated their claim for classification of “Com- Silk Extract Powder” under Customs Tariff Sub-heading 13021919, which, they stated, duty supported by the HSN Explanatory notes under Heading 13.02. As per the HSN explanatory notes under Heading 13.02, the said Heading covers Extracts obtained from parts of Plant by using Solvents, including water and the solid extract is obtained by evaporating the solvent. They submitted that “Corn Silk Extract” is clearly such Vegetable Extract. As evident from the Manufacturing process flow chart, the only process involved is of extraction by using Hot water as solvent and thereafter evaporating the water and spray drying. The said product therefore satisfies the criteria specified in the HSN notes under Heading 13.02. They further submitted that the Classification of Corn Silk Extract under Heading 13.02 is also supported by US Customs Ruling No. N241904 dated 4th June 2013, which is at page 16 of the Application.

5.1.1 The applicant further submitted that the contention of the Jurisdictional Commissionerate (Nhava Sheva Commissionerate) in Para 3 (1) of the said Reply dated 28-5-2025 that Corn Silk Extract powder stands excluded from Heading 13.02 in view of the following HSN Note is ex-facie erroneous:

“The heading also excludes vegetable extracts which have been mixed or compounded (without the addition or other substances) for therapeutic or prophylactic purposes. Such mixtures and similar medicinal compound extracts made by treating a mixture of plants, are classified in Heading 30.03 or 30.04. The latter heading also covers simple vegetable extracts (whether or not standardised or dissolved in airy solvent) when put up in measured doses for therapeutic or prophylactic purposes in forms or packings for retail sale for such purposes.” (Emphasis supplied).

5.1.2 The applicant submitted that the first portion of the above notes, which is relied upon by the Jurisdictional Commissionerate, applies to vegetable extracts which have been mixed or compounded for therapeutic or prophylactic purpose. It refers to mixtures or compounds made by treating mixture of plants. In the present case, Corn Silk Extract powder is an extract of a single plant and is not a mixture or compound of extracts of two or more plants. Further, the use of the same in manufacture of nutraceutical cannot be equated with therapeutic or prophylactic use. If the goods are mixture of compound of extracts for therapeutic or prophylactic use, the same fall under Headings 30.03 or 30.04 as per the said HSN notes.

5.1.3 The applicant submitted that the second part of the said HSN note, refers to simple vegetable extract when put up in measured doses for therapeutic or prophylactic purposes or in forms or packings for retail sale for such purpose and provides for their classification under Heading 30.04. The goods in the present case are not imported/ put up in measured doses for therapeutic or prophylactic purposes, nor are they in forms or packings for retail sale for such purpose.

5.1.4 The applicant submitted that the manufacturer’s flow chart does not show use of Ethanol as solvent and merely refers to Water as the solvent for extraction. They further submitted that even if ethanol is used as solvent, the same is permissible as per the HSN notes under Heading 13.02. The HSN notes clearly refer to alcohol (i.e Ethanol) as an example of solvent for extraction of Vegetable extracts falling under Heading 13.02. The applicant further submitted that once it is clear that Vegetable extract is specifically falling under Heading 13.02, it cannot be classified under the Residuary Heading 21.06 which covers “Food Preparations not elsewhere specified”. The applicant further submitted that the HSN Notes under Heading 13.02 makes it clear that Vegetable Extract by itself will not fall under Heading 21.06. Only when, because of addition of other substances to the Vegetable Extract, it acquires character of food preparation, it goes out of Heading 13.02 and falls under Heading 21.06. In the present case, the goods are simply Corn silk extract, to which no other substance is added. The HSN notes under Heading 13.02, Para A,,,(7)given example:–OrGinstig extract as falling under Heading 13.02. However, if ginseng is mixed with other ingredients such as lactose or glucose, it goes in 1-leading 21.06. Going by the said example, it would follow that since in the present case the goods arc only Corn Silk extract, without mixing or adding any other substance, it will be classifiable under Heading 13.02 and not under Heading 21.06.

5.2 The applicant vide email dated 20.08.2025 submitted that as per the HSN Explanatory Notes under Heading 13.02, Vegetable Extracts are extracts obtained by solvent extraction from the original vegetable material. It will be evident from the examples of Vegetable Extracts given in the HSN Notes that the term vegetable for purpose of Heading 13.02 is used in the broadest sense to cover various vegetable material such as:

a) Herbs, e.g. Opium, Liquorice, Cannabis, Ginseng, Aloe, Belladonna,

b) Flowers, e.g. Hops, Pyrethrum,

c) Leguminous Plant roots e.g. Derris

d) Shrubs, e.g. Quassia Amara,

e) Cereal, e.g. Rye,

f) Nuts, e.g. Cashew Nut shell extract, Cola (kola) nuts,

g) Berries e.g. Mistletoe Berries, Holly,

h) Spices e.g. Cassia,

i) Fruits e.g. Pawpaw.

5.2.1 The applicant submitted that in view of the aforesaid wide coverage of the term “Vegetable” in the HSN notes for the purpose of Heading 13.02, it is totally erroneous to contend that Extract from part of Corn is not Vegetable Extract since Corn is a Cereal. The example of extract from Rye (which is a Cereal) in HSN notes as Vegetable Extract clearly demonstrates that Extract from Cereal is Vegetable Extract for the purpose of Heading 13.02 and Sub-heading 1302 19 19. Further, the applicant submitted that in customs Tariff, “Vegetable Products” are covered by Section II of the Tariff, which covers Chapters 6 to 13. A perusal of these Chapters under Section II reveals that the coverage of Vegetable Products is so wide as to cover Plants, flowers, roots (Chapter 6), edible vegetables, roots, tubers (Chapter 7), Fruits and Nuts (Chapter 8), Coffee, Tea, Spices (Chapter 9), Cereals (Chapter 10), Flour of Cereals (Chapter 11) and Seeds, Fruits and Plant Parts (Chapter 12). It is therefore clear that any Extract obtained by solvent extraction from any of the products of Chapters 6 to 12 will be Vegetable Extract for the purpose of Heading 13.02 and Sub-Heading 1302 1919. The very fact that the Tariff itself covers Cereal and Cereal Flour under the Section of Vegetable Products demonstrates that Extract of Cereal Can be considered as Vegetable Extract for the purpose of Heading 13.02 and Sub-Heading 1302 19 19. Further, when the examples of Vegetable Extracts given in HSN Notes under Heading 13.02 are considered, it becomes amply clear that Vegetable Extracts for the purpose of Heading 13.02 are extracts obtained for various vegetable products/ material covered under Section II of the Tariff- Vegetable Products i.e. Plants, flowers, roots (Chapter 6), edible vegetables, roots, tubers (Chapter 7), Fruits and Nuts (Chapter 8), Coffee, Tea, Spices (Chapter 9), Cereals (Chapter 10) and Seeds, Fruits and Plant Parts (Chapter 12).

5.2.2 The applicant submitted that a bare perusal of Heading 13.02 and the HSN Notes for 13.02 show that Heading 13.02 is divided into three main parts (Three Single Dash (-) descriptions) as follows:

a) First Single dash Description is “Vegetable saps and extracts”,

b) Second Single Dash Description is ‘Pectic substances, pectinates and pectates- Subheading 1302 20 00 and

c) Third Single Dash Description is “Mucilages and thickeners, whether or not modified, derived from locust beans, locust seeds or guar seeds, Sub-heading 1302 32.

5.2.3 The applicant submitted that the Sub-heading 1302 39 90 is under the Third Single Dash Description viz. “Mucilages and thickeners, whether or not modified, derived from locust beans, locust seeds or guar seeds” – 1302 32. For any goods to fall under Sub-heading 1302 39 90, they must first answer the said single dash description of “Mucilages and thickeners, whether or not modified, derived from locust beans, locust seeds or guar seeds” – 1302 32. Corn Silk Extract is most certainly not Mucilage and Thickener derived from locust beans, locust seeds or guar seeds.

5.2.4 The applicant further submitted that since the Corn Silk Extract Powder proposed to be imported by the Applicant, does not have any added protein or other constituents, but is only an extract from Corn Silk, question of classification under Heading 2106 9099 does not arise.

5.2.5 The applicant, in summary, submitted as follows:

a) Corn Silk Extract is indeed a Vegetable Extract and rightly classifiable under Heading 13.02, Sub-Heading 1302 1919 and therefore eligible for the partial exemption from customs duty under Sr. No.54 of notification No. 50/2017-Customs

b) Corn Silk Extract is most certainly not classifiable under Sub-heading 1302 3990 because it does not answer the single dash (-) description of “Mucilages and thickeners, whether or not modified, derived from locust beans, locust seeds or guar seeds” – 1302 32 under which Sub-heading 1302 3990 falls and

c) since the Corn Silk Extract Powder proposed to be imported by the Applicant, does not have any added protein or other constituents, but is only an extract from Corn Silk, question of classification under Heading 2106 9099 does not arise.

5.2.6 The applicant submitted that the Corn Silk Extract Powder is classifiable under CTSH 1302 19 19 and is eligible for partial exemption from customs duty under Sr. No.54 of notification No. 50/2017-Customs, dated the 30th June, 2017

6. Records of Personal Hearing

6.1 A personal hearing was held on 08.07.2025 at 11:30 AM in the office of the CAAR, Mumbai. Shri J. C. Patel, Advocate (AR); Shri Abhishek Sakharkar, Manager — Purchase and Shri Mahendra Chikhale, Assistant Manager — Logistics, both from Gangwal Healthcare Private Limited appeared for the personal hearing on behalf of the applicant. They had already requested for hearing in physical mode to explain the process in person, which was permitted considering the nature of process of extraction of the subject goods. They contended that the subject goods i.e. Corn Silk Extract Powder which are extracted from the “Style and Stigma” part of Zea Mays L (Corn) by using hot water as the solvent for extraction and that it merits classification under CTH 1302 and more specifically under Tariff Item 1302 19 19 (other). They relied upon the description of CTH 1302 in as much as it is very specific that covers Vegetable Saps and Extracts; and the subject import good is truly extract of vegetable and that there is no carrier or additive is added. They also relied upon the Cross Ruling N241904 dated 04.06.2013 on the identical goods. They rebutted the contention of the department (NS-I). On specifically asked about the constituents / ingredients / nutrients / micronutrients etc. in the subject extract and the function of the product in the final product as such, they sought two days’ time to submit the same.

Noone appeared for the hearing from the departments side.

6.2 The applicant vides their email dated 20.08.2025 requested for another personal hearing to be granted to enable them to explain the submissions made by them in resporisv,z13.7.„ nts received from the department. The request was granted.

6.3 Another personal hearing was held on 25.08.2025 at 12:30 PM in the office of the CAAR Mumbai. Shri J. C. Pate( Advocate appeared for the Personal Hearing in the matter on behalf of the applicant, in continuation of earlier hearing dated 08.07.2025. He reiterated the contention made in the application that the subject goods i.e. “Corn Silk Extract Powder” which is extracted and dried from the style and stigma part of Corn Plant, merit classification under CTH 1302 19 19. He rebutted the reply filed by the department vide submission dated 20.08.2025. He submitted that the product contains Carbohydrates, Proteins, and Minerals with Natural Oxidants such as Polyphenols and Flavonoids and is used as ingredient only in further manufacturing; that the CTH 1302 covers broader group of vegetable saps and extracts and attract a wide range of plant and vegetable products. He stressed that solid extract which are obtained by evaporating the solvents are generally covered in the said CTH 1302. He also referred to the reply filed on 08.07.2025.

Nobody appeared for hearing from the department side.

7. Discussions and Findings

7.1 I have considered all the materials placed before me in respect of the classification of subject goods. I have gone through the submissions made by the applicant during the personal hearing, additional submissions as well as the comments received from the concerned jurisdictional commissionerate and the rebuttal of the same by the applicant. Therefore, I proceed to pronounce a ruling on the basis of information available on record as well as existing legal framework.

7.2 The applicant has sought advance ruling in respect of the classification of the subject goods i.e. “Corn Silk Extract Powder” and applicability of exemption under Sr. No. 54 of notification No. 50/2017-Customs, dated the 30th June, 2017

7.3 At the outset, I find that the issue raised at the Sr. No. 08 in the CAAR-1 form is squarely covered under Section 28H(2) of the Customs Act, 1962 being a matter related to the classification of goods. Further, I find that Section 28E (c) defines the ‘Applicant’ as any person holding a valid Importer-exporter Code Number granted under section 7 of the Foreign Trade (Development and Regulation) Act, 1992; or exporting any goods to India; or with a justifiable cause to the satisfaction of the Authority, who makes an application for advance ruling under Section 28H. In this matter, the applicant holds a valid Importer-exporter Code Number, thereby satisfies one of the criterions mentioned under the definition of the Applicant under Section 28E and therefore, is a valid applicant for filing application under Section 28H of the Customs Act, 1962.

7.4 The applicant is seeking an advance ruling for the classification of the subject goods i.e. “Corn Silk Extract Powder”. The applicant has submitted that the subject goods i.e. Corn Silk Extract Powder is obtained by extraction from the “Style and Stigma” parts of the Plant having the botanical name “Zea Mays L”, commonly known as “Corn” by Water extraction, using hot water as the Solvent for extraction. The water is thereafter evaporated to obtain the solid, which is spray dried to obtain the powder, which is 100% Corn Silk Extract in powder form. The applicant further submitted that the subject goods i.e. “Corn Silk Extract Powder” is used as an ingredient/ raw material in the manufacture of Nutritional Supplement.

7.5 Before deciding on the issue, let me deliberate on the legal framework prescribed in Customs Tariff Act, 1975, Chapter/Section notes along with HSN explanatory notes. Classification of goods in the Harmonized System of Nomenclature (HSN) is governed by the General Rules for the interpretations. Rule 1 of the General Rules for the Interpretation of the Import Tariff to the Customs Tariff Act, 1975 stipulate that for legal purposes, the classification of the import item shall be determined acc9rding to the terms of the headings and any relative Section or Notes.

7.6 In this regard, I find that the applicant has suggested Heading 1302 for the classification and the department has suggested heading 2106 for the classification of the subject goods. Relevant heading text for both the headings i.e. 1302 and 2106 is as under:

| Heading | Heading Text |

| 1302 | Vegetable saps and extracts; pectic substances, pecti nate s and pectates; agar-agar and other mucilages and thickeners, whether or not modified, derived from vegetable products |

| 2106 | Food preparations not elsewhere specified or included |

7.7 The heading 1302 covers vegetable saps and extracts whereas heading 2106 is a residuary heading covering all the food preparations not elsewhere specified or included. The subject goods i.e. Corn Silk Extract Powder are an extract from Zea mays stigmas, containing flavonoids, phenolic acids, polysaccharides, etc., and used for diuretic/antioxidant and related purposes in supplements or herbal teas. Further, as per applicant’s submission, it is produced by water extraction using hot water as solvent and nothing else is added into the subject goods. Since the Heading 1302 covers vegetable saps and extracts, and the subject goods under consideration is also of plant / vegetable origin, it is necessary to examine the relevant Chapter Notes and HSN Explanatory Notes for heading 1302, the same are as under:

Chapter Note 1 of Chapter 13:

“1.- Heading 13.02 applies, inter alia, to Liquorice extract and extract of pyrethrum, extract of hops, extract of aloes and opium.

The heading does not apply to :

(a) Liquorice extract containing more than 10% by Inveigh of sucrose or put up as confectionery (heading 17.04);

(b) Malt extract (heading 19.01);

(c) Extracts of coffee, tea or mate (heading 21.01);

(d) Vegetable saps or extracts constituting alcoholic beverages (Chapter 22);

(e) Camphor, glycyrrhizin or other products of heading 29.14 or 29.38;

(f) Concentrates of poppy straw containing not less than 50 % by weight of alkaloids (heading 29.39);

(g) Medicaments of heading 30.03 or 30.04 or blood-grouping reagents (heading 38.22);

(h) Tanning or dyeing extracts (heading 32.01 or 32.03);

(ij) Essential oils, concretes, absolutes, resinoids, extracted oleoresins, aqueous distillates or aqueous solutions of essential oils or preparations based on odoriferous substances of a kind used for the manufacture of beverages (Chapter 33); or

(k) Natural rubber, balata, gutta-percha, guayule, chicle or similar natural gums (heading 40.01 ).”

Relevant HSN Explanatory Notes for Heading 1302:

7.8 Chapter Note 1 to Chapter 13 mentions exclusions from heading 1302. I have gone through the exclusions mentioned there and have found that the subject goods are not excluded from the heading by the application of Chapter Note 1 of Chapter 13. Exclusions include malt extract (19.01), coffee/tea extracts (21.01), alcoholic beverages (Ch. 22), and medicaments of Chapter 30. Chapter Note 1 to Chapter 13 excludes medicaments of 3003/3004. However, Explanatory Notes to 3003/3004 make clear that “simple vegetable extracts (whether or not standardised or dissolved in solvent) remain under Heading 1302 unless they are mixed or compounded for therapeutic or prophylactic purposes, or put up in measured doses or retail packs for such purposes.” i.e. simple vegetable extracts remain in Heading 1302 unless they are put up in measured doses or are in forms or packings for retail sale for therapeutic purposes. As the subject goods are imported in bulk, it fails to meet this critical “put-up” condition and cannot be considered a medicament classifiable under heading 3003 or 3004.

7.9 Further, on-going through the Explanatory Notes for heading 1302 (as mentioned above), I observed that this heading covers extract which are vegetable products extracted from the original vegetable material by solvents. The Explanatory notes further allow the addition of certain inert substances to certain extracts to more easily reduce them to powder or to obtain a standard strength without changing their classification. However, the Explanatory notes make it clear that addition of additional extraction cycles or purification process which increase or decrease certain compounds or compound classes to a degree that cannot be achieved solely by means of initial solvent extraction, would render the goods out of purview of the heading 13.02. The Explanatory Notes further states that the products falling under this heading are generally raw materials for various manufactured products and they would be excluded from this heading if addition of other substances changes their character to food preparations, medicaments etc. Further, I also observe from the list of examples given in the Explanatory Notes for the products covered under this heading that it covers extracts obtained from various parts of plants such as roots, flowers, leaves barks etc. and is not limited to the term “Vegetable” as used in common parlance.

7.10 From the above, I gather that to be able to classifiable under heading 1302, the product should be of plant / vegetable origin, a raw material and only in the form as initially extracted and not further chemically purified. I find that in the instant case; the goods are of plant / vegetable origin as these are made from a part (styles /stigma) of the plant (Zea mays); are imported in bulk and are raw material which would be further used to manufacture other products (as per the applicant’s submission). Further, based on the manufacturing process submitted by the applicant, I observe that the goods are as initially extracted and no further extraction or purification process has been carried out on the goods; neither it has been mixed or compounded for therapeutic or prophylactic purposes.

7.11 The subject goods, as per the submissions made by the applicant, are a simple extract from a sin le plant source, obtained through an in–it–omsxtr and are not subjected to further purification or chemical modification. Therefore, it can be said that the subject goods are plainly of plant origin produced by a permitted extraction method, and presented as a bulk raw material without chemical modification. They are therefore squarely within the scope of Heading 1302. In view of the above, I find that the subject goods satisfy all the conditions laid out by the HSN Explanatory Notes for classification under Heading 1302 and therefore, can be classified under Heading 1302.

7.12 Further, I find that Heading 2106 is a residual heading which refers to food preparations for human consumption directly or after basic processing such as cooking, dissolving or boiling in water, milk etc. The Explanatory Notes illustrate that it covers formulated food preparations and dietary supplements presented in measured doses. Since the subject goods as per the submissions made by the applicant, are a single-ingredient raw material used for manufacturing nutritional supplement, and is not a finished preparation, as such classification under 2106 is ruled out. The principle of specificity (GM 3(a)) also dictates that a product specifically describedi dot be placed in the residuary heading 2106. As Heading 1302 provides a more specific description, classification under the residual Heading 2106 is ruled out by GRI 3(a).

7.13 Further, in the matter of Cachet Pharmaceuticals (P) Ltd. v. Commr. of Customs, New Delhi, the Tribunal in its Final Order No. C/A/55016/2017-CU(DB) in Appeal No. C/53062/2015(DB) held that a plant extract, even in tablet or powder form, should be classified under heading 1302 and not under 2106, as long as the product remains a pure extract with minimal non-active binder and is not a composite preparation. The tribunal found that food supplements or health products based predominantly on vegetable extracts, when not blended or processed as food preparations, should remain within heading 1302.

7.14 In view of the above, I conclude that the subject goods are classifiable under Heading 1302. The relevant excerpts of the Heading 1302 are as under:

| Tariff Item | Description of goods |

| 1302 | Vegetable saps and extracts; pectic substances, pectinates and pectates, agar-agar and other mucilages and thickeners, whether or not modified, derived from vegetable products -Vegetable saps and extracts : |

| 1302 11 00 | — Opium |

| 1302 12 00 | — Of liquorice |

| 1302 13 00 | — Of hops |

| 1302 14 00 | –– Of ephedra |

| 1302 19 | — Other |

| —Extracts : | |

| 1302 19 11 | — Of belladonna |

| 1302 19 12 | —- Of cascara sagrada |

| 1302 19 13 | –— Of nuxvomica |

| 1302 19 14 | —- Of ginseng (including powder) |

| 1302 19 15 | —- Of agarose |

| 1302 19 16 | —- Of neem |

| 1302 19 17 | –— Of gymnema |

| 1302 19 18 | — Of garcinia and gamboge |

| 1302 19 19 | —- Other |

From the above, I find that since goods are extracts of styles and stigma of corn plant, these are more precisely classifiable under CTI 1302 19 19 i.e. Vegetable saps and extracts: — Other : —Extracts : Other.

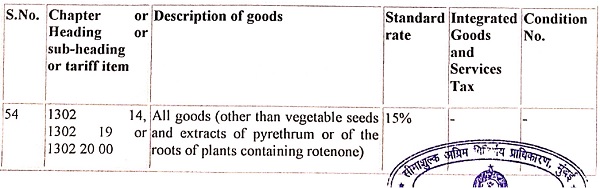

7.15 Applicability of exemption benefit under Sr. No. 54 of notification No. 50/2017-Customs, dated the 30th June, 2017 : The relevant excerpts of the said notification are as under:

7.16 From the above, it is observed that the exemption is available to all the goods classifiable under Heading 1302 14, 1302 19 or 1302 20 00 except vegetable seeds and extracts of pyrethrum or of the roots of plants containing rotenone. Since the subject goods are classifiable under CTSH 1302 19 and are not mentioned as the exceptions, therefore, the exemption benefit under Sr. No. 54 of the notification No. 50/2017-Customs, dated the 30th June, 2017 is applicable for the subject goods.

8. In light of the above facts, discussions and observations, I am of the view that the subject goods i.e. Corn Silk Extract Powder is classifiable under CTI 1302 19 19 as these are of plant / vegetable origin; are raw material used for further manufacturing nutritional supplements and are in the form as initially extracted (not have been further subjected to additional extraction or chemical purification). Further, the subject goods i.e. Corn Silk Extract Powder are eligible to claim exemption benefit under Sr. No. 54 of the notification No. 50/2017-Customs, dated the 30th June, 2017

9. I rule accordingly.

Author Bio